- Telecommunications

- Industrial Router Market

Industrial Router Market Size, Share, and Growth Forecast 2026 – 2033

Industrial Router Market by Product Type (Wired Industrial Routers, Wireless Industrial Routers), by Enterprise Size (SME, Large), by End-user Industry (Manufacturing, Energy, Oil & Gas, Pharmaceuticals), and Regional Analysis 2026 – 2033

Industrial Router Market Share, Size, and Trends Analysis

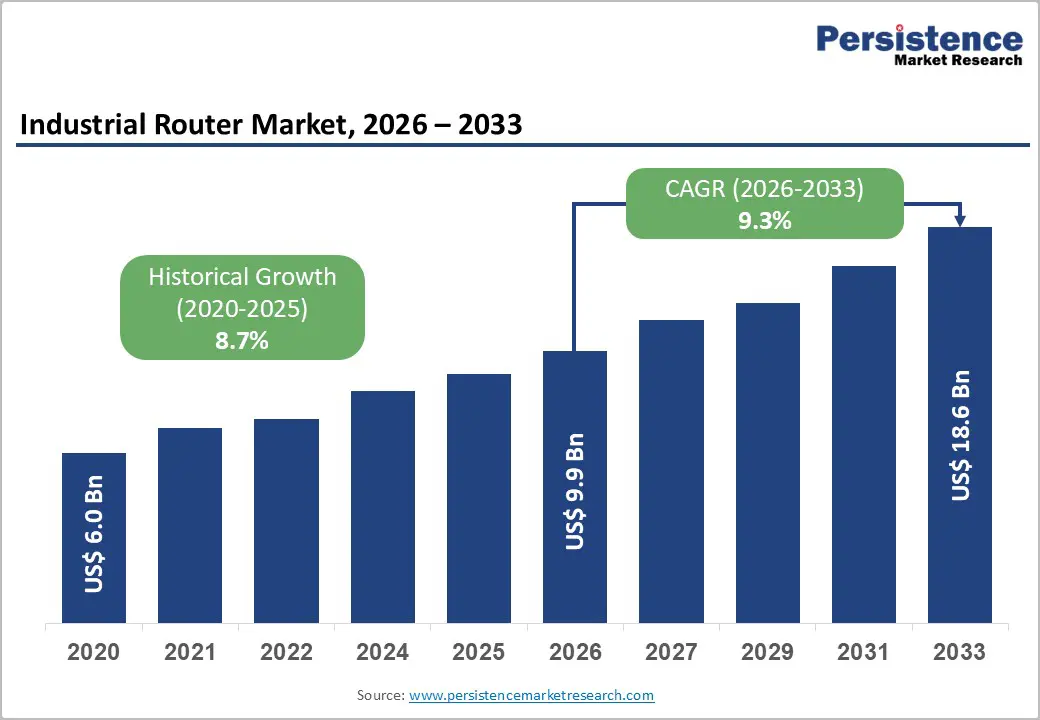

The global industrial router market size is projected to be valued at US$9.9 billion in 2026 and is projected to reach US$18.6 billion by 2033, growing at a CAGR of 9.3% during the forecast period from 2026 to 2033, driven by the acceleration of Industry 4.0 and the critical integration of Operational Technology (OT) with Information Technology (IT). While legacy wired infrastructure remains foundational, the rapid deployment of private 5G networks and edge computing capabilities is reshaping the investment landscape, shifting focus toward wireless, ruggedized intelligent gateways. The market has demonstrated consistent expansion, thereby validating the strong underlying demand fundamentals driving this market expansion during the forecast period.

Key Industry Highlights:

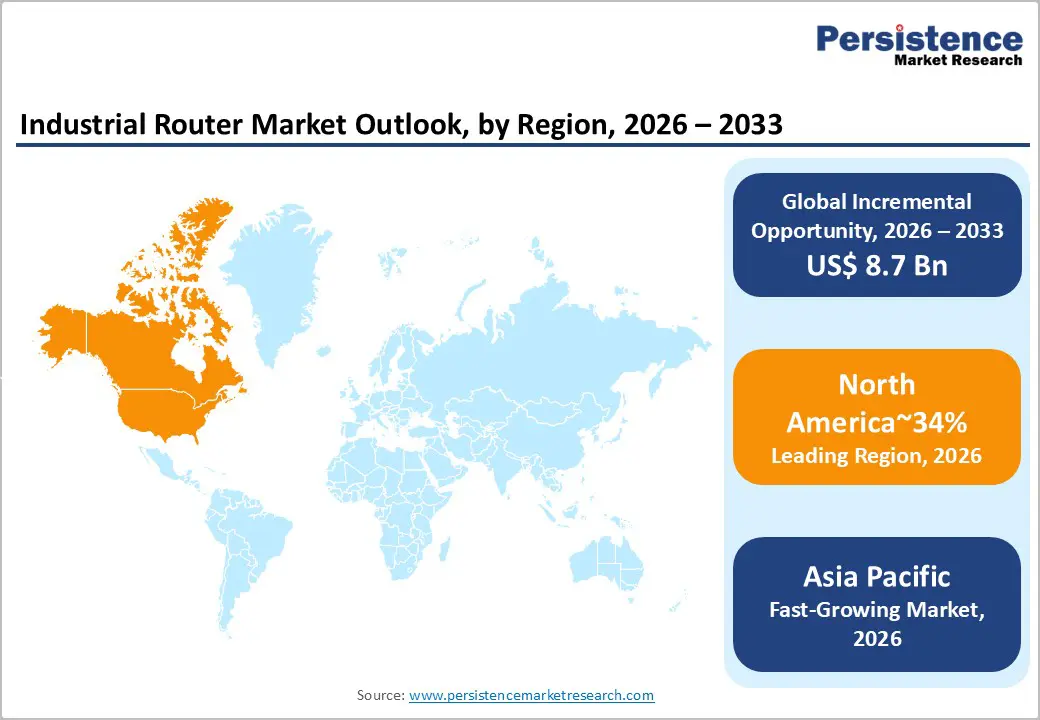

- Leading Region: North America, with a 34% share, driven by early adoption, a strong automation vendor presence, and ongoing investments in high-reliability solutions for utilities, transportation, and critical infrastructure.

- Fastest-growing Region: Asia Pacific, due to industrial growth, policy support, and adoption across sectors. Key countries are expected to drive adoption through manufacturing scale, electronics and energy demand, and infrastructure initiatives.

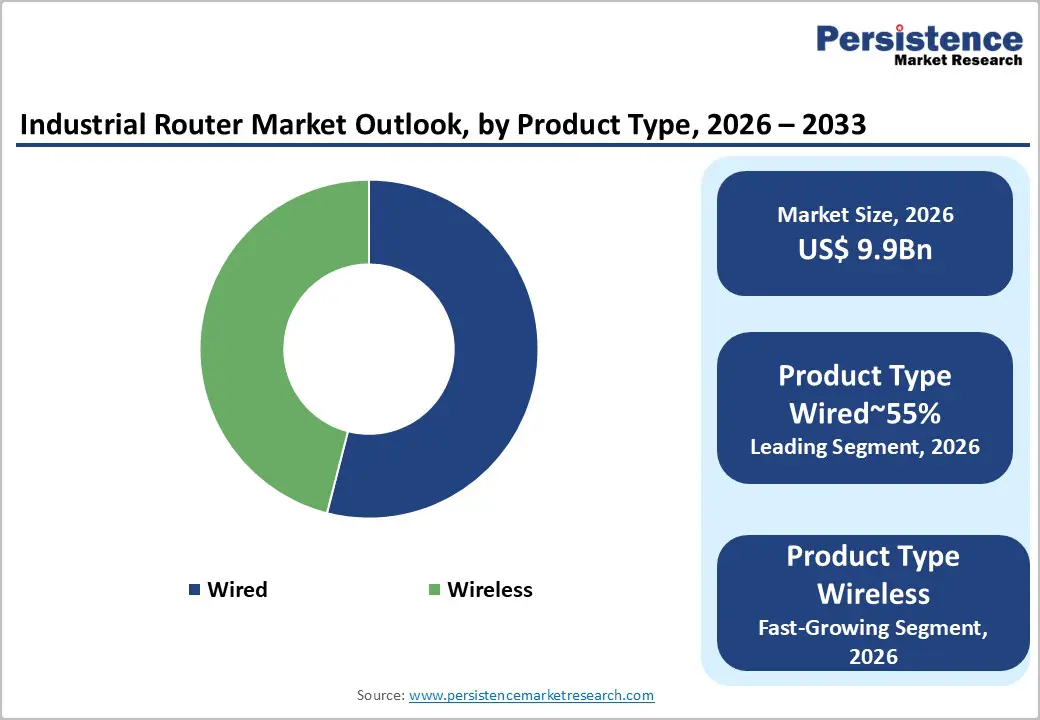

- Leading Product Type: Wired industrial routers, to lead accounting for approximately 55% share through industrial adoption, throughput, quality, and high-value applications.

- Leading Enterprise Size: Large enterprises, to dominate for simplicity, cost, adoption, and functional use across key sectors, holding approximately 65% share.

- Key Industry Developments: Key developments in the market include consolidation through acquisitions, industrial 5G expansion, and compliance with IEC 62443 standards, with Nokia launching ruggedized Industrial 5G routers in March 2025, supporting AI and ML for enhanced machine insights and productivity.

| Report Attribute | Details |

|---|---|

|

Industrial Router Market Size (2026E) |

US$9.9 Bn |

|

Market Value Forecast (2033F) |

US$18.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

5G Industrial Deployments and Edge Computing Integration

The rollout of industrial-grade private 5G networks is creating a structural demand driver for advanced industrial routers. Nonpublic 5G deployments enable ultra-reliable, low-latency communication required for mission-critical operations. Applications such as remote equipment control, autonomous vehicle coordination, and real-time inspection depend on deterministic network performance. This shifts connectivity from best effort communication toward guaranteed service delivery. Industrial routers, therefore, evolve into core control infrastructure rather than peripheral networking devices. Enterprises increasingly treat router upgrades as foundational investments within broader digital transformation programs.

Edge computing integration further amplifies this demand by decentralizing processing closer to operational assets. Distributed architectures require routers with embedded compute, container orchestration, and multi-access edge support. Manufacturing, energy, logistics, and mining environments are replacing legacy Wi-Fi and LTE gateways to support dense device connectivity and real-time control. Autonomous mobile robots and guided vehicles benefit directly from low-latency coordination. This refresh cycle favors ruggedized routers capable of handling compute, security, and routing simultaneously. As private 5G scales, router functionality converges with edge intelligence across industrial networks.

Ring Topology Redundancy Protocol Limitations (MRP, PRP, HSR)

The limitations of ring topology redundancy protocols hinder the widespread adoption of industrial routers in mission-critical networks. Industrial environments, which rely on ring architectures, require failover times under 20 milliseconds to protect motion control and safety systems. However, standard IP routing protocols cannot meet these fast recovery requirements due to slower convergence, limiting their use in latency-sensitive industrial control networks. This incompatibility makes it challenging for enterprises to integrate operational technology networks with corporate IP infrastructure.

Native support for industrial redundancy protocols is limited across router platforms, with only a small percentage of industrial routers offering hardware-level integration of protocols lsuch as Media Redundancy, Parallel Redundancy, or Seamless Redundancy. To maintain deterministic performance, organizations often operate parallel industrial Ethernet networks. Implementing these protocols demands custom ASIC development, which incurs high upfront engineering costs and long development timelines, delaying platform updates and innovation. This situation creates barriers to entry, benefiting established vendors with specialized expertise in industrial networking.

Integration of Edge Computing

The integration of edge computing capabilities into industrial routers is creating a distinct growth opportunity within industrial networking markets. Edge routers move data processing closer to machines, sensors, and operational assets. Local analytics reduce reliance on centralized cloud infrastructure and lower data transmission intensity. This architecture improves response times for latency-sensitive industrial applications. Real-time filtering and preprocessing enable faster decision-making at the network edge. These capabilities are increasingly critical for automation, robotics, and continuous asset monitoring environments.

This convergence is particularly valuable in remote and bandwidth-constrained sectors. Industries such as oil and gas benefit from reduced backhaul dependency and improved operational resilience. Edge-enabled routers support containerized workloads, allowing deployment of analytics and AI models locally. This expands router functionality beyond connectivity into operational intelligence. Vendors offering platforms with native container support and compute scalability gain a strategic advantage. As edge architectures mature, routers evolve into core infrastructure for distributed industrial intelligence. In February 2024, Digi International launched the Digi IX40, a 5G edge computing industrial IoT cellular router. The router supports Industry 4.0 applications like advanced robotics and asset monitoring, offering rapid data processing and integration to boost efficiency and predictive maintenance in factories.

Category–wise Analysis

Product Type Insights

Wired industrial routers are projected to lead the industrial router market, accounting for approximately 55% share in 2026, underpinned by superior reliability, deterministic performance, and immunity to electromagnetic interference across manufacturing, logistics, and transportation operations. Adoption remains anchored by high security, signal stability, and predictable latency, with enterprises prioritizing standardized deployments, long asset lifecycles, and integration with legacy control systems in mission-critical environments. Ongoing platform evolution, including multi-port high-density designs, edge computing, and enhanced cybersecurity protocols, continues to reinforce replacement cycles and operational continuity. Vendors such as Cisco Systems, Siemens, ABB, and Rockwell Automation are expanding portfolios with integrated networking solutions to lock in enterprise workflows and long-term service contracts. This combination of mature infrastructure, ecosystem lock-in, and predictable demand sustains the segment’s dominance across structured industrial deployments.

Wireless industrial routers are anticipated to be the fastest-growing, driven by the integration of Industrial 5G, Industry 4.0 adoption, and the need for flexible, mobile production floor connectivity. Growth is being catalyzed by edge computing, ultra-low latency performance for autonomous robotics, and hybrid multi-service platforms that reduce cloud dependency, materially improving responsiveness, scalability, and operational efficiency. Accelerating adoption is supported by tri-band router architectures, private 5G networks, and modular deployment models, lowering technical barriers for first-time adopters. Companies including Cisco Systems, Siemens AG, Advantech, and Huawei are scaling compact 4G/5G and Wi-Fi 6/6E solutions to capture emerging demand. As wireless infrastructure matures and mobile production scenarios expand, this segment is expected to outpace overall market growth through 2032.

Enterprise Size Insights

Large enterprises are projected to lead the Industrial IoT (IIoT) and 5G router market, accounting for approximately 65% share in 2026, underpinned by the sheer scale of their infrastructure, legacy modernization budgets, and the ability to absorb high first-mover costs across mining, oil & gas, and multi-site manufacturing operations. Adoption remains anchored by high-throughput, low-latency performance, and deterministic connectivity, with enterprises prioritizing standardization, global certifications, and secure IT/OT integration in complex networks. Ongoing platform evolution, including private 5G networks, edge AI processing, and RedCap integration, continues to reinforce replacement cycles and utilization intensity. Vendors such as Casa Systems, Cisco, and Cradlepoint are expanding portfolios with secure, cloud-managed routers to lock in enterprise workflows and long-term service contracts. This combination of mature infrastructure, ecosystem lock-in, and predictable demand sustains the segment’s dominance within structured deployment models.

Small and Medium Enterprises (SMEs) are anticipated to be the fastest-growing segment within the Industrial IoT (IIoT) and 5G router market, driven by the transition of 5G from a high-cost experimental technology to an affordable, standardized utility across small-scale factories, workshops, and supplier networks. Growth is being catalyzed by plug-and-play “5G-in-a-box” solutions, cloud-managed AI integration, and hybrid connectivity that materially improve operational efficiency, automation, and real-time monitoring. Accelerating adoption is supported by network-as-a-service models, government subsidies, and simplified no-code router interfaces, lowering operational friction for first-time adopters. Companies, including Teltonika Networks, Peplink, and Robustel, are scaling cost-effective platforms to capture early-cycle demand and embed switching costs. As SME familiarity, regulatory clarity, and affordable 5G hardware improve, this segment is expected to outpace overall market growth over the forecast period.

Regional Insights

North America Industrial Router Market Trends

North America is expected to lead, accounting for approximately 34% of the market share, supported by early IIoT adoption, advanced industrial automation, and robust regulatory frameworks governing critical infrastructure. Growth is reinforced by the reshoring of manufacturing, smart grid modernization, and extensive investments in digital industrial ecosystems. Market leadership is reinforced by sustained investments in smart manufacturing, grid modernization, and secure industrial communications across utilities, transportation, and defense-linked sectors. Regulatory standards such as NERC CIP, CISA guidance, and ISA/IEC 62443 drive consistent demand for high-reliability, security-certified routing solutions. Enterprises in the region prioritize resilience, uptime, and compliance, resulting in higher per-facility spending on industrial networking equipment. The presence of established vendors and system integrators fosters a competitive yet relatively consolidated ecosystem focused on integrated IT/OT architectures and secure edge connectivity.

The U.S. dominates the North American market, driven by large-scale manufacturing reshoring and semiconductor capacity expansion supported by federal industrial policy initiatives. New fabs, automation-heavy plants, and logistics hubs require hardened, FIPS-compliant routers for mission-critical operations. Vendor competition centers on cloud-managed industrial routers, edge computing capabilities, and security by design architectures, positioning North America as both the largest revenue contributor and a technology benchmark region.

Europe Industrial Router Market Trends

Europe constitutes a structurally advanced and regulation-driven industrial router market, underpinned by strong manufacturing depth and digital standardization across core economies. The region’s market development is shaped by stringent quality benchmarks, deterministic network performance requirements, and integrated IT/OT architectures across industrial operations. EU-wide regulatory frameworks such as NIS2, DORA, and GDPR materially influence procurement decisions, elevating demand for secure, compliant, and audit-ready industrial routing solutions. European manufacturers prioritize reliability, lifecycle traceability, and data sovereignty, favoring vendors capable of supporting localized data processing and standardized industrial communication protocols. This regulatory coherence supports cross-border deployments while reinforcing Europe’s positioning as a premium, compliance-centric market rather than a purely volume-driven one.

Germany dominates the European industrial router landscape, driven by its leadership in industrial automation and Industry 4.0 implementation. Strong coordination between manufacturing firms, research institutions such as Fraunhofer, and industry bodies such as VDMA accelerates the adoption of advanced networking solutions across automotive, machinery, and process industries. Secondary markets, including the U.K. and France, show differentiated demand patterns linked to infrastructure modernization and regulated industrial sectors. Regional investment focus centers on secure industrial IoT platforms, digital twins, and advanced manufacturing clusters, particularly across Central and Eastern Europe.

Asia Pacific Industrial Router Market Trends

Asia Pacific is likely to be the fastest-growing industrial router market globally, supported by large-scale manufacturing expansion and industrial capacity migration from developed economies. The region’s growth trajectory is anchored in rising factory automation, expanding industrial IoT deployments, and sustained investments in electronics, automotive, energy, and process manufacturing. Government-led industrialization programs, infrastructure digitization, and greenfield manufacturing projects across emerging economies continue to strengthen demand for secure, high-reliability industrial networking solutions. Unlike mature Western markets, Asia Pacific combines scale-driven deployment with rapid technology catch-up, positioning it as the primary volume growth engine for industrial routers.

China, Japan, and India anchor regional demand with distinct structural drivers. China leads through large-scale manufacturing ecosystems, renewable energy infrastructure expansion, and state-backed industrial modernization initiatives. Japan’s dominance in automotive, robotics, and precision manufacturing sustains demand for high-performance, low-latency industrial routers. India is emerging as a critical growth contributor, driven by electronics, pharmaceuticals, and automotive manufacturing expansion under national incentive programs. Southeast Asian economies such as Vietnam, Thailand, and Malaysia further reinforce regional momentum through new industrial parks and export-oriented manufacturing investments.

Competitive Analysis

The global industrial router market is moderately consolidated, with the top four vendors, Cisco Systems, Siemens Industrial Edge, HMS Networks, and Huawei, commanding approximately 52% of the total market value. Leading players maintain dominance through integrated IT/OT portfolios, robust partner ecosystems, and established relationships across manufacturing, energy, and transportation verticals.

Cisco launched the Catalyst IR1800 series for harsh manufacturing environments, supporting AI-driven predictive maintenance. Siemens partnered with NVIDIA to embed CUDA-based edge AI in Scalance routers, enabling autonomous network optimization. Hirschfeld Electronics acquired NetComm Wireless to expand 5G industrial connectivity in Asia Pacific. HMS Networks strengthened its global position through acquisitions of Red Lion Controls and Molex Industrial Communications, while Digi International launched the Digi IX40 5G edge router, targeting predictive maintenance and advanced robotics, reflecting a competitive focus on end-to-end IIoT solutions.

Key Industry Developments:

- In July 2025, Lantronix launched the NTC-500 Series rugged industrial-grade 5G wireless router. This affordable, award-winning series disrupts industrial connectivity by enabling next-gen mobility and real-time insights, leading to improved ROI through efficient edge AI deployment.

- In February 2024, Semtech launched the AirLink XR60, claimed as the world's smallest rugged 5G router. Designed for industrial and smart city applications, it offers compact, high-speed connectivity with GPS, reducing deployment costs and enabling scalable IoT networks in space-constrained environments.

- In January 2024, Casa Systems unveiled the AurusXT 5G Industrial IoT Router Series featuring the NTC-500 5G IIoT router. This launch provides high-performance, rugged 5G connectivity tailored for industrial environments, enabling seamless IIoT integration and reducing downtime through reliable remote operations.

Companies Covered in Industrial Router Market

- Cisco Systems

- Siemens

- Huawei Technologies

- HMS Networks

- Digi International

- Advantech

- Moxa

- Teltonika Networks

- Sierra Wireless

- Juniper Networks

- Belden

- Ericsson

- Nokia

- Westermo

- Phoenix Contact

Frequently Asked Questions

The global industrial router market is projected to be valued at US$9.9 billion in 2026 and is expected to reach US$18.6 billion by 2033, reflecting the accelerating integration of Operational Technology (OT) with Information Technology (IT) under Industry 4.0 initiatives.

Demand is rising due to enterprise-wide digital transformation, the rollout of private 5G networks for mission-critical communication, integration of edge computing capabilities, and the growing need for secure, low-latency networking to support automation and smart infrastructure.

The industrial router market is expected to grow at a CAGR of 9.3% between 2026 and 2033, supported by the expansion of industrial IoT (IIoT), smart manufacturing, and the deployment of advanced cellular connectivity.

The fastest growth opportunities are emerging in Asia Pacific, driven by large-scale manufacturing expansion, government-led industrial incentive programs, rapid factory automation, and significant investments in new energy and electronics production capacity.

Key players include Cisco Systems, Siemens, HMS Networks, Huawei Technologies, Digi International, Advantech, Moxa, Teltonika Networks, Sierra Wireless, Juniper Networks, Belden, Ericsson, Nokia, Westermo, and Phoenix Contact.