- Specialty & Fine Chemicals

- Industrial Lubricants Market

Industrial Lubricants Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Industrial Lubricants Market by Product Type (Process Oils, Hydraulic Fluids, Metalworking Fluids, Compressor Oil, Turbine Oil, Gear Oil, Grease, Others), Grade (Mineral Oil, Synthetic Oil, Bio-based Oil), Industry (Oil & Gas, Construction, Metal & Mining, Power Generation, Chemical Production, Textile Manufacturing, Food Processing, Agriculture, Marine Applications, Others), by Regional Analysis, 2025 - 2032

Industrial Lubricants Market Size and Trend Analysis

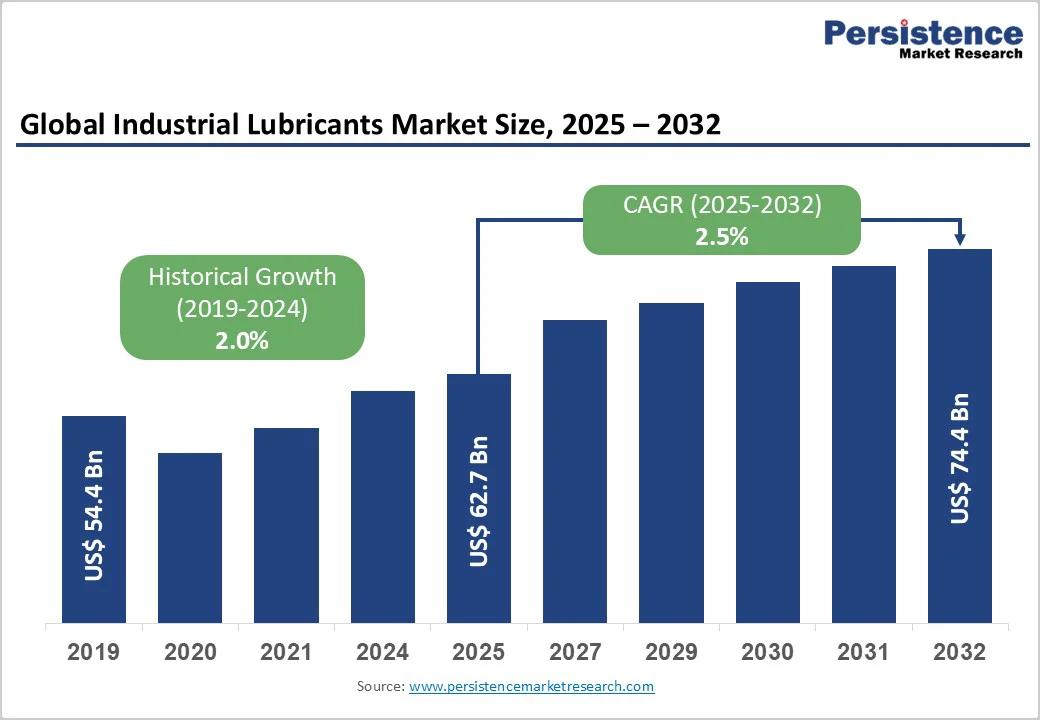

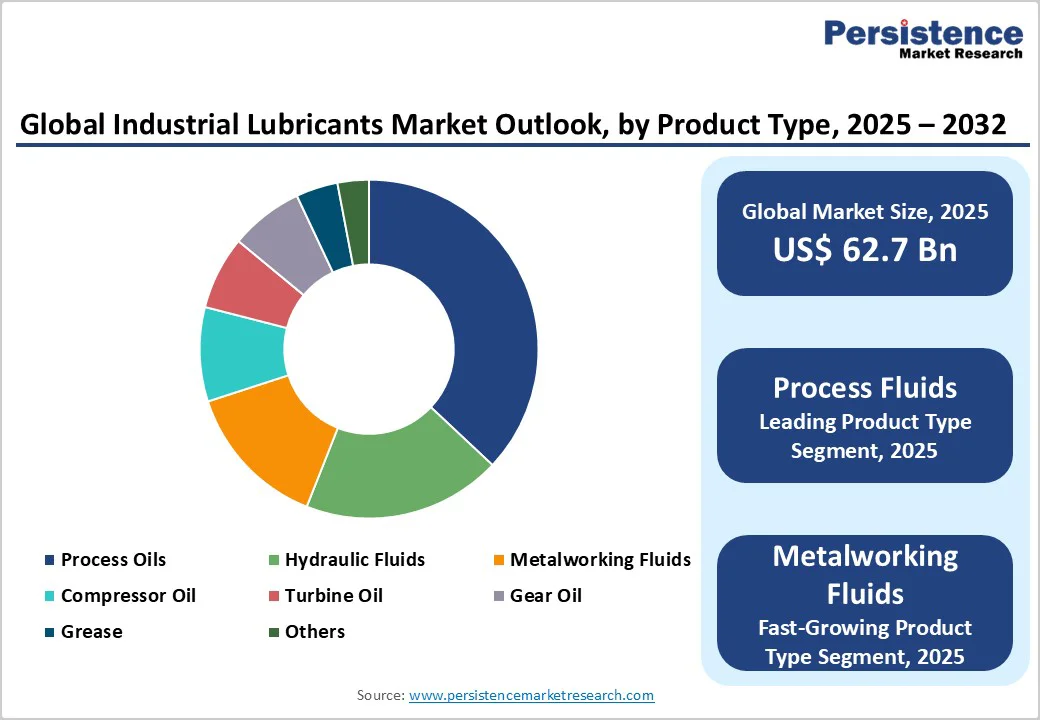

The global industrial lubricants market size is valued at US$62.7 billion in 2025 and is expected to reach US$74.5 billion, growing at a CAGR of 2.5% between 2025 and 2032.

Market expansion is driven by rising machinery automation, industrialization, and the demand for high-performance lubricants that enhance efficiency and equipment durability. Increasing adoption of advanced manufacturing technologies and expansion across emerging economies further fuel growth.

Additionally, heightened environmental awareness and regulatory pressure are boosting the shift toward sustainable, bio-based, and synthetic lubricants, offering superior performance and compliance with ecological standards.

Key Market Highlights

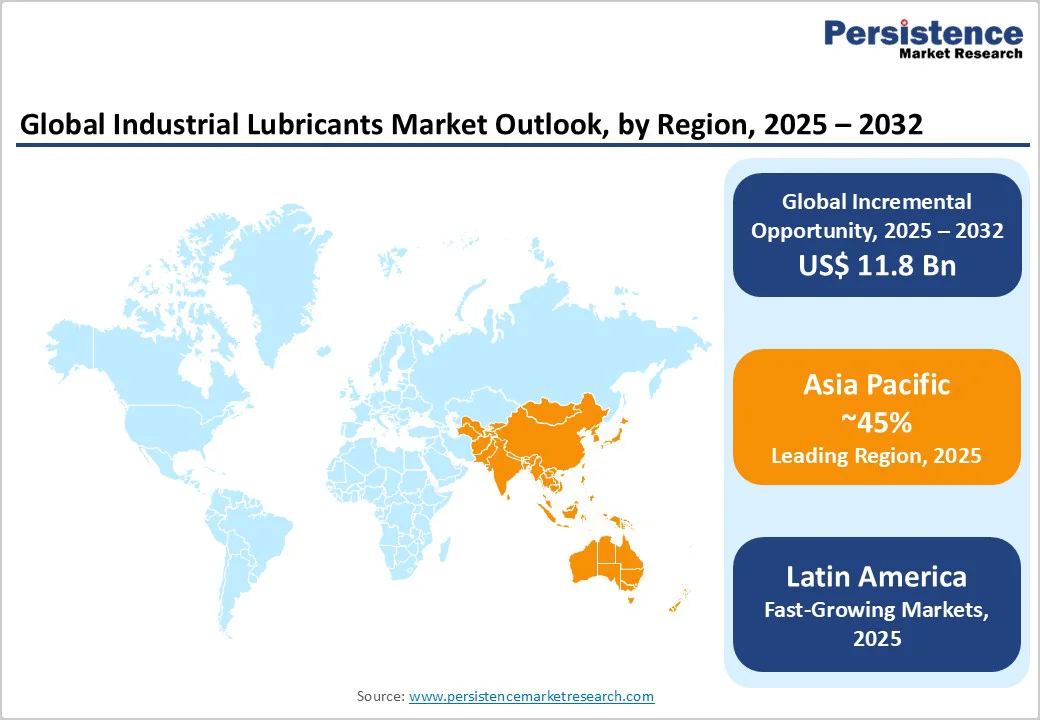

- Leading Region - Asia Pacific leads the global industrial lubricants market with approximately 45% share in 2025, driven by rapid industrialization, large-scale manufacturing, and expanding infrastructure across China, India, and Southeast Asia.

- Fastest-Growing Region - Latin America has been experiencing the fastest growth in the global industrial lubricants market, growing at a CAGR of 3.5% between 2025 and 2032, supported by nearshoring manufacturing expansion, mining sector growth, agricultural mechanization, and infrastructure development.

- Dominant Segment - Process Oils dominate the product landscape with nearly 35% share in 2025, reflecting their essential role in industrial machinery, power transmission systems, and construction equipment.

- Fastest-Growing Segment - Synthetic lubricants capture around 24.6% market share, gaining traction due to superior thermal stability, extended service life, and adoption across precision manufacturing and energy sectors.

- Key Opportunity - Bio-based and environmentally acceptable lubricants hold an emerging ~2% share, offering strong growth potential as industries transition toward sustainable, eco-friendly lubrication solutions.

| Key Insights | Details |

|---|---|

| Industrial Lubricants Market Size (2025E) | US$ 62.7 Billion |

| Market Value Forecast (2032F) | US$ 74.5 Billion |

| Projected Growth CAGR (2025 - 2032) | 2.5% |

| Historical Market Growth (2019 - 2024) | 2.0% |

Market Dynamics

Driver - Rising Industrialization and Manufacturing Automation

The rapid adoption of Industry 4.0 technologies, including robotics, IoT, and AI, has accelerated demand for high-performance industrial lubricants that can endure heavy loads, high speeds, and extreme conditions. According to UNIDO, global manufacturing value added grew by 4.1% in 2024, led by emerging economies such as China, India, and Vietnam. As industries shift toward precision manufacturing and smart factories, lubricants play a critical role in minimizing wear, reducing downtime, and extending machinery life.

Automation-driven operations increasingly rely on advanced lubrication systems for hydraulic circuits, compressors, and gearboxes, ensuring seamless equipment performance and operational efficiency. This growing industrial automation trend is directly fueling lubricant consumption across manufacturing and processing facilities worldwide.

Demand from Power Generation and Energy Sectors

The power generation sector has emerged as a key end-user of industrial lubricants, driven by expanding global energy needs and renewable infrastructure development. The International Energy Agency (IEA) forecasts a 3.4% annual rise in global electricity demand through 2026, propelled by new wind, hydro, and gas-based capacity installations. Specialized lubricants are essential for maintaining the reliability of turbines, generators, and transmission systems operating under high-stress conditions.

Parallelly, the oil and gas industry’s exploration and production activities continue to boost demand for premium-grade lubricants with superior oxidation stability and extended service life. In 2024, global turbine lubricant demand grew by over 5%, underscoring the sector’s focus on efficiency, reduced maintenance intervals, and enhanced equipment durability.

Restraint-Environmental Regulations and Sustainability Pressures

Stringent environmental and chemical regulations are significantly influencing the industrial lubricants landscape, particularly across Europe and North America. Frameworks such as REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) and the EU Ecolabel impose strict mandates on biodegradability, low toxicity, and emission reduction. These compliance standards necessitate extensive R&D investment and complex reformulation processes, increasing overall production costs.

While such regulations promote eco-friendly innovation, they also create entry barriers for small and mid-sized manufacturers, prolong product approval timelines, and limit market agility. Consequently, the cost of sustainable product transitions and testing under regulatory frameworks can slow market growth in highly regulated regions despite long-term environmental benefits.

Electric Vehicle Adoption and Reduced Lubricant Demand

The rapid adoption of electric vehicles (EVs) is reshaping the lubricant industry by reducing reliance on conventional automotive lubricants. According to the International Energy Agency (IEA), global EV sales surpassed 14 million units in 2023, marking a significant shift from internal combustion engines toward electric mobility. EVs use fewer lubricated components, mainly gearbox and thermal management fluids, compared to traditional engines that rely heavily on engine and transmission oils.

This transition directly diminishes lubricant volume demand from the automotive sector, traditionally one of the largest consumers. As electrification accelerates, lubricant manufacturers are being compelled to develop specialized fluids for EV drivetrains, e-axles, and battery cooling systems to adapt to the evolving mobility ecosystem and offset declining demand for conventional formulations.

Opportunity- Bio-based and Environmentally Acceptable Lubricants (EALs) Development

The development of bio-based and environmentally acceptable lubricants (EALs) offers one of the most promising growth avenues in the industrial lubricants market. Derived from renewable sources such as vegetable oils, animal fats, and synthetic esters, these lubricants exhibit superior biodegradability and low toxicity, aligning with global sustainability targets. According to industry estimates, the bio-lubricants segment is growing five times faster than the overall market.

The European Union’s environmental directives and green procurement standards increasingly mandate EAL usage in sectors like marine, forestry, and agriculture. Major players such as Shell, FUCHS SE, and Klüber Lubrication are heavily investing in R&D to create high-performance, eco-friendly products. With regulatory momentum driving up to fourfold higher growth impact than voluntary initiatives, manufacturers offering compliant, sustainable lubricant formulations are well-positioned to capture premium opportunities across industrial applications.

Specialized Lubricants for Mining and Agricultural Equipment

Rising mineral extraction activities and agricultural mechanization are generating substantial demand for specialized industrial lubricants. The global mining lubricants market size is likely to be valued at US$ 5.5 Billion in 2025 and is projected to reach US$ 7.5 Billion by 2032, growing at a CAGR of 4.5% between 2025 and 2032, driven by the need for high-performance hydraulic fluids, gear oils, and engine oils in heavy-duty machinery such as excavators, haul trucks, and draglines. These lubricants must withstand extreme pressure, high loads, and abrasive conditions.

Similarly, the agricultural sector’s mechanization boom in India, Brazil, and Indonesia is amplifying demand for tailored lubricants for tractors, harvesters, and irrigation systems. The rise of precision farming technologies and large-scale agribusiness operations further accelerates the consumption of premium-grade lubricants that enhance fuel efficiency, reduce maintenance costs, and improve machinery reliability. Manufacturers delivering equipment-specific lubricant formulations stand to gain strong market positioning and higher profit margins in these high-growth industries.

Category-wise Insights

Product Type Analysis

Process oils lead the demand for industrial lubricants, accounting for over 35% of the global demand in 2025. Process oils demonstrate unparalleled versatility across various industrial applications, serving as essential processing aids and raw material components far beyond their traditional role in lubrication.

Their most critical role remains in rubber and tire manufacturing, where they serve as plasticizers to enhance processability, flexibility, and filler dispersion, a particularly significant market given China's production of 859 million rubber tires annually.

Beyond tires, process oils are integral to polymer processing, where they improve the properties of thermoplastic elastomers (TPEs) and PVC through enhanced softness and extrusion capabilities, with this polymer segment demonstrating the fastest growth trajectory within process oil applications. They further extend their reach into chemicals and personal care formulations, serving as carrier fluids, reaction mediums, and functional additives in adhesives, sealants, and coatings.

This broad application portfolio creates a sustainable competitive moat that narrow-use lubricants cannot replicate. Process oils additionally penetrate agriculture and food processing sectors, where they function as crop protection carriers, pesticide fluids, anti-foaming agents, and production additives.

Unlike specialized lubricants constrained to specific machinery or equipment types, process oils' integration into fundamental material production processes, from tire compounds to polymer matrices to consumer care products, ensures consistent, volume-driven demand across diverse industries and economic conditions.

Hydraulic fluids hold the second-highest share in the industrial lubricants market, accounting for over 18% of the global share in 2025. Their dominance stems from extensive use in manufacturing machinery, construction equipment, and automotive systems, where they perform critical functions such as lubrication, power transmission, corrosion protection, and heat dissipation.

The segment benefits from rising industrial automation and infrastructure development, especially across Asia Pacific and the Middle East regions. Advancements in synthetic and bio-based hydraulic fluids have further enhanced performance efficiency, offering superior viscosity control and thermal stability under extreme operating conditions.

Grade Analysis

Mineral oil dominates the Grade segment, capturing 60-64% market share across diverse applications. Its cost-effectiveness, easy availability, and proven performance make it the preferred choice in cost-sensitive industries such as manufacturing, transportation, and construction.

Derived from crude oil refining, mineral oils deliver consistent lubrication and thermal stability, making them suitable for conventional equipment. Their affordability ensures strong adoption in emerging economies, where industrial expansion drives lubricant consumption despite environmental concerns.

Synthetic Grades represent the fastest-growing segment, supported by industries seeking extended oil drain intervals, reduced friction, and enhanced environmental compliance. These lubricants meet the requirements of advanced manufacturing systems and energy-efficient machinery, with growth further accelerated by rising adoption in aerospace, power generation, and heavy engineering sectors.

Industry Analysis

The oil and gas sector remains the leading Industry, accounting for the largest market share in 2025. It relies heavily on industrial lubricants for drilling rigs, compressors, turbines, and refining machinery exposed to high temperatures and contamination.

Lubricants enhance operational efficiency, reduce wear, and ensure equipment reliability across exploration, production, and transportation. The global expansion of oil extraction and refining capacities, especially in the Middle East and North America, continues to drive robust lubricant consumption across upstream and downstream activities.

Power generation is the fastest-growing end-use segment, supported by global energy demand, renewable capacity additions, and the modernization of aging thermal plants. Increasing installations of gas turbines, compressors, and wind turbines are creating strong demand for high-performance lubricants optimized for extreme pressure, temperature, and oxidative stability.

Regional Insights

North America Industrial Lubricants Trends

North America accounts for around 25% of the global industrial lubricants market, reflecting its mature yet stable demand base supported by strong manufacturing, aerospace, and energy sectors. U.S. leads regional consumption, driven by its extensive shale gas operations, construction machinery use, and precision industrial applications. Widespread adoption of synthetic and bio-based lubricants aligns with sustainability mandates and advanced equipment requirements.

Infrastructure reinvestment programs such as the U.S. Infrastructure Investment and Jobs Act bolster lubricant demand across heavy equipment and manufacturing plants. While market maturity limits volume growth, steady replacement cycles and the premiumization trend sustain healthy value expansion. Growth in North America remains moderate at 1.8% CAGR, underpinned by ongoing industrial modernization and emphasis on performance efficiency.

Europe Industrial Lubricants Trends

Europe is a technologically advanced, regulation-intensive market with strong adoption of synthetic and environmentally acceptable lubricants. Regulatory frameworks such as REACH, EU Ecolabel, and biodegradability mandates shape product portfolios and favor suppliers with R&D and compliance capabilities. Germany, France, the U.K., and other industrial powerhouses drive demand in automotive, precision engineering, and renewable energy sectors, particularly offshore wind and grid modernization projects.

Despite market maturity, Europe’s transition to circular-economy practices, increased re-refining, and procurement rules for EALs sustain steady growth. The region is projected to expand at a ~1.5% CAGR, supported by steady replacement cycles, equipment upgrades, and focused investment in sustainable lubricant technologies.

Asia Pacific Industrial Lubricants Trends

Asia Pacific leads the global industrial lubricants market, accounting for over 45% of total consumption in 2025, driven by rapid industrialization, expanding manufacturing sectors, and infrastructure growth across China, India, Japan, and ASEAN economies.

China dominates regional demand due to its massive automotive and machinery base, while India shows accelerating consumption under its “Make in India” and PLI initiatives. Strong manufacturing expansion, mechanized agriculture, and large-scale mining operations underpin the region’s growing lubricant requirements across hydraulic, gear, and compressor oil segments.

The region attracts substantial foreign and domestic investment in new blending plants and production capacity, as seen with ExxonMobil and Klüber Lubrication expansions in India. Rising automation and adoption of high-performance synthetic lubricants for industrial machinery sustain Asia Pacific’s dominance, positioning it as the global growth hub through the forecast period.

Competitive Landscape

The global industrial lubricants market is moderately consolidated, with dominance by vertically integrated producers offering complete value-chain control from Grade refining to finished lubricant formulation. These companies leverage extensive R&D capabilities, global supply networks, and advanced manufacturing technologies to develop high-performance and sustainable lubricant solutions. Product innovation focuses on synthetic, bio-based, and energy-efficient formulations catering to industrial automation and regulatory demands.

Competition is increasingly driven by differentiation rather than pricing, with emphasis on digital monitoring, predictive maintenance, and customized technical services. Strategic mergers, acquisitions, and partnerships enhance regional presence, expand specialty lubricant portfolios, and strengthen market positioning amid rising sustainability expectations.

Key Market Developments

- In April 2024, ExxonMobil Corporation announced a US$110 million investment to establish a greenfield lubricant manufacturing facility in Maharashtra, India, with an annual production capacity of 159,000 kiloliters of finished lubricants, targeting commercial startup by the end of 2025 to support "Make in India" initiatives and meet growing regional demand.

- In May 2024, Klüber Lubrication announced an investment of INR 142 crores to expand its Mysore production facility, incorporating state-of-the-art technology, new IATF and ISO 21469 certifications, and enhanced R&D infrastructure to accelerate new product development and serve specialized automotive and food-grade lubricant segments.

- In July 2024, TotalEnergies SE announced the acquisition of Tecoil, a leading producer of re-refined Grades (RRBOs), processing 50,000 tons of re-refined Grades annually from facilities in Hamina, Finland, strengthening sustainability credentials and supporting circular economy initiatives in lubricant production.

Companies Covered in Industrial Lubricants Market

- Shell plc

- ExxonMobil Corporation

- BP p.l.c.

- Chevron Corporation

- TotalEnergies SE

- FUCHS SE

- Klüber Lubrication

- Valvoline Inc.

- Quaker Chemical Corporation

- Idemitsu Kosan Co., Ltd.

- PetroChina Company Limited

- China Petroleum & Chemical Corporation (Sinopec)

- PETRONAS Lubricants International (PLI)

- Motul S.A.

- Houghton International Inc.

Frequently Asked Questions

The global industrial lubricants market was valued at US$ 62.7 billion in 2025 and is projected to reach US$ 74.5 billion by 2032, growing at a CAGR of 2.5%.

Market growth is driven by industrialization, automation, power generation expansion, oil & gas activities, mining, and infrastructure development.

Process oils dominate the market with over 35% share in 2025, due to widespread use in industrial and construction machinery.

Asia Pacific leads the market with around 45% share, driven by manufacturing expansion and rapid industrialization in China, India, and Southeast Asia.

The key growth opportunity lies in bio-based and environmentally acceptable lubricants and specialized products for mining and agriculture.

The market is led by major global manufacturers and specialty producers with strong R&D, integrated operations, and advanced product portfolios.