- Chipsets & Processors

- Programmable Robots Market

Programmable Robots Market Size, Share, and Growth Forecast, 2026 - 2033

Programmable Robots Market by Component (Hardware and Software), by Application (Education, Research & Prototyping, Entertainment, Household, and Other), and Regional Analysis for 2026 - 2033

Programmable Robots Market Size and Trends Analysis

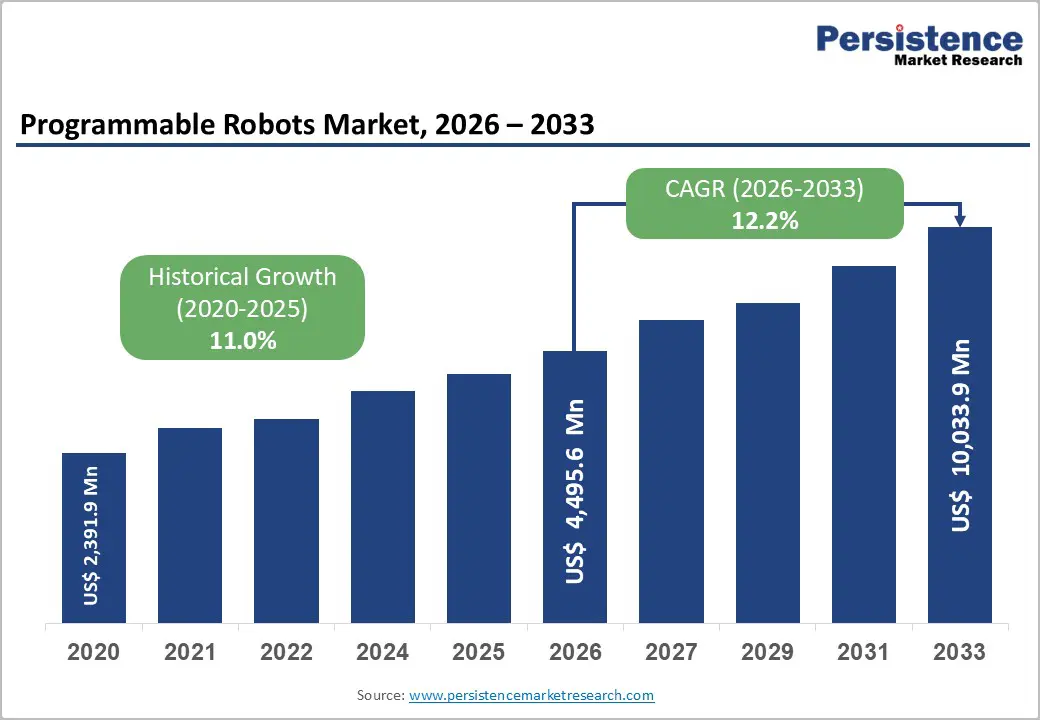

The global programmable robots market size was valued at US$ 4,495.6 Million in 2026 and is projected to reach US$ 10,033.9 Million by 2033, growing at a CAGR of 12.2% between 2026 and 2033. The historical CAGR from 2020 - 2026 was 11.0%, demonstrating sustained acceleration driven by expanding STEM education adoption, increasing automation demand across manufacturing sectors, and accelerating technological convergence in artificial intelligence and machine learning applications.

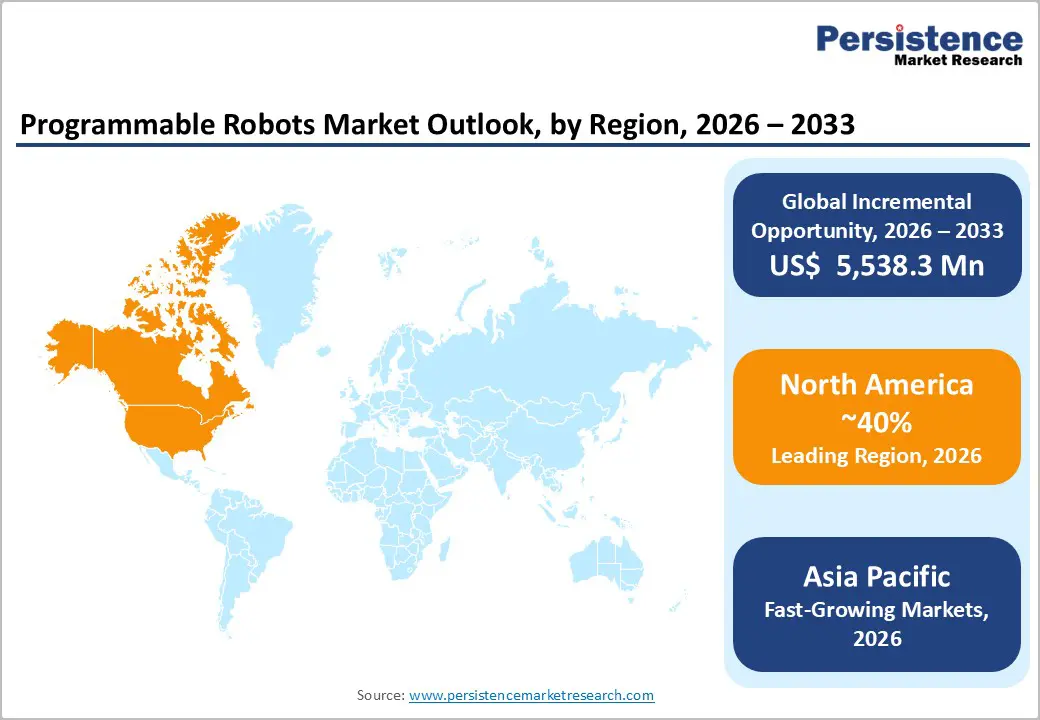

Primary growth catalysts include surging educational institution investment in robotics curricula, rising labor costs driving industrial automation adoption, and expanding research and prototyping applications across academic and commercial institutions. The market displays robust momentum across both developed economies emphasizing educational penetration and emerging markets prioritizing industrial automation, with Asia Pacific emerging as the fastest-growing regional market at 14.3% CAGR, signaling substantial technological democratization and skill development opportunities.

Key Industry Highlights:

- Component Dominance and Software Acceleration: Hardware components maintain market leadership with 60%+ revenue share driven by manufacturing capital investment; Software components demonstrate fastest growth at 14% CAGR reflecting cloud robotics, AI integration, and subscription-based service model monetization opportunities.

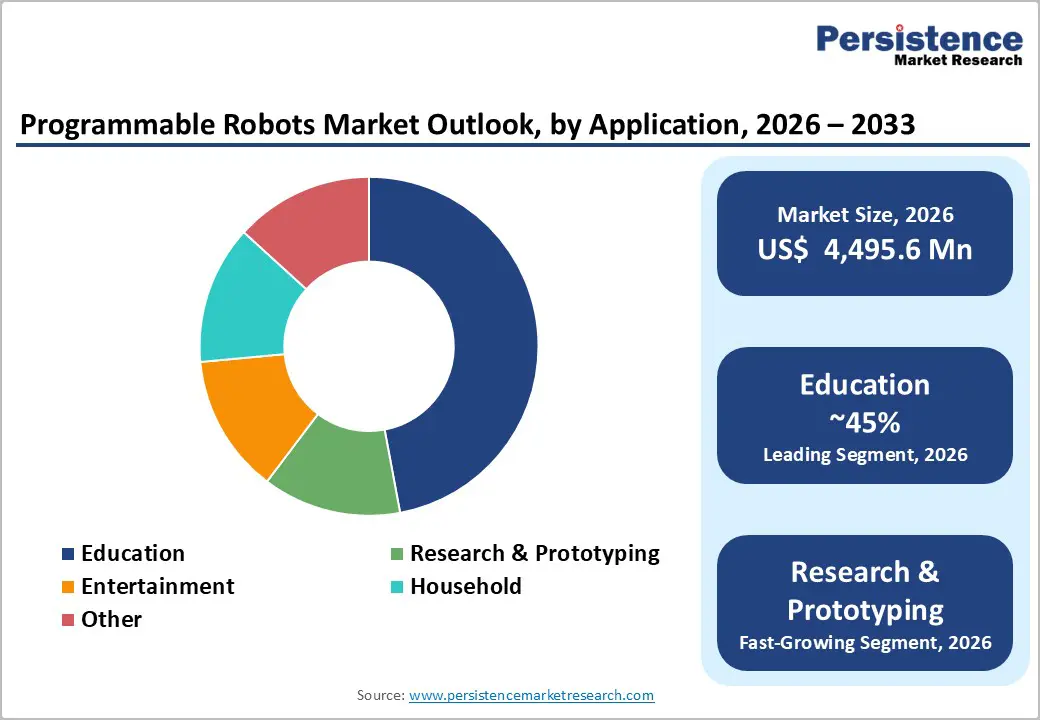

- Application Growth Leadership: Education applications command 45%+ market share through sustained institutional investment and curriculum integration; Research & Prototyping accelerates at 14.5% CAGR driven by university research expansion and commercial technology development initiatives.

- Regional Growth Leadership: Asia Pacific emerges as fastest-growing region at 14.3% CAGR substantially outpacing 11.8% North American and 11.5% European growth, with China, India, and ASEAN nations driving 60%+ incremental market value creation through 2033 manufacturing automation and educational modernization.

- Competitive Intensification: Market remains concentrated with 4-5 dominant manufacturers controlling 50-55% share; rapid Chinese manufacturer expansion capturing 15-20% market share in cost-competitive segments through subsidized production and emerging market penetration strategies.

- Healthcare and Specialty Market Expansion: Healthcare robotics regulatory approval and commercial deployment support estimated US$ 1.2-1.5 billion addressable market expansion reflecting 16-18% CAGR in assistive, surgical, and laboratory automation applications, distinct from traditional manufacturing focus.

| Global Market Attributes | Key Insights |

|---|---|

| Programmable Robots Market Size (2026E) | US$ 4,495.6 Mn |

| Market Value Forecast (2033F) | US$ 10,033.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 12.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.0% |

Key Growth Drivers

Manufacturing Automation Expansion and Industry 4.0 Adoption

Industrial automation adoption has accelerated substantially as manufacturers confront labor cost escalation, workforce skill shortages, and competitive pressure to enhance operational efficiency and product quality consistency. According to the International Federation of Robotics (IFR), global industrial robot installations exceeded 486,000 units in 2023, representing 5-7% annual growth with collaborative and programmable robot subcategories demonstrating 12-15% growth acceleration. Small and medium-sized enterprises (SMEs) increasingly deploy programmable robots for manufacturing flexibility, production optimization, and supply chain resilience following pandemic-induced disruptions.

Labor cost inflation across developed economies (particularly manufacturing sectors) exceeds 4-6% annually, creating economic justification for automation investments with 3-5 year payback periods. Industry 4.0 digital transformation initiatives across automotive, electronics, pharmaceuticals, and precision manufacturing sectors create substantial demand for programmable systems integrating production planning, quality assurance, and logistics automation. This driver supports sustained Research & Prototyping application growth at 14.5% CAGR as manufacturers utilize programmable robots for product development, prototyping, and production process optimization.

Market Restraining Factors

Technical Complexity and Skill Gap Constraints

Programmable robot utilization requires substantial technical expertise in programming, maintenance, integration, and troubleshooting, creating adoption barriers for organizations lacking dedicated technical resources. Educational institutions frequently struggle deploying robotics curricula due to insufficient teacher training, inadequate technical support infrastructure, and curriculum development complexity. Manufacturing SMEs encounter challenges integrating programmable robots into existing production environments, requiring system customization, workforce training, and operational disruption during implementation phases.

Technical talent scarcity in robotics engineering, embedded systems programming, and advanced control systems constrains adoption velocity, particularly in developing economies and geographic regions with limited higher education robotics programs. Industry reports document 40-50% technical adoption failure rates attributed to inadequate implementation planning, insufficient workforce training, and organizational change management gaps. Regulatory compliance requirements for industrial safety (ISO/TS 15066 for collaborative robots) impose additional technical and documentation requirements, extending implementation timelines and increasing deployment costs.

Programmable Robots Market Trends and Opportunities

Healthcare and Assistive Robotics Market Expansion

Programmable robots demonstrate emerging applications in elderly care, rehabilitation therapy, surgical assistance, and laboratory automation, creating substantial commercial opportunities as healthcare systems confront demographic aging, chronic workforce shortages, and operational efficiency pressures. The global elderly care market, valued at US$ 1.2 trillion annually, is increasingly adopting assistive robots for patient mobility, fall prevention, and companionship applications. Surgical robotics platforms integrating programmable capabilities and AI-assisted decision-making support minimally invasive procedures with improved clinical outcomes.

Laboratory automation utilizing programmable robots for sample handling, testing, and data management reduces human error while accelerating diagnostic and research throughput. The estimated healthcare and assistive robotics market opportunity exceeds US$ 2.5 billion by 2033, with 15-17% CAGR reflecting demographic aging trends, reimbursement model evolution, and clinical efficacy validation. Regulatory pathways through FDA approval and medical device classification frameworks are becoming increasingly accessible to robotics manufacturers, supporting commercialization acceleration.

Programmable Robots Market Insights and Trends

Component Insights

Hardware Dominates Programmable Robotics Components While Software Accelerates Rapidly Through 2033 Globally

The component structure of the programmable robots market is led by hardware, which accounts for over 60% of total revenue. This dominance is driven by the high value and capital intensity of physical robot systems, including mobile platforms, robotic arms, humanoid frames, controllers, sensors, and actuators. Hardware leadership is reinforced by established robotics manufacturers with vertically integrated production, strong supply chain control, and differentiated designs. In parallel, educational robotics hardware continues to gain traction due to user-friendly platforms, curriculum integration, and well-developed academic distribution networks. As education spending and industrial automation increase, hardware revenue is projected to reach approximately US$ 6.0-6.5 billion by 2033, expanding at an estimated CAGR of 11.5%. Ongoing innovation in modular design, ease of use, and cost efficiency supports the segment’s long-term primacy, despite rising competitive pressure from lower-cost manufacturers.

In contrast, software represents the fastest-growing component segment, expanding at nearly 14% CAGR. Growth is driven by advanced programming platforms, cloud-based control systems, and AI-enabled robotics intelligence. Software revenues are expected to rise sharply by 2033, supported by SaaS models, open-source ecosystems, enterprise integration, and increasing adoption of cloud robotics and machine learning frameworks.

Application Insights

Education Dominates Programmable Robotics Adoption While Research Prototyping Accelerates Rapidly Worldwide

The education segment represents the leading application area in the programmable robots market, accounting for more than 45% of global revenue. This dominance is driven by widespread curriculum integration, stable institutional budgets, and sustained government support for STEM education. K-12 institutions form the core demand base, particularly in advanced economies, while adoption is expanding rapidly across emerging markets. Universities and higher education institutions further strengthen demand by using programmable robots for research, project-based learning, and workforce skill development. Educational procurement typically includes platform-based robot kits, competition-oriented systems, and curriculum-aligned solutions bundled with teacher training and digital resources. According to market estimates, the education segment was valued at approximately US$ 2.0-2.2 billion in 2026 and is growing steadily at an 11.8% CAGR, reflecting long-term institutional commitment.

In contrast, research and prototyping applications represent the fastest-growing segment, expanding at a CAGR of about 14.5%. Universities, research laboratories, and technology companies increasingly rely on programmable robots for autonomous systems research, human-robot interaction studies, and rapid product prototyping. Growth is further supported by rising use in biomedical and life sciences research and strong public funding programs. This segment is projected to reach US$ 1.8-2.1 billion by 2033, underlining its accelerating innovation-driven momentum.

Regional Insights and Trends

North America Leads Programmable Robots Market Through Education, Automation, Innovation, and Investment Strength

North America remains the dominant region in the programmable robots market, accounting for over 40% of global revenue, supported by advanced educational infrastructure, strong industrial automation adoption, high research funding, and a mature innovation ecosystem. The United States alone contributes roughly 32% of global revenue, driven by widespread K-12 and university robotics programs, large-scale industrial deployments, and concentrated venture capital activity. The regional market is valued at approximately US$ 1.8-1.9 billion in 2026 and is projected to reach US$ 3.8-4.1 billion by 2033, growing at an estimated CAGR of 11.8%. While growth is slightly below the global average due to market maturity, Canada is expanding at a faster 12.4% CAGR, and Mexico represents an emerging opportunity as industrial automation investments increase.

Growth is reinforced by persistent labor shortages across manufacturing, healthcare, and logistics, accelerating automation demand, alongside strong STEM-focused education technology adoption. Substantial public and private research funding continues to drive innovation, particularly in AI-enabled and collaborative robotics. A supportive regulatory environment, especially in healthcare and education, further strengthens commercialization prospects. The competitive landscape is concentrated in industrial robotics but fragmented in education-focused platforms, while rising venture capital, mergers, and strategic investments signal sustained long-term growth potential across multiple application segments.

Asia Pacific Programmable Robots Market Growth Driven by Industrialization, Education, and Automation Investments

Asia Pacific is the fastest-growing regional market for programmable robots, expanding at a robust CAGR of 14.3%, significantly outperforming the global average. This growth is driven by rapid industrialization, cost-efficient manufacturing ecosystems, accelerated educational modernization, and rising public and private research funding. The region’s market size is estimated at approximately US$ 1.3-1.4 billion in 2026 and is projected to reach US$ 3.5-3.9 billion by 2033. China dominates the regional landscape, accounting for nearly 40-45% of total demand, supported by large-scale manufacturing automation and a rapidly maturing domestic robotics industry.

According to the International Federation of Robotics, China leads with over 268,000 industrial robot installations in 2023 and strong growth in programmable robot adoption, while Japan maintains a premium position through technologically advanced domestic manufacturers. India is emerging as a high-growth market, particularly in educational robotics, backed by government-led STEM initiatives and a growing startup ecosystem. ASEAN countries are also witnessing steady expansion as manufacturing modernization and educational investments increase.

Overall growth is reinforced by labor cost inflation, automation-driven productivity needs, supportive government policies, and increasing applications across education, healthcare, and research, positioning Asia Pacific as the global growth engine for programmable robots.

Programmable Robots Market Competitive Landscape

The programmable robots market exhibits a moderately concentrated competitive structure, with approximately four to five dominant industrial robot manufacturers collectively accounting for nearly 50-55% of global market share. Established players such as Universal Robots, ABB Robotics, KUKA, Rethink Robotics, and Yaskawa dominate industrial automation applications through long-standing customer relationships, extensive global distribution networks, and strong after-sales technical support capabilities.

The market is characterized by a dual-track competitive environment. The industrial automation segment features high entry barriers driven by capital intensity, system integration complexity, and application-specific customization requirements. In contrast, the educational and research robotics segment remains highly fragmented, with numerous platform providers competing aggressively on price, modularity, and innovation speed, leading to shorter product life cycles and rapid technology iteration.

Geographically, manufacturing capabilities are concentrated across Japan, Germany, and emerging Asian production hubs, supporting supply chain resilience while reinforcing incumbent advantages. Meanwhile, emerging technology firms and startups are gaining traction in collaborative robotics, autonomous systems, and AI-enabled platforms, introducing disruptive potential and intensifying competition across niche and specialized applications.

Key Industry Developments

- On 15 December 2025, Researchers from the University of Pennsylvania and the University of Michigan unveiled the world’s smallest fully programmable and autonomous robots. These microscale swimming robots are capable of sensing their environment, processing information, and independently performing tasks. The breakthrough opens significant opportunities in advanced manufacturing, targeted medical procedures, and microscale automation, redefining how programmable robotics can function at extremely small scales.

- On 18 June 2024, Sphero launched Sphero BOLT+™, the next-generation version of its widely adopted programmable educational robot. The upgraded platform enhances coding capabilities, sensor performance, and classroom durability, reinforcing Sphero’s leadership in interactive robotics solutions for STEM education and hands-on learning environments.

- On 13 April 2023, SynSense introduced the world’s first neuromorphic programmable robot equipped with dynamic vision sensing. Designed to enable advanced human-machine interaction, the robot leverages brain-inspired computing to process visual data efficiently in real time, marking a major step forward in energy-efficient, intelligent robotic systems.

Companies Covered in Programmable Robots Market

- Universal Robots

- ABB Robotics

- KUKA AG

- Yaskawa Electric

- FANUC Corporation

- Rethink Robotics

- Techman Robotics

- Lego Group

- VEX Robotics

- Aubo Robotics

- Hiwin Technologies

- DJI RoboMaster

- Boston Dynamics

- UR+ ecosystem partners

- MiR

- Sphero

- RobotShop Inc.

- Yujin Robot

- WowWee Group

- RoboBuilder

- SoftBank Robotics

- iRobot Corporation

- Honda Motor Co., Ltd.

- Evolve Inc.

- Other Market Players

Frequently Asked Questions

The Programmable Robots market is estimated to be valued at US$ 4,495.6 Mn in 2026.

The key demand driver for the Programmable Robots market is the rising need for flexible, intelligent automation across education, manufacturing, and service applications.

In 2026, the North America region will dominate the market with an exceeding 40% revenue share in the global Programmable Robots market.

Among applications, education has the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other applications.

Universal Robots, ABB Robotics, KUKA AG, VEX Robotics, Aubo Robotics, Sphero, RobotShop Inc., and Yujin Robot. There are a few leading players in the Programmable Robots market.