- Food Ingredients & Additives

- Industrial Starch Market

Industrial Starch Market Size, Share, and Growth Forecast, 2025 - 2032

Industrial Starch Market By Product Type (Native Starch, Cationic Starch, Others), Source (Corn, Wheat, Cassava, Others), Application (Food & Beverage, Feed, Others), and Regional Analysis for 2025 – 2032

Industrial Starch Market Size and Trends Analysis

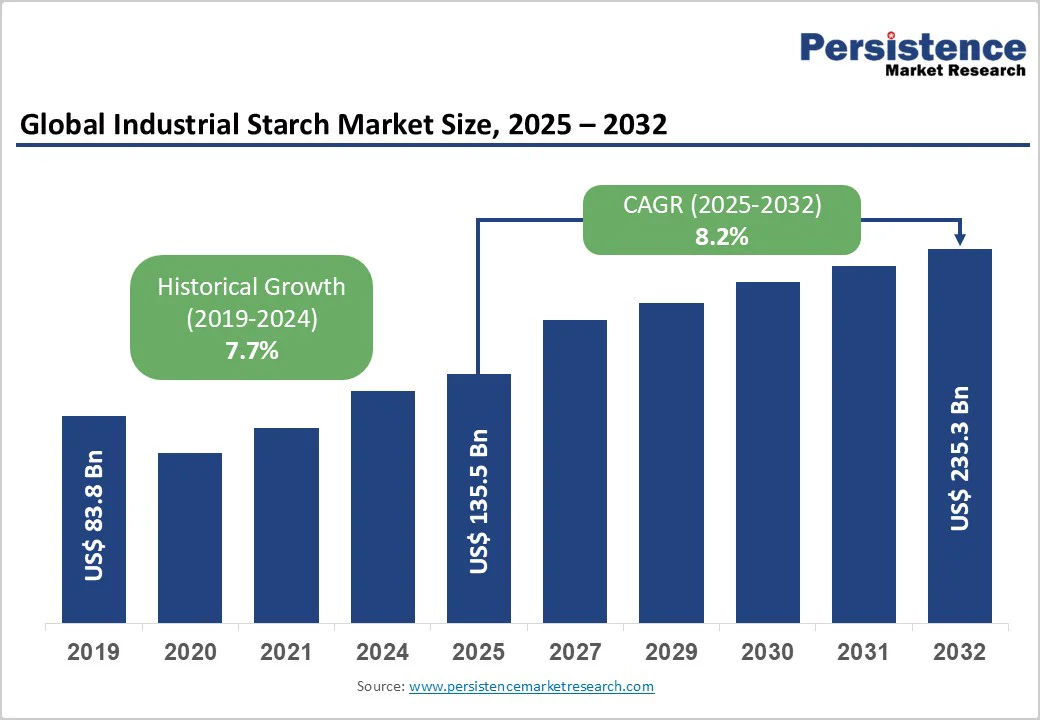

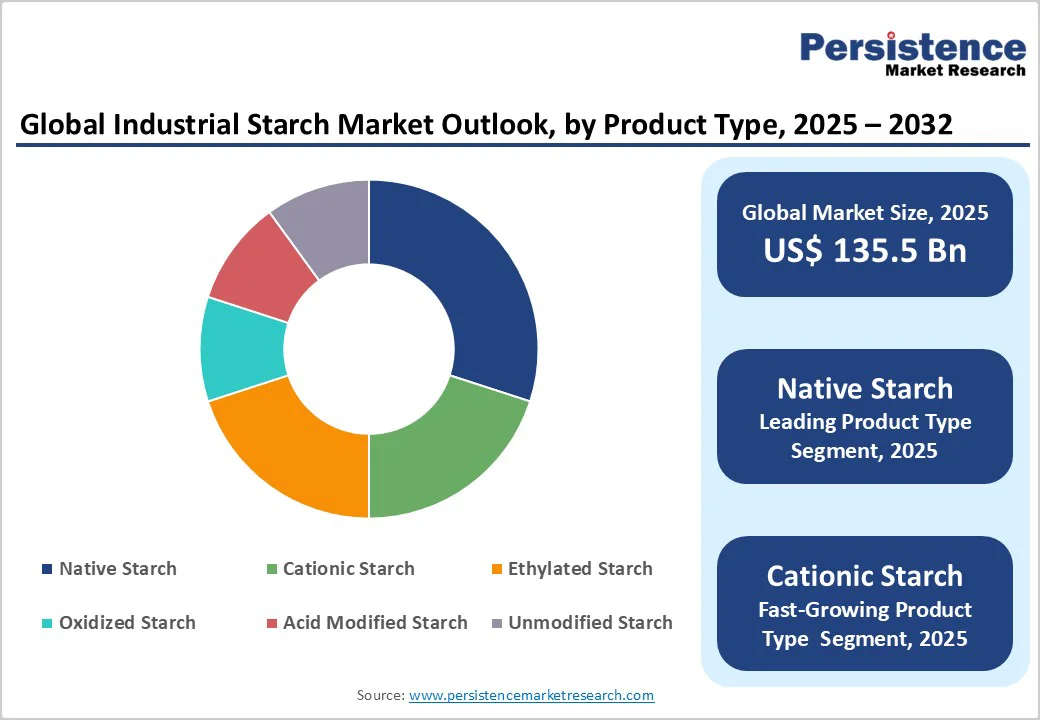

The global Industrial Starch Market size is likely to be valued US$135.5 Billion in 2025, growing to US$235.3 Billion by 2032 at a CAGR of 8.2% during the forecast period from 2025 to 2032 driven by increasing demand for starch in food processing, pharmaceuticals, and industrial applications, rising adoption of bio-based materials, and advancements in modification technologies.

The market is further propelled by innovations in modified starches for enhanced functionality, catering to preferences for eco-friendly and high-performance solutions. The growing acceptance of industrial starch as a renewable alternative to synthetic polymers, especially in food & beverage and feed industries, is a key growth factor.

Key Industry Highlights:

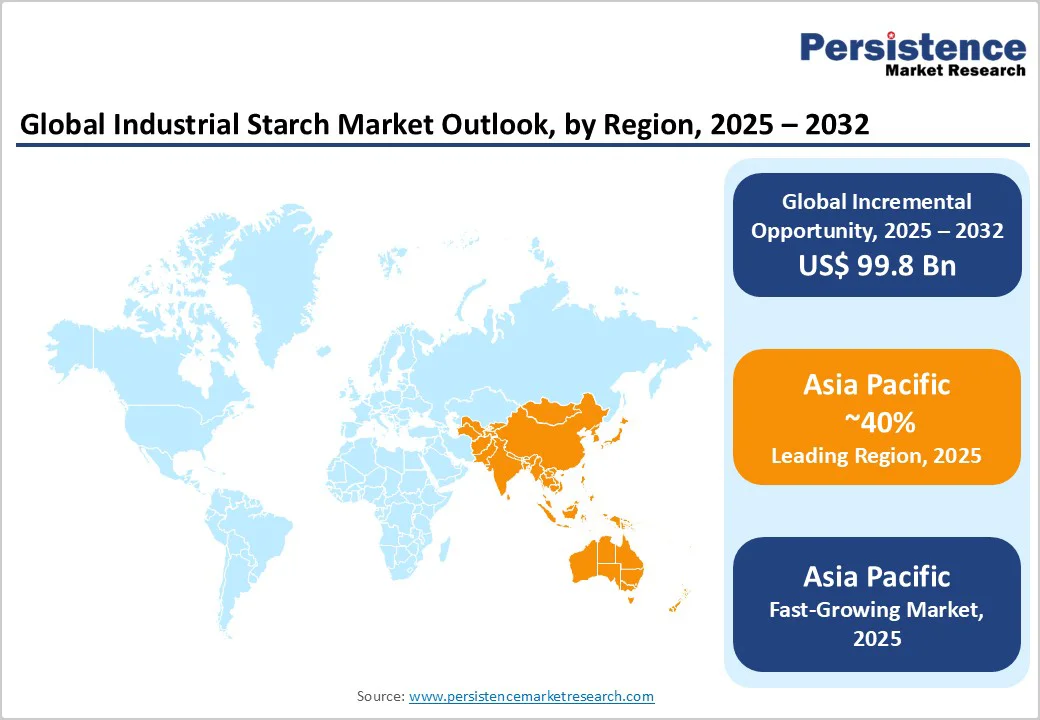

- Leading Region: Asia Pacific, commanding a 40% market share in 2025, driven by robust food processing and textile industries in China and India.

- Fastest-growing Region: Asia Pacific, fueled by rising industrialization, agricultural output, and investments in bio-based products.

- Dominant Product Type: Native Starch, holding approximately 35% of the market share, due to its cost-effectiveness and wide use in basic applications.

- Leading Source: Corn, accounting for over 45% of market revenue, driven by abundant supply and versatility.

- Leading Application: Food & Beverage, contributing nearly 40% of market revenue, owing to demand for thickeners and stabilizers.

- Key Market Driver: Increasing need for advanced drug delivery and patient-friendly formulations drives starch adoption in healthcare.

- Growth Opportunity: Advancements in cationic starch for paper manufacturing, enabling sustainable packaging solutions.

| Key Insights | Details |

|---|---|

|

Industrial Starch Market Size (2025E) |

US$135.5 Bn |

|

Market Value Forecast (2032F) |

US$235.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Demand for Bio-Based Materials in Food and Industrial Applications

The rising demand for sustainable, bio-based ingredients in food processing and industrial uses is a primary driver of the industrial starch market. Consumers and manufacturers are progressively prioritizing sustainability, driving a shift from synthetic, petroleum-based products toward natural, renewable alternatives.

In the food sector, starch serves as a versatile ingredient, acting as a thickener, stabilizer, and binder in bakery, dairy, and processed products. The preference for clean-label, non-GMO, and naturally derived ingredients further boosts the adoption of starch, reinforcing its role as a bio-based material.

In industrial applications, starch is increasingly used in biodegradable packaging, adhesives, textiles, and paper coatings. Its renewable nature, biodegradability, and compatibility with other eco-friendly materials make it an ideal substitute for conventional plastics and chemical-based additives. Regulatory frameworks and environmental policies across regions are encouraging manufacturers to adopt bio-based solutions, amplifying demand.

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuations in crop prices and supply chain issues pose significant restraints on market growth. Raw materials such as corn, potatos, and cassava are heavily influenced by factors such as seasonal variations, adverse weather conditions, and fluctuating global commodity prices.

Geopolitical tensions and trade restrictions may restrict imports and exports, creating localized shortages and price spikes. For manufacturers relying on a consistent supply of starch, these uncertainties lead to increased operational costs, inventory management challenges, and pricing pressures for end consumers.

The combined effect of raw material volatility and supply chain instability forces companies to adopt risk mitigation strategies, including diversifying sourcing, investing in local production, maintaining buffer inventories, and exploring alternative starch sources.

For instance, droughts, floods, or crop diseases can reduce yields, driving up raw material costs and affecting the availability of starch for downstream industries. Supply chain disruptions further exacerbate these challenges. Transportation bottlenecks, port congestion, fuel price fluctuations, and labour shortages can delay the movement of raw materials and finished products.

Expansion in Pharmaceuticals and Sustainable Packaging

Advancements in modified starches for pharmaceuticals and eco-friendly packaging present significant growth opportunities for the industrial starch market. In the pharmaceutical sector, starch plays a crucial role as an excipient, serving as a binder, filler, disintegrant, and stabilizer in tablets, capsules, and other drug formulations.

Increasing demand for targeted drug delivery systems, controlled-release medications, and patient-friendly oral formulations has accelerated the adoption of high-purity starches such as potato and corn derivatives.

The preference for natural, non-GMO, and clean-label ingredients aligns with the growing focus on safety, efficacy, and regulatory compliance in the pharmaceutical industry, further driving growth.The push for sustainable packaging solutions is creating new opportunities for starch-based materials.

As environmental concerns intensify and regulations against single-use plastics tighten, starch is increasingly used in biodegradable films, coatings, and molded packaging products. Its renewable nature, biodegradability, and compatibility with other bio-based materials make it an ideal alternative to conventional plastics.

Category-wise Analysis

Product Type Insights

Native Starch dominates the market, accounting for 35% of the share in 2025, owing to its simplicity, low production cost, and versatility. Widely used as a thickening, gelling, and stabilizing agent in food products, it meets basic industrial and culinary needs efficiently. Its accessibility and broad application across bakery, dairy, and processed foods sustain its leading market position.

Cationic Starch is the fastest-growing segment, driven by rising demand in the paper and textile industries. Its positive charge enhances fiber bonding, improves paper strength, and facilitates dye fixation in textiles. Increasing production of high-quality paper products and vibrant, durable fabrics is accelerating adoption, while industrial growth and sustainability trends further boost the use of cationic starch across these sectors.

Source Insights

Corn leads with over 45% share, driven by its high yield, cost-effectiveness, and well-established supply chains. Its versatility in food, beverage, and industrial applications, combined with consistent quality and wide availability, makes it a preferred choice for manufacturers. Strong global production and infrastructure support further reinforce corn starch’s dominant position in the market.

Potato is the fastest-growing, propelled by its increasing use in premium pharmaceutical applications. Valued for its high purity, excellent binding properties, and digestibility, it is widely adopted in tablets, capsules, and controlled-release formulations. Growing demand for natural, non-GMO excipients and clean-label products further accelerates the uptake of potato starch in pharmaceutical manufacturing.

Application Insights

Food & Beverage holds nearly 40% share, driven by extensive use of industrial starch to enhance texture, consistency, and stability in products. Its application spans bakery, dairy, and processed foods, improving viscosity and shelf life. Rising demand for clean-label, natural ingredients and functional foods further reinforces starch adoption, sustaining strong growth in this sector.

Pharmaceuticals are the fastest-growing, driven by increasing demand for advanced drug delivery systems. Growth is fueled by the need for precise, targeted therapies, enhanced bioavailability, and patient-friendly formulations such as oral, injectable, and transdermal delivery. Rising chronic disease prevalence and innovations in controlled-release and nanotechnology-based drugs further accelerate market expansion in this sector.

Regional Insights

Asia Pacific Industrial Starch Market Trends

Asia Pacific commands around 40% share and is the fastest-growing region, driven by the rapid expansion of manufacturing and agricultural sectors. China’s robust manufacturing base, particularly in textiles, paper, and adhesives, fuels significant demand for starch as a functional ingredient in industrial processes.

India’s strong agricultural output, including corn, cassava, and wheat, provides a reliable supply of raw materials, supporting large-scale starch production. Rising urbanization, increasing disposable incomes, and expanding food processing industries in countries such as Thailand, Vietnam, and Indonesia further contribute to regional growth.

Industrial starch is extensively used in processed foods, bakery products, sauces, and convenience foods, meeting the demand for texture enhancement, thickening, and stabilization. The shift toward bio-based and sustainable products, such as biodegradable packaging and eco-friendly adhesives, is driving further adoption in the region.

Investments in advanced processing technologies and supply chain optimization are helping manufacturers improve yield, reduce costs, and maintain quality standards.

North America Industrial Starch Market Trends

North America accounts for 25% in 2025, driven by the United States’ thriving food processing industry. Starch is widely used as a thickener, stabilizer, and texture enhancer in bakery, dairy, sauces, and convenience foods, while modified starches play a key role in meeting specific functional requirements such as improved viscosity, freeze-thaw stability, and shelf-life extension.

The increasing demand for clean-label, natural, and non-GMO ingredients is encouraging manufacturers to adopt high-quality, sustainably sourced starches in both food and beverage applications.

Industrial starch finds applications in paper, textile, and adhesive production, particularly in bio-based and eco-friendly formulations. The U.K. market, although part of Europe, exhibits similar trends, driven by the adoption of clean-label starches and growth in bio-based adhesives for sustainable packaging solutions. Companies are investing in product innovation, advanced processing technologies, and strategic partnerships to meet evolving customer demands.

Europe Industrial Starch Market Trends

Europe holds about 30% market share, led by Germany and France, due to EU sustainability regulations and strong pharmaceutical sectors. The market growth is strongly influenced by the European Union’s stringent sustainability and environmental regulations, which encourage the adoption of bio-based, renewable, and eco-friendly starch products.

Industrial starch in Europe finds extensive applications across food processing, paper, textile, adhesives, and especially the pharmaceutical industry, where it is used as a binder, filler, and excipient in tablet formulations.

Germany’s well-established chemical and pharmaceutical sectors, along with France’s strong food processing and specialty chemicals industries, create consistent demand for high-quality starch variants, including modified starches and resistant starches. The growing consumer preference for clean-label, natural, and non-GMO ingredients supports the use of starch in food and beverage applications.

Companies are also investing in research and development to produce starch-based biodegradable packaging and other sustainable solutions, aligning with regional environmental policies. Robust distribution networks, advanced processing technologies, and collaborations with local suppliers further strengthen the market position of Europe.

Competitive Landscape

The global industrial starch market is highly competitive, dominated by major players such as Archer Daniels Midland Company, Cargill, Tate & Lyle, and Grain Processing Corporation, who collectively influence market trends and pricing.

These companies are increasingly emphasizing sustainable sourcing practices, including the use of non-GMO crops and environmentally responsible cultivation methods, to meet rising consumer and regulatory demands for eco-friendly products. Product innovation is a central strategy, with firms developing specialty starches tailored for diverse applications across food, beverage, paper, textile, adhesives, and bio-based industries.

Modified starches, resistant starches, and enzymatically processed variants are being introduced to enhance functionality, performance, and nutritional value. The push toward bio-based and biodegradable solutions is driving research into starch-based polymers and packaging materials, offering alternatives to conventional plastics.

Companies are also investing in advanced processing technologies to improve yield, reduce waste, and maintain consistent quality. Strategic partnerships, mergers, and acquisitions are common to strengthen regional presence and expand product portfolios.

Key Developments

- In February 2025, Cargill entered a joint venture with KMC Kartoffelmelcentralen to expand the European production capacity of resistant potato starch. This move aims to strengthen the supply for functional food and nutrition applications.

- In May 2025, Roquette Frères, a global leader in plant-based ingredients, launched a new line of tapioca-based starches to strengthen its product portfolio. The expansion aims to address the rising demand for bio-based materials across food and industrial applications.

Companies Covered in Industrial Starch Market

- Archer Daniels Midland Company

- Tate & Lyle

- Grain Processing Corporation

- Cargill, Incorporated

- Manildra Group

- Universal Starch Chem Allied Ltd.

- EVEREST STARCH (IND) PVT.LTD.

- GreenTech Industries Ltd.

- Karandikars Cashell Private Limited

- Bangkok Starch Industrial Co., Ltd.

Frequently Asked Questions

The global industrial starch market is projected to reach US$135.5 Bn in 2025, driven by demand for bio-based ingredients in food and pharma.

Growing preference for biodegradable and bio-based materials fuels starch use in food, packaging, and industrial applications.

The market is poised to witness a CAGR of 8.2% from 2025 to 2032, supported by modified starch innovations.

Expansion in cationic industrial starch for sustainable packaging offers key opportunities in paper and textiles.

Archer Daniels Midland, Cargill, Tate & Lyle, Grain Processing, and Manildra Group lead through sustainable industrial starch innovations.