- Food Ingredients & Additives

- Industrial Fat Fraction Market

Industrial Fat Fraction Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Industrial Fat Fraction Market by Product Type (Milk Fat Fractions, Vegetable Fat Fractions), by End-user (Food & Beverage, Personal Care & Cosmetics, Pharmaceutical, Industrial Applications), and Regional Analysis from 2026 - 2033

Industrial Fat Fraction Market Share and Trends Analysis

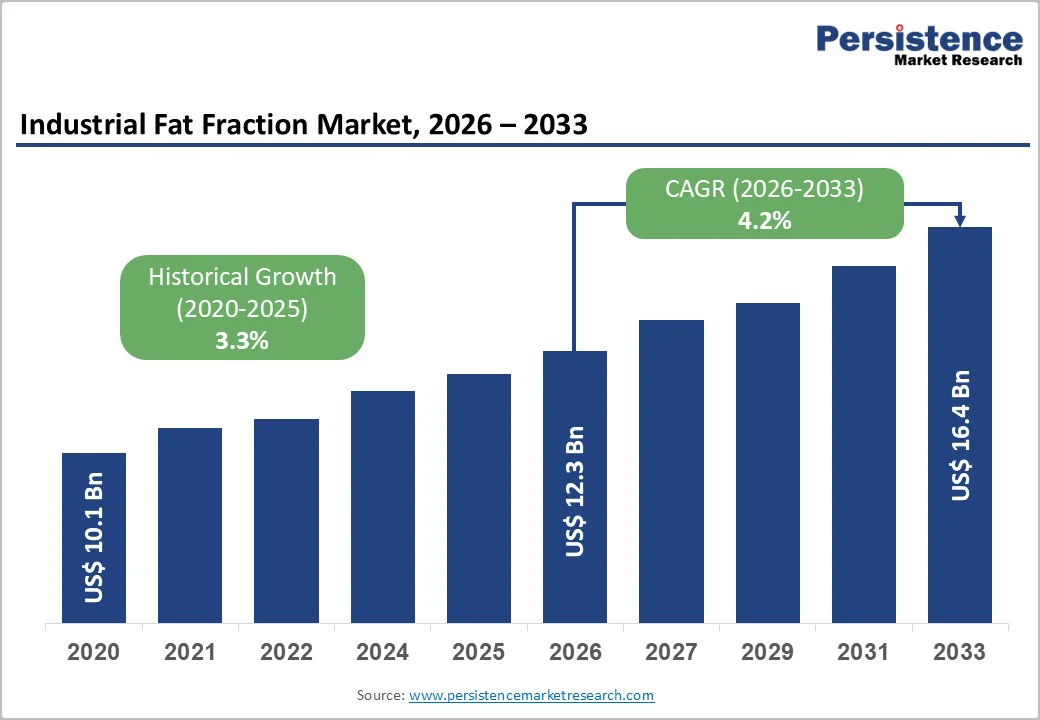

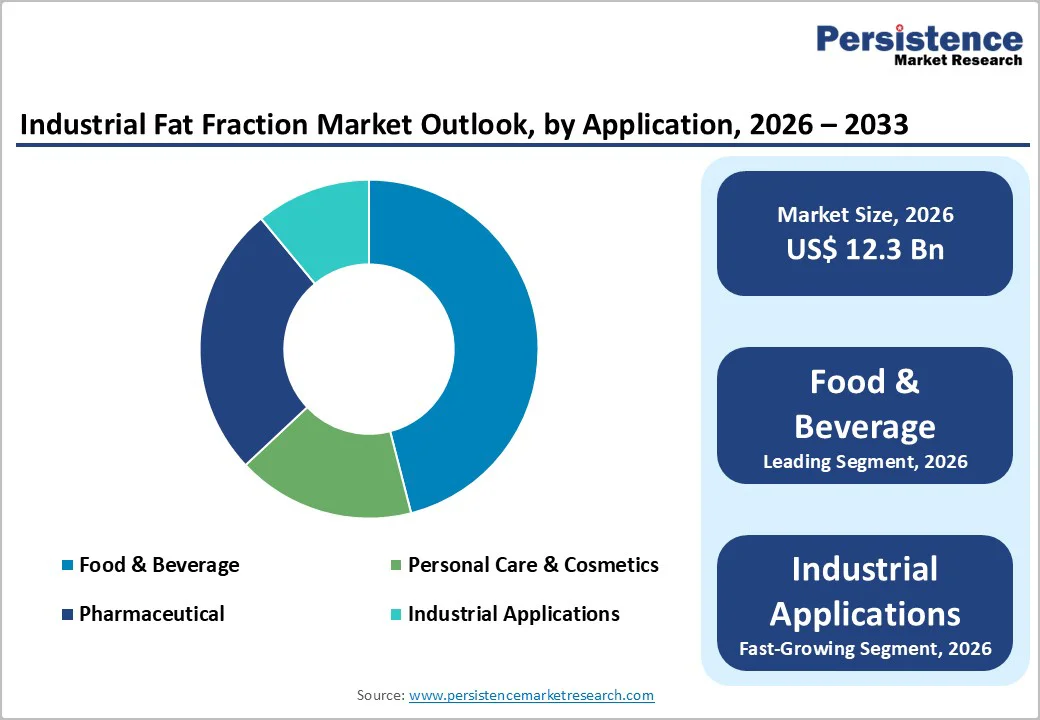

The global industrial fat fraction market size is estimated to grow from US$ 12.3 billion in 2026 to US$ 16.4 billion by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033.

A rapidly evolving fat-processing ecosystem is reshaping global competition as food, confectionery, and specialty ingredient manufacturers lean heavily on precision-engineered fat fractions. Emerging sustainability commitments, advanced fractionation technologies, and rising demand for heat-stable, clean-label fats are accelerating strategic activity across regions and product categories.

Key Industry Highlights:

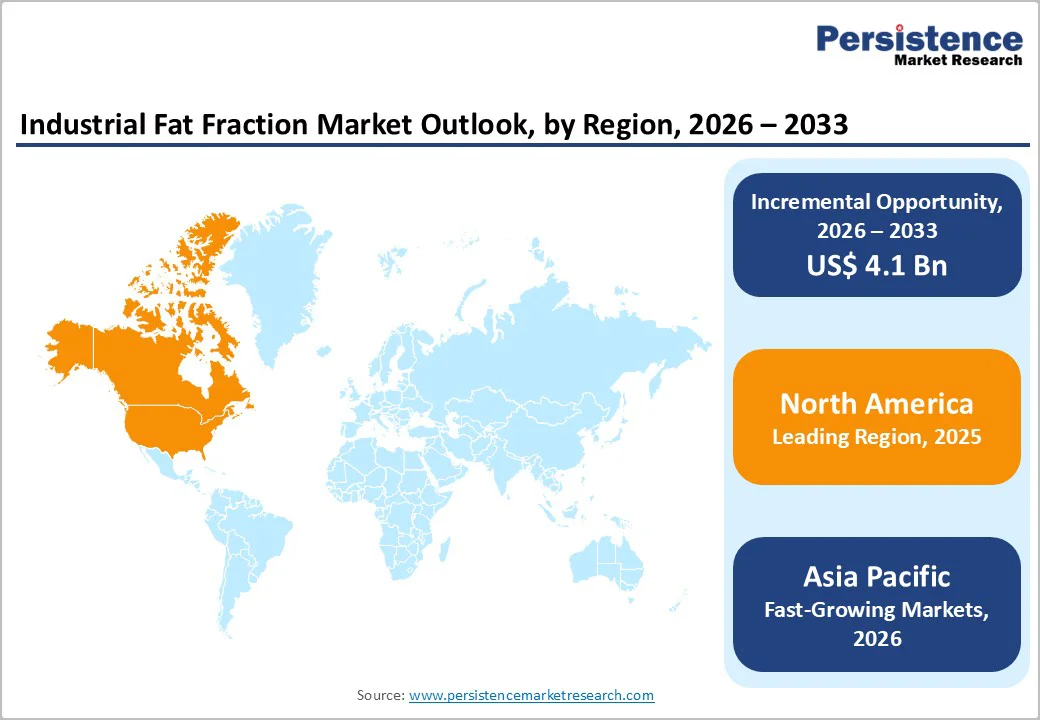

- Leading Region: North America leads the global Industrial Fat Fraction market, driven by aggressive reformulation in bakery, confectionery, and dairy alternatives, as well as strong adoption of high-performance specialty fats.

- Fastest-Growing Region: Asia Pacific is expanding swiftly as China, India, Japan, and South Korea accelerate investments in tailored mid-fractions, enzymatically modified fats, and region-specific clean-label sourcing.

- Dominant Product Type Segment: Vegetable Fat Fractions remain the most widely used due to their versatility, scalable supply chains, and strong alignment with plant-focused product innovation.

- Market Drivers: Rising consumption of processed foods and snacks is intensifying demand for fat fractions that enhance stability, texture, melting behavior, and shelf-life performance across mass-market and premium product lines.

- Opportunities: Expanding use of cocoa-butter substitutes is unlocking new value for specialty fat processors offering tailored CBE and CBS systems with advanced melting control and cost-efficient formulation benefits.

- Key Developments: In May 2025, the Danish government collaborated with global industry players to enhance sustainable palm oil production in Indonesia. In May 2025, Cargill secured the top position in the Edible Oil Supplier Index for fully eliminating industrial trans fats across its global edible oils portfolio.

| Key Insights | Details |

|---|---|

|

Industrial Fat Fraction Market Size (2026E) |

US$ 12.3 Bn |

|

Market Value Forecast (2033F) |

US$ 16.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.3% |

Market Dynamics

Driver - Rising consumption of processed foods and snacks

A noticeable shift in global eating patterns is placing processed foods and ready-to-eat snacks at the center of everyday consumption, directly accelerating demand for industrial fat fractions. As busy lifestyles reshape meal routines, manufacturers rely on specialty fat fractions to enhance texture, stability, mouthfeel, and shelf life in baked goods, confectionery, noodles, fillings, and snack coatings. These ingredients help achieve consistent melting profiles and improve product performance during high-temperature processing, making them indispensable for large-scale food production. The surge in indulgent snacking, premium bakery launches, and convenience-driven product innovation further expands usage. With brands developing cleaner, tastier, and more functional processed foods, industrial fat fractions become strategic enablers of quality improvement and cost-efficient formulation.

Restraints - Stringent food-safety and labeling regulations

A tightening regulatory environment is reshaping how industrial fat fractions are produced, labeled, and marketed, creating a significant restraint for manufacturers. Governments are imposing stricter rules on contaminants, allergen management, trans-fat limits, and traceability, forcing companies to upgrade processes and adopt more rigorous quality-control systems. Compliance requires detailed documentation on sourcing, refining steps, and nutritional composition, increasing operational complexity for producers handling multiple fat fractions such as low-, mid-, and high-melting fractions. Frequent regulatory updates can delay product launches and raise certification costs, especially for exporters targeting regions with differing standards. These pressures limit flexibility in formulation and slow down innovation cycles, challenging companies attempting to scale efficiently while maintaining regulatory alignment across global markets.

Opportunity - Expanding Use of Cocoa-Butter Substitutes Boosts Strategic Potential for Specialty Fat Processors

A fresh wave of formulation redesign in confectionery and bakery is creating a strong opening for specialty fat processors as demand for cocoa-butter substitutes accelerates. Brands are rebalancing cost structures and improving texture performance by integrating palm-, shea-, and kernel-based mid-fractions that mimic cocoa butter’s melting behavior while offering greater stability in warm climates. This shift enables processors to position tailored CBE and CBS solutions with precise melting profiles, sharper crystallization control, and improved compatibility with chocolate coatings. Startups can enter with agile refining, enzymatic interesterification, and sustainable sourcing models that appeal to manufacturers seeking resilient, ethically aligned fat systems. The rising adoption of cocoa-butter alternatives expands long-term opportunities for processors delivering consistent functionality and high-quality specialty fat fractions.

Category-wise Analysis

By Product Type Insights

Vegetable Fat Fractions command market dominance because manufacturers increasingly rely on their stability, cost efficiency, and broad applicability across bakery, confectionery, infant nutrition, and savory formulations. Their adaptable melting profiles, consistent crystallization behavior, and scalable supply chains make them the preferred choice for high-volume processors seeking dependable performance in diverse product lines. The rise of plant-focused reformulation further strengthens their position as brands prioritize clean-label, allergen-friendly, and sustainably sourced fat systems. Milk Fat Fractions maintain a strong presence in premium applications, particularly in chocolate, dairy analogues, and specialty bakery, where richness, flavor depth, and natural butter notes are critical. Their role continues to expand within high-end segments that value sensory quality and authentic dairy functionality.

By End-user Insights

Industrial applications are projected to grow at a CAGR of 5.2% during the forecast period, reflecting a clear shift in how manufacturers approach fat structuring, ingredient optimization, and performance-driven formulations. Demand is strengthening as food processors, pharmaceutical companies, and personal-care manufacturers seek specialty fat fractions that deliver precision melting behavior, improved stability, and consistent textural outcomes. In bakery and confectionery, tailored fractions enhance mouthfeel, aeration, and shelf life, supporting large-scale automated production. Pharmaceuticals rely on these fats for controlled-release systems and excipient functionality, while cosmetic and skincare brands use structured lipids to create smoother emulsions and long-lasting sensory profiles. As efficiency, product consistency, and functional customization become top priorities, industrial applications are set to expand across multiple downstream sectors.

Region-wise Insights

North America Industrial Fat Fraction Market Trends

North America dominates the global industrial fat fraction market as brands across the region aggressively push toward cleaner formulations, advanced processing, and high-performance specialty fats. In the US, food manufacturers are reformulating bakery, confectionery, and dairy alternatives with precision-engineered mid- and high-melting fractions to enhance stability, heat resistance, and mouthfeel. Canada is seeing rising adoption of enzymatically interesterified fats in premium snacks, infant nutrition, and plant-based products. Leading players are expanding tailored fat systems, modernizing refineries, and strengthening collaborations with confectionery, bakery, and nutraceutical companies. The trend toward sustainably sourced palm, shea, and kernel fractions, combined with investments in advanced fractionation and R&D-driven customization, is shaping a highly innovation-focused regional market.

Asia Pacific Industrial Fat Fraction Market Trends

Asia Pacific industrial fat fraction market is expected to grow at a CAGR of 5.1% as manufacturers across the region accelerate modernization of fractionation, specialty fat customization, and clean-label sourcing. China is witnessing strong demand for tailored mid-fractions in confectionery, instant foods, and bakery chains seeking heat-stable coatings. India’s processed food sector is rapidly integrating structured vegetable fats into snacks, dairy alternatives, and affordable chocolate compounds. Japan continues to lead in precision lipid engineering for pharmaceuticals, cosmetics, and ultra-refined food applications.

South Korea is expanding the use of specialty fats in premium bakery, K-snacks, and functional beverages, driven by rising consumer interest in texture and better-for-you formulations. Growing investments in palm, shea, and kernel-based fractions and region-specific R&D are reshaping the Asia Pacific’s fat innovation landscape.

Competitive Landscape

The global Industrial Fat Fraction market operates as a moderately consolidated landscape where leading processors leverage scale, advanced refining, and strategic sourcing to strengthen their competitive edge. Major players are investing heavily in precision fractionation, enzymatic interesterification, and tailored melting profiles to meet the evolving needs of bakery, confectionery, nutraceutical, and personal-care manufacturers. Product development is shifting toward high-stability mid-fractions, clean-label vegetable fat systems, and application-specific blends that enhance texture, structure, and performance. Companies are rapidly expanding B2B partnerships, supplying custom fat solutions to large food processors seeking consistency and formulation efficiency. Collaborations across ingredient houses, chocolate manufacturers, and bakery chains are accelerating the launch of innovative fat systems while reinforcing long-term supply chain reliability and technical support capabilities.

Key Industry Developments:

- In May 2025, the Danish government joined forces with Preferred by Nature, Ferrero, SAN, Agriterra, and Musim Mas to advance sustainable palm oil production in Indonesia. The collaboration focuses on strengthening responsible sourcing, improving farmer livelihoods, and accelerating deforestation-free supply chains.

- In May 2025, Cargill secured the top position in the first-ever Edible Oil Supplier Index released by the Access to Nutrition Initiative. The recognition highlights its achievement in eliminating industrially produced trans fats from its global edible oils portfolio, including regions without regulatory requirements.

Companies Covered in Industrial Fat Fraction Market

- AAK AB

- Cargill, Incorporated

- Bunge Limited

- Wilmar International Limited

- Fuji Oil Holdings Inc.

- IOI Group

- Fonterra Co-operative Group Limited

- Mewah International

- Musim Mas Holdings

- Olam International

- Others

Frequently Asked Questions

The global industrial fat fraction market is projected to be valued at US$ 12.3 Bn in 2026.

Growing demand for processed foods and snack products is fueling momentum across the global Industrial Fat Fraction market.

The global Industrial Fat Fraction market is poised to witness a CAGR of 4.2% between 2026 and 2033.

Rising adoption of cocoa-butter substitutes is creating a strong strategic growth avenue for specialty fat processors.

Major players in the global Industrial Fat Fraction market include AAK AB, Cargill, Incorporated, Bunge Limited, Wilmar International Limited, Fuji Oil Holdings Inc., and others.