- Plastics, Polymers & Resins

- High Performance Plastics Market

High Performance Plastics Market Size, Share, Trends, and Growth Forecast for 2025 - 2032

High Performance Plastics Market by Product Type (Fluoropolymers, High Performance Polyamides, Aromatic Ketone Polymers, PPS, SP, LCP, Others), End-use Industry (Transportation, Electricals and Electronics, Industrial, Medical, Other), and Regional Analysis from 2025 - 2032

High Performance Plastics Market Size and Trends

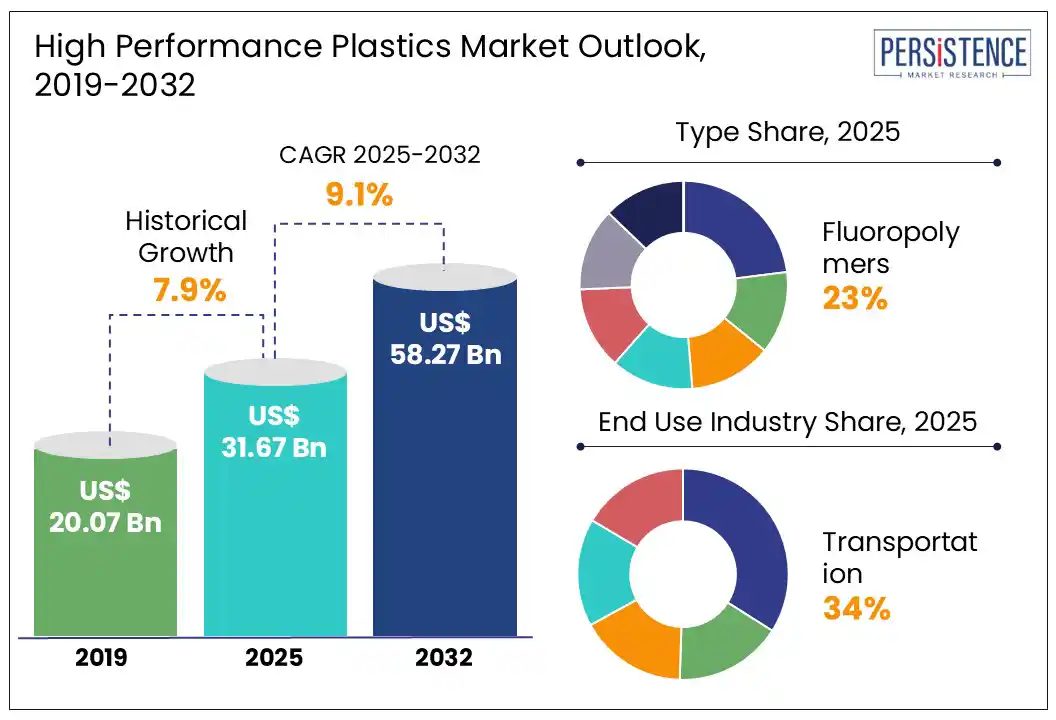

The global high performance plastics market is likely to be valued at US$ 31.67 Bn in 2025 to US$ 58.27 Bn by 2032, growing at a CAGR of 9.1% during the forecast period 2025 to 2032.

According to the Persistence Market Research report, the high performance plastics market expected to be driven by miniaturization, electrification and focus on sustainability regulations across several sectors. Automotive OEMs are progressively focusing on recyclable or bio-based grades, pushing the market players to develop high-temperature efficient polymers.

Key Industry Highlights:

- Rising interest of OEMs in HPPs due to its lightweight, high-strength properties continues to drive the market demand, particularly in transportation and semiconductor industries.

- The high cost of resins and the need for specialized processing equipment keep the total cost of ownership elevated, limiting the market expansion in cost-sensitive applications.

- The growing EV industry, the rollout of 5G infrastructure, and increased demand for single-use healthcare devices are creating new high-margin market opportunities for the high performance plastics market.

- Based on type, fluoropolymers lead the market, due to their superior chemical and thermal resistance, making them essential in wiring, seals, and semiconductor applications.

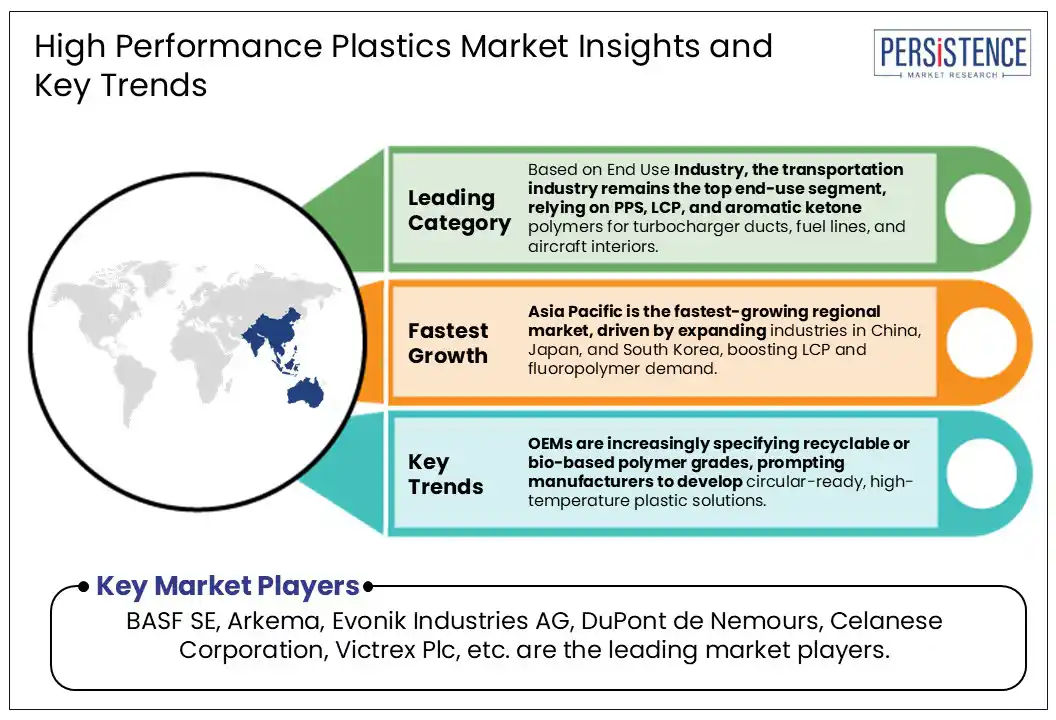

- Based on end-user industry, the transportation industry remains the top end-use segment, relying on PPS, LCP, and aromatic ketone polymers for turbocharger ducts, fuel lines, and aircraft interiors.

- North America maintains stable demand, maintaining a share of 29%, supported by strong aerospace and medical-device industries, a shale-gas feedstock advantage, and automotive light-weighting trends driving PPS and HPPA use.

- Europe high performance plastics are poised to grab 23% share and is driven by strict environmental regulations and the adoption of recyclable HPP, supported by strong collaboration between OEMs and polymer producers.

- Asia Pacific is the fastest-growing regional market, with a share of 35%, driven by expanding industries in China, Japan, and South Korea, boosting LCP and fluoropolymer demand.

|

Global Market Attribute |

Key Insights |

|

High Performance Plastics Market Size (2025E) |

US$ 31.67 Bn |

|

Projected Market Value (2032F) |

US$ 58.27 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

9.1% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

7.9% |

Market Dynamics

Driver - Light weighting in EV industry propel demand for high-performance plastics

The high-performance plastics market is heavily driven by the shift of OEMs to improve the products efficiency. The significant growth in the EV industry results leads the automotive manufacturers replacing metals with HPPs to reduce the vehicle weight for better fuel efficiency. The electronics manufacturers are also investing in HPPs due to their suitable properties in device miniaturization.

The government regulations are also favoring the market growth. Euro 7 standards in Europe and CAFE regulations in the U.S., are demanding significant reductions in vehicle emissions and energy consumption. HPPs offer excellent strength, thermal stability, and corrosion resistance, making them ideal for components such as engine housings, battery enclosures, and connectors.

Leading market players are intensely focusing on investing in high-performance plastics. For instance, in March 2025, BASF introduced the world's first biomass-balanced Polyethersulfone high-performance thermoplastic, Ultrason ® E 2010 BMB. Ultrason® E 2010 BMB contributes to substituting fossil resources, reducing greenhouse gas emissions, and increasing the use of renewable feedstock. It applies to industries as diverse as household and catering, automotive, electrical and electronics (E&E), healthcare, and water and sanitary to differentiate their products from the competition.

Restraint - Capital-intensive processing and trade tariffs suppress high-performance plastics adoption

The advanced processing in the production of HPPs and high resin prices hinders the market growth. The HPPs require advanced compounding, tight molding tolerances, and high-temperature processing which results in increase capital and operational expenses.

The rise in geopolitical tensions results in the rise in the plastic prices. In March 2025, the Trump administration placed 25 % duties on Canadian and Mexican polymers, and the hike on Chinese imports from 10 % to 20 %. It has triggered retaliatory tariffs of up to 15 % from China, 25 % from Canada. This challenge is compounded by ongoing volatility in global supply chains and rising input costs.

The manufacturers are responding to the rising plastic prices by increasing the product prices. For instance, in May 2025, Celanese Corporation announced the raise in prices across its specialty polymer portfolio, citing increased costs related to raw materials, logistics, plant operations, and shifting trade regulations. These hikes, effective June 2025, reflect broader industry pressures that elevate the total cost of ownership for OEMs and processors.

Opportunity - Electrification and biocompatibility create new opportunities for strategic investment in high-performance plastics

The global shift toward electrification, digital connectivity, and advanced healthcare is creating an opportunity for high-performance plastics. The EVs requires lightweight, thermally stable, and electrically insulating materials for many parts such as battery housings and powertrain components. The rising competition in EV industry leads the manufacturers to apply HPPs solutions to address the above conditions.

The innovation in the HPPs to make it biodegradable as well as follows the environmental regulations. In the healthcare sector, the rise of single-use medical devices and strict sterility norms are increasing reliance on biocompatible, high-strength plastics.

The manufacturers are investing in the innovations considering the above conditions. For instance, in October 2023, Victrex plc, launched a new product grade developed exclusively for Drug Delivery and Pharmaceutical Contact applications. VICTREX PC™101 meets the highest levels of Industry biocompatibility certification for USP Class VI and also meets industry standards such as USP 661 for use in non-implantable pharmaceutical contact applications.

Category-wise Analysis

Type Insights

Fluoropolymers are leading the high-performance plastics market, primarily due to their high thermal stability and electrical insulation properties. These properties lead the fluoropolymers in products such as wiring insulations, seals, and gaskets, which are exposed to extreme environments.

Rising government investments in semiconductor industry, such as the U.S. CHIPS Act and India’s Semicon India Programme, are further driving demand for fluoropolymer in semiconductor industry. The CHIPS and Science Act of 2022 of U.S. is focusing on domestic semiconductor manufacturing and reduction in reliance on foreign supply chains. The Act allocates over $52 billion in federal subsidies, tax incentives, and R&D funding.

Following the government’s investment, the manufacturers are investing heavily in fluoropolymers. For instance, in May 2025, DuPont announced its participation in SEMICON Southeast Asia, taking place May 20-22, 2025, in Singapore. At booth L3105, DuPont showcased the latest offerings of Kalrez® perfluoroelastomer parts specifically designed for semiconductor and electronics applications, aimed at enhancing manufacturing efficiency and operational sustainability. Such initiatives highlight how fluoropolymers remain indispensable to new technologies and infrastructure, sustaining their leading market position.

End Use Industry Insights

The transportation sector is dominating the High-performance plastics market, driven by rising demand for lightweight, high-strength, and heat-resistant materials. These properties help the manufacturers to reduce vehicle weight, improve fuel efficiency, and meet the emission regulations more efficiently. Products such as fuel-line systems, powertrain components and air ducts drives the demand for polymers such as PPS, LCP, and aromatic ketone polymers.

The government regulatory measures such as Euro 7 standards and U.S. EPA GHG Phase 3 rules, are driving manufacturers to lower vehicle’s GHG emissions and improve the energy efficiency. Euro 7 standards set strict limit on pollutants such as nitrogen oxides and particulates aiming to reduce urban air pollution. These regulations drive the demand of HPPs from the automotive manufacturers.

The market players are investing in innovations on HPP based products due to rising demand from automotive manufacturers. For instance, in October 2024, BASF developed a polyphthalamide that is especially suited for manufacturing housings of insulated-gate bipolar transistors. Ultramid® Advanced N3U41 G6 addresses the growing demand for high-performance, reliable electronic components, e.g., electric vehicles, high-speed trains, smart manufacturing, and the generation of renewable energy.

Regional Insights

North America High Performance Plastics Market Trends

North America high performance plastics market is fairly matured yet innovative, supported by advanced aircraft, medical, and automotive industries. The U.S. market is driven by the consistent demand for biocompatible polymers, including HPPs due to their lightweight and thermal stability properties.

The U.S. High-performance plastics market demands more due to rising focus on sustainability from industries and government. In November 2024 the EPA released its National Strategy to prevent plastic pollution, mapping actions to eliminate land-based plastic leakage by 2040 and create certification programs for low-impact materials.

The market players are also following the government’s strategy to reduce plastic waste by investing in product innovation. For instance, in October 2024, Celanese Corporation introduced three new sustainable engineering thermoplastics, Hostaform® | Celcon® POM ECO-C, Zytel® PA ECO-R, Vectra® | Zenite® LCP ECO-B.

Europe High Performance Plastics Market Trends

Europe’s high-performance plastics market is mature but powered by policies. The stringent environmental regulations and strong focus on material sustainability drive the market. The EU “Plastics Transition” roadmap commits the sector to a circular, net-zero model by 2050 and positions plastics as a strategic asset for the Green Deal.

In February 2025, the European Commission approved a €500 million French scheme that reimburses up to 40 % of capital costs for chemical-recycling plants, creating fresh quality feedstock. Such incentives support the technology scale-up and secure the supply chain of raw materials for premium fluoropolymer, PPS, and LCP compounds.

The market players are also focusing on sustainability in various ways. In November 2024, Arkema and Authentic Material partner to offer innovative and more sustainable materials for the luxury goods market and beyond. The partnership leverages Arkema’s leadership position in the design, manufacture, and recycling of advanced bio-circular materials and the proprietary expertise of Authentic Material in leather recycling.

Asia Pacific emerges as global growth hub for high-performance plastics market

Asia Pacific is the fast-growing market in high-performance plastics market, driven by rapid industrialization and rising investments in semiconductor industries in China, Japan, and South Korea. These industries demand HPPs for applications requiring high thermal and chemical stability.

Government initiatives such as China’s “Made in China 2025” and South Korea’s K-Semiconductor strategy further promotes the local manufacturers to invest in the high performance plastic’s innovation.

The global manufacturers are also investing in the innovation in the market. For instance, in November 2024, SABIC inaugurated its US$170 million ULTEM™ resin manufacturing facility in Singapore, significantly boosting the regional supply of premium thermoplastics.

As Asia Pacific accelerates its shift toward high-tech and sustainable manufacturing, it remains the global growth engine for the High-performance plastics market.

Competitive Landscape

The high-performance plastics market is highly fragmented, driven by strategies focused on innovation and growing focus on sustainability. Leading players such as BASF, DuPont, Arkema, SABIC, Celanese, and Victrex are continuously expanding their portfolios through bio-based materials.

Companies are successfully following sustainability regulations while delivering innovative, cost-effective solutions. A prime example is Arkema’s acquisition of a 54% stake in South Korea’s PI Advanced Materials in June 2023, strengthening its position in the high-temperature polyimide segment for electronics and mobility. The competitive landscape is thus shaped by global players that leverage advanced materials science, regional manufacturing footprints, and sustainability-focused innovation to secure long-term market leadership.

Recent Industry Developments:

- In April 2025, DuPont announced the launch of DuPont™ Liveo™ Pharma TPE Ultra-Low Temp Tubing, a new thermoplastic elastomer tubing designed to withstand the low temperatures required for many biopharmaceutical processing applications.

- In January 2025, SABIC unveiled its new polypropylene pipe solution, which is made with a random copolymer. The new solution, SABIC VESTOLEN P9421, aims to provide improved properties at high pressures and temperatures with enhanced durability and reliability.

Companies Covered in High Performance Plastics Market

- Solvay

- BASF SE

- Arkema

- Evonik Industries AG

- Daikin Industries Ltd

- DuPont De Nemours

- SABIC

- Celanese Corporation

- Victrex Plc

- Saint-Gobain Performance Plastics

- DSM

Frequently Asked Questions

Yes, the market is set to reach US$ 58.3 Bn by 2032.

India is estimated to witness a CAGR of 10.5.0% in forecast period.

BASF SE is considered the leading player of the high performance plastics market.

The rise in 5G infrastructure and increased demand for single-use healthcare devices are creating the opportunities for the high performance plastic market.

The rising interest of OEMs in high performance plastics due to its lightweight and high strength properties is propelling the market growth.