- Processed Food

- High Protein Yogurt Market

High Protein Yogurt Market Size, Share, and Growth Forecast, 2026 - 2033

High Protein Yogurt Market by Product Type (Spoonful, Drinkable), Nature (Conventional, Organic), Source (Dairy Based, Plant Based), Flavor (Regular, Fruit Flavored, Other Flavor), Distribution Channel (Supermarket, Others), and Regional Analysis 2026 - 2033

High Protein Yogurt Market Share and Trends Analysis

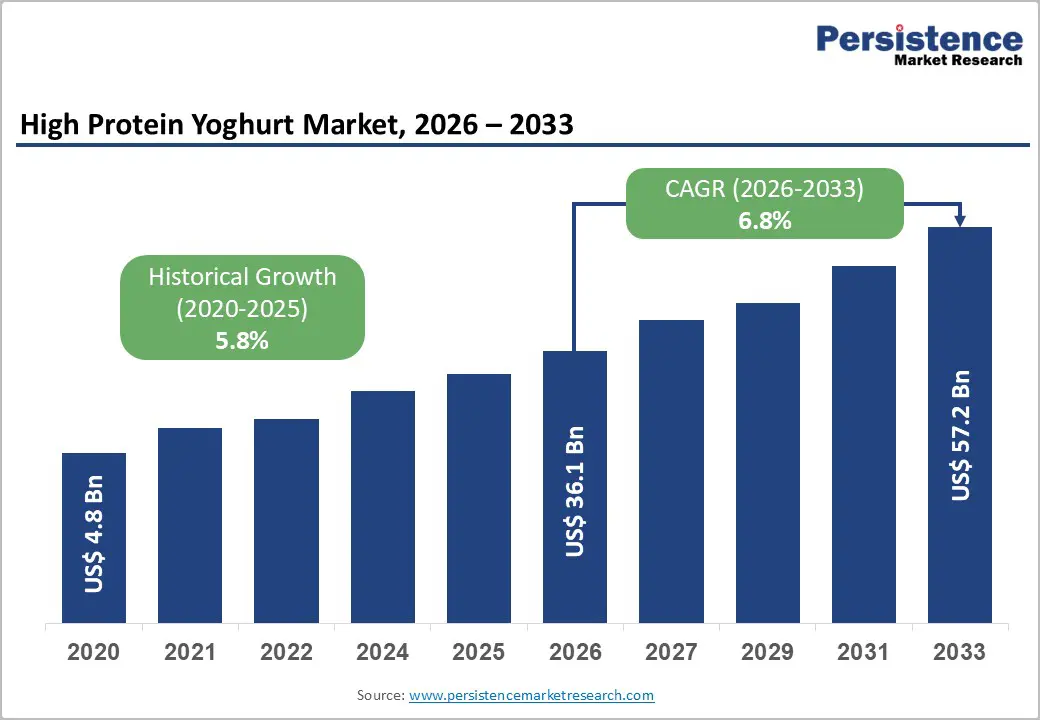

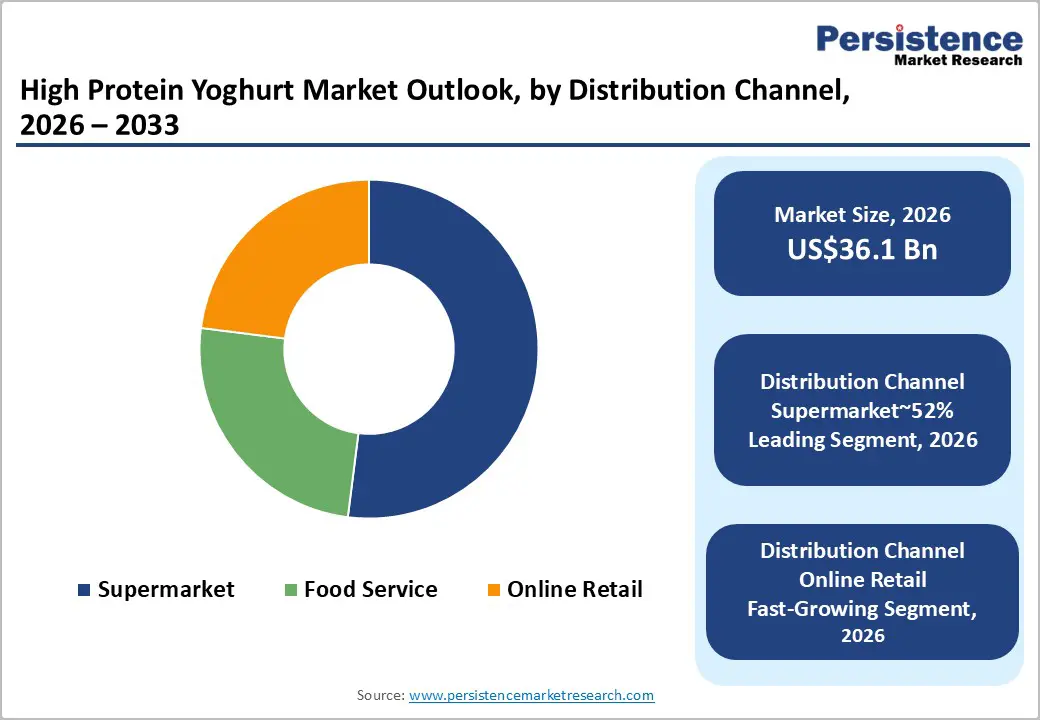

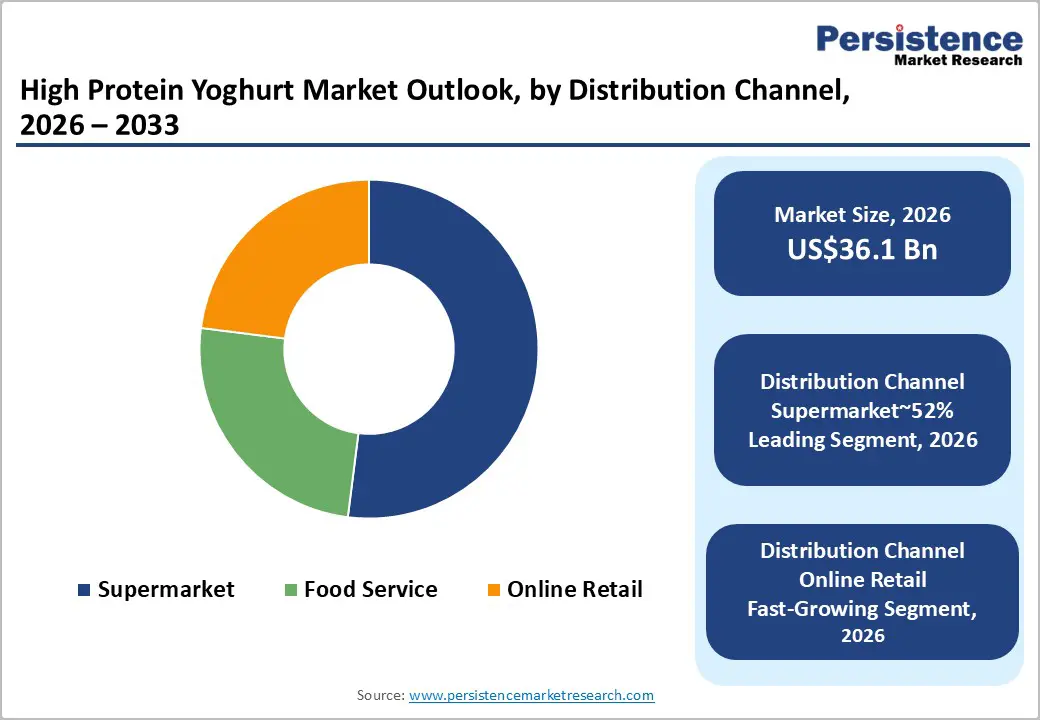

The global high-protein yogurt market size is projected to be valued at US$36.1 billion in 2026 and is projected to reach US$57.2 billion by 2033, growing at a CAGR of 6.8% during the forecast period between 2026 and 2033, driven by the global shift toward proactive healthcare and the snackification of protein-dense foods. Innovations in filtration technologies, such as ultrafiltration and microfiltration, have enabled manufacturers to increase protein concentration without compromising the product's sensory profile or mouthfeel.

Key Industry Highlights:

- Leading Market Region: North America is expected to dominate the high-protein yogurt market, accounting for 42% market share in 2026, driven by established retail networks, high consumer protein awareness, and mature market adoption.

- Fastest-growing Market Region: Asia Pacific is expected to be the fastest-growing region, fueled by rapid urbanization, expanding middle-class consumption, and increasing adoption of ambient-stable, drinkable, and plant-based high-protein yogurt.

- Leading Product Type: Spoonful yogurt is projected to remain the leading format with 70% consumption share in 2026, anchored by entrenched consumer familiarity, shelf economics, and alignment with premium dairy positioning.

- Leading Distribution Channel: Supermarkets and hypermarkets are expected to remain dominant with 52% share, driven by scale efficiencies, entrenched shopping habits, and strong in-store visibility for mainstream adoption.

- Key Industry Developments: In November 2025, Arla Foods Ingredients showcased a world-first transparent high-protein yogurt at Fi Europe. The development of a clear, transparent, high-protein format removes the "heavy/milky" barrier for consumers, opening new consumption windows in the hydration and refreshment categories.

| Key Insights | Details |

|---|---|

|

High Protein Yogurt Market Size (2026E) |

US$36.1 Bn |

|

Market Value Forecast (2033F) |

US$57.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.8% |

Market Dynamics - Growth, Barrier, and Opportunity Analysis

Rising Global Health and Wellness Consciousness

Protein consumption has shifted from a niche sports-nutrition focus to a mainstream dietary priority, reshaping demand dynamics across the yogurt category. Retail performance indicators in developed markets show high-protein offerings consistently outperforming conventional yogurt, reflecting a sustained recalibration of consumer value perception toward functional nutrition.

This shift is reinforced by increased protein salience in purchase decisions, particularly among younger, fitness-oriented cohorts influenced by digital wellness ecosystems, gym culture, and evidence-based messaging on satiety and muscle maintenance. The result is a demand profile increasingly anchored in daily nutritional optimization rather than episodic performance use.

In parallel with protein prioritization, digestive wellness has emerged as a reinforcing consumption driver, strengthening the commercial position of probiotic-enriched, high-protein formulations. Consumer preference data indicate increasing receptivity to products that combine macronutrient density with gut health benefits, positioning functional yogurt as a dual-purpose staple for breakfast and snacking occasions.

This convergence of protein adequacy science and gastrointestinal health awareness creates durable demand momentum, supporting premiumization while favoring manufacturers capable of substantiating health claims through formulation credibility and regulatory-aligned communication.

High Production Costs and Premium Pricing Barriers

The cost-intensive nature of protein concentration remains a core structural restraint within the high-protein yogurt value chain. Filtration-heavy production models materially increase milk input requirements, amplifying exposure to upstream raw milk volatility.

Feed cost inflation and climate-related pressures on livestock productivity further intensify input price variability, thereby directly compressing processors' margins. These dynamics structurally elevate unit economics relative to conventional yogurt, limiting pricing flexibility even for scaled manufacturers with procurement leverage.

Downstream, elevated production costs are passed through as sustained retail price premiums, constraining addressable demand in price-sensitive markets. In Southeast Asia and parts of Latin America, high-protein yogurt adoption remains concentrated within upper-income urban cohorts, slowing penetration beyond niche consumption occasions.

This uneven affordability profile reinforces market fragmentation and delays volume-led expansion, positioning cost efficiency, alternative protein sourcing, and process optimization as critical determinants of long-term competitiveness rather than brand-led demand creation alone.

Technological Advancements in Fortification and Bioavailability

Technological convergence between food processing and biotechnology is redefining the opportunity landscape for high-protein yogurt by addressing longstanding constraints around protein efficiency, sourcing stability, and formulation flexibility. Precision fermentation enables the production of bio-identical dairy proteins without reliance on livestock, positioning the technology as a structural solution rather than a peripheral innovation. This shift reduces exposure to agricultural volatility, lowers dependence on filtration-intensive processes, and aligns with tightening environmental and sourcing expectations across developed markets.

As regulatory frameworks mature, manufacturers adopting fermentation-enabled protein platforms improve margin durability while maintaining functional equivalence to conventional dairy proteins. Technology adoption increasingly determines competitive positioning, favoring players with capital scale, regulatory readiness, and vertically integrated processing capabilities.

Manufacturers are also expanding category value by embedding functional health attributes directly into high-protein yogurt formulations. The integration of probiotics, prebiotics, postbiotics, and adaptogenic ingredients elevates the category from a macronutrient solution to a broader wellness platform aligned with holistic nutrition behaviors.

This convergence supports premium pricing, expands the number of consumption occasions, and reduces reliance on lifestyle branding alone. Market analyses identify functional high-protein yogurt as a distinct opportunity pool, particularly in regions with high health literacy and established pathways for functional claims. Long-term success depends on formulation credibility.

Category-wise Analysis

Product Type Insights

Spoonful yogurt is expected to anchor the high-protein yogurt category, accounting for 70% of product type consumption and maintaining leadership as the category’s structural baseline. This format benefits from entrenched consumer familiarity, established retail shelf economics, and strong alignment with premium dairy positioning. Producers use spoonful formats to reinforce perceptions of craftsmanship, ingredient quality, and nutritional credibility, supporting margin stability despite slower velocity.

Demand patterns signal maturity across developed markets, with growth increasingly dependent on premiumization levers, including functional fortification, clean-label formulations, and sustainable packaging. Regulatory scrutiny of health claims and protein concentration methods further reinforces scale and compliance capabilities as key competitive filters in this segment.

Drinkable yogurt is likely to emerge as the fastest-growing format, driven by portability, convenience, and integration into on-the-go nutrition routines. This format aligns with evolving consumption occasions, digital retail penetration, and direct-to-consumer distribution models, reinforcing volume momentum.

Producers position drinkable formats to capture incremental demand by combining high protein density with digestive health functionality, expanding relevance beyond traditional dairy usage.

As adoption accelerates, execution advantages increasingly hinge on cold-chain efficiency, formulation stability, and regulatory-aligned functional claims, positioning drinkable yogurt as the primary growth engine within the product type landscape.

In 2026, Danone’s Oikos Pro Fusion is a prime example of a drinkable yogurt designed to drive market growth through specialized, on-the-go nutrition. The drinkable format is positioned as a seamless, ready-to-consume breakfast or post-workout snack that requires zero preparation.

Distribution Channel Insights

Supermarkets and hypermarkets are projected to remain the dominant channel in 2026, capturing approximately 52% of the total share and sustaining leadership through scale efficiencies, entrenched shopping habits, and strong in-store visibility. These formats continue to drive mainstream adoption by facilitating price comparison, impulse buying, and brand discovery among mass consumers.

Structural pressures are mounting as retailers optimize refrigerated shelf space, increase private-label penetration, and enforce more stringent listing and margin requirements. Increasing functional segmentation within yogurt aisles further consolidates advantage among large manufacturers with robust trade-spend capabilities, compliant labeling, and dependable supply chains. While supermarkets continue to lead in volume, their incremental growth potential is moderating, underscoring the growing importance of complementary channels for future expansion.

The food service channel, encompassing hotels, restaurants, and cafés (HoReCa), is emerging as the fastest-growing distribution segment, driven by shifting consumption patterns and lifestyle changes. The growing “snackification” of meals has led consumers to replace traditional dining with frequent, nutrient-dense snacks, boosting demand across cafés, quick-service restaurants, and transit-oriented outlets. Convenience and on-the-go accessibility are central growth drivers, supported by ready-to-eat, drinkable, and pre-portioned formats that require minimal preparation and align with operational efficiency needs.

Rising fitness and wellness awareness further accelerates adoption, positioning high-protein and functional offerings as staples for post-workout recovery and everyday nutrition. In emerging markets, increasing disposable incomes and urbanization are encouraging protein-rich, Western-style diets.

Menu innovation in HoReCa includes integrating high-protein products into smoothie bowls, breakfast combinations, and artisanal bakery items, alongside premiumization through exotic flavors and indulgent textures. Expanding plant-based options, weight-management formats, and sustainable packaging adoption further reinforce the channel’s strategic role in reaching health-conscious, convenience-driven consumers.

Regional Insights

North America High Protein Market Trends

North America is expected to lead the global high-protein yogurt market, accounting for roughly 42% of the total market share, with the U.S. serving as the dominant country-level contributor. Regional leadership is supported by advanced retail and foodservice distribution networks, high per-capita yogurt consumption, and a deeply entrenched health- and fitness-oriented consumer base that actively prioritizes protein intake. Supportive regulatory frameworks allow functional claims and rapid product innovation, while a mature cold-chain infrastructure enables efficient scaling across both mass-market and premium segments.

Sustained demand for Greek-style and other high-protein yogurt formats underpins growth, even as overall volumes mature. Single-serve packaging, mix-in concepts, fortified formulations, and drinkable yogurt formats enhance convenience and profitability, particularly within on-the-go nutrition routines. Clean-label and organic positioning further strengthens regional appeal, as consumers are willing to pay premiums for traceability, low or no added sugar, and functionally positioned products delivering 15–35 grams of protein per serving.

To defend pricing and margins, manufacturers are increasingly deploying AI-driven production optimization and precision fermentation technologies to improve texture, extend shelf life, and preserve clean-label credentials. FDA initiatives, such as guidance on high-protein labeling and expanded allowances for ingredients and non-nutritive sweeteners, reduce regulatory uncertainty and accelerate product development. Fitness-oriented marketing narratives, reinforced by sports nutrition partnerships, continue to normalize protein-rich diets across demographic groups.

Market concentration among incumbents strengthens scale-driven innovation while raising entry barriers. Leading players, including Danone North America (Oikos), Chobani, and General Mills (Yoplait), collectively control an estimated 30–42% of the regional market. Overall, North America’s regulatory clarity, infrastructure maturity, and premium consumer orientation position it as both a structural leader and a global benchmark for innovation.

Europe High Protein Yogurt Market Trends

Europe is expected to continue growing, with Germany, the U.K., France, and Spain representing the largest individual markets. Nordic countries lead in per-capita consumption, supported by established dietary habits and high awareness of functional nutrition. The region benefits from harmonized regulatory frameworks, including EC Regulation 1169/2011 and EFSA health claim guidelines, which, despite requiring compliance, strengthen the premium positioning of products.

Organic, GMO-free, and sustainability-certified yogurts consistently command retail premiums, while regional fortification standards and novel-food approvals shape product innovation timelines. Strong baseline consumption, combined with institutional preference for certified products, provides a stable foundation for growth in both volume and value.

Growth drivers vary across European markets. In Germany and the U.K., health-conscious and sustainability-focused consumers are accelerating the adoption of plant-based and clean-label products, while France and Spain capitalize on traditional yogurt culture and alignment with the Mediterranean diet to reinforce premium positioning.

Strong regulatory oversight and supply-chain compliance favor scale-driven players, particularly multinational and cooperative producers with established certifications and distribution networks. Private-label penetration further shapes competitive dynamics, especially in Northern Europe.

Investment is increasingly focused on plant-based innovation, functional fortification, and sustainability certification. The combination of stringent regulations, health-conscious demand, and structured premiumization positions Europe as a growth-oriented yet compliance-intensive market within the global high-protein yogurt sector.

Asia Pacific High Protein Yogurt Market Trends

Asia Pacific is poised to be the fastest-growing regional segment in the global high-protein yogurt market, driven by structural demographic and economic shifts. Rapid urbanization across China, India, Southeast Asia, and Vietnam is expanding refrigeration infrastructure and access to premium dairy, while rising middle-class populations broaden the addressable base for protein-enriched products.

Cultural familiarity with fermented dairy traditions such as lassi, curd, and kefir supports adoption, particularly among younger consumers influenced by social media, fitness culture, and functional nutrition awareness.

To overcome persistent cold-chain gaps, especially in rural India and Southeast Asia, manufacturers are scaling ambient, shelf-stable high-protein yogurt. Companies such as Yili, through its Ambrosial brand, have refined advanced heat-treatment and aseptic packaging technologies that allow protein-dense yogurt to be sold through non-refrigerated kiosks, materially extending market reach. E-commerce platforms, increasingly dominant in urban centers, further enable domestic and international brands to penetrate tier-two and tier-three cities efficiently.

Country-level dynamics reinforce growth momentum. In China, urban consumers favor premium brands and ambient-stable formulations that mitigate logistics constraints. India benefits from dairy fortification mandates, organized retail expansion, and drinkable yogurt formats aligned with traditional consumption habits. Japan and South Korea demonstrate more selective adoption, emphasizing functional benefits and premium positioning amid aging demographics.

Competitive Analysis

The global high-protein yogurt market is moderately consolidated, with the top five players, including Danone, General Mills, Chobani, Fage, and Lactalis, controlling approximately 55% of total market revenue. Leading companies maintain competitive advantage through scale-driven procurement efficiencies, dedicated innovation budgets, and established retail relationships that secure premium shelf positioning.

They actively acquire smaller disruptor brands to access niche technologies and younger consumer bases, reinforcing their market influence and enabling product differentiation in organic, plant-based, and functional segments.

Regional and emerging sub-segments remain fragmented, particularly in Europe and Asia-Pacific, where specialized health-food brands and direct-to-consumer players target underserved consumer niches. Conventional segments face intense price competition, while plant-based and functional categories experience innovation-driven rivalry.

Market growth is supported by digital channel adoption, sustainability-focused product narratives, and functional ingredient innovation, allowing new entrants to capture high-value demand, while established players continue to consolidate mainstream segments and strengthen strategic positioning.

Key Industry Developments:

- In November 2025, Danone North America introduced 'Silk Protein', a high-protein plant-based dairy range. Offering 13g of complete plant protein per serving helps bridge the "protein gap" that has historically caused plant-based yoghurts to lag behind dairy, potentially revitalizing the struggling vegan dairy sector.

- In March 2025, Danone expanded its U.K. portfolio with the launch of a new Icelandic-style 'Skyr' range. This launch capitalizes on the "non-HFSS" (HIGH IN FAT, SALT, OR SUGAR) regulatory environment in the U.K., providing a high-protein, zero-fat solution that satisfies European health labeling standards.

Companies Covered in High Protein Yogurt Market

- Danone S.A.

- Chobani, LLC

- Groupe Lactalis

- Fage International

- Arla Foods Amba

- Müller Group

- Nestlé S.A.

- Greek Gods

- The Kraft Heinz Company

- Epigamia

- Noosa Yogurt

- Liberté

- Valio Ltd.

- Stonyfield Farm

Frequently Asked Questions

The global high protein yogurt market is projected to be valued at US$36.1 billion in 2026 and is expected to reach US$57.2 billion by 2033, driven by the global shift toward proactive healthcare and protein-dense snacking.

Demand is rising due to the global prioritization of health and wellness, the "snackification" of protein-rich foods, and consumer preference for convenient, functional nutrition that supports satiety, muscle maintenance, and digestive wellness.

The global high protein yogurt market is forecast to grow at a CAGR of 6.8% from 2026 to 2033, supported by innovations in protein fortification and expanding distribution channels.

Asia Pacific is the fastest-growing regional market, fueled by rapid urbanization, rising middle-class populations, government fortification mandates, and the expansion of e-commerce platforms in China and India.

Key players include Danone S.A., General Mills, Chobani LLC, Groupe Lactalis, and Fage Internationals.