- Specialty & Fine Chemicals

- Polyphthalamide Market

Polyphthalamide Market Size, Share, and Growth Forecast, 2025 - 2032

Polyphthalamide Market By Product Type (Unfilled PPA, Others), Application (Automotive, Electrical & Electronics, Others), Technology (Flame-Retardant PPA, Bio-based/Sustainable PPA, Others), and Regional Analysis for 2025 - 2032

Polyphthalamide (PPA) Market Share and Trends Analysis

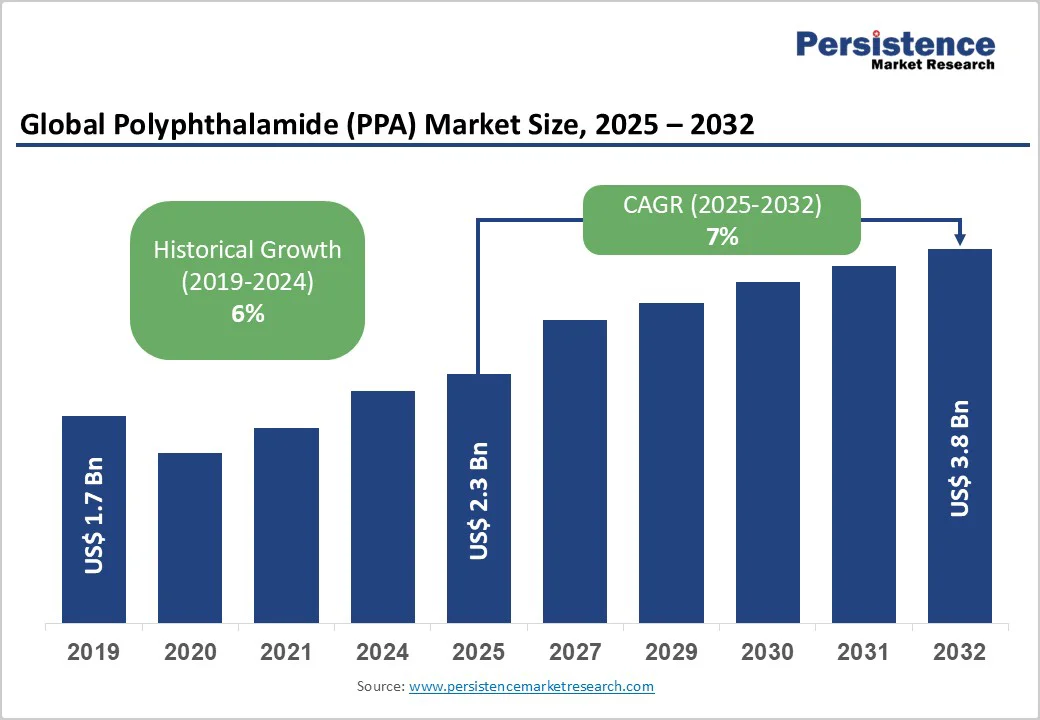

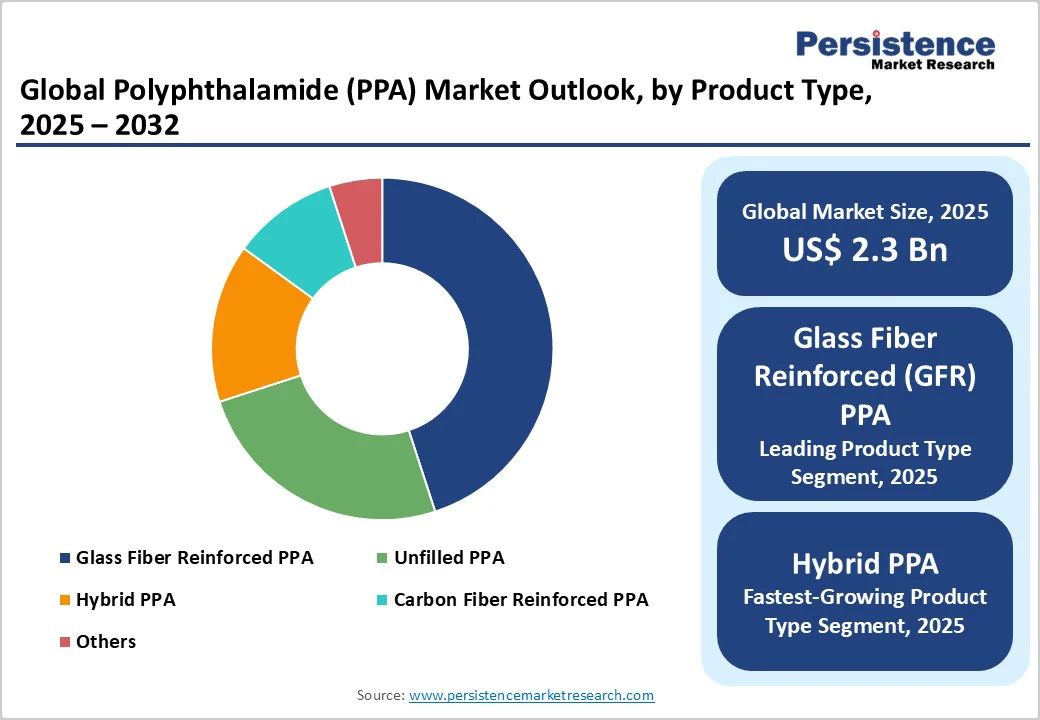

The global polyphthalamide market size is likely to be valued at US$2.3 Billion in 2025, and is estimated to reach US$3.8 Billion by 2032, growing at a CAGR of 7% during the forecast period 2025 - 2032, driven by the rising demand for advanced polymers in automotive electrification, high-performance electronics, and industrial applications.

The polyphthalamide (PPA) market is expanding due to stringent emission norms favoring lightweight materials, rising EV adoption, and growing demand for polymers with thermal and flame-retardant properties.

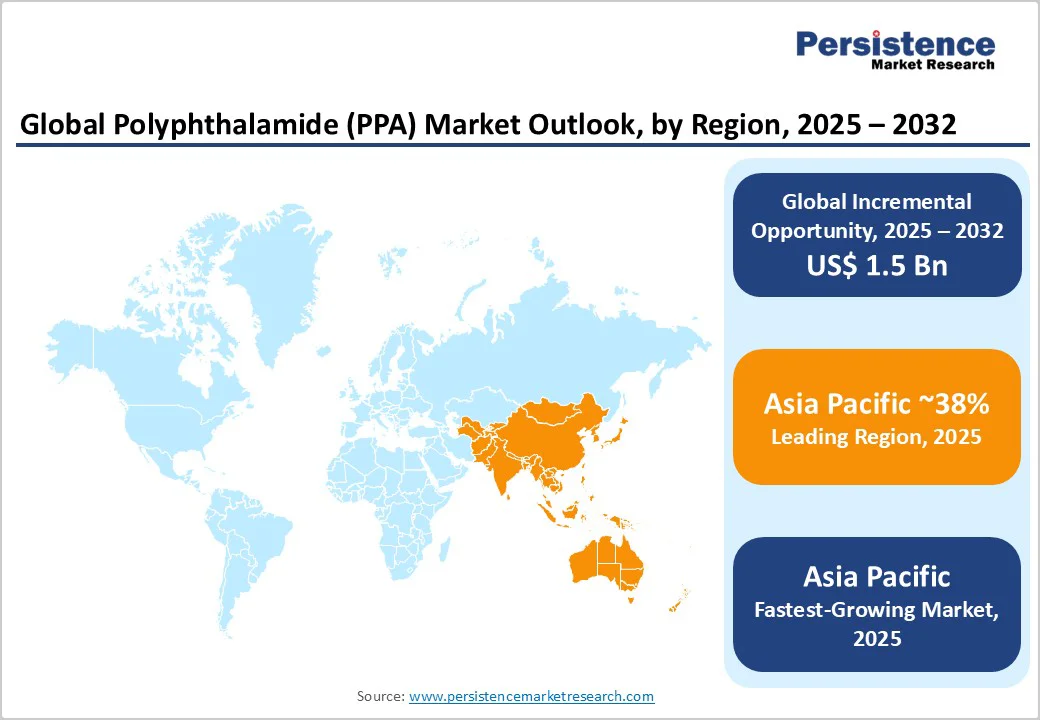

Advancements in bio-based formulations and sustainability-focused regulations are further driving global growth, with Asia Pacific leading consumption, followed by North America and Europe.

Key Industry Highlights

- Leading & Fastest-growing Product Types: Glass fiber reinforced PPA leads product types with a 45% share in 2025; hybrid PPA is projected to be the fastest-growing through 2032.

- Dominant & Fastest-growing Applications: Automotive applications dominate with 38% share in 2025, while the electrical & electronics sector is set to grow the fastest during 2025 - 2032.

- Leading & Fastest-growing Technologies: Flame-retardant PPAs are likely to hold about 40% of the revenue share in 2025, whereas bio-based formulations are slated to register the highest 2025 - 2032 CAGR.

- Largest & Fastest-growing Regional Market: Asia Pacific is expected to be the largest and fastest-growing region at 38% market share in 2025, driven by China’s industrial expansion and EV growth.

- Regional Dynamics: North America is set to hold around 23% market share in 2025, led by innovation in polymers and stringent emissions regulations; Europe is anticipated to command around 22% share in 2025, benefiting from regulatory harmonization and advanced manufacturing.

| Key Insights | Details |

|---|---|

| Polyphthalamide (PPA) Market Size (2025E) | US$2.3 Bn |

| Market Value Forecast (2032F) | US$3.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7% |

| Historical Market Growth (CAGR 2019 to 2024) | 6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Electrification and Lightweighting in Automotive Applications

The automotive sector is currently undergoing a transformative shift driven by electrification and the quest for lightweight materials to enhance energy efficiency and reduce emissions. The International Energy Agency (IEA) revealed that global electric car sales surpassed 17 million in 2024, constituting around 20% of the total car sales worldwide.

This surge is likely to intensify the demand for materials such as PPA, which offer exceptional thermal stability, mechanical strength, and electrical insulation for critical components such as battery enclosures, connectors, and sensor housings.

Regulatory frameworks, including the U.S. Corporate Average Fuel Economy (CAFE) standards and the European Union (EU)’s CO2 emission targets, encapsulate this trend by mandating lower vehicle emissions and fuel consumption.

Lightweighting through replacing metals with reinforced PPA lowers fuel use significantly, as per the U.S. EPA estimates, directly enhancing vehicle range and performance while ensuring compliance. The integration of flame-retardant and reinforced PPA grades by original equipment manufacturers (OEMs) caters to the nuanced needs of EV safety and durability, fostering a specialized growth niche for businesses to explore and invest.

Elevated Production Costs and Process Complexity

The adoption of polyphthalamide faces restrictions owing to high production costs and processing challenges that limit broader industrial uptake, especially within cost-sensitive emerging regions. The synthesis of polymer involves expensive raw materials such as aromatic amines and acid chlorides, with rigorous polymerization conditions driving manufacturing expenses substantially above conventional plastics such as polypropylene or standard nylons.

PPA’s high melting point around 285°C necessitates specialized processing equipment and skilled technical expertise for injection molding or extrusion, inflating capital expenditures and operational costs for fabricators. These cost factors, coupled with sensitive supply chain dependencies on volatile raw materials, constrain the penetration of PPA in commodity segments and slow down the pace of innovation.

While strategies toward catalyst optimization and recycling initiatives seek to attenuate these barriers, the economic threshold remains a salient growth inhibitor requiring continuous R&D focus and market education to realize scalable, cost-effective solutions.

Expansion of Bio-based PPA Variants

With escalating global emphasis on sustainability and carbon footprint reduction, the bio-based PPA market segment is emerging as a lucrative opportunity, poised for accelerated growth. Policies such as the European Green Deal and China’s Circular Economy initiatives strongly incentivize manufacturers to adopt renewable raw materials and develop recyclable polymers, catalyzing the relevance of bio-based polyphthalamide.

Lifecycle assessments have validated their potential in lowering greenhouse gas (GHG) emissions notably relative to petroleum-derived counterparts, an attribute increasingly demanded by automotive and electronics manufacturers striving for compliance with environmental, social, & governance (ESG) goals.

Market research indicates bio-based PPA formulations are likely to grow at a high CAGR to 2032, highlighting opportunities for polymer producers to differentiate via eco-innovations and capture green consumer segments. Early adopters leveraging sustainable chemistry and chemical recycling technologies stand to capitalize on regulatory tailwinds, consumer sentiment shifts, and evolving manufacturer mandates, making bio-based PPA a strategically vital growth vector.

Category-wise Analysis

Product Type Insights

By product type, glass fiber reinforced (GFR) PPA dominates, holding a commanding presence with an estimated 45% of the PPA market share in 2025. This segment benefits from the enhanced mechanical strength, stiffness, and heat resistance of polyphthalamide, which are essential for the increasingly stringent performance requirements in automotive under-the-hood components and electrical connectors.

GFR PPA has been extensively adopted as a substitute for metals, balancing lightweighting objectives with the need for structural durability amid regulatory constraints on vehicle emissions and safety standards. The segment growth is supported by automotive OEMs’ focus on improving fuel efficiency and electrical system performance across regions, particularly in mature markets such as North America and Europe.

The fastest-growing sub-segment through 2032 within this category is likely to be hybrid PPA, which combines PPA with other polymers such as polyamides or polyphenylene sulfide to tailor properties including chemical resistance, flexibility, and cost efficiency.

This segment is witnessing a rapid CAGR, driven by a massive demand for customized polymer solutions in aerospace, electronics, and specialized industrial applications. The flexibility in formulation allows manufacturers to target niche requirements for multi-functional materials, enabling new product development with enhanced thermal, mechanical, and flame-retardant properties.

Application Insights

Automotive is slated to be the largest application area, projected to account for roughly 38% of the revenue share in 2025. This leadership is fueled by intensified adoption of PPA in electric and hybrid vehicles for components such as fuel system parts, electrical connectors, cable insulation, and battery enclosures.

Regulatory pressures, including CAFE standards and EU vehicular emission reduction targets, compel manufacturers to adopt lightweight, high-performance polymers to meet demanding safety and environmental benchmarks. The movement of the automotive industry toward electrification and autonomous driving has augmented PPA demand through requirements for electrically insulating, thermally stable, and durable polymers.

The electrical & electronics sector is the fastest growing application, propelled by escalating miniaturization and performance demands inherent to advanced consumer electronics, automotive electronics, and telecommunication devices. PPA’s characteristics, including excellent electrical insulation, resistance to high temperatures, and flame retardancy, render it ideal for connectors, circuit breakers, and sensor housings subject to rigorous thermal and electrical stresses.

The proliferation of 5G infrastructure, IoT devices, and smart automotive systems further catalyzes the segment growth, providing manufacturers with opportunities to innovate compact, reliable components that meet futuristic performance criteria.

Technology Insights

Flame-retardant PPAs are forecast to capture an estimated 40% of the revenue share in 2025. This dominance stems from safety regulations globally, requiring materials in automotive, aerospace, and consumer electronics markets to exhibit stringent fire resistance.

In response, halogen-free flame retardants are gaining increased preference due to environmental and health considerations, leading to reformulation efforts that align with regulatory bans on halogenated compounds. These capabilities are particularly crucial for EV battery systems and electronic component insulation.

Bio-based/sustainable PPA formulations are poised to emerge as the fastest-growing technological segment with a high CAGR through 2032. The growing emphasis on reducing the environmental footprint of polymer production has driven innovation in renewable feedstock and polymer-recycling technologies.

Bio-based PPAs exhibit performance parity with petrochemical analogues but reduce lifecycle greenhouse gas emissions, gaining traction across environmentally conscious markets in Europe, North America, and, gradually Asia Pacific. The rise of circular economy models and regulatory incentives for sustainable materials is accelerating commercial adoption, making sustainability-focused innovation a key competitive frontier.

Regional Insights

Asia Pacific Polyphthalamide (PPA) Market Trends

Asia Pacific is the dominant regional market for PPA, representing nearly 38% of the global value in 2025. China, Japan, and India constitute the core growth engines, with China alone accounting for nearly 50% of regional volume.

The market here is benefiting from rapid industrialization, sustained expansion of the electric vehicle sector, and thriving consumer electronics manufacturing. Government incentives in China and India are actively promoting the use of advanced polymer materials to enhance manufacturing efficiency, safety, and sustainability.

Manufacturing cost advantages and capacity additions support competitive pricing and supply chain resilience. Emerging regulatory frameworks in China and India are increasingly aligning with global environmental and safety standards, enhancing the demand for flame-retardant and bio-based polyphthalamide formulations.

The Asia Pacific PPA market is the fastest-growing globally. Competitive dynamics include the rapid expansion of domestic polymer producers leveraging technological collaborations and government-backed research initiatives to capture both regional and international markets.

North America Polyphthalamide (PPA) Market Trends

North America is a key market for polyphthalamide, constituting approximately 23% of the global market share by 2025. The U.S. is the predominant regional market, accounting for nearly 70% of North American consumption.

This regional market expansion is primarily driven by the automotive sector’s robust electrification and lightweighting initiatives, tightly coupled with regulatory frameworks enforced by agencies such as the U.S. Environmental Protection Agency (EPA) and the National Highway Traffic Safety Administration (NHTSA).

The market here rewards alignment with emission control regulations and fuel economy standards, fostering a huge demand for polymers such as PPA that enable compliance via lightweight, durable, and flame-retardant vehicle components.

Innovation ecosystems, supported by cooperative efforts between polymer manufacturers, OEMs, and academic institutions, are catalyzing product development and faster market penetration of advanced PPA grades.

Investments in R&D are notably targeting flame-retardant and bio-based PPA formulations to meet safety and sustainability goals. Competitive dynamics include vertically integrated supply chains and strategic partnerships tailored to rapidly evolving electric and autonomous vehicle requirements.

Europe Polyphthalamide (PPA) Market Trends

Europe is anticipated to hold about 22% of the polyphthalamide market share in 2025, with Germany, the U.K., France, and Spain being the primary contributors. Germany alone accounts for approximately 35% of regional consumption volume.

The regional market benefits from harmonized regulatory frameworks, including the EU’s REACH legislation and climate initiatives under the Green Deal, streamlining market entry for innovative flame-retardant and sustainable polyamide formulations. Automotive electrification mandates and the region’s advanced electrical equipment manufacturing base consistently stimulate demand for high-performance polymers.

Investment trends include capacity expansions focused on halogen-free flame-retardant PPA grades and recycling partnerships aligned with circular economy goals. Collaborative efforts among public institutions and the private sector enhance regulatory compliance, driving product innovation and supporting the competitive market structure characterized by leading European polymer producers.

Competitive Landscape

The global polyphthalamide market structure is characterized by moderate consolidation, with approximately 60% of the share concentrated among leading multinational chemical companies.

Key players such as BASF SE, Solvay SA, Evonik Industries AG, Arkema Group, DSM, and DuPont de Nemours Inc. hold dominant positions owing to their global production capabilities, diversified product portfolios covering flame-retardant and bio-based grades, and significant R&D investments facilitating innovation leadership.

This concentrated market structure offers stability and extensive resource allocation for large-scale technology development and supply chain integration.

The market boasts strong competitive dynamics owing to the presence of specialized niche producers focusing on novel formulations, sustainability, and high-performance applications targeting emerging industrial sectors. Smaller players enhance innovation agility, complementing the scale of industry leaders and creating a balanced ecosystem that accelerates technology adoption and market growth.

The competitive positioning across firms emphasizes differentiation through sustainable materials, proprietary flame-retardant technologies, and close collaborative development with end-market customers such as automotive and electronics OEMs.

Key Industry Developments

- In September 2025, Syensqo introduced a medical-grade Amodel polyphthalamide designed for single-use, high-temperature medical devices. This glass-filled polymer maintains strength up to 280°C and is suitable for advanced manufacturing processes such as surface mount technology (SMT) assembly and IR reflow. It is particularly ideal for electrosurgical instruments and electronic assemblies, offering complex molding advantages over other materials. The material will be commercially available in 2026.

- In July 2025, SIBUR showcased its advanced super-structural polyphthalamide at the Innoprom exhibition, highlighting its superior mechanical strength, thermal stability, and resistance to moisture, chemicals, and temperature variations. This high-performance PPA is ideal for applications in automotive engine compartments, packaging films for sensitive food and pharmaceutical products, and demanding industrial parts such as pumps and compressors. SIBUR is pioneering production in Russia, aiming to reduce reliance on imports while supporting the national “New Materials and Chemistry” initiative.

- In June 2025, BASF expanded its PPA portfolio with Ultramid Advanced N3U42G6, a non-halogenated flame-retardant polyamide 9T designed for high-voltage connectors in EVs. This PPA grade enhances the durability, chemical resistance, and electrical insulation of miniaturized, thin-walled connectors used in inverters, batteries, and DC-DC converters. Its low moisture uptake and high heat distortion temperature (265°C) make it suitable for surface mount technology (SMT), ensuring dimensional stability during high-temperature processing.

Companies Covered in Polyphthalamide Market

- BASF SE

- Solvay SA

- Evonik Industries AG

- Arkema Group

- DSM

- DuPont de Nemours, Inc.

- SABIC

- Lanxess AG

- RadiciGroup

- Ascend Performance Materials

- Celanese Corporation

- Mitsui Chemicals, Inc.

- Polyplastics Co., Ltd.

- Evonik Röhm GmbH

- DIC Corporation

Frequently Asked Questions

The polyphthalamide (PPA) market is projected to reach US$2.3 Billion in 2025.

Rising demand for advanced polymers in automotive electrification, high-performance electronics, and industrial applications, and stringent emission regulations promoting lightweight vehicle components are driving the polyphthalamide (PPA) market.

The polyphthalamide (PPA) market is poised to witness a CAGR of 7% from 2025 to 2032.

Rapid growth of electric vehicles worldwide, increasing preference for polymers with thermal and flame-retardant capabilities, and promising progress in bio-based polymer formulations are key market opportunities.

BASF SE, Solvay SA, and Evonik Industries AG are some of the key players in the polyphthalamide (PPA) market.