- Electric Mobility

- Electric Vehicle Insulation Market

Electric Vehicle Insulation Market Size, Share, and Growth Forecast 2026 - 2033

Electric Vehicle Insulation Market by Insulation Type (Thermal Insulation, Electrical Insulation, Acoustic Insulation, Others), Material Type (Foamed Plastics, Ceramics, Thermal Interface Materials (TIMs), Fiberglass, Aerogels, Polyurethane Foam, Others), Vehicle Type (Battery Electric Vehicles (BEV), Hybrid Electric Vehicles (HEV), Plug-in Hybrid Electric Vehicles (PHEV), Fuel Cell Electric Vehicles (FCEV)), Application (Battery Systems, Electric Motors, Power Electronics, Charging Systems, Wiring Harnesses, Interior, Underbody), by Regional Analysis, 2026 - 2033

Electric Vehicle Insulation Market Size and Trend Analysis

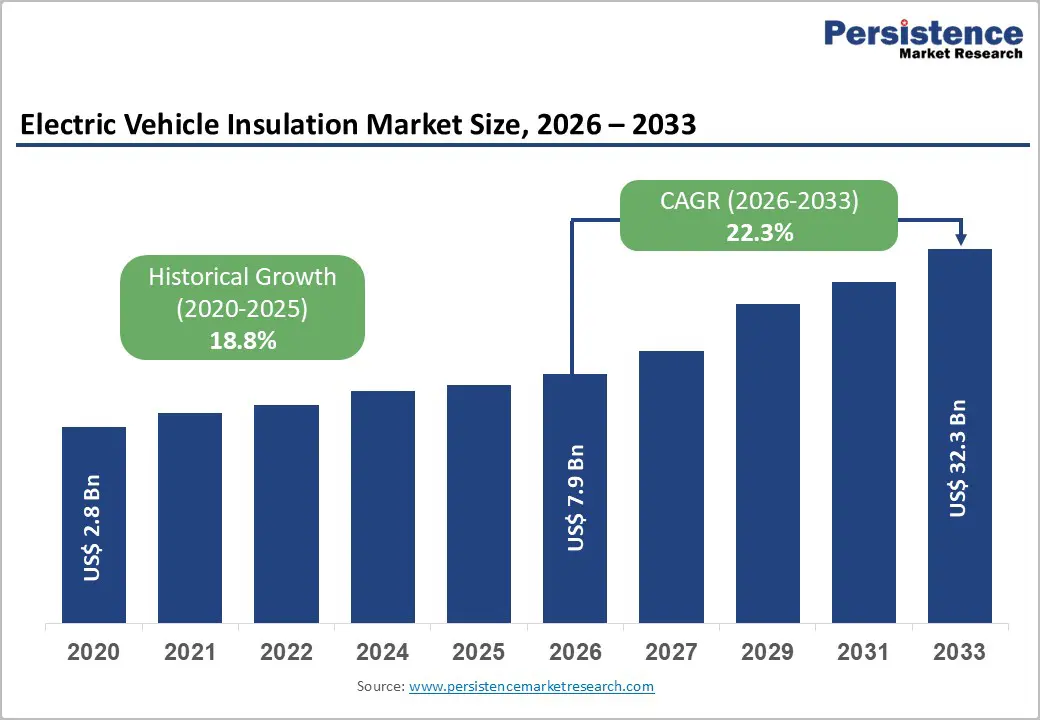

The global electric vehicle insulation market size is expected to be valued at US$ 7.9 billion in 2026 and projected to reach US$ 32.3 billion by 2033, growing at a CAGR of 22.3% between 2026 and 2033.

This exceptional growth trajectory is anchored in three converging forces: the accelerating global transition to electromobility, increasingly stringent battery safety and thermal management regulations, and rapid innovation in advanced insulation materials. Government fleet electrification mandates across the European Union, United States, China, and India are driving automakers to integrate sophisticated thermal, electrical, and acoustic insulation systems across every EV subsystem. The structural shift from internal combustion engines to high-voltage electric powertrains fundamentally raises insulation requirements, creating sustained, multi-decade demand that far exceeds historical demand in the automotive insulation market.

Key Industry Highlights

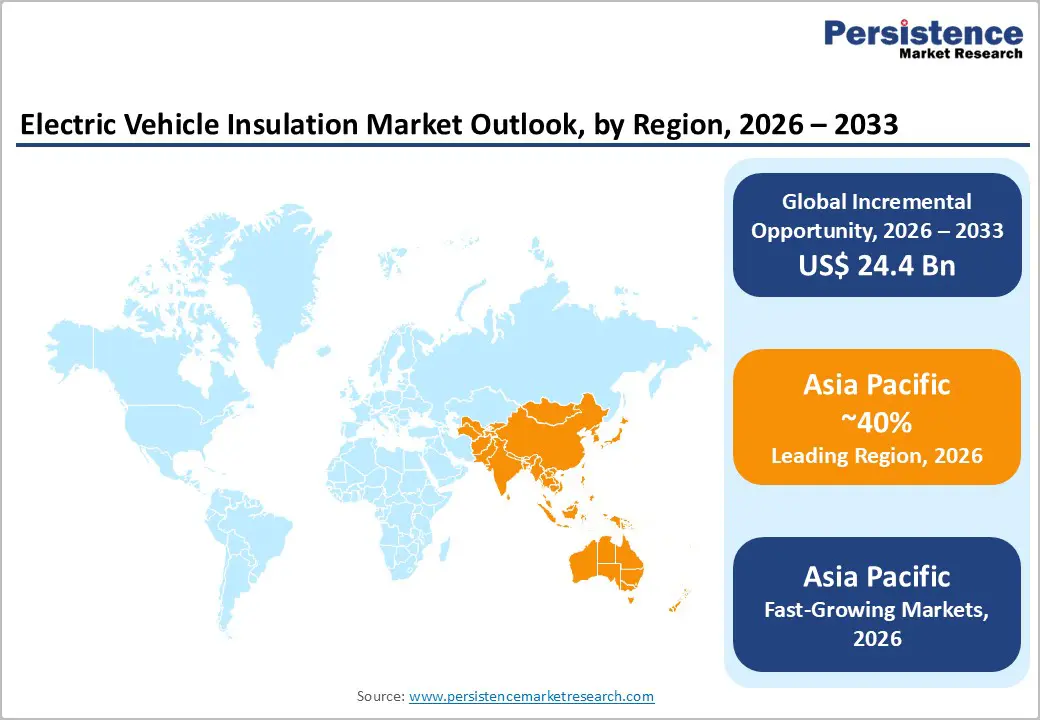

- Leading Region: Asia Pacific leads the global electric vehicle insulation market with approximately 40% share in 2025, anchored by China’s 9 million+ NEV sales in 2023, Japan and South Korea’s battery manufacturing ecosystems, and surging ASEAN EV investments.

- Fastest Growing Region: Asia Pacific is also the fastest growing region during 2026 - 2033, driven by India’s PM E-DRIVE scheme, China’s Dual Credit Policy NEV mandates, and rapid BYD, VinFast, and Mitsubishi manufacturing expansions across Southeast Asia.

- Dominant Segment: Battery Systems dominates the application segment with approximately 38% market share in 2025, fueled by multi-layer insulation requirements in high-energy-density lithium-ion packs and stringent UL 94 V-0 and ECE R100 thermal runaway safety standards.

- Fastest Growing Segment: Aerogels are the fastest growing material segment during 2026 - 2033, driven by unmatched thermal resistance-to-thickness ratio, growing adoption in solid-state battery prototypes, and increasing OEM specification in premium BEV battery pack designs from Toyota, BMW, and QuantumScape.

- Key Opportunity: Solid-state battery commercialization by Toyota, Volkswagen, and BMW between 2027 and 2030, combined with the US$7.5 billion U.S. NEVI program, represents the most significant multi-year demand opportunity for advanced EV insulation material innovators.

| Key Insights | Details |

|---|---|

| Electric Vehicle Insulation Market Size (2026E) | US$ 7.9 Billion |

| Market Value Forecast (2033F) | US$ 32.3 Billion |

| Projected Growth CAGR (2026 - 2033) | 22.3% |

| Historical Market Growth (2020 - 2025) | 18.8% |

Market Dynamics

Surging Global EV Adoption Underpinned by Government Policy and Emission Targets

The most powerful structural driver of the electric vehicle insulation market is the unprecedented pace of global EV adoption, directly catalyzed by government policy frameworks targeting net-zero emissions. The European Union has legislated a de facto ban on new internal combustion engine vehicle sales by 2035 under Regulation (EU) 2023/851, while the U.S. Environmental Protection Agency (EPA)’s finalized 2032 light-duty vehicle emission standards are expected to require that 56% of new passenger car sales be fully electric by 2032. According to the International Energy Agency (IEA)’s Global EV Outlook 2024, global electric car sales exceeded 17 million units in 2023, a 35% year-on-year increase, with the global EV fleet surpassing 40 million vehicles. Each additional EV on the road demands specialized thermal insulation for battery packs, electrical insulation for high-voltage systems, and acoustic insulation for cabin comfort, directly expanding addressable demand for insulation solution providers.

Escalating Battery Safety Regulations and Thermal Management Requirements

High-voltage lithium-ion battery systems in modern Battery Electric Vehicles (BEVs) operate at voltages exceeding 800V in next-generation platforms, imposing extreme electrical insulation requirements to prevent short circuits, thermal runaway, and electrocution risks. Regulatory bodies worldwide are tightening standards; the United Nations Economic Commission for Europe (UNECE)’s Regulation No. 100 on electric vehicle safety mandates rigorous electrical isolation standards for battery packs, requiring insulation resistance of at least 100 Ω/V for high-voltage systems. Simultaneously, the Society of Automotive Engineers (SAE) and International Electrotechnical Commission (IEC) have updated standards for thermal interface materials and dielectric insulation in EV powertrains. Battery thermal management systems incorporating advanced Thermal Interface Materials (TIMs), aerogels, and ceramic insulation layers are becoming standard on premium and mass-market BEV platforms, significantly increasing the value of per-vehicle insulation content compared to conventional automobiles.

High Material and Development Costs Limiting Rapid Market Penetration

Despite robust demand signals, the electric vehicle insulation market faces a meaningful restraint: elevated material and development costs for advanced insulation technologies. Aerogel-based insulation materials, among the most thermally effective available, carry significantly higher production costs than conventional foam or fiberglass solutions, limiting their adoption to premium EV segments and specialty battery applications. According to the U.S. Department of Energy (DOE), the high cost of advanced thermal interface materials and specialty dielectrics adds meaningfully to total battery pack cost, which already represents approximately 30-40% of a BEV’s total vehicle cost. For mass-market OEMs facing intense pricing pressure, this cost burden constrains the pace at which advanced insulation systems can be standardized across full model lineups.

Supply Chain Vulnerabilities and Raw Material Concentration Risks

The electric vehicle insulation market is exposed to supply chain fragility, particularly for specialty raw materials such as silicone-based TIMs, ceramic fibers, and high-purity fiberglass. Silicone, a key constituent of many thermal interface and electrical insulation materials, relies heavily on silicon metal derived from China, which accounts for over 60% of global silicon metal production according to the U.S. Geological Survey (USGS). Disruptions to this supply chain, whether from geopolitical tensions, export controls, or logistical bottlenecks, could significantly increase input costs and constrain insulation manufacturers' production capacity. The concentration of aerogel precursor and specialty polymer manufacturing in a small number of global facilities further amplifies supply risk, creating margin and delivery vulnerabilities that could dampen market responsiveness to surging EV demand.

Solid-State Battery Commercialization Creating Next-Generation Insulation Demand

The impending commercialization of solid-state batteries (SSBs) represents a transformative opportunity for developers of next-generation EV insulation materials. Solid-state batteries operate at higher temperatures and voltages than conventional lithium-ion cells, require entirely new approaches to thermal management, and present novel dielectric insulation challenges. Leading automakers, including Toyota, Volkswagen, BMW, and QuantumScape, have announced timelines for SSB-powered vehicle launches between 2027 and 2030. The U.S. DOE’s Vehicle Technologies Office has committed hundreds of millions of dollars to SSB development under the Battery500 Consortium. This technology transition will require insulation material suppliers to develop entirely new product categories, including ultra-thin ceramic dielectric layers, high-temperature aerogel composites, and novel TIM formulations, creating significant first-mover revenue opportunities for companies investing in SSB-compatible insulation R&D today.

Expansion of EV Charging Infrastructure Driving Charging System Insulation Demand

The global build-out of DC fast-charging and ultra-fast-charging infrastructure is driving substantial demand for electrical and thermal insulation solutions. Public charging networks operating at 150 kW to 350 kW and above require advanced high-voltage cable insulation, power electronics thermal management materials, and flame-retardant housing insulation. The U.S. National Electric Vehicle Infrastructure (NEVI) program, authorized with US$ 7.5 billion under the Bipartisan Infrastructure Law, mandates deployment of 500,000 public EV chargers across the United States by 2030. The European Alternative Fuels Infrastructure Regulation (AFIR) requires fast charging stations with at least 150 kW output every 60 km along EU core road networks by 2026. These regulatory-driven expansions create durable, multi-year demand for insulation solutions in charging systems beyond the vehicle itself.

Category-wise Insights

Insulation Type Analysis

Electrical Insulation emerged as the dominant segment in the electric vehicle insulation market, accounting for approximately 42% of total market share in 2025. This leadership reflects the fundamental safety and regulatory imperative to electrically isolate high-voltage battery systems, power electronics, wiring harnesses, and motor windings in modern EV architectures. As EV platforms scale to 800V and beyond, a trajectory led by Hyundai’s E-GMP platform, Porsche Taycan, and emerging Lucid Air variants, the dielectric strength and thermal stability requirements for electrical insulation materials escalate substantially. UNECE Regulation No. 100 and IEC 60664 standards mandate specific creepage and clearance distances for high-voltage components, legally obligating OEMs to invest in certified electrical insulation materials. The growing density of power electronics per vehicle further amplifies per-unit insulation content, reinforcing the dominance of this segment through the forecast period.

Material Type Analysis

Thermal Interface Materials (TIMs) led the material type category, with an estimated market share of approximately 31% in 2025, driven by their critical role in managing heat transfer between lithium-ion battery cells, cooling plates, and structural housings in BEV battery packs. Effective thermal management is directly correlated with battery longevity and charge-rate capability; according to research published in the Journal of Power Sources, uniformity in battery cell temperature within ±2°C across a pack can improve cycle life by up to 20%. Leading TIM products, including phase-change materials, thermally conductive gap pads, and potting compounds, are specified by major battery manufacturers and OEM Tier-1 suppliers as standard bill-of-materials components. Companies including 3M, Morgan Advanced Materials, and Unifrax have expanded their TIM portfolios specifically targeting EV battery applications, cementing this material category’s market leadership.

Vehicle Type Analysis

Battery Electric Vehicles (BEVs) held the dominant share of approximately 58% in the vehicle type segment in 2025, reflecting the highest per-vehicle insulation content demand and the fastest-growing sales volumes within the broader EV ecosystem. Unlike hybrid or plug-in hybrid vehicles, BEVs rely entirely on high-voltage battery systems for propulsion, requiring comprehensive thermal insulation for the battery enclosure, full electrical insulation for high-voltage components, and acoustic insulation to compensate for the absence of combustion engine noise masking. According to the IEA’s Global EV Outlook 2024, BEV sales accounted for approximately 70% of total EV sales globally in 2023. As BEV price parity with ICE vehicles approaches in key segments, supported by declining battery costs and government purchase incentives, BEV sales growth will continue to outpace hybrid variants, sustaining this segment’s market dominance through 2033.

Application Analysis

The Battery Systems application segment held the leading market share position of approximately 38% in 2025, driven by the complex, multi-material insulation requirements of modern lithium-ion battery packs. Battery systems in contemporary BEVs incorporate thermal insulation between cell layers to prevent thermal runaway propagation, TIMs between cells and cooling plates for heat dissipation, electrical insulation for cell interconnects and high-voltage busbars, and flame-retardant enclosure materials meeting UL 94 V-0 and ECE R100 standards. The energy density competition among CATL, Panasonic, LG Energy Solution, and Samsung SDI, competing to deliver higher-capacity packs in smaller form factors, intensifies the thermal management challenge and proportionally increases insulation material content per kilowatt-hour. This dynamic makes battery system insulation the single largest application-level revenue pool in the EV insulation ecosystem.

Regional Insights

North America Electric Vehicle Insulation Market Trends and Insights

North America held approximately 24% of the global electric vehicle insulation market share in 2025, with the United States as the undisputed regional leader. The Inflation Reduction Act (IRA) of 2022 has been transformative, directing over US$ 370 billion toward clean energy and electric vehicle incentives, including consumer tax credits of up to US$ 7,500 for qualifying EV purchases and significant Advanced Manufacturing Production Credits that incentivize domestic battery and EV component manufacturing. This policy architecture has triggered a wave of domestic EV and battery factory investments from Tesla, General Motors, Ford, Stellantis, and foreign OEMs, including Hyundai and Volkswagen, all of which require localized insulation material supply chains.

The U.S. innovation ecosystem is also highly active, with DOE-funded research at institutions such as Oak Ridge National Laboratory (ORNL) and Argonne National Laboratory advancing next-generation thermal management materials and aerogel composites for EV applications. Canada is emerging as a key battery supply chain hub, with Stellantis-LG LGES’s NextStar Energy gigafactory in Windsor, Ontario, representing the country’s largest-ever manufacturing investment. The EPA’s 2032 Clean Car Standards ensure sustained regulatory pull for advanced EV insulation materials throughout the forecast period.

Europe Electric Vehicle Insulation Market Trends and Insights

Europe accounted for approximately 27% of the global electric vehicle insulation market in 2025, driven by a robust regulatory framework and a deep automotive manufacturing heritage. The EU’s 2035 ICE ban under Regulation (EU) 2023/851, combined with CO2 Standards for Cars and Vans targeting a 55% reduction by 2030, has compelled Volkswagen Group, BMW, Mercedes-Benz, and Renault to accelerate electrification and deepen domestic supply chain partnerships for EV-specific materials. Germany, as Europe’s largest automotive manufacturer, is the epicenter of EV insulation demand, while France and Spain are emerging as significant EV production hubs under national electrification strategies.

The European Battery Alliance (EBA) and the EU Battery Regulation (EU) 2023/1542 are reshaping supply chain dynamics by mandating minimum recycled content thresholds and carbon footprint disclosures for EV batteries, indirectly influencing insulation material selection toward more sustainable formulations. Companies including Armacell International, Sika Automotive, Zotefoams, and Tecman Speciality Materials are headquartered or heavily active in Europe, positioning the region as both a major demand market and a technology development hub for EV insulation innovation through 2033.

Asia Pacific Electric Vehicle Insulation Market Trends and Insights

Asia Pacific is the largest and fastest-growing region in the electric vehicle insulation market, commanding approximately 40% of global market share in 2025 and expected to sustain the highest CAGR through 2033. China is the unrivaled epicenter, accounting for the majority of the region’s demand. According to the China Association of Automobile Manufacturers (CAAM), China sold over 9 million new energy vehicles (NEVs) in 2023, representing nearly 35% of all passenger vehicle sales in the country. China’s NEV mandates under the Dual Credit Policy and its 2060 carbon neutrality commitment continue to drive accelerating EV adoption, sustaining enormous demand for battery system insulation, TIMs, and high-voltage electrical insulation materials.

Japan and South Korea contribute significantly through world-class battery manufacturing ecosystems anchored by Panasonic, LG Energy Solution, Samsung SDI, and SK Innovation. India is rapidly emerging as a high-growth market, with the Ministry of Heavy Industries’ PM E-DRIVE scheme allocating INR10,900 crore (approximately US$ 1.3 billion) to accelerate EV adoption. The ASEAN bloc, particularly Thailand, Indonesia, and Vietnam, is attracting major EV manufacturing investments from BYD, VinFast, and Mitsubishi, creating new demand clusters for localized EV insulation supply chains across Southeast Asia.

Competitive Landscape

The global electric vehicle insulation market is moderately fragmented, characterized by the presence of specialty material manufacturers, automotive component suppliers, and emerging advanced material developers competing across multiple insulation technologies. Market participants offer a broad portfolio of thermal, electrical, and acoustic insulation solutions designed to meet the evolving performance and safety requirements of electric vehicle architectures.

Competition is largely driven by material innovation, product customization, and close collaboration with automotive OEMs and battery manufacturers. Companies are focusing on developing high-performance materials such as aerogels, ceramic composites, and advanced polymer foams to improve thermal stability, fire resistance, and lightweight performance. Strategic initiatives include long-term supply agreements with vehicle manufacturers, co-development of application-specific insulation components, and increased investments in research and development. In addition, manufacturers are expanding production capacities and strengthening regional supply chains in Asia Pacific and Europe to align with rapidly growing electric vehicle manufacturing hubs and rising demand for advanced battery safety solutions.

Key Developments

- April, 2024: Huntsman Corporation launched new SHOKLESS™ polyurethane foam systems designed for electric vehicle battery applications, enabling lightweight potting and encapsulation solutions that enhance structural protection, thermal insulation, and impact resistance for battery cells, modules, and packs.

- June, 2025: Alkegen announced full-scale commercial production of its fiber-enhanced AlkeGel™ aerogel insulation for electric vehicle batteries, expanding its advanced materials portfolio and enabling scalable thermal runaway and fire protection solutions for EV manufacturers.

- June, 2025: WEVO-CHEMIE GmbH launched the WEVOSIL 2210x FL series of high-performance silicone potting compounds designed for next-generation EV power electronics, providing improved thermal management, electrical insulation, and long-term reliability for components such as inverters and DC/DC converters.

- August, 2025: Wacker Chemie AG unveiled ELASTOSIL® R 531/60, a flame-resistant silicone rubber designed for EV traction battery busbars, forming an insulating ceramic layer during fires to prevent short circuits and enhance high-voltage battery safety.

Companies Covered in Electric Vehicle Insulation Market

- 3M Inc.

- CYG TEFA Co. Ltd.

- Armacell International S.A.

- Sika Automotive AG

- ADDEV Materials

- Sumitomo Riko Company Limited

- Adler Pelzer Holding GmbH

- INOAC Corporation

- Morgan Advanced Materials plc

- Pritex Limited

- Autoneum

- Tecman Speciality Materials Ltd

- Toyota Boshoku Corporation

- Zotefoams plc

- Unifrax

- Rogers Corporation

- Henkel AG & Co. KGaA

- Elringklinger AG

- BASF SE

- Freudenberg Performance Materials

- Huntsman Corporation

- Alkegen

- WEVO-CHEMIE GmbH

- Wacker Chemie AG

Frequently Asked Questions

The global Electric Vehicle Insulation market is estimated to reach US$ 7.9 billion in 2026, driven by rapid EV adoption and increasing battery safety requirements.

Demand is driven by growing EV production, stricter battery safety regulations, and increasing use of high-voltage EV architectures requiring advanced insulation materials.

Asia Pacific leads the market due to strong EV production, large battery manufacturing capacity, and rapid adoption of electric vehicles.

Key opportunities include development of insulation materials for solid-state batteries and growing demand from high-power EV charging infrastructure.

Key companies include 3M, BASF, Rogers Corporation, Morgan Advanced Materials, Sumitomo Riko, Autoneum, Henkel, and Freudenberg Performance Materials.