- Food Ingredients & Additives

- High Oleic Oil Market

High Oleic Oil Market Size, Share, and Growth Forecast, 2025 - 2032

High Oleic Oil Market By Product Type (Sunflower Oil, Canola Oil, Soybean Oil, Safflower Oil, Rapeseed Oil), Nature (Organic, Conventional), Application (Foodservice, Health Supplements, Personal Care, Biodiesel), and Regional Analysis for 2025 - 2032

High Oleic Oil Market Size and Trends Analysis

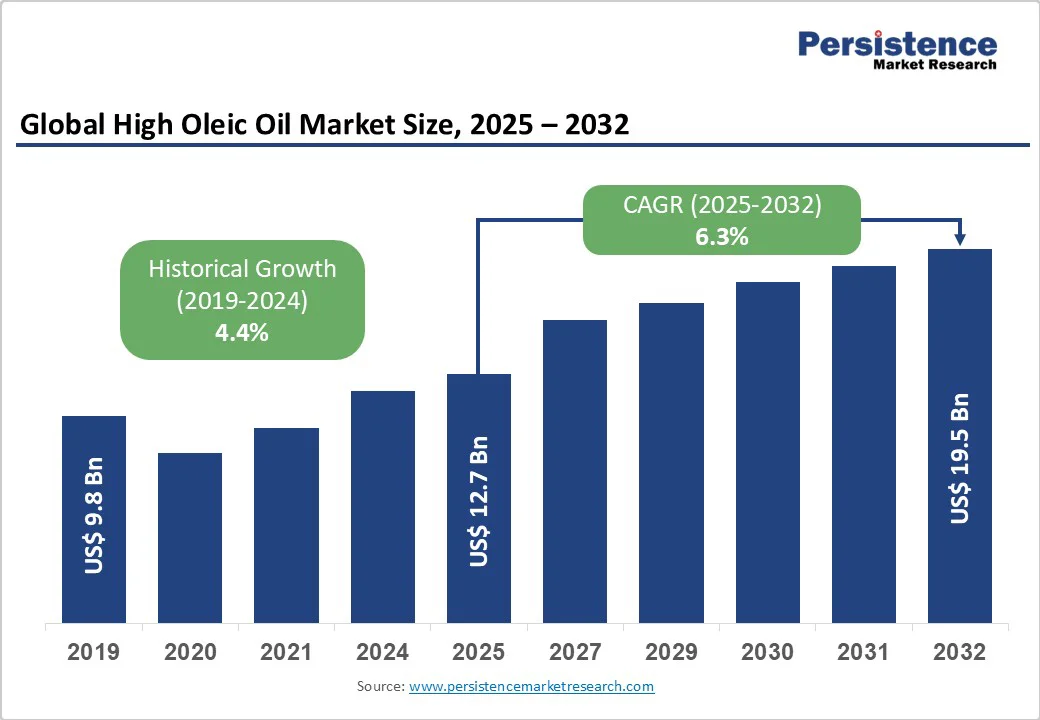

The global high oleic oil market size is likely to be valued at US$12.7 billion in 2025. It is estimated to reach US$19.5 billion in 2032, growing at a CAGR of 6.3% during the forecast period 2025 - 2032, driven by the oil’s high content of monounsaturated fats that support heart health by improving cholesterol balance, appealing to health-conscious consumers.

Key Industry Highlights

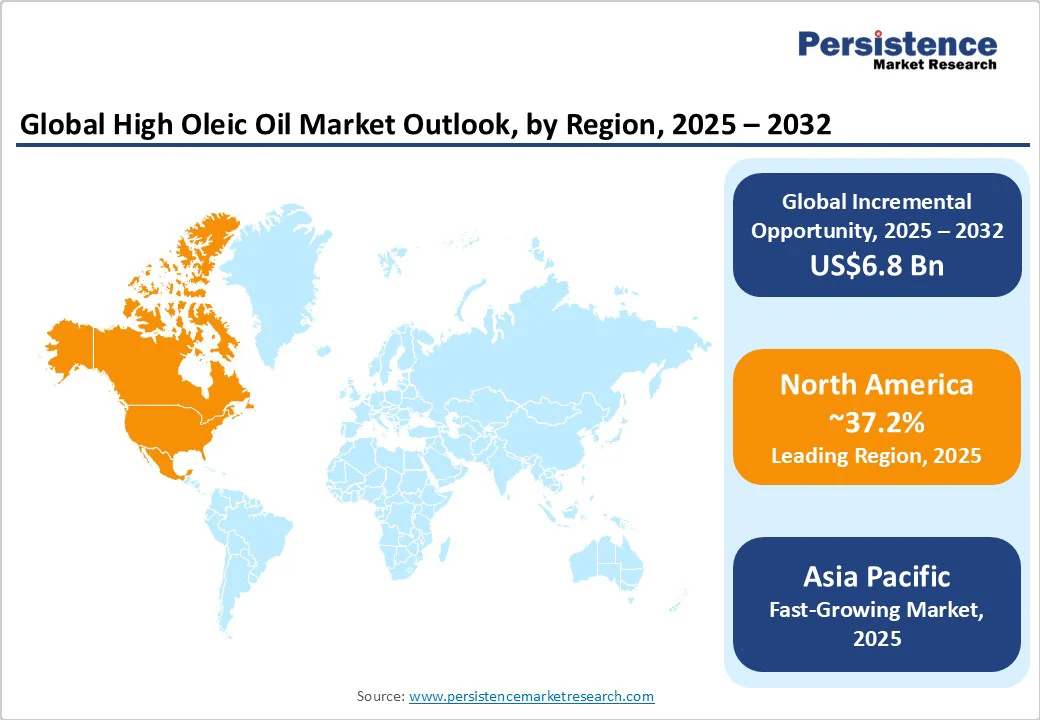

- Leading Region: North America, with about 37.2% share in 2025, spurred by the high production of high oleic soybeans and superior agricultural infrastructure.

- Fastest-growing Region: Asia Pacific, backed by increasing imports of sunflower and soybean oils.

- Expansion Plan: Ventura Foods, a joint venture with Mitsui & Co., annually purchased a major portion of refined soy and canola oil from CHS Inc. This collaboration ensured a steady supply of high-quality oils for food production.

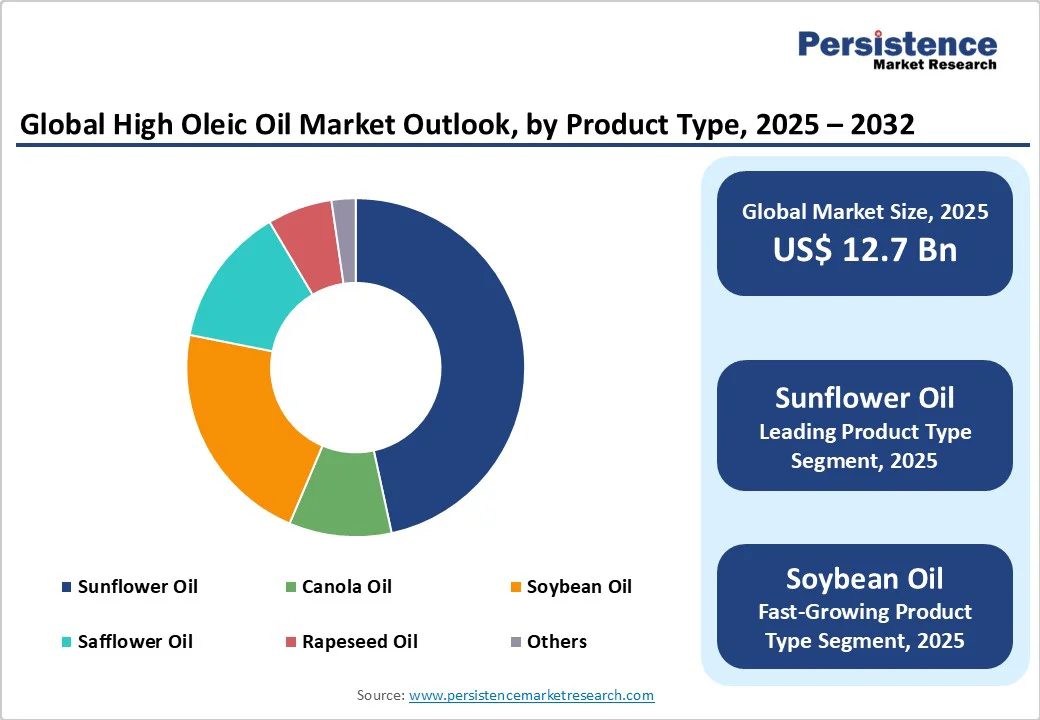

- Leading Product Type: Sunflower oil holds nearly 46.6% share in 2025, bolstered by neutral taste and heart-healthy monounsaturated fats.

- Dominant Nature: Organic high oleic oil, approximately 73.2% of the high oleic oil market share in 2025, accelerated by consumer preference for clean-label oils.

- Key Application: Foodservice recorded about 39.6% of the market share in 2025, due to the long frying life of high oleic oil that helps reduce costs in restaurants.

| Key Insights | Details |

|---|---|

| High Oleic Oil Market Size (2025E) | US$12.7 Bn |

| Market Value Forecast (2032F) | US$19.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Health Benefits Supporting Consumer Preference

A key driver of high oleic oil adoption is its heart-healthy fat profile. These oils are abundant in monounsaturated fats, which help improve cholesterol balance by lowering LDL (bad) cholesterol while supporting HDL (good) cholesterol levels. This makes them a preferred choice for consumers seeking to reduce cardiovascular risks without compromising taste or cooking versatility.

The rising awareness of diet-related health impacts in regions such as North America and Europe has encouraged both households and foodservice providers to switch to high oleic sunflower, soybean, and safflower oils. For instance, health-focused brands in the U.S. and the U.K. actively market these oils as better-for-heart alternatives in cooking and packaged food, reinforcing consumer trust in their nutritional benefits.

Superior Cooking Performance Boosting Adoption

High oleic oils are gaining traction due to their resistance to oxidation and thermal breakdown, which allows for extended use in frying, baking, and industrial food processing. This durability not only reduces the requirement for frequent oil replacement but also helps maintain consistent taste and texture in prepared food items.

Commercial bakeries and packaged snack manufacturers are increasingly switching to high oleic oils to improve product shelf life and stability. This demonstrates that the oil’s resilience benefits both cost management and quality control across various food production environments.

Barrier Analysis - Concerns Associated with Nutritional Imbalance

One factor restraining the growth of high oleic oils is the potential nutritional imbalance that may arise if these oils dominate the diet. While high in heart-healthy monounsaturated fats, relying excessively on high oleic oils can inadvertently reduce the intake of other essential macronutrients, such as proteins and complex carbohydrates.

Dieticians in developed economies have cautioned against overconsumption, emphasizing that a balanced diet should include a mix of fats, proteins, and carbohydrates. Consumer awareness campaigns sometimes highlight this risk, limiting rapid adoption, particularly among health-conscious individuals who are attentive to dietary composition rather than isolated benefits of monounsaturated fats.

Thermal Degradation Risks

Another growth restraint stems from the potential formation of harmful compounds when high oleic oils are repeatedly exposed to very high temperatures. Prolonged heating, especially beyond recommended frying limits, can lead to the production of aldehydes and other toxic byproducts.

This has been observed in some commercial frying operations in North America, prompting regulatory agencies to issue guidance on safe usage. Concerns over these health risks can make foodservice providers and home cooks cautious, limiting the market expansion of high oleic oils despite their stability and performance advantages.

Opportunity Analysis - Development of Genetically Engineered Oilseed Varieties

One leading growth opportunity for high oleic oil lies in the development of genetically improved oilseed crops. Novel breeding techniques, including gene editing and selective hybridization, are enabling the development of sunflower, soybean, and safflower varieties with high oleic content, better yield, and improved disease resistance.

These developments not only increase production efficiency but also refine oil stability, making it suitable for frying, baking, and packaged foods. For instance, research programs in the U.S. and Europe have introduced over a thousand high oleic soybean breeding lines, some of which are now undergoing commercial trials, reflecting a push toward precision agriculture and optimized oil quality.

Expansion into Industrial and Pharmaceutical Sectors

High oleic oils are finding increasing applications beyond food, especially in industrial and pharmaceutical sectors. Their oxidative stability and neutral flavor make them valuable in biodiesel production, lubricants, and specialty chemicals. In the pharmaceutical and nutraceutical segments, these oils are extensively used in dietary supplements, topical formulations, and carrier oils for active compounds.

Companies in Europe and North America are incorporating high oleic sunflower and soybean oils into ointments, creams, and capsules, due to their long shelf life and skin-friendly properties. These initiatives exhibit the oil’s versatility and potential for cross-sector growth.

Category-wise Analysis

Product Type Insights

Sunflower oil is expected to account for approximately 46.6% of the market share in 2025, due to its high oxidative stability, making it ideal for deep frying, baking, and processed food items without breaking down or producing off-flavors. It contains a high proportion of monounsaturated fats, which are considered heart-healthy, and has a longer shelf life compared to conventional sunflower or other vegetable oils. In 2024, renowned fast-food chains in the U.S., including McDonald’s and Wendy’s, switched to high oleic sunflower oil in several outlets to improve frying performance and meet consumer demand for healthy cooking oils.

Soybean oil is estimated to witness considerable growth through 2032, supported by its versatility and cost-effectiveness. It is widely used in frying, salad dressings, margarine, and dairy substitutes as it combines stability with a neutral flavor profile. In North America, U.S. farmers have increasingly planted high oleic soybean varieties, with over 1.6 million acres in 2024, to meet the rising demand from food manufacturers looking for oils with improved frying life and healthy fat content.

Nature Insights

Organic high oleic oil is speculated to capture a market share of nearly 73.2% in 2025 as it combines the health benefits of high oleic content with the appeal of chemical-free and sustainable farming practices. Consumers seeking clean-label products and environmentally responsible options tend to choose organic high oleic oils for cooking, baking, and salad applications. For example, in Europe, Biona Organic and La Tourangelle have reported strong growth in high oleic sunflower and safflower oils due to rising consumer demand for organic and heart-healthy oils.

Conventional high oleic oil will likely showcase a decent CAGR in the foreseeable future as it delivers cost-effective stability and versatility for large-scale food processing and frying applications. Food manufacturers and restaurants prefer it for its longer shelf life, neutral taste, and oxidative stability, reducing oil replacement frequency. In the U.S., high oleic soybean oil remains a staple in commercial kitchens and fast-food chains due to its reliability and affordability compared to organic variants, ensuring consistent demand across industrial and retail segments.

Application Insights

Foodservice is estimated to hold a market share of about 39.6% in 2025, as high oleic oils provide high oxidative stability and long frying life, which is essential for restaurants, fast-food chains, and catering services. They maintain flavor integrity even at high temperatures, reducing waste and operational costs. For example, key chains in North America and Europe, including McDonald’s and KFC, have switched to high oleic sunflower and soybean oils to refine frying performance and meet rising consumer demand for healthy cooking oils.

Personal care is projected to witness a substantial CAGR from 2025 to 2032 as high oleic oils are rich in monounsaturated fats and antioxidants, making them ideal for skincare, haircare, and cosmetic formulations. They provide moisturizing and protective benefits without leaving a greasy residue. Brands such as L’Oréal and The Body Shop have incorporated high oleic sunflower and safflower oils into lotions, creams, and hair serums to improve product stability and deliver natural, nourishing properties to consumers.

Regional Insights

North America High Oleic Oil Market Trends

In 2025, North America is expected to account for nearly 37.2% of the market share, owing to the increasing demand for healthy cooking oils and developments in oilseed production. The U.S. is a major producer of high oleic soybeans, with over 1.6 million acres planted in 2024, and projections suggest this could increase to 2.7 million acres by 2027. These soybeans are primarily used in food applications, accounting for about 60% of their usage, with the remainder utilized in dairy rations and industrial applications.

Despite domestic production, the U.S. imports a significant amount of refined high oleic sunflower oil, with 152 shipments recorded between November 2023 and October 2024. China, Spain, and Germany were the leading exporters, supplying 65% of these imports. The market is also witnessing innovations in breeding and processing. For instance, Michigan State University has developed over 1,000 high oleic soybean breeding lines, with 15 currently undergoing university variety trials.

Asia Pacific High Oleic Oil Market Trends

Asia Pacific is currently experiencing considerable growth due to increasing health awareness and demand for stable, heart-healthy cooking oils. China, India, and Japan are leading the adoption of high oleic oils, specifically sunflower and soybean oils, backed by their higher monounsaturated fat content and longer shelf life compared to traditional oils. China has seen a drastic rise in sunflower oil imports, with a 74.8% increase in 2019, overtaking soybean oil as the third-highest imported oil.

This shift reflects a rising preference for high oleic sunflower oil among consumers in China. India is witnessing a surge in sunflower oil imports, reaching levels not seen since January 2025, as refiners favor it over palm oil due to cost-effectiveness and health considerations. The country’s government is actively promoting the cultivation of high oleic oilseeds through initiatives aimed at doubling domestic edible oil production by 2030.

Middle East and Africa High Oleic Oil Market Trends

In the Middle East & Africa, the market is being influenced by shifting dietary preferences and increasing health consciousness. Saudi Arabia, the UAE, and South Africa are witnessing a surge in demand for high oleic oils, mainly in the foodservice sector. This trend is attributed to the oils' stability and health benefits, making them suitable for high-heat cooking applications. Market players are focusing on product promotion, distribution expansion, and strategic partnerships to capitalize on emerging opportunities in the region.

In North Africa, sunflower oil, known for its high smoke point and health benefits, is gaining traction. This shift reflects a rising preference for oils that cater to health-conscious consumer choices. Olive oil consumption has surged in the Gulf Cooperation Council (GCC) region, augmented by rising disposable incomes and the surging popularity of the Mediterranean diet. The market faces challenges such as limited domestic production and reliance on imports.

Competitive Landscape

The global high oleic oil market is characterized by a blend of established agribusiness giants, regional producers, and emerging players focusing on specialized oilseed variants. Major multinational corporations such as Cargill, ADM, Bunge, and Olam Agri dominate the market, using their extensive supply chains and processing capabilities. For instance, in the high oleic soybean oil segment, these companies maintain significant market shares, capitalizing on developments in breeding and oil extraction technologies.

Key Industry Developments

- In April 2025, SOYLEIC collaborated with Byron Seeds to expand access to high-oleic soybean genetics. This collaboration aims to improve the availability of high-oleic soybeans for farmers, supporting the rising demand for healthy oils in food production.

- In May 2024, CHO America debuted Bella Del Sol at SIAL Canada. This pioneering brand of high oleic sunflower oils is expected to transform the landscape of healthy cooking with its exceptional fatty acid profile.

Companies Covered in High Oleic Oil Market

- Archer Daniels Midland Company

- DowDupont Inc.

- Bunge Limited

- IOI Corporation Berhad

- Cargill, Incorporated

- Louis Dreyfus Company B.V.

- AAK AB

- Conagra Brands, Inc.

- The J.M. Smucker Company

- Ventura Foods, LLC

- Avena Nordic Grain Oy

Frequently Asked Questions

The high oleic oil market is projected to reach US$12.7 Billion in 2025.

Rising health consciousness and preference for heart-healthy, monounsaturated fats are the key market drivers.

The high oleic oil market is poised to witness a CAGR of 6.3% from 2025 to 2032.

Development of genetically improved oilseed varieties and adoption in fast food frying are the key market opportunities.

Archer Daniels Midland Company, DowDupont Inc., and Bunge Limited are a few key market players.