- Biotechnology

- High Throughput Process Development Market

High Throughput Process Development Market Size, Share, and Growth Forecast 2026 - 2033

High Throughput Process Development Market by Tools & Systems (Manual Tools, Automated Tools, Analytical Tools, High Throughput Integrated Bioreactor Systems), by Application (Bioprocess Development, Drug Discovery, Vaccine Development, Quality Control), by Process Stage (Upstream Process Development, Downstream Process Development), by End User (Biopharmaceutical & Biotechnology Companies, Pharmaceutical Companies, CROs & CMOs, Academic & Research Institutes), by Regional Analysis, 2026-2033.

High Throughput Process Development Market Size and Trend Analysis

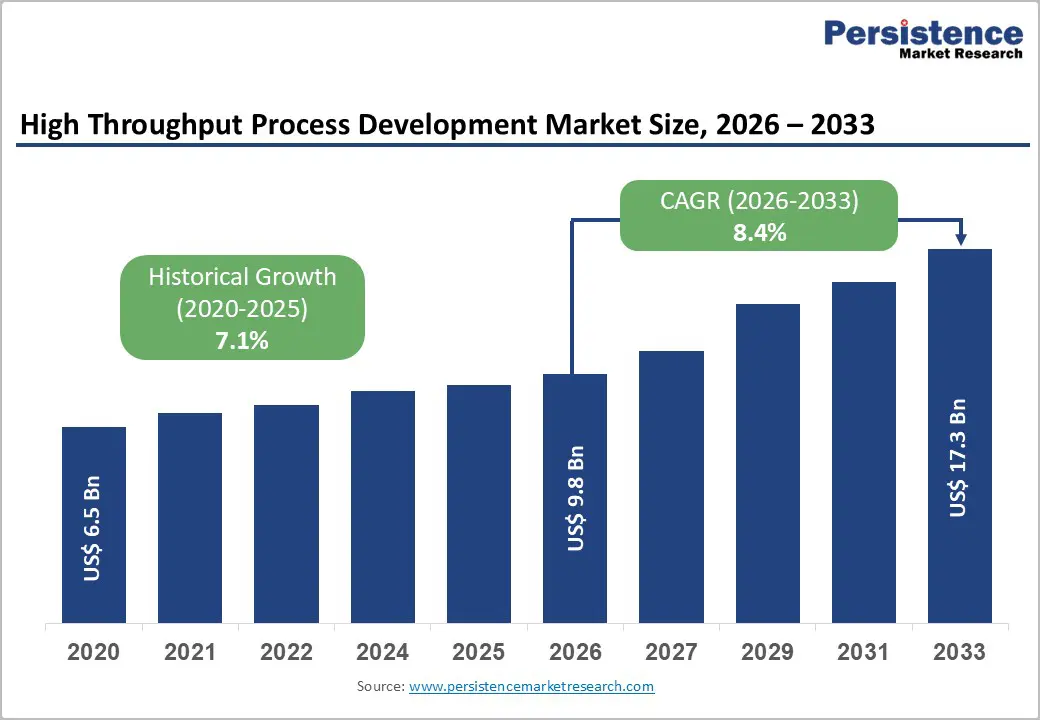

The global high throughput process development market size is expected to be valued at US$ 9.8 billion in 2026 and projected to reach US$ 17.3 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

Rapid expansion of biologics, vaccines, and advanced therapies is accelerating the adoption of automated, data?rich development platforms that shorten process cycles and reduce costs. Biopharmaceutical manufacturers are under pressure to intensify upstream and downstream operations, supported by regulatory encouragement for process analytical technology (PAT) and Quality by Design (QbD) approaches that favor high throughput experimentation. At the same time, increasing complexity of molecules and global competition are pushing companies to deploy integrated robotics, miniaturized bioreactors, and advanced analytics to optimize hundreds of conditions in parallel, making high throughput process development a strategic capability across leading innovation hubs.?

Key Market Highlights

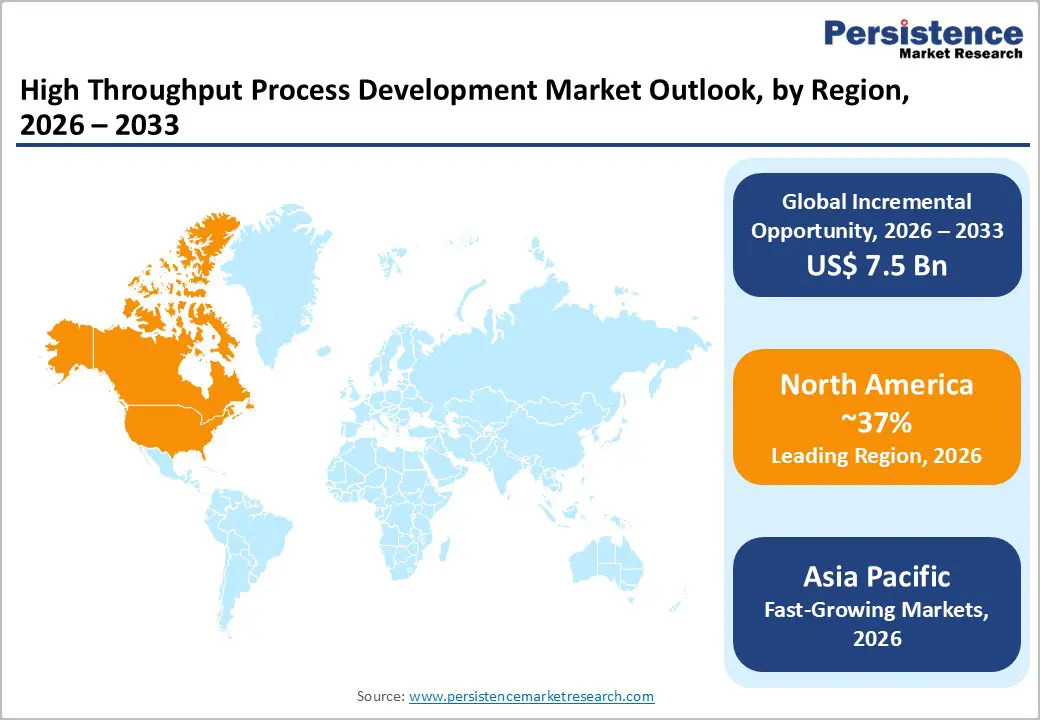

- North America leads the high-throughput process development market, driven by strong U.S. biopharmaceutical R&D, supportive FDA guidance on PAT and continuous manufacturing, and deep adoption of automation and advanced analytics across major manufacturers.?

- Asia Pacific is the fastest growing region, supported by aggressive investments in biologics and vaccine capacity in China, India, Japan, and ASEAN, with CDMOs and local biopharma firms rapidly adopting high throughput platforms and single?use technologies.?

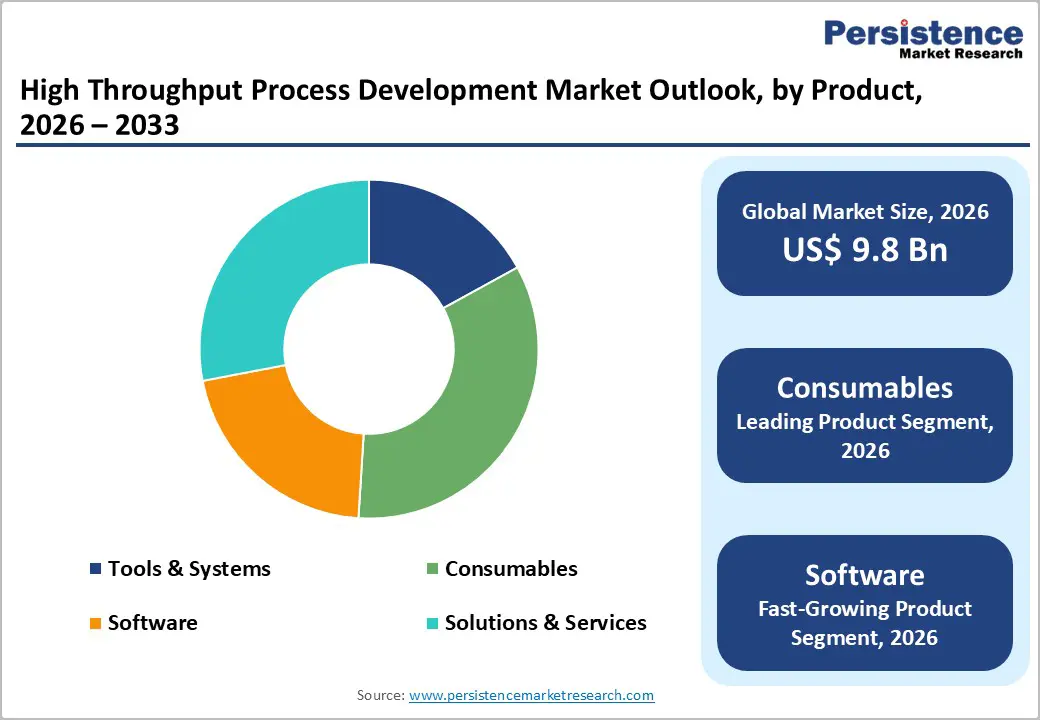

- The Consumables segment dominates product revenues with about 34% share in 2025, reflecting recurring usage of microplates, resins, and single-use accessories across intensive upstream and downstream screening workflows in bioprocess development.?

- Software is the fastest growing product segment as vendors integrate AI?driven DoE, digital twins, and advanced analytics into high throughput platforms, enabling smarter experiment design, faster optimization, and more effective data utilization across sites.?

- A key opportunity lies in applying high throughput process development to vaccines and cell and gene therapies, where governments and industry are funding advanced manufacturing hubs that rely on automated, data?rich workflows to ensure speed, scalability, and quality.

| Key Insights | Details |

|---|---|

| High Throughput Process Development Market Size (2026E) | US$ 9.8 billion? |

| Market Value Forecast (2033F) | US$ 17.3 billion |

| Projected Growth (CAGR 2026 to 2033) | 8.4%? |

| Historical Market Growth (CAGR 2020 to 2025) | 7.1% |

Market Dynamics

Market Growth Drivers

Rising biologics, vaccines, and advanced therapy pipeline

Escalating global demand for monoclonal antibodies, recombinant proteins, cell and gene therapies, and novel vaccines is a primary driver for high throughput process development solutions. Biopharmaceutical pipelines now include thousands of candidates, and developers must rapidly screen media, feed strategies, and process parameters across hundreds of conditions to reach robust manufacturing processes in compressed timelines. Regulatory agencies such as the U.S. FDA and European Medicines Agency (EMA) encourage enhanced process understanding through PAT and QbD, which inherently rely on dense experimental and analytical data, making high throughput tools indispensable in modern biologics manufacturing. During the COVID?19 pandemic, accelerated vaccine development demonstrated how high throughput screening, automation, and integrated analytics can cut development timelines significantly, setting new expectations for speed and scalability in future programs.?

Regulatory push for PAT, QbD, and continuous bioprocessing

Global regulators have issued influential guidance to support innovative manufacturing and real?time quality assurance, underpinning steady adoption of high throughput experimentation. The FDA’s Process Analytical Technology (PAT) guidance and subsequent updates emphasize real?time monitoring, risk?based control, and science?driven development, encouraging manufacturers to adopt integrated analytical tools, miniaturized reactors, and automated sampling to generate large datasets for model?based decision?making. In parallel, the shift toward continuous bioprocessing in biologics and biosimilars production is accelerating, as leading companies deploy perfusion bioreactors and continuous chromatography platforms that require robust, high throughput process development during scale?up. This regulatory and technological convergence is enhancing demand for automated design?of?experiments (DoE), multiplex analytics, and software?driven optimization modules embedded in high throughput systems.?

Market Restraints

High capital investment and integration complexity

Despite clear benefits, advanced high-throughput platforms often require substantial upfront investments in robotic liquid handlers, integrated bioreactor arrays, multiplex analyzers, and data infrastructure. Small and mid-sized biotechnology firms and academic centers may struggle to justify these costs without clear utilization plans or collaborative funding models. Integration of diverse hardware and software components, including LIMS, MES, and data?analytics platforms, can be complex and resource-intensive, particularly in legacy facilities with limited digital maturity. These factors can delay procurement decisions and slow penetration in emerging markets.?

Skills gap, data management, and standardization challenges

High-throughput process development generates large, complex datasets that demand expertise in multivariate statistics, chemometrics, and, increasingly artificial intelligence (AI) and machine learning for actionable insights. Many organizations report shortages of process data scientists and automation engineers capable of maintaining and optimizing sophisticated high-throughput systems. In addition, lack of standardized protocols, reference materials, and validation frameworks for some high-throughput analytical methods, particularly in vaccine and viral vector development, can limit broad regulatory acceptance and slow implementation. Data silos and inconsistent metadata practices further hinder cross?site comparability and reuse of historical development data.?

Market Opportunities

Expansion of software, AI, and data?driven optimization solutions

One of the most attractive opportunities lies in software and analytics, which is identified as the fastest?growing segment within the high throughput process development ecosystem. Vendors are increasingly embedding AI?driven design?of?experiments, Bayesian optimization, and digital twin capabilities into their platforms to propose optimal process conditions with fewer experiments and higher success rates. For instance, recent umbrella reviews on AI in vaccine R&D show that AI can significantly streamline target identification, formulation optimization, and scale?up by integrating genomic, preclinical, and manufacturing data. Similar tools applied to high throughput process data can accelerate process characterization, enable adaptive control strategies, and support continuous bioprocessing initiatives, creating recurring revenue opportunities for software providers and platform integrators.?

Growing demand from vaccines, cell and gene therapy, and intensified manufacturing

High throughput process development is poised to benefit from the sustained expansion of vaccines and cell and gene therapy (CGT) manufacturing capacity worldwide. In vaccines, high throughput sequencing and screening techniques are already used to assess safety, effectiveness, and genomic variation, with applications across mRNA, viral vector, and recombinant protein platforms. In CGT, intensified and small?volume processes demand rapid optimization of media, transfection parameters, and purification conditions using miniaturized bioreactors and parallel chromatography. Governments and industry consortia are investing heavily in advanced manufacturing hubs in North America, Europe, and Asia Pacific, many of which prioritize high throughput experimentation, automated sampling, and PAT as part of “biopharma 4.0” agendas. This ecosystem creates fertile ground for vendors offering integrated bioreactor arrays, automated sample handling, and analytics specifically tailored to vaccines and CGT workflows.?

Category-wise Insights

Product Analysis

The Consumables segment accounts for approximately 34% of the high throughput process development market in 2025, making it the leading product category due to recurring demand across all stages of bioprocess development. This segment includes microplates, tips, membranes, chromatography resins, filters, single?use bioreactor accessories, and assay reagents that are consumed in large volumes when screening hundreds or thousands of conditions. As high throughput experimentation scales, consumables benefit from higher run frequencies, assay miniaturization, and increased adoption of single?use technologies in both upstream and downstream workflows. Vendors differentiate through low?binding materials, improved chemical compatibility, and formats optimized for automation, which reduce variability and increase data quality, further reinforcing consumables as a stable, high?margin revenue stream.?

Application Analysis

Within applications, bioprocess development is the leading segment in the high throughput process development market, contributing an estimated share of around 45?50% in 2025 across global users. Bioprocess development teams rely on high throughput tools to optimize media compositions, feeding strategies, pH and temperature profiles, and purification conditions across multiple molecules and scales, helping compress development timelines from years to months. The rise of complex biologics, biosimilars, and intensified continuous processes has expanded the number of variables that need systematic exploration, making high throughput DoE a core requirement rather than a niche capability. Regulatory expectations for robust process characterization and lifecycle management also drive investment in high throughput platforms that can generate rich datasets to support control strategies and comparability studies.?

Process Stage Analysis

By process stage, upstream process development is typically the leading segment, accounting for an estimated 55?60% share of high throughput process development spending in 2025, as cell culture optimization is highly experiment?intensive. Cell line selection, media and feed optimization, and process intensification (such as perfusion and high?cell?density cultures) require systematic evaluation of large design spaces, which is best achieved using high throughput mini?bioreactors, micro?bioreactors, and automated sampling solutions. Moreover, the move toward continuous and intensified upstream processes in biologics and vaccines magnifies the need for robust, small?scale models to predict large?scale performance. High throughput upstream platforms enable this scaling insight, supporting lower development risk and more efficient technology transfer to clinical and commercial manufacturing facilities.?

End User Analysis

Among end users, biopharmaceutical & biotechnology companies represent the dominant segment in high throughput process development, with an estimated market share above 50% in 2025. Large biopharma organizations operate extensive biologics and vaccine pipelines and maintain multiple manufacturing sites, requiring standardized, scalable high throughput platforms to harmonize process development across regions. These companies are at the forefront of adopting automation, PAT, and continuous bioprocessing, aligning with strategic initiatives to boost productivity and reduce cost of goods for complex therapies. Contract research organizations (CROs) and contract manufacturing organizations (CMOs) also increasingly deploy high throughput platforms to differentiate their service offerings, but big biopharma remains the primary purchaser of sophisticated integrated systems, analytics software, and consumables.?

Regional Insights

North America High Throughput Process Development Market Trends

North America continues to be the leading region in the High Throughput Process Development (HTPD) market, driven by its robust biopharmaceutical R&D ecosystem, strong adoption of cutting?edge automation and analytics platforms, and deep investment in advanced bioprocessing infrastructure. Major hubs in the U.S. and Canada host leading biotech firms, contract research organizations, and academic collaborations that prioritize rapid process screening and optimization, accelerating technology uptake. The presence of favorable regulatory support and substantial funding for biologics innovation further reinforces North America’s dominance, enabling early integration of AI?driven and high?throughput solutions in drug discovery and biomanufacturing. As a result, the region accounts for a significant share of global HTPD revenues and remains a center for ongoing technological advancement and strategic market growth.

Asia Pacific High Throughput Process Development Market Trends

The Asia Pacific region is emerging as a high-growth market for High Throughput Process Development (HTPD) due to its rapidly expanding biopharmaceutical and biotechnology sectors. Countries like China, India, Japan, and South Korea are witnessing increased investment in biologics R&D, contract manufacturing, and academic-industry collaborations, driving demand for high-throughput instruments, consumables, and software solutions. Growing government initiatives to support life sciences innovation, coupled with lower operational costs and a skilled workforce, are attracting global HTPD players to establish regional operations. Additionally, rising adoption of automation, AI-driven analytics, and miniaturized bioreactor systems is enabling faster drug discovery and efficient process optimization. As a result, the Asia Pacific market is experiencing the fastest CAGR globally, positioning it as a strategic growth hub for HTPD technologies and attracting sustained attention from leading industry players.?

Competitive Landscape

Market Structure Analysis

The competitive landscape of the High Throughput Process Development market is highly dynamic and moderately concentrated, with established players continually innovating to differentiate through advanced automation, integrated analytics, and AI?driven solutions. Competition is driven by the need to offer comprehensive platforms that combine speed, accuracy, and scalability to meet rising demands in biologics and process optimization. Companies are investing in strategic partnerships, mergers, and R&D to enhance capabilities and broaden market reach.

Key Market Developments

- In December 2025, Bio-Techne Corporation, a global provider of life science tools, reagents, and diagnostic products, launched its first shipment of its next-generation Leo™ System, powered by Simple Western™ Technology.

- In November 2025, Aber Instruments and Sartorius Stedim Biotech announced the introduction of the BioPAT®?Viamass single-use biomass sensor, which was fully integrated into Ambr® 250 High Throughput single-use bioreactor vessels. This expansion marked a significant milestone in scaling advanced Process Analytical Technology (PAT) across the Sartorius bioreactor portfolio, including both Biostat STR® Generation 3 and Biostat® RM systems.

Companies Covered in High Throughput Process Development Market

- Thermo Fisher Scientific

- Sartorius

- Danaher

- Merck KGaA (MilliporeSigma)

- Agilent Technologies

- Tecan Group, Eppendorf

- PerkinElmer

- Bio-Rad Laboratories

- Cytiva

- Hamilton Company

- Beckman Coulter

- Waters Corporation

- Shimadzu

- GEA Group

- Repligen

- Pall Corporation

- Mettler-Toledo

Frequently Asked Questions

The global high throughput process development market is estimated to reach around US$ 9.8 billion in 2026, supported by increasing adoption of automated bioprocess development tools and data‑rich optimization platforms across major biopharmaceutical hubs

Key demand is driven by the expanding pipeline of biologics, vaccines, and cell and gene therapies, which requires rapid optimization of complex upstream and downstream processes using automated, high throughput experimentation supported by PAT and QbD frameworks.

North America leads the market, underpinned by strong U.S. biopharmaceutical R&D, advanced manufacturing infrastructure, and supportive FDA guidance that promotes adoption of PAT, continuous bioprocessing, and automation-intensive high-throughput development platforms.

A major opportunity lies in software, AI, and analytics solutions that transform large high throughput datasets into optimized process conditions, particularly for vaccines and cell and gene therapies, enabling faster development and more robust continuous manufacturing strategies.

Thermo Fisher Scientific, Sartorius, Danaher, Merck KGaA (MilliporeSigma), etc.