- Food Ingredients & Additives

- High Maltose Syrups Market

High Maltose Syrups Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

High Maltose Syrups Market by Product Type (Maltose Syrup (<50%), High Maltose Syrup (50–70%), Ultra-High Maltose Syrup (>70%)), by Source (Corn/Maize, Rice, Wheat, Others), End-user (Food & Beverage, Pharmaceutical, Cosmetics & Personal Care, Others), and Regional Analysis from 2026 - 2033

High Maltose Syrups Market Share and Trends Analysis

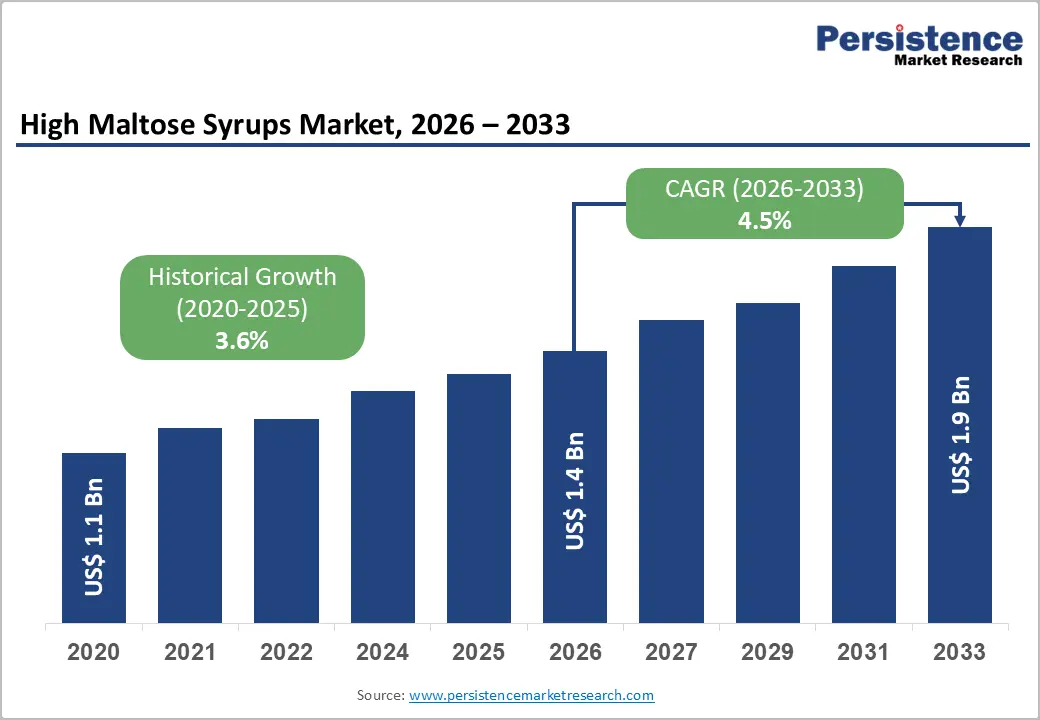

The global high maltose syrups market size is likely to be valued at US$ 1.4 billion in 2026 to US$ 1.9 billion by 2033 growing at a CAGR of 4.5% during the forecast period from 2026 to 2033. High maltose syrup quietly delivers liquid sweetness to a wide array of everyday foods, yet the industry is undergoing a dynamic transformation.

Strategic advances in sourcing, evolving regulatory landscapes, and sophisticated formulation innovations are redefining its competitive edge and fueling global growth. Presently, the market momentum extends far beyond sheer volume-it's increasingly driven by functional performance, regulatory compliance, and application-specific innovation that unlock new possibilities across confectionery, bakery, beverages, and beyond.

Key Industry Highlights

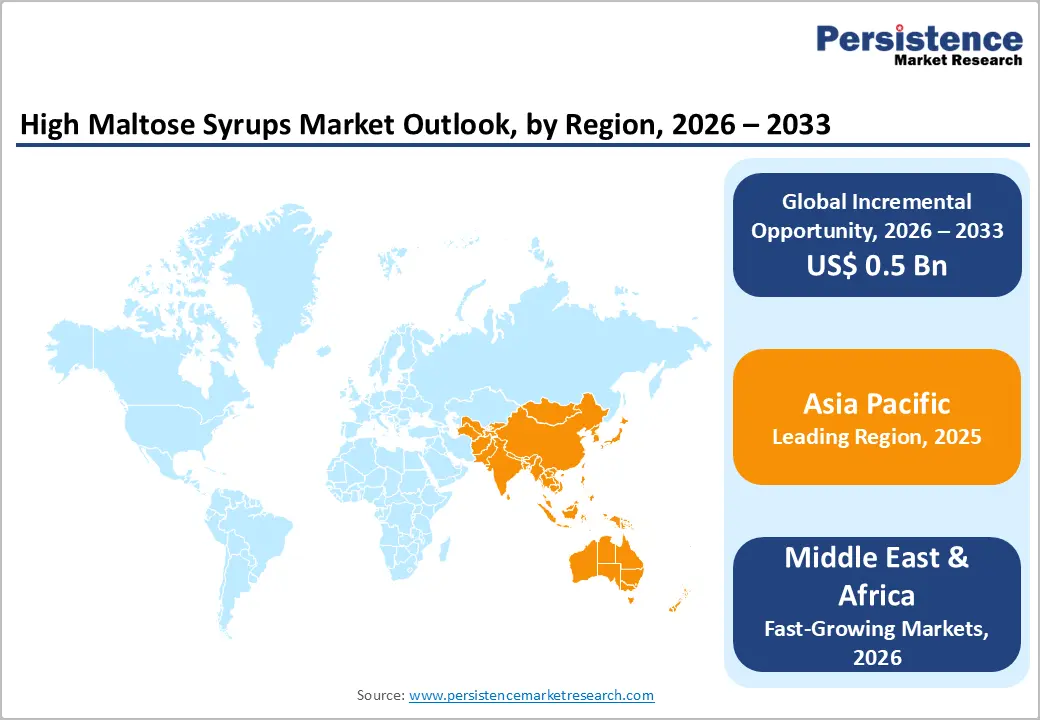

- Leading Region: Asia Pacific, holding approximately 41% market share, supported by large-scale starch processing capacity, strong confectionery demand, and rapid expansion of packaged foods across China, India, and Southeast Asia.

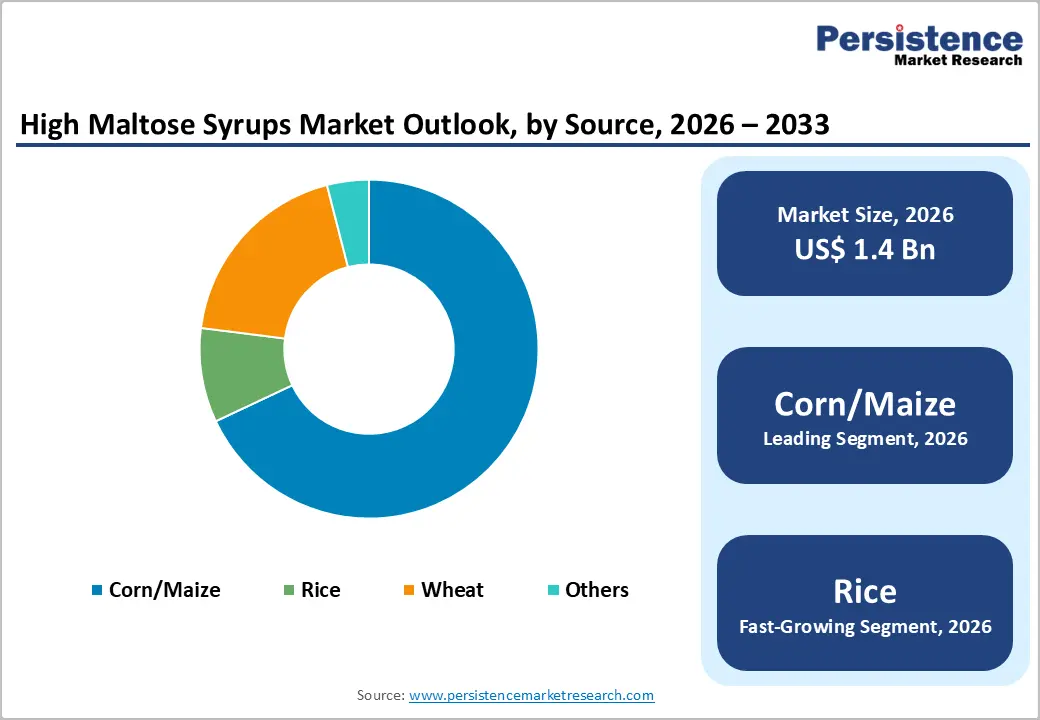

- Dominant Source Segment: Corn/Maize, accounting for around 68% market share, due to abundant availability, mature wet milling ecosystems, cost efficiency, and reliable enzymatic conversion for high-volume food processing.

- Market Drivers: Growth in processed and convenience foods sustains demand for liquid sweetener systems that deliver consistent sweetness, viscosity control, browning performance, and shelf-life stability under industrial conditions.

- Opportunities: Development of rice- and cassava-based high maltose syrups with gluten-free and clean-label positioning enables differentiation in premium, infant, and allergen-sensitive food applications.

- Key Developments: In November 2025, Tate & Lyle PLC launched a regenerative agriculture program in France to strengthen sustainable corn sourcing. In July 2025, Samyang Corporation introduced an AI-driven sugar reduction solution in the U.S., signaling a shift toward data-led formulation strategies.

| Key Insights | Details |

|---|---|

|

Global High Maltose Syrups Market Size (2026E) |

US$ 1.4 Bn |

|

Market Value Forecast (2033F) |

US$ 1.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.6% |

Market Dynamics

Driver - Growing processed food consumption sustains demand for liquid sweetener systems

Production lines operating at high speed reflect how processed foods have become everyday staples, reinforcing demand for functional liquid sweeteners such as high maltose syrups. These syrups provide consistent sweetness, viscosity, and process control, making them essential in bakery, confectionery, beverages, and convenience foods. Their liquid form allows smooth incorporation into automated systems, supporting uniform texture, reliable fermentation, and stable shelf performance at scale.

As packaged food consumption expands across urban and emerging economies, manufacturers favor ingredients that deliver predictable results under intensive processing conditions. High maltose syrups help manage browning, retain moisture, and preserve freshness across extended supply chains. This operational dependence anchors long-term demand, keeping liquid sweetener systems central to formulation strategies in the global high maltose syrups market.

Restraints - Regulatory pressure on sugar reduction slows volume growth

Policy signals flashing across nutrition labels are reshaping how sweeteners are evaluated, placing high maltose syrups under growing scrutiny. Governments and health authorities are tightening guidelines around added sugars, encouraging manufacturers to reformulate products with lower sweetness intensity or alternative sweetening systems. This pressure directly affects volume growth as high maltose syrups are often associated with traditional sugar profiles that attract regulatory attention.

Reformulation timelines add further friction. Food processors face technical challenges when reducing or replacing high maltose syrups without compromising texture, browning, or shelf life. As brands experiment with blends, enzymes, or high-intensity sweeteners, demand growth for conventional high maltose syrups can soften. Regulatory uncertainty across regions also complicates long-term planning, creating cautious procurement behavior within the global high maltose syrups market.

Opportunity - Developing fortified rice- and cassava-based high maltose syrups to serve gluten-free and clean-label applications

New starch sources stepping into the spotlight are reshaping innovation pathways for high maltose syrups. Rice- and cassava-based variants offer inherent gluten-free credentials and neutral flavor profiles, making them attractive for clean-label bakery, beverages, and infant-friendly foods. When fortified with minerals or functional carbohydrates, these syrups move beyond sweetness, supporting nutritional positioning while maintaining processing performance such as viscosity control and browning behavior.

For key players and startups, this opens room to differentiate through origin, functionality, and health alignment. Cassava enables localized sourcing in tropical regions, strengthening supply resilience, while rice supports premium positioning in allergen-sensitive applications. Fortified, single-source syrup narratives resonate with manufacturers seeking simplified labels and regional authenticity, creating scalable growth opportunities within the global high maltose syrups market.

Category-wise Analysis

By Source, Corn/Maize dominate the global High Maltose Syrups market

Corn/Maize holds approx. 68% market share as of 2025, reflecting its unmatched role as the backbone feedstock for high maltose syrup production. Abundant global availability, well-established wet milling infrastructure, and predictable starch quality make corn the preferred source for large-scale, cost-efficient processing. Its consistent enzymatic conversion performance supports high maltose yields, reliable viscosity control, and stable sweetness profiles, which are essential for bakery, confectionery, and beverage manufacturers operating high-volume production lines.

Wheat-based high maltose syrups serve a smaller but specialized segment. They are valued in regions with strong wheat supply chains and in applications where subtle flavor nuances are desirable. However, gluten considerations and higher processing complexity limit broader adoption, keeping corn firmly dominant in the global high maltose syrups market.

High maltose syrups sourced from rice are expected to show promising growth during the forecast period

High maltose syrups sourced from rice are projected to grow at a CAGR of 7.1% during the forecast period in the global High Maltose Syrups market, as manufacturers seek cleaner and allergen-friendly sweetening solutions. Rice offers a naturally neutral taste and smooth sweetness profile, making it well suited for sensitive applications such as infant foods, beverages, and premium bakery products. Its gluten-free positioning aligns strongly with evolving dietary preferences and clean-label formulation goals.

Beyond functionality, rice-based syrups support regional sourcing strategies across Asia and parts of Europe, improving supply stability and traceability. Processors value rice starch for its consistent gelatinization behavior and predictable conversion performance. As brands prioritize ingredient transparency and consumer trust, rice-derived high maltose syrups are gaining momentum across food and beverage formulations.

Region-wise Insights

Asia Pacific High Maltose Syrups Market Trends

Asia Pacific holds approximately 41% market share in the global High Maltose Syrups Market, reflecting the region’s strong base of starch processing capacity and expanding processed food consumption. In India, rising demand for packaged bakery and confectionery products is encouraging manufacturers to adopt liquid sweeteners that improve texture and shelf stability. Local producers are also exploring cassava and rice-derived syrups to meet clean-label and cost-efficiency goals.

In China, high maltose syrups are widely used in confectionery, dairy drinks, and traditional sweets, supported by large-scale corn processing infrastructure. Japan emphasizes precision in sweetness control, driving adoption in premium snacks and beverages, while South Korea’s growing ready-to-eat food sector favors syrups for moisture retention and consistency. Regional investments in food processing and formulation innovation continue to shape Asia Pacific market momentum.

North America High Maltose Syrups Market Trends

North America High Maltose Syrups Market shows a mature yet innovation-driven nature, shaped by advanced food processing infrastructure and consistent demand from bakery, confectionery, and beverage manufacturers. In the United States, producers are refining enzymatic processes to deliver tighter sweetness control and improved browning performance, supporting premium baked goods and snack formulations. Clean-label positioning is gaining traction, encouraging the use of non-GMO corn sources and simplified ingredient declarations.

In Canada, demand is influenced by strong frozen dessert and processed food segments, where high maltose syrups help maintain texture stability under temperature fluctuations. Manufacturers are also adapting formulations to align with sugar reduction strategies through precise usage levels rather than outright replacement. Cross-border trade, reliable raw material access, and focus on functional performance continue to define market dynamics across North America.

Market Competitive Landscape

The global High Maltose Syrups Market is moderately consolidated, with established starch processors holding strong production capabilities alongside regional players serving local demand. Leading companies are focusing on product innovation through improved enzymatic conversion techniques that enhance sweetness precision, viscosity control, and application-specific performance. Sustainability is becoming a competitive lever, with investments in energy-efficient processing, responsible corn sourcing, and waste valorization from starch by-products.

Production expansion remains active in Asia and North America as manufacturers scale capacity to meet growing demand from processed foods and confectionery. Regulatory frameworks around sugar labeling and food safety are shaping formulation strategies, encouraging compliance-driven innovation rather than volume expansion. Competitive advantage increasingly depends on technical support, supply reliability, and the ability to customize syrup profiles for diverse food applications.

Key Developments:

- In November 2025, Tate & Lyle PLC established a new regenerative agriculture programme to support its corn suppliers in France, strengthening sustainable farming practices and reinforcing long-term raw material resilience.

- In July 2025, Samyang Corporation unveiled an AI-based standardized sugar reduction solution at a U.S. food technology expo, highlighting its focus on data-driven formulation innovation and healthier food solutions.

Companies Covered in High Maltose Syrups Market

- Ingredion Incorporated

- Cargill, Incorporated

- Samyang Corporation

- Gujarat Ambuja Exports Limited

- Daesang Corporation

- The Sukhjit Starch & Chemicals Ltd

- AGRANA Beteiligungs-AG

- Nectafresh

- Sanstar Limited

- Bharat Glucose Pvt. Ltd.

- Kasyap Sweeteners Ltd.

- Others

Frequently Asked Questions

The global high maltose syrups market is projected to be valued at US$ 1.4 Bn in 2026.

Growing processed food consumption sustains demand for liquid sweetener systems is driving the growth of the global High Maltose Syrups market.

The global High Maltose Syrups market is poised to witness a CAGR of 4.5% between 2026 and 2033.

Developing fortified rice- and cassava-based high maltose syrups to serve gluten-free and clean-label applications is a key opportunity.

Major players in the global High Maltose Syrups market include Ingredion Incorporated, Cargill, Incorporated, Samyang Corporation, Gujarat Ambuja Exports Limited, Daesang Corporation, AGRANA Beteiligungs-AG, Sanstar Limited, and others.