- Food Ingredients & Additives

- High Fructose Corn Syrup Market

High Fructose Corn Syrup Market Size, Share, and Growth Forecast, 2025 - 2032

High Fructose Corn Syrup Market by Product Type (HFCS-42, HFCS-55, HFCS-90 & above), Application (Food & Beverages, Pharmaceuticals, Animal Feed), and Regional Analysis for 2025 - 2032

High Fructose Corn Syrup Market Size and Trends Analysis

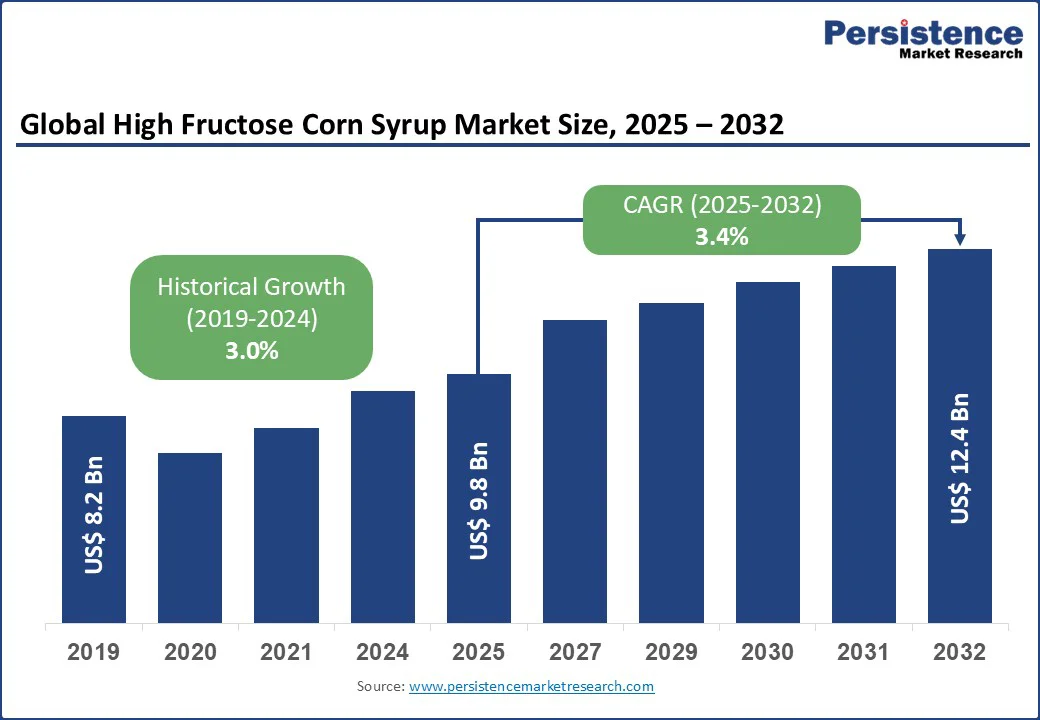

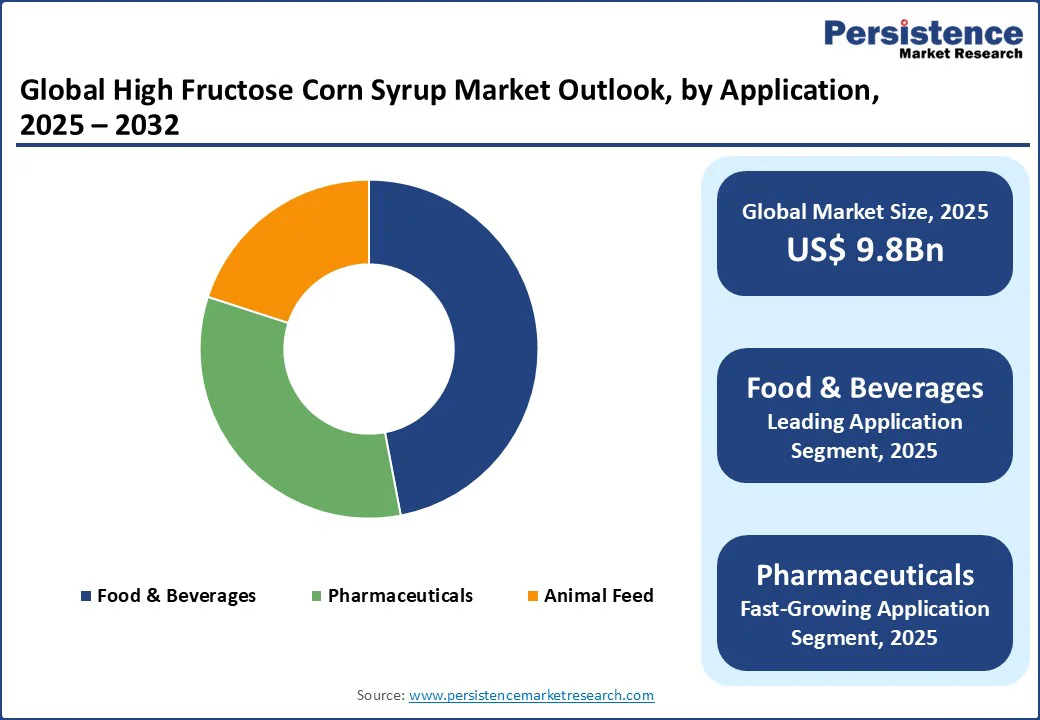

The global high fructose corn syrup (HFCS) market size is likely to be valued at US$ 9.8 Bn in 2025 and is expected to reach US$ 12.4 Bn by 2032, growing at a CAGR of 3.4% during the forecast period from 2025 - 2032.

Key Industry Highlights:

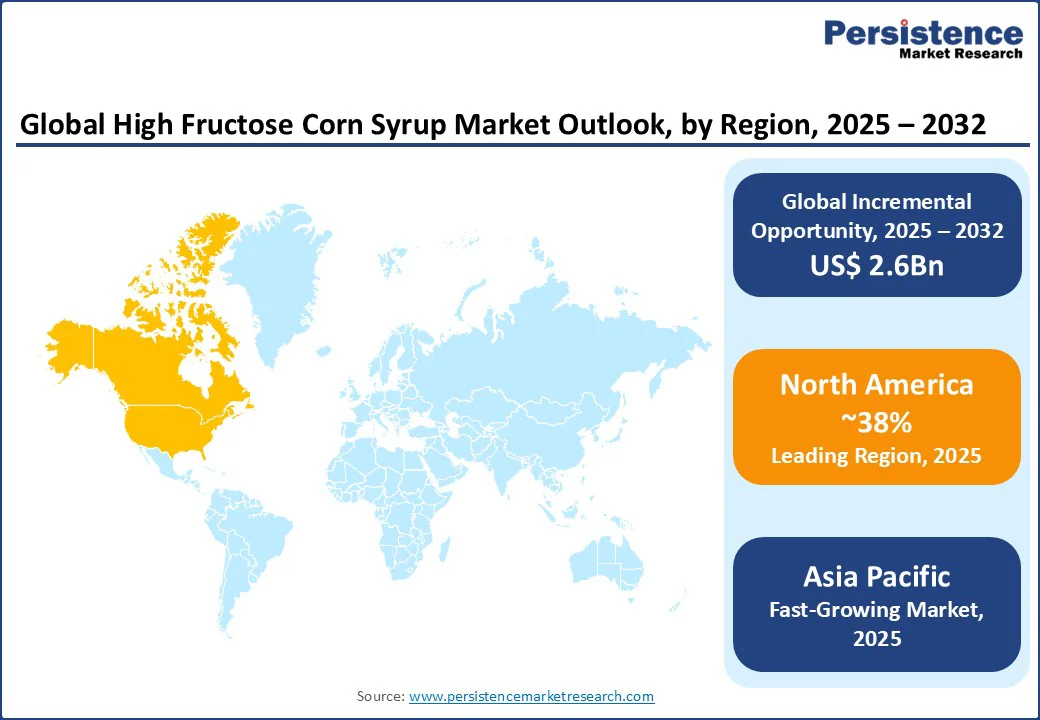

- Leading Region: North America holds the largest market share, accounting for 38% in 2025, driven by the U.S.’s robust food and beverage industry.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, fueled by rapid urbanization and increasing demand for processed foods in China and India.

- Dominant Product Type: HFCS-55 segment with a 52% share, widely used in soft drinks and processed foods.

- Leading Application: The food and beverage application segment leads with a 47% share, driven by demand for cost-effective sweeteners.

| Global Market Attribute | Key Insights |

|---|---|

| High Fructose Corn Syrup Market Size (2025E) | US$ 9.8 Bn |

| Market Value Forecast (2032F) | US$ 12.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.0% |

This growth is driven by the widespread use of HFCS as a cost-effective sweetener in the food and beverage industry, particularly in processed foods, soft drinks, and baked goods. It has seen steady expansion due to the increasing demand for convenient, shelf-stable food products, coupled with the rising global consumption of sweetened beverages.

Market Dynamics

Driver- Rising Demand for Cost-Effective Sweeteners in the Food and Beverage Industry

The growing demand for cost-effective sweeteners is a major driver of the global High Fructose Corn Syrup (HFCS) market. HFCS offers an economical alternative to traditional sugar, enabling food and beverage manufacturers to reduce production costs while maintaining sweetness and product quality.

Its high solubility, stability, and versatility make it ideal for applications across soft drinks, baked goods, confectionery, dairy products, and processed foods. With increasing global consumption of packaged and convenience foods, manufacturers are seeking sweeteners that balance affordability with functional performance.

For instance, Cargill’s SweetSpan HFCS-55 is widely used in beverages to provide consistent sweetness at a lower cost compared to cane sugar.

In regions such as Asia Pacific and Latin America, where price sensitivity is high, HFCS adoption is accelerating as it allows companies to meet consumer demand for affordable products without compromising taste.

For instance, ADM has expanded its HFCS production capacity in China to serve growing demand in soft drinks and processed foods. Additionally, the trend toward large-scale industrial food production has amplified the need for bulk sweeteners that are cost-efficient and consistent in quality. Overall, the economic benefits, wide applicability, and scalability of HFCS are positioning it as a preferred choice in the cost-driven global food and beverage sector.

Restraint- Health Concerns and Regulatory Scrutiny

Health concerns surrounding HFCS consumption pose a significant restraint on market growth. Studies linking high HFCS intake to obesity, diabetes, and other metabolic disorders have led to increased consumer awareness and regulatory scrutiny.

In regions such as North America and Europe, public health campaigns and advocacy groups have pushed for reduced sugar intake, prompting some manufacturers to explore alternative sweeteners such as stevia or agave. Regulatory bodies, such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), have imposed stricter labeling requirements and guidelines for HFCS usage in food products.

These regulations increase compliance costs and create challenges for manufacturers, particularly small and medium enterprises (SMEs). For instance, the European Court of Auditors' special report on food labeling highlights the EU's commitment to providing accurate and clear food information to consumers, which has implications for food producers' operations.

Additionally, consumer preferences are shifting toward natural and organic sweeteners, particularly in developed markets, which limits the growth potential of HFCS in premium product segments.

Opportunity- Expansion in Emerging Markets

The expansion into emerging markets represents a significant growth opportunity for the high fructose corn syrup market. Rapid urbanization, rising disposable incomes, and changing dietary patterns in regions such as the Asia Pacific, Latin America, and parts of Africa are driving increased consumption of processed foods, beverages, and convenience products.

HFCS, being a cost-effective and versatile sweetener, is well-positioned to meet the demand for affordable, scalable, and functional sweetening solutions in these markets.

Companies are leveraging this opportunity by establishing local production facilities, forming joint ventures with regional food and beverage manufacturers, and customizing HFCS formulations to suit local taste preferences.

For instance, ADM and Cargill have expanded manufacturing capacities in China and India to cater to the growing soft drink and packaged food sectors. Moreover, government initiatives supporting industrial food processing and trade facilitation in these regions further enhance market potential.

The combination of economic growth, evolving consumer lifestyles, and industrial support makes emerging markets a strategic focus for HFCS manufacturers seeking sustainable long-term growth.

Category-wise Analysis

Product Type Insights

HFCS-55 dominates, expected to account for approximately 52% of the share in 2025. Its dominance is attributed to its widespread use in the beverage industry, particularly in carbonated soft drinks, where it provides an optimal balance of sweetness and cost-effectiveness.

HFCS-55’s versatility and compatibility with large-scale production processes make it a preferred choice for major manufacturers such as Coca-Cola, PepsiCo, and Dr Pepper Snapple Group. Its ability to blend seamlessly with other ingredients and maintain product consistency further drives its adoption in processed foods and beverages.

The HFCS-90 & above segment is the fastest-growing, driven by its increasing use in pharmaceuticals and specialized food applications. Its high sweetness intensity allows for lower usage levels, making it cost-efficient for niche products such as low-calorie beverages and medicinal syrups.

The growing demand for high-potency sweeteners in health-focused formulations and the pharmaceutical industry’s need for stable, high-sweetness ingredients are accelerating the adoption of HFCS-90, particularly in North America and the Asia Pacific.

Application Insights

The food and beverage segment leads the high fructose corn syrup market, holding a 47% share in 2025. This dominance is driven by the extensive use of HFCS in soft drinks, baked goods, confectionery, and processed foods.

The segment benefits from the global expansion of the food processing industry and the rising demand for convenient, ready-to-eat products. HFCS’s cost advantages and functional properties, such as moisture retention and flavor enhancement, make it indispensable for large-scale food production.

The pharmaceutical segment is the fastest-growing, fueled by the increasing use of HFCS in medicinal syrups, cough drops, and other formulations. HFCS-90’s high sweetness and stability make it ideal for pharmaceutical applications, where precise sweetness levels and long shelf life are critical. The rise in chronic diseases and the growing demand for palatable medicinal products, particularly in emerging markets, are driving rapid adoption in this segment.

Regional Insights

North America High Fructose Corn Syrup Market Trends

North America is projected to hold the largest share of the global high fructose corn syrup (HFCS) market, accounting for approximately 38% in 2025. This dominance is largely driven by the United States, which boasts a well-established and highly developed food and beverage industry.

The region’s strong demand for soft drinks, baked goods, confectionery, dairy products, and processed foods underpins the consistent consumption of HFCS. Its versatility, high sweetness, and cost-effectiveness make HFCS an essential ingredient for manufacturers seeking to maintain product quality while controlling production costs.

The U.S. is home to major HFCS producers such as Archer Daniels Midland Company (ADM), Cargill, and Ingredion, whose large-scale production facilities and extensive distribution networks ensure a consistent supply across the region. Additionally, well-developed logistics, regulatory frameworks, and consumer acceptance of HFCS-containing products further support market growth.

The presence of established brands and the continuous launch of new processed food and beverage products contribute to high HFCS consumption. Furthermore, the focus on functional and specialty HFCS formulations, such as blends for low-calorie or high-fructose beverages, drives innovation, sustaining North America’s leadership position in the global high fructose corn syrup market.

Europe High Fructose Corn Syrup Market Trends

Europe is a significant player in the high fructose corn syrup market, supported by strong food processing industries and regulatory frameworks. Leading countries such as Germany, France, and the United Kingdom drive demand, with Germany holding the largest share due to its advanced food manufacturing sector.

Europe is characterized by the use of HFCS in baked goods, confectionery, and beverages, although its adoption is tempered by strict EU regulations on sugar quotas and health labeling. For instance, the EU’s sugar reform policies have historically limited HFCS production, but recent relaxations have spurred growth.

Companies such as Tate & Lyle and Roquette Frères are investing in R&D to develop HFCS formulations that comply with health standards and appeal to health-conscious consumers.

The growing demand for convenience foods and the expansion of retail chains in Eastern Europe are further boosting HFCS consumption. Europe’s focus on sustainability and clean-label products is encouraging manufacturers to explore HFCS blends with natural sweeteners, ensuring steady market growth.

Asia Pacific High Fructose Corn Syrup Market Trends

Asia Pacific is the fastest-growing region in the high fructose corn syrup market, driven by rapid urbanization, rising disposable incomes, and changing dietary patterns. Countries such as China and India are witnessing significant growth in the consumption of processed foods, beverages, and convenience products, creating strong demand for cost-effective sweeteners.

The expanding food and beverage industry, coupled with increasing westernization of diets, has accelerated the adoption of HFCS in products such as soft drinks, baked goods, confectionery, and dairy-based items. Key players, including Cargill, ADM, and Ingredion, are capitalizing on this growth by establishing local production facilities, forming joint ventures with regional food manufacturers, and customizing HFCS formulations to suit local taste preferences.

For instance, Cargill has expanded its corn milling and HFCS production capacities in China and India to serve the growing demand from beverages and packaged foods. Additionally, government initiatives supporting industrial food processing, trade facilitation, and food safety regulations further bolster market growth.

The combination of strong economic growth, evolving consumer lifestyles, and industrial support positions the Asia Pacific as a critical region for high fructose corn syrup market expansion.

Competitive Landscape

The global high fructose corn syrup market is highly competitive, shaped by regional strengths and a mix of global and niche players. In North America and Europe, major companies such as Archer Daniels Midland Company (ADM), Cargill, and Tate & Lyle dominate through scale, advanced production capabilities, and established supply chains.

In the Asia Pacific, rapid growth in the food processing sector and increasing demand for affordable sweeteners are attracting investments from international leaders such as Ingredion and Roquette Frères, alongside regional players such as Baolingbao Biology and DAESANG Corporation.

Companies are focusing on product innovation, including HFCS blends with natural sweeteners to address health-conscious consumer trends. Strategic partnerships with food and beverage manufacturers, investments in sustainable production, and vertical integration to secure corn supply chains are key strategies.

In emerging markets, local production facilities are being established to reduce costs and improve market penetration, while innovation in formulation and efficiency serves as a differentiator in this dynamic and evolving market.

Key Developments:

- In August 2022, Cargill announced plans to invest over $50 million in a sustainable corn syrup plant in Fort Dodge, Iowa, aiming to meet the growing demand for corn syrup in products ranging from infant formula to confectionery.

- In June 2024, Tate & Lyle announced new capabilities in texture and mouthfeel, including a proprietary formulation tool named Tate & Lyle Sensation. This initiative aims to help food and beverage customers reduce calories, sugar, and fat in their products, aligning with the growing consumer demand for healthier options.

Companies Covered in High Fructose Corn Syrup Market

- Archer Daniels Midland Company

- Cargill, Incorporated

- Ingredion Incorporated

- Tate & Lyle PLC

- Global Sweeteners Holdings Limited

- Showa Sangyo Co., Ltd.

- Roquette Frères

- DAESANG Corporation

- HUNGRANA KFT.

- Baolingbao Biology Co., Ltd.

- Sinofi Ingredients

- Kasyap Sweeteners Ltd.

- Others

Frequently Asked Questions

The global high fructose corn syrup market is projected to reach US$ 9.8 Bn in 2025.

The increasing demand for cost-effective sweeteners in the food and beverage industry is a key driver.

The HFCS market is poised to witness a CAGR of 3.4% from 2025 to 2032.

Expansion in emerging markets, particularly in the Asia Pacific, is a key opportunity.

Archer Daniels Midland Company (ADM), Cargill, Incorporated, Ingredion Incorporated, Tate & Lyle PLC, and Roquette Frères are key players.