- Hardware & Software IT Services

- Healthcare IoT Market

Healthcare IoT Market Size, Share, and Growth Forecast, 2026 - 2033

Healthcare IoT Market by Component Type (Hardware, Software, Services), Connectivity Technology (Wi-Fi, Bluetooth / BLE, Cellular (2G/3G/4G/5G), LPWAN (NB-IoT, LTE-M, LoRaWAN), RFID, Zigbee / Other Short-Range Protocols), Device Type (Wearable Medical Devices, Implantable Medical Devices, Stationary / In-hospital Medical Devices, Remote Medical Monitoring Devices, Non-Medical Healthcare IoT Devices) End-user and Regional Analysis for 2026 - 2033

Healthcare IoT Market Size and Trends Analysis

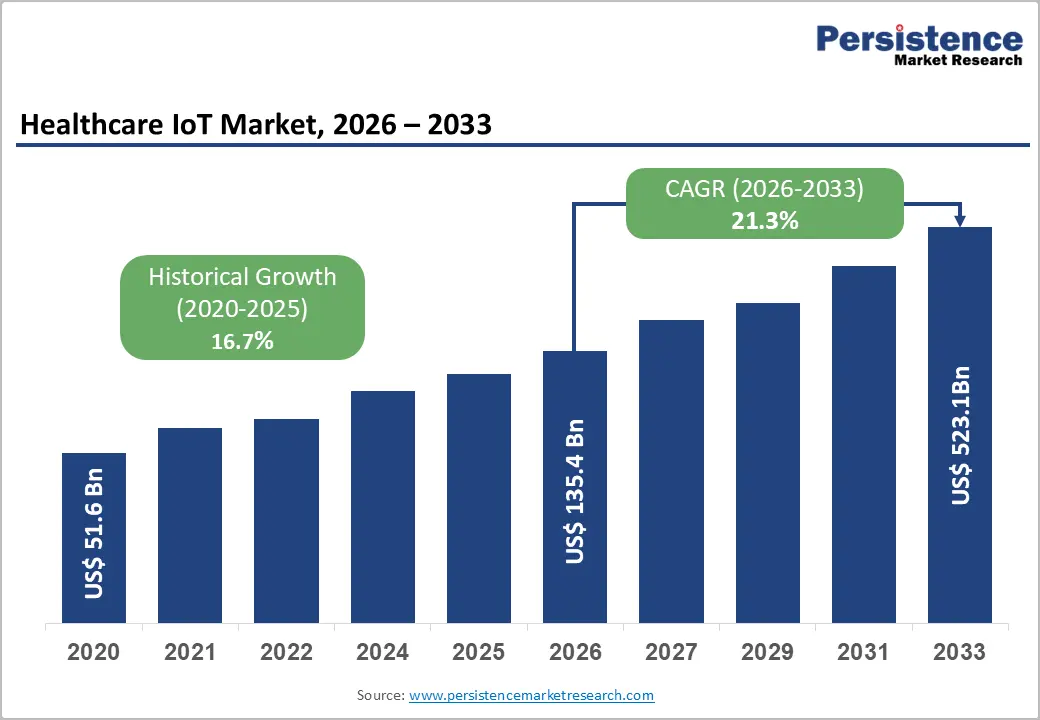

The Global Healthcare IoT Market size was valued at US$ 135.4 billion in 2026 and is projected to reach US$ 523.1 billion by 2033, reflecting a robust compound annual growth rate (CAGR) of 21.3% during this period. This substantial acceleration from the historical CAGR of 16.7% (2020-2026) underscores the sector's momentum as healthcare systems globally adopt interconnected medical devices, sensors, and platforms to enhance patient outcomes and operational efficiency.

The market expansion is fundamentally driven by escalating chronic disease prevalence, ageing demographic patterns, government-supported digital health infrastructure initiatives, and technological convergence of 5G networks with artificial intelligence and cloud computing.

Key Industry Highlights:

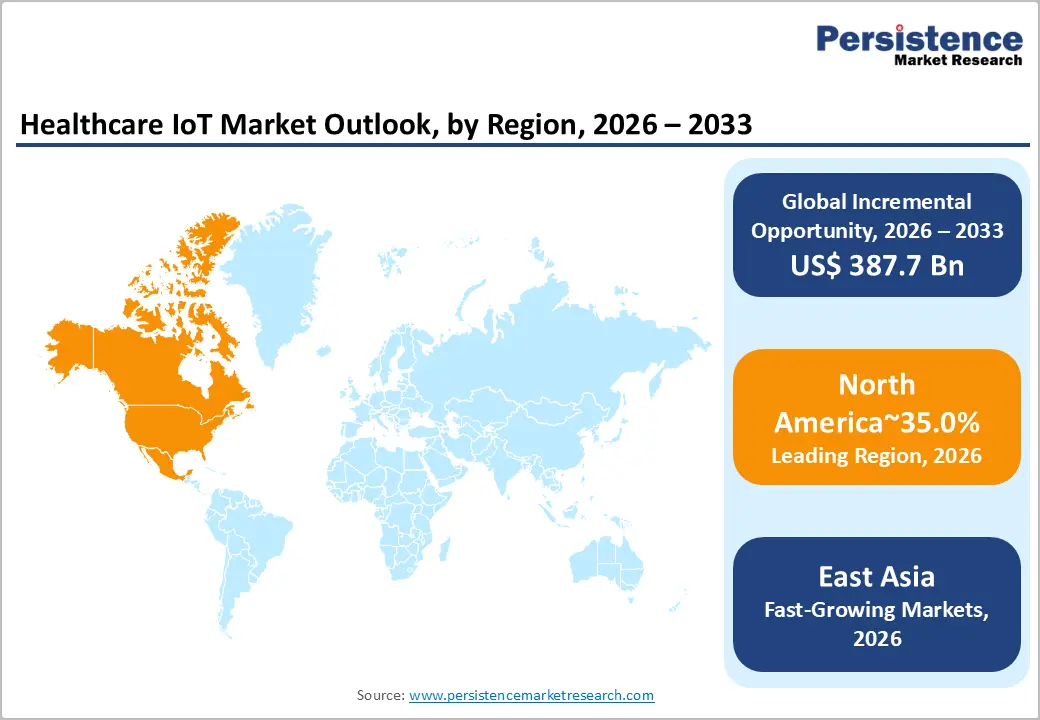

- Regional Leadership: North America dominates the global Healthcare IoT Market with ~35% share, supported by mature healthcare infrastructure, high technology adoption, and favorable reimbursement policies enabling connected care deployment.

- Fastest-Growing Region: East Asia accounts for ~22% share and represents the fastest-growing regional market, driven by China’s Healthy China 2030 initiative, Japan’s regulatory clarity for digital health, and South Korea’s advanced 5G infrastructure.

- Regional Prominence: Europe holds ~25% share, reflecting strong digital health investment, regulatory frameworks like the European Health Data Space, and initiatives addressing workforce shortages and chronic disease management.

- Leading Component Segment: Hardware leads the market with ~55% share, reflecting the critical role of medical sensors, wearable devices, implantables, and hospital monitoring infrastructure.

- Fastest-Growing End-user: Ambulatory care centers are the fastest-growing end-user segment, benefiting from outpatient-centric care models, lower capital requirements, and seamless integration with electronic health record systems.

- Connectivity Technology Leadership: Wi-Fi maintains ~30% connectivity market share as the leading technology, while Bluetooth Low Energy emerges as the fastest-growing segment due to widespread adoption in wearables and patient monitoring devices.

| Key Insights | Details |

|---|---|

|

Healthcare IoT Market Size (2026E) |

US$ 135.4 Bn |

|

Market Value Forecast (2033F) |

US$ 523.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

21.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

16.7% |

Market Dynamics

Drivers - Government Policy Support and Digital Health Infrastructure Investment

Government initiatives establishing digital health frameworks represent a critical enabling mechanism for Healthcare IoT Market expansion. The U.S. Food and Drug Administration (FDA) launched the Digital Health Innovation Action Plan, which establishes pathways for expedited clearance of digital health devices and includes the Pre-Certification (Pre-Cert) Program for software manufacturers.

The FDA announced the Technology-Enabled Meaningful Patient Outcomes (TEMPO) for Digital Health Devices Pilot in December 2025, designed to promote access to digital health devices while maintaining patient safety standards. India's Ayushman Bharat Digital Mission (ABDM), established with a five-year budget allocation of INR 1,600 crore (approximately US$ 192 million), has created 728.1 million digital health accounts and established the E-Sanjeevani telemedicine platform, which has facilitated approximately 372 million remote consultations through 220,000 healthcare providers.

The government's allocation to ABDM increased 70% in fiscal year 2023-2024 to INR 341.02 crore, signaling sustained commitment. In Europe, the European Health Data Space (EHDS) Regulation, which entered into force on March 26, 2025, establishes a unified framework for electronic health data exchange across EU Member States, with key implementation phases extending through 2029. These policy frameworks reduce regulatory uncertainty, accelerate device adoption, and create standardized infrastructure that facilitates Healthcare IoT Market penetration across diverse healthcare settings.

5G Network Deployment and Connectivity Technology Advancement

Fifth-generation (5G) wireless networks are enabling a transformative shift in Healthcare IoT Market capabilities by providing ultra-reliable, low-latency connectivity required for real-time clinical applications. The global 5G in healthcare market is expanding at a significant CAGR. This technological infrastructure is fundamental to emerging use cases, including remote surgery, high-resolution medical imaging transmission, and continuous wearable device monitoring without perceptible latency.

Industry forecasts suggest approximately 22 million 5G IoT units will be deployed in the 4.0 industry and healthcare segments by 2030. The integration of 5G network slicing technology enables healthcare providers to establish dedicated connectivity channels for critical patient services, ensuring security and reliability. 5G Reduced Capability (RedCap) technology bridges 4G LTE and 5G, creating cost-effective pathways for resource-constrained healthcare settings.

This technological advancement eliminates transmission delays that previously constrained real-time clinical decision-making and enables the Healthcare IoT Market to expand into applications requiring instantaneous data synchronization across multiple medical devices and systems.

Restraint - Capital Expenditure Requirements and Integration Complexity

High implementation and operational costs represent the most significant barrier to Healthcare IoT Market adoption, particularly among smaller healthcare providers. Beyond initial hardware and sensor procurement, healthcare organizations must allocate substantial capital for data storage infrastructure, cybersecurity systems, software licensing, technical personnel training, and continuous system maintenance. Financial analysis from healthcare supply chain research identifies high deployment costs as the primary impediment, especially given sustained budget constraints across hospital systems.

Integration with legacy healthcare IT infrastructure creates additional complexity and expense. Lack of standardization across different vendors' IoT systems requires custom integration work, multiplying implementation timelines and costs. Smaller hospitals and ambulatory care centers in resource-constrained geographies face particular difficulty justifying capital allocation to IoT solutions, thereby limiting Healthcare IoT Market scalability across certain geographic and provider segments.

Opportunity - AI-Enabled Diagnostic and Predictive Analytics Integration

Ambulatory care centers represent an emerging high-growth segment within the Healthcare IoT Market, driven by healthcare systems' strategic shift toward outpatient-centric delivery models. Ambulatory care centers are increasingly prioritizing IoT-enabled connectivity solutions to optimize operational workflows, enhance real-time clinical decision-making, and facilitate seamless integration with electronic health record systems. These centers benefit from lower capital requirements relative to hospital infrastructure while generating comparable patient volumes, creating favorable unit economics for IoT technology adoption. The Medical Device Connectivity Market analysis indicates ambulatory care centers will experience around 22-25% CAGR growth through 2034, substantially exceeding hospital segment growth rates.

Value-based care reimbursement models create strong incentives for healthcare providers to adopt remote monitoring and predictive analytics capabilities enabled by IoT devices. By demonstrating improved patient outcomes, reduced hospital readmissions up to 75% reduction documented in remote patient monitoring research, and lower total cost of care, healthcare providers can negotiate superior reimbursement terms with payers.

Private equity investors and healthcare service companies are actively acquiring healthcare IT and IoT platforms that advance value-based care delivery, with notable 2024-2025 transactions including Bain Capital's acquisition of HealthEdge and New Mountain Capital's formation of an AI-driven revenue cycle management platform. The Healthcare IoT Market thus benefits from the convergence of regulatory incentives, reimbursement economics, and investor capital concentration on outpatient care optimization.

AI-Enabled Diagnostic and Predictive Analytics Integration

The convergence of IoT data generation capacity with artificial intelligence and machine learning algorithmic sophistication creates unprecedented diagnostic and prognostic capabilities. AI-powered medical imaging analysis for computed tomography and magnetic resonance imaging scans, combined with real-time IoT sensor data, enables earlier disease detection and more precise treatment stratification than conventional clinical assessment methodologies.

Advanced analytics applied to remote patient monitoring datasets identify deterioration patterns 72-96 hours before acute clinical events, enabling preventive interventions that reduce intensive care unit admissions and associated healthcare expenditures. The Healthcare IoT Market increasingly incorporates AI-native architectures where embedded edge computing processes sensor data locally, reducing cloud transmission bandwidth while enabling sub-second clinical decision support for life-critical applications, including robotic surgery guidance and real-time hemodynamic optimization.

Venture capital investment in AI-powered healthtech companies reached US$16.9 billion in 2024, a 219% increase from 2023, reflecting investor conviction regarding AI-driven Healthcare IoT Market expansion. Organizations successfully integrating AI analytics into connected device platforms achieve differentiation through superior clinical outcomes and operational efficiency metrics, positioning them as preferred technology partners within emerging value-based care reimbursement models.

Category-wise Analysis

Component Type Insights

Hardware components, encompassing medical sensors, wearable devices, implantable systems, and hospital-based monitoring infrastructure, commanded 55.0% of the global healthcare IoT market share in 2026. This leadership position reflects the essential role of sensor technology in generating the clinical-quality data upon which IoT platforms operate. Wearable sensors for continuous glucose monitoring, cardiac rhythm tracking, and vital sign measurement demonstrate rapid innovation cycles and expanding clinical validation, supporting migration from episodic monitoring within hospital settings to continuous surveillance in ambulatory and home-based care environments.

Implantable medical devices incorporating wireless connectivity such as pacemakers, defibrillators, and neuromodulation systems, increasingly incorporate Bluetooth 5.4 and ultra-wideband protocols that enable remote monitoring while reducing power consumption through advanced semiconductor design.

Smart hospital infrastructure encompasses building automation, patient tracking, asset management, and environmental monitoring systems that leverage low-cost IoT sensors to optimize facility operations, reduce equipment loss, and enhance patient safety.

Industry Insights

Wi-Fi and wireless local area network technologies maintained approximately 30% market share of connectivity-based Healthcare IoT Market segmentation in 2026, retaining leadership through mature deployment infrastructure, high data throughput, and integration with existing hospital information technology networks.

Hospitals have invested in Wi-Fi 6 and emerging Wi-Fi 6E technologies that triple available spectrum through 6 gigahertz band allocation, reducing interference and supporting simultaneous high-bandwidth applications, including medical imaging transmission, telemedicine video conferencing, and high-frequency patient monitoring telemetry. Wi-Fi 7 technologies introduce multi-link operation that bonds 2.4, 5, and 6 gigahertz radios, eliminating packet loss during clinician handoffs a critical safety requirement in hospital environments.

Bluetooth Low Energy technologies represent the fastest-growing connectivity segment within the Healthcare IoT Market, driven by ubiquitous integration in consumer wearables, smartphones, and emerging health monitoring patches.

Continuous glucose monitors, cardiac monitors, and activity trackers primarily communicate through Bluetooth, enabling seamless integration with consumer smartphone ecosystems while maintaining battery life measured in weeks or months.

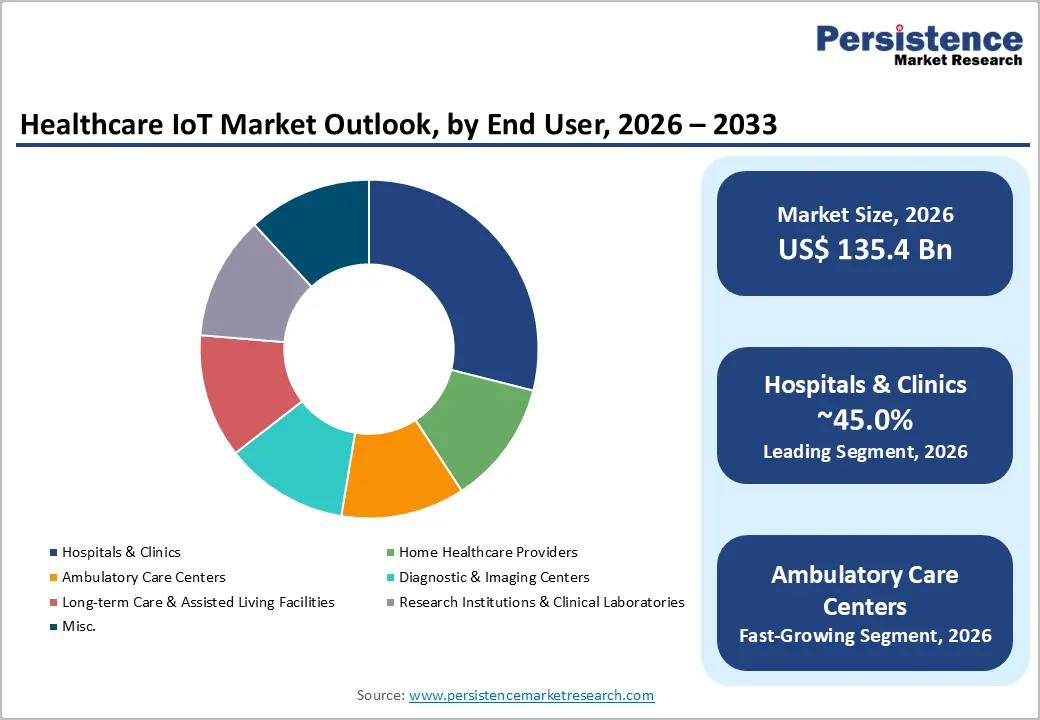

End-user Insights

Hospitals and clinics accounted for approximately 45% of the global revenue in 2026, reflecting their role as primary capital equipment purchasers and centers for complex clinical services requiring continuous patient monitoring and advanced diagnostic infrastructure.

Large hospital systems represent sophisticated technology purchasers with established information technology governance structures, dedicated clinical engineering departments, and integration capabilities to deploy multi-vendor IoT ecosystems. Hospital-based IoT applications encompass patient bedside monitoring, asset tracking and logistics management, environmental monitoring for infection prevention, staff communication systems, and supply chain optimization creating diversified revenue opportunities for healthcare IoT solution providers.

Ambulatory care centers, encompassing outpatient physician practices, urgent care clinics, surgery centers, and diagnostic imaging facilities, represent the fastest-growing end-user segment within the Healthcare IoT Market.

Regional Insights

North America Healthcare IoT Market Trends

North America retained approximately 35% of the global Healthcare IoT Market revenue in 2026, reflecting mature healthcare infrastructure, high technology adoption rates, and favorable reimbursement frameworks that incentivize connected care deployment. The United States dominates North American IoT healthcare spending, benefiting from Medicare remote physiologic monitoring CPT codes that provide US$60 per patient per month reimbursement, creating predictable revenue streams that justify healthcare provider capital investment.

Hospital and health system leaders prioritize cybersecurity infrastructure and electronic health record modernization as top digital investment categories, driving vendor consolidation around security-enhanced platforms capable of managing multi-vendor IoT ecosystems. North American healthcare providers have invested in advanced wireless infrastructure, with over 200 hospital systems operating private Citizens Broadband Radio Service 5G networks that isolate medical devices from administrative traffic, ensuring deterministic performance for patient monitoring and clinical decision-support applications. The integration of artificial intelligence and machine learning into IoT device platforms accelerates, with major manufacturers investing heavily in embedded analytics that differentiate devices through superior diagnostic insights rather than hardware specifications.

Canada's healthcare system supports satellite-backhauled telehealth for remote indigenous communities, demonstrating government commitment to extending Healthcare IoT Market services to underserved geographies despite infrastructure constraints. Mexico's social-security institute has equipped tens of thousands of diabetes patients with cellular glucometers, creating demand for cloud-based analytics and data management infrastructure. Health system consolidation trends across North America, driven by strategic buyers rather than private equity, continue to favor solutions offering broad interoperability and reduced vendor lock-in risk.

East Asia Healthcare IoT Market Trends

East Asia, comprising China, Japan, and South Korea, accounts for approximately 22% of the Global Healthcare IoT Market and represents the fastest-growing regional market in the forecast period.

China leads Asia Pacific Healthcare IoT adoption, supported by government-backed smart healthcare initiatives, including Healthy China 2030, which explicitly prioritizes medical device innovation and connected healthcare infrastructure development. The country's manufacturing cost advantages and integration of commercial IoT development with military applications enable rapid prototyping and scaling of connected medical devices at price points competitive with legacy incumbents. China's state-led approach to IoT standards development raises global competitiveness concerns while creating opportunities for Chinese manufacturers to establish market dominance in price-sensitive geographies.

Japan's healthcare system, characterized by sophisticated technological adoption and aging population demographics, has established clear regulatory pathways for digital health innovation, supporting rapid commercialization of connected wearables and remote monitoring platforms. South Korea's advanced 5G infrastructure and high smartphone penetration create attractive environments for mobile health and wearable-based IoT ecosystems. Southeast Asian healthcare systems increasingly recognize digital health investment as essential to managing rising chronic disease prevalence and healthcare workforce constraints, creating emerging opportunities for scalable, regionally adapted IoT solutions.

Europe Healthcare IoT Market Trends

Europe accounted for approximately 25% of the global Healthcare IoT Market revenue in 2026, representing mature markets with established healthcare IT infrastructure, robust regulatory frameworks, and increasing emphasis on healthcare digitalization driven by post-COVID policy evolution. The European Union has committed €17 billion in funding through the Recovery and Resilience Facility and Cohesion Policy programs through 2027 to support healthcare digitalization initiatives, creating government-backed demand for interoperable IoT solutions aligned with European Health Data Space standards.

Germany leads European healthcare digitalization investment, implementing the Health Data Use Act and Digital Act initiatives targeting electronic patient record systems and health data infrastructure modernization.

The German government actively supports digitalization adoption through regulatory clarification and funding, accelerating IoT solution deployment across private and public provider networks. Europe's healthcare systems confront critical workforce shortages, with an estimated 1.2 million-person deficit in doctors, nurses, and midwives, creating compelling economic cases for workflow automation and remote patient monitoring solutions that enable productivity gains per clinical FTE Aging population demographics with nearly one-third of EU citizens projected to exceed 65 years by 2050 generate disproportionate demand for chronic disease management and assisted living applications suitable for IoT-enabled monitoring.

Competitive Landscape

The global healthcare IoT market is moderately consolidated with oligopolistic tendencies, dominated by major players like Medtronic, GE Healthcare, Cisco Systems, IBM, Microsoft, and SAP SE. These companies lead in medical IoT devices, connectivity platforms, and cloud-based analytics, leveraging strong industry expertise and global reach. Mid-sized and regional players also compete in niche areas such as wearable devices, remote monitoring, and asset tracking. The market sees intense competition driven by strategic partnerships, co-development initiatives, and technology integration. High barriers to entry, including regulatory compliance and data security requirements, help established players maintain dominance.

Key Developments:

- Jun 2024, TE Connectivity expanded its healthcare-focused IoT sensor capabilities by showcasing advanced miniaturised sensors and high-performance connectivity technologies that enhance medical IoT device reliability and data transmission. The company strengthened its healthcare IoT portfolio through the integration of Laird Connectivity’s antenna business and Linx Technologies, supporting next-generation low-power medical devices. TE’s advancements in sensor-ready Satellite IoT connectivity further enable continuous remote patient monitoring in regions with limited terrestrial coverage.

- October 2024, Siemens deployed a customized IoT smart hospital platform at Kantonsspital Baden, integrating 7,000 IoT sensors and 2,000 smart asset tags to enhance patient experience and optimize hospital operations. The Siemens Xcelerator–based open platform enables real-time asset tracking, app-based navigation, and scalable digital use cases, positioning KSB as one of Switzerland’s smartest IoT-enabled hospitals.

Companies Covered in Healthcare IoT Market

- Medtronic

- Cisco Systems, Inc.

- IBM Corporation

- GE Healthcare

- Microsoft Corporation

- SAP SE

- Infosys Limited

- Cerner Corporation

- QUALCOMM Incorporated

- Amazon

- Intel corporation

- Wipro Ltd

Frequently Asked Questions

The global Healthcare IoT Market is projected to be valued at US$ 135.4 Bn in 2026.

The Hospitals & Clinics are expected to account for approximately 55.0% of the global Healthcare IoT Market by Solution Type in 2026.

The market is expected to witness a CAGR of 21.3% from 2026 to 2033.

Healthcare IoT market growth is driven by government support for digital health initiatives and infrastructure, along with advancements in 5G and connectivity technologies enabling real-time, low-latency clinical applications.

Key market opportunities in the Healthcare IoT Market include AI-enabled diagnostic and predictive analytics integration, rapid growth in ambulatory care centers, adoption of remote patient monitoring for value-based care, and increased investment in AI-driven healthtech platforms.

The key players in the Healthcare IoT Market include Medtronic, GE Healthcare, Cisco Systems, IBM, Microsoft, and SAP SE.