- Healthcare Services

- Healthcare Mobility Solutions Market

Healthcare Mobility Solutions Market Size, Share, and Growth Forecast 2026 - 2033

Healthcare Mobility Solutions Market by Product & Services (Mobile Devices, Mobile Applications, Mobile Applications), by Deployment (On-Premises, Cloud-Based, Button Cells), by Application (Patient Monitoring, Telemedicine, Mobile Health Records, Medication Management), by End User (Hospitals & Clinics, Diagnostic Centers, Home Healthcare, Pharma / Biotech), by Regional Analysis, 2026-2033

Healthcare Mobility Solutions Market Size and Trend Analysis

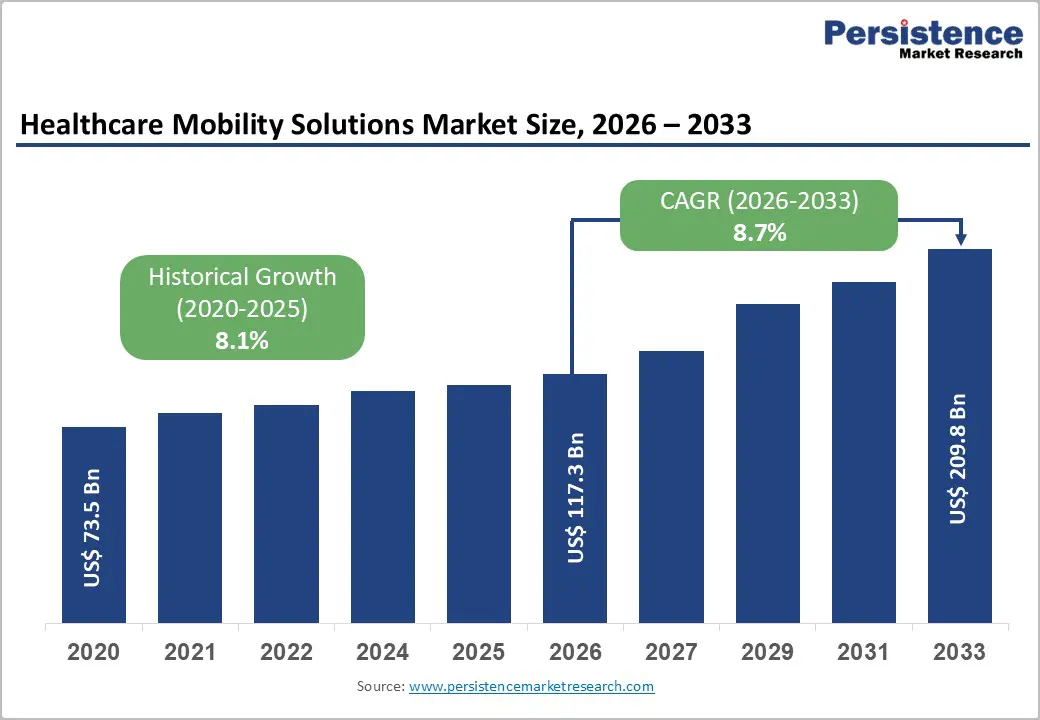

The global healthcare mobility solutions market size is expected to be valued at US$ 117.3 billion in 2026 and projected to reach US$ 209.8 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

This robust growth trajectory is driven primarily by the accelerating adoption of mobile devices in clinical settings, with approximately 92% of healthcare organizations acknowledging the necessity of automation to address staffing constraints, and the expanding telemedicine infrastructure, where around 300 hospitals in the U.S. utilize CMS waivers for acute home care delivery through mobile applications. The convergence of patient-centric care models, regulatory mandates supporting digital health frameworks such as the FDA's Device Software Functions policy updated in 2022, and the proliferation of remote patient monitoring capabilities, particularly for chronic disease management, are fundamentally transforming healthcare delivery ecosystems globally.

Key Market Highlights

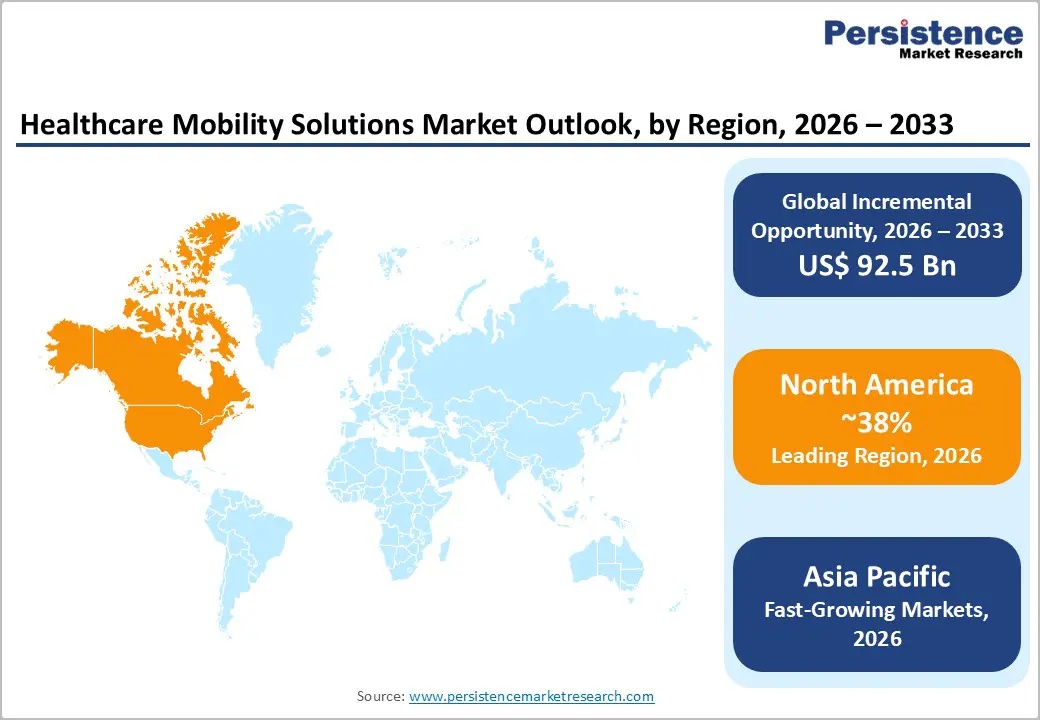

- Leading Region: North America dominates the healthcare mobility solutions market with 38% market share in 2025, driven by the United States' advanced digital health infrastructure, the FDA's progressive regulatory framework authorizing over 1,250 AI-enabled medical devices, widespread smartphone adoption, and CMS waivers enabling approximately 300 hospitals to deliver acute home care through mobile applications.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market with projected CAGR exceeding 10% during 2025-2032, fueled by 1.5 billion smartphone users, government digital health initiatives, including India's Ayushman Bharat Digital Mission and China's Healthy China 2030 plan, and demographic pressures creating urgent, scalable healthcare delivery needs.

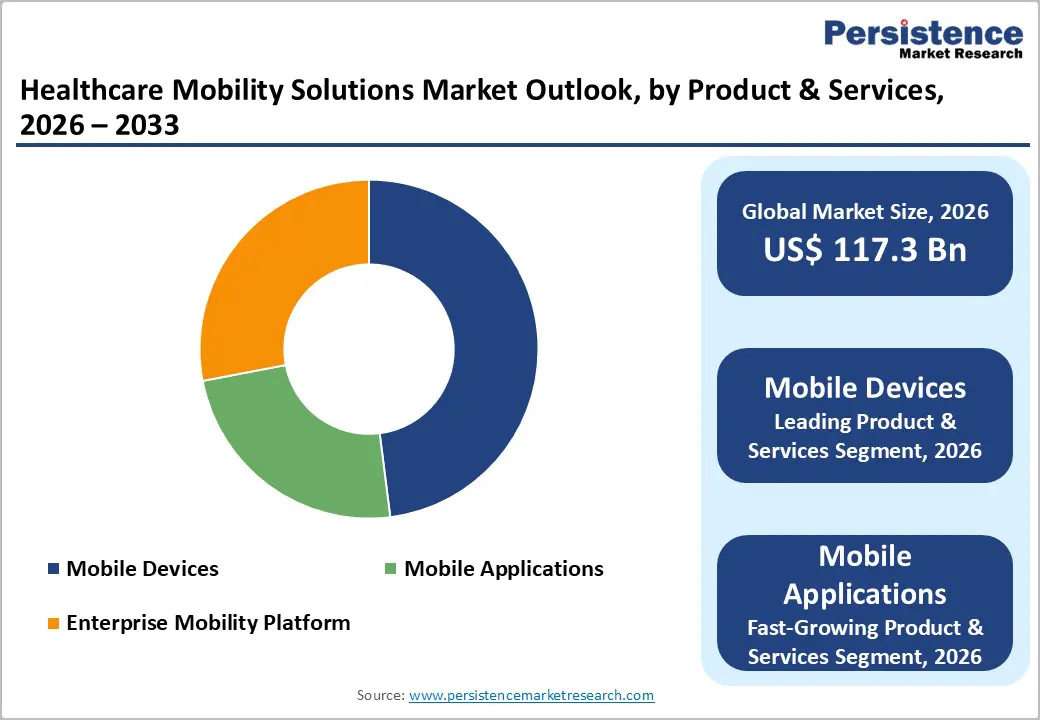

- Dominant Segment: Mobile Devices command 48% market share in 2025 within the Product & Services category, reflecting their fundamental role as infrastructure enabling real-time electronic health record access, medication verification, clinical collaboration, and photographic documentation across healthcare workflows, with manufacturers like Zebra Technologies providing comprehensive disinfection-ready portfolios.

- Fastest Growing Segment: Mobile Applications represent the fastest-growing Product & Services segment with projected CAGR exceeding 10% through 2032, driven by AI-assisted platforms, wearable device integration, chronic disease management applications, and expanding telemedicine capabilities supported by 5G network deployment and improved connectivity infrastructure.

- Key Market Opportunity: Artificial intelligence integration with healthcare mobility platforms presents transformative revenue opportunities, with FDA guidance published in December 2024 establishing clear pathways for AI-enabled device approvals, companies like Oracle Health introducing voice-prompt AI systems, and Asia Pacific startups deploying AI algorithms for smartphone-based diagnostics, addressing massive underserved populations.

| Global Market Attributes | Key Insights |

|---|---|

| Healthcare Mobility Solutions Market Size (2026E) | US$ 117.3 billion |

| Market Value Forecast (2033F) | US$ 209.8 billion |

| Projected Growth CAGR (2026-2033) | 8.7% |

| Historical Market Growth (2020-2025) | 8.1% |

Market Dynamics

Market Growth Drivers

Surge in Chronic Disease Prevalence and Remote Patient Monitoring Adoption

The escalating burden of chronic diseases is fundamentally reshaping healthcare delivery models and accelerating demand for mobility solutions. According to the World Health Organization, chronic conditions account for 63% of worldwide deaths, with cardiovascular disease, diabetes, and respiratory illnesses leading this epidemic. In the United States, three in four American adults have at least one chronic condition, with over half managing two or more, driving annual healthcare costs to $4.9 trillion. The CDC reports that more than 38 million Americans have diabetes, with an additional 98 million adults having prediabetes. This massive patient population requires continuous monitoring and medication management, which healthcare mobility solutions uniquely address through remote patient monitoring devices, mobile health applications, and integrated care platforms. Remote patient monitoring systems have demonstrated measurable impact, with systematic reviews showing a 18 per 1,000 patients reduction in all-cause hospitalization risk and a 37 per 1,000 patients decrease in condition-related hospitalizations. The ability to deliver continuous surveillance through connected devices while reducing hospital readmissions positions mobility solutions as essential infrastructure for managing the chronic disease epidemic cost-effectively.

Digital Transformation and Regulatory Framework Support

Government initiatives and regulatory frameworks are creating favorable environments for healthcare mobility adoption across major markets. The FDA has maintained clear oversight of mobile medical applications through its Device Software Functions guidance, with more than 1,250 AI-enabled medical devices authorized for marketing in the United States as of July 2025, reflecting substantial regulatory acceptance of digital health technologies. The FDA's establishment of the Technology-Enabled Meaningful Patient Outcomes (TEMPO) pilot in December 2025, in partnership with the Center for Medicare and Medicaid Innovation (CMMI) ACCESS model, demonstrates its institutional commitment to expanding access to digital health devices while safeguarding patient safety. In Europe, Germany's pioneering Digital Healthcare Act (DiGA), enacted in 2019 and strengthened by the Digital Act (DigiG) in February 2024, enables "apps on prescription," reimbursed by statutory health insurers, and covers approximately 90% of the German population. The Federal Institute for Drugs and Medical Devices (BfArM) maintains a fast-track approval process, expanding the number of approved applications from 24 at the end of 2021 to 68 by December 2024, with cumulative reimbursements totaling €234 million. These regulatory infrastructures reduce market entry barriers, accelerate innovation cycles, and provide reimbursement certainty that encourages sustained investment in healthcare mobility platforms.

Market Restraints

Data Security and Interoperability Challenges

Healthcare mobility solutions face significant challenges related to data protection and system integration that constrain market expansion. The Health Insurance Portability and Accountability Act (HIPAA) compliance requirements in the United States mandate rigorous security protocols for the transmission of patient health information, with violations carrying substantial penalties. Germany's enhanced cybersecurity measures introduced in the DigiG legislation mandate independent penetration testing and app hardening for all digital health applications, both new and existing, reflecting growing recognition of vulnerability risks. Interoperability remains a persistent barrier: approximately 66% of device-based remote monitoring studies lack electronic medical record integration, according to systematic reviews, forcing manual data entry that undermines efficiency gains. The fragmentation of healthcare IT systems and the diversity of proprietary platforms create quality and quantity losses in data exchange, limiting the seamless information flow necessary for optimal clinical decision-making. These technical challenges require substantial investment in cybersecurity infrastructure and standardized data exchange protocols, increasing implementation costs and extending deployment timelines for healthcare organizations.

Market Opportunities

Artificial Intelligence Integration and Predictive Healthcare

The convergence of artificial intelligence with healthcare mobility platforms represents a transformative opportunity for market participants to deliver next-generation clinical solutions. In August 2025, Oracle Health introduced an innovative electronic health record system utilizing AI technology, enabling clinicians to use voice prompts, substantially reducing manual data entry burdens. The FDA published final guidance in December 2024 titled "Marketing Submission Recommendations for a Predetermined Change Control Plan for Artificial Intelligence-Enabled Device Software Functions," establishing clear pathways for AI-enabled device approvals. Companies are developing sophisticated AI-assisted mHealth applications, including platforms like Sword Health for digital physical therapy, SkinVision for dermatological screening, and Raccoon .Recovery for mental health support, demonstrating the breadth of clinical applications. In Asia Pacific, particularly in China and India, startups are deploying AI algorithms to support overburdened diagnostic systems in rural hospitals, with platforms predicting diabetic retinopathy and cardiovascular disease using smartphone cameras. The InstaKC device, unveiled in India, represents the first smartphone-based, AI-driven, portable screening tool for keratoconus detection. As natural language processing, predictive modeling, and patient engagement tools mature, AI integration will enable proactive, personalized healthcare delivery that anticipates clinical deterioration, optimizes treatment protocols, and enhances patient outcomes while creating substantial revenue opportunities for technology providers.

Category-wise Insights

Product & Services Analysis

Mobile Devices dominate the healthcare mobility solutions market with 48% market share in 2025, driven fundamentally by the proliferation of smartphones, tablets, and wearable technologies delivering real-time access to electronic health records and patient data. The widespread adoption stems from clinical workflow optimization, where Zebra Technologies' comprehensive mobility portfolio enables healthcare workers to reliably access information in back-end clinical applications, scan barcodes for medication verification, preventing medical errors, collaborate through integrated communication systems, and capture photographic documentation for wound assessment and patient identification. Healthcare-grade mobile devices manufactured by Zebra Technologies are specifically designed to withstand frequent disinfection protocols required in clinical environments, featuring antimicrobial coatings and sealed interfaces protecting against fluid ingress while maintaining touchscreen functionality with gloved hands. The segment's dominance reflects institutional recognition that mobile devices serve as the fundamental infrastructure enabling all other healthcare mobility applications, from bedside medication administration and specimen collection to asset tracking and clinician collaboration.

Application Analysis

Patient Monitoring applications hold a leading position, with approximately 40% market share in 2025, reflecting the critical importance of continuous surveillance in modern healthcare delivery and chronic disease management. The segment's dominance is supported by systematic evidence: 72% of device-based remote monitoring studies report decreased hospital service utilization, and continuous measurement and data transmission yield superior outcomes compared with periodic monitoring. Remote patient monitoring systems enable healthcare providers to track vital signs, medication adherence, and disease progression without requiring in-person visits, addressing both the escalating chronic disease burden and healthcare staffing constraints. Approximately 300 hospitals in the United States use CMS waivers to deliver acute care at home through patient-monitoring applications that include virtual wound assessments, Bluetooth-enabled sensors, and on-demand physician dashboards. The 24/7 support characteristic of advanced patient monitoring platforms is associated with an 81% reduction in hospital service use, according to comprehensive systematic reviews. Companies like Philips Healthcare and Omron Corporation provide integrated monitoring solutions combining wearable sensors, wireless connectivity, and cloud-based analytics platforms enabling clinicians to identify clinical deterioration early and intervene proactively, ultimately improving patient outcomes while reducing healthcare system costs through hospitalization avoidance and complication prevention.

End User Analysis

Hospitals & Clinics represent the dominant end-user segment, with approximately 45% market share in 2025, driven by institutional scale, complex workflow requirements, and comprehensive integration needs across multiple clinical departments. Major healthcare technology providers, including Cerner Corporation, McKesson Corporation, Philips Healthcare, and IBM Corporation, are increasingly deploying mobile electronic health record systems, asset monitoring platforms, and telehealth applications within hospital environments to enhance operational efficiency and patient care quality. Hospitals serve large outpatient and inpatient populations requiring extensive diagnostic testing, creating substantial demand for mobility solutions that streamline clinician workflows, reduce medication errors through barcode verification, and enable real-time collaboration across care teams.

Regional Insights

North America Healthcare Mobility Solutions Market Trends and Insights

North America dominates the healthcare mobility solutions market with 38% market share in 2025, anchored by the United States' advanced digital health infrastructure, favorable regulatory environment, and widespread smartphone adoption. The region's leadership position reflects the FDA's progressive oversight framework for mobile medical applications, with over 1,250 AI-enabled medical devices authorized as of July 2025, creating regulatory certainty that encourages sustained investment in innovation. The Centers for Medicare and Medicaid Services (CMS) waivers enabling approximately 300 hospitals to deliver acute care at home through mobile applications demonstrate institutional support for mobility-enabled care models. AT&T and Cisco Systems provide robust connectivity infrastructure that supports seamless wireless coverage across healthcare facilities, while companies like AirStrip Technologies deliver real-time patient data access platforms that integrate with existing hospital information systems.

Asia Pacific Healthcare Mobility Solutions Market Trends and Insights

Asia Pacific is the fastest-growing regional market, with a projected CAGR exceeding 10% for 2025-2032, driven by rapid smartphone adoption, government digital health initiatives, and demographic pressures that create urgent needs for scalable healthcare delivery models. The region's 1.5 billion smartphone users in 2024, projected to reach 1.8 billion by 2030 according to GSMA data, provide the fundamental infrastructure for deploying mobile health applications. China dominates the regional market with 974.69 million smartphone users representing 68.4% population penetration as of June 2025, with Tencent's WeChat developing affiliated hospital networks enabling appointment scheduling, follow-up tracking, and medical bill settlement at scale. Government programs, including India's Ayushman Bharat Digital Mission and China's Healthy China 2030 plan, establish centralized platforms for health records, teleconsultation, and e-prescriptions, creating institutional frameworks supporting mobility solution adoption.

India emerges as the fastest-growing market in Asia-Pacific, with platforms like Practo, PharmEasy, and Tata 1mg democratizing access to virtual care, diagnostics, and e-pharmacy through mobile applications that support regional languages and UPI payments. The partnership between MediBuddy and Japan's Elecom in February 2025 to co-develop smart health IoT devices tailored for Indian markets demonstrates growing cross-border collaboration and localization efforts. In September 2025, L&T Technology Services partnered with SiMa.ai to promote AI-powered solutions across mobility, healthcare, industrial automation, and robotics, reflecting regional technology integration trends. In July 2022, Thailand's government collaborated to connect 116 government hospitals through integrated IT systems and mobile applications, exemplifying infrastructure investments that address rural healthcare access gaps. Japan and South Korea lead in home-care technology solutions and robotic monitoring for aging populations, with Society 5.0 initiatives prioritizing healthcare innovation. The region's manufacturing advantages, lower development costs, and massive underserved populations create exceptional opportunities for companies establishing early market presence in the Asia Pacific's rapidly evolving healthcare mobility ecosystem.

Competitive Landscape

The competitive landscape of the healthcare mobility solutions market is highly dynamic and fragmented, with numerous global and regional players competing for market share through continuous innovation, strategic partnerships, and expanded service offerings. Companies are heavily investing in advanced technologies such as AI, cloud computing, and real-time patient monitoring to improve clinical outcomes and workflow efficiency. There is a strong emphasis on product differentiation and interoperability, as firms develop integrated platforms and mobile applications tailored to evolving needs of providers and patients.

Key Market Developments

- In September 2025, L&T Technology Services Ltd. (LTTS) announced a strategic partnership with SiMa.ai, a Silicon Valley–based Physical AI company, to deliver AI-driven solutions across mobility, healthcare, industrial automation, and robotics.

Companies Covered in Healthcare Mobility Solutions Market

Oracle Corporation, Cerner Corporation, McKesson Corporation, Zebra Technologies, Cisco Systems, SAP SE, Philips Healthcare, AT&T, Omron Corporation, IBM Corporation, Samsung Electronics, AirStrip Technologies, Practo, MediBuddy, Tencent, Ping An Good Doctor, AvaSure, Equum Medical, Hundred Health, L&T Technology Services, NetSfere, Sword Health, SkinVision

Frequently Asked Questions

The global healthcare mobility solutions market is expected to be valued at US$ 117.3 billion in 2026.

The escalating chronic disease burden with 63% of worldwide deaths attributed to chronic conditions according to the World Health Organization, combined with digital transformation initiatives and regulatory frameworks like the FDA's Device Software Functions policy and Germany's Digital Healthcare Act (DiGA) establishing reimbursement pathways, fundamentally drive demand. Remote patient monitoring demonstrating 18 per 1,000 patients reduction in hospitalization risk provides measurable clinical and economic benefits accelerating adoption.

North America dominates with 38% market share in 2025, anchored by the United States' advanced digital health infrastructure, FDA authorization of over 1,250 AI-enabled medical devices as of July 2025, widespread smartphone adoption, favorable reimbursement policies through CMS waivers enabling approximately 300 hospitals to deliver acute home care, and concentration of leading technology providers including Oracle Corporation, Cerner Corporation, and McKesson Corporation.

Artificial intelligence integration presents transformative opportunities, with the FDA publishing final guidance in December 2024 establishing clear AI-enabled device approval pathways. Companies like Oracle Health introducing voice-prompt AI systems in August 2025, Asia Pacific startups deploying smartphone-based AI diagnostics like InstaKC for keratoconus screening, and platforms including Sword Health and SkinVision demonstrating the breadth of AI-assisted clinical applications create substantial revenue potential across predictive diagnostics, personalized treatment, and proactive care management.

Leading companies include Oracle Corporation, Cerner Corporation, McKesson Corporation, Zebra Technologies, Cisco Systems, SAP SE, Philips Healthcare, AT&T, Omron Corporation, IBM Corporation, Samsung Electronics, and AirStrip Technologies.