- Healthcare Services

- Healthcare Clinical Analytics Market

Healthcare Clinical Analytics Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Healthcare Clinical Analytics Market by Platform (Stand-alone, Integrated), Deployment (On-Premise, Cloud-based), End-user (Hospitals, Clinics, Insurance Companies, Government Payers, Others), Regional Analysis, from 2026 - 2033

Healthcare Clinical Analytics Market Share and Trends Analysis

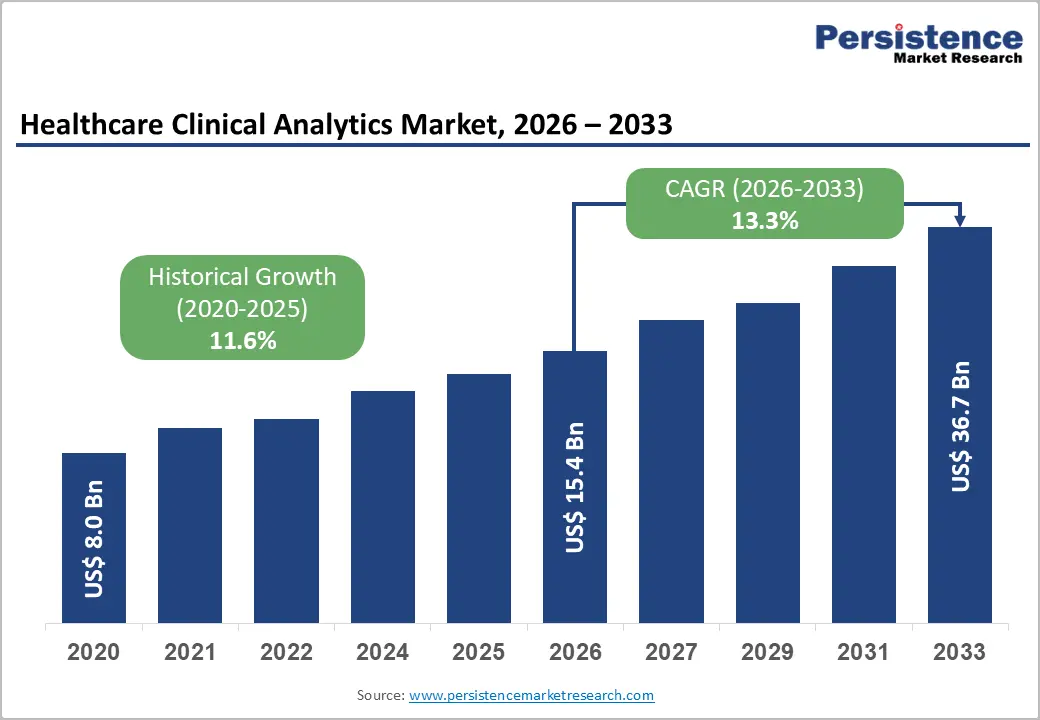

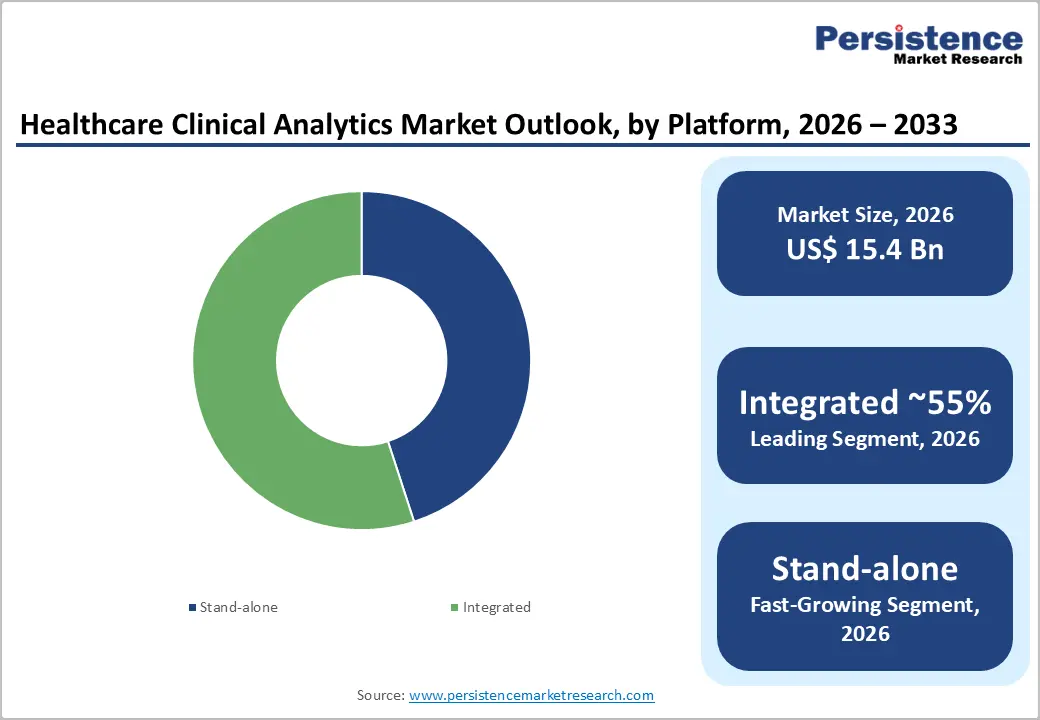

The global healthcare clinical analytics market size is estimated to grow from US$ 15.4 billion in 2026 to US$ 36.7 billion by 2033 growing at a CAGR of 13.3% during the forecast period from 2026 to 2033.

The global market is witnessing strong growth, driven by the rapid adoption of electronic health records (EHRs) and the storage of clinical data digitally. Healthcare systems are increasingly moving away from paper-based records toward digital platforms, enabling large volumes of patient data to be captured, stored, and analyzed efficiently. At the same time, rising pressure to reduce healthcare expenditure and improve clinical outcomes is accelerating the use of big data analytics, allowing providers to extract meaningful insights from complex datasets.

Healthcare clinical analytics plays a critical role in supporting the shift toward value-based care. By enabling data-driven clinical decision-making, these solutions help providers enhance care quality, eliminate avoidable costs, and improve operational efficiency. The ongoing transformation of healthcare infrastructure from fragmented manual data systems to integrated digital environments has made clinical information more transparent, accessible, and actionable, further strengthening the adoption of advanced clinical analytics solutions across care settings.

Key Industry Highlights

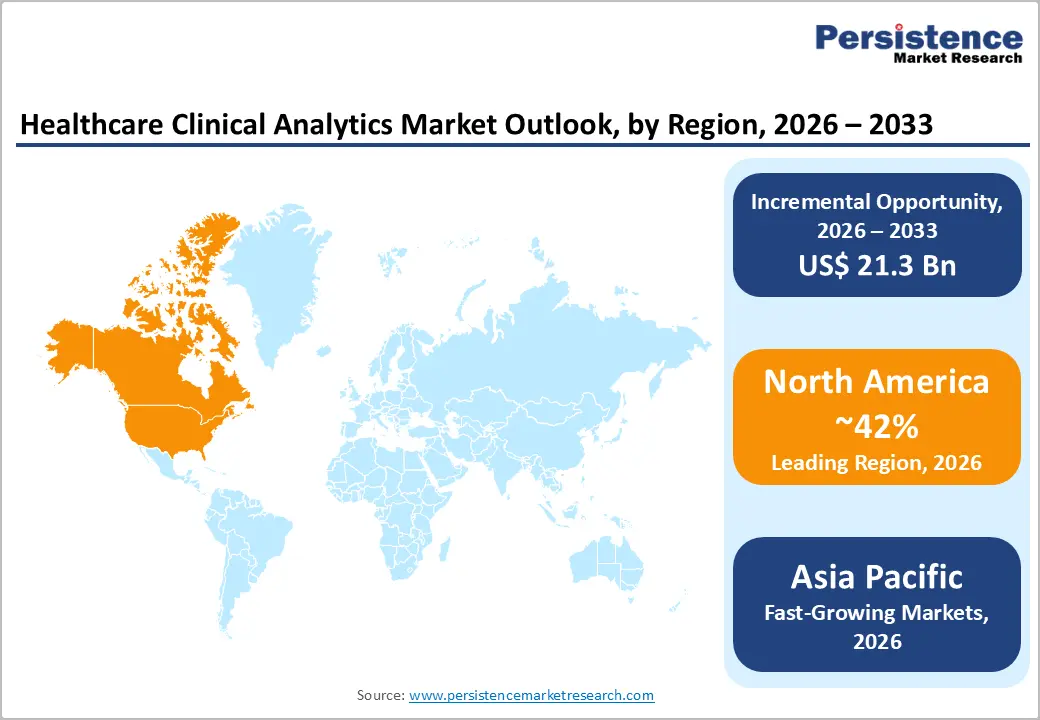

- Leading Region: North America dominates the market due to high EHR adoption, strong healthcare IT spending, advanced digital infrastructure, and value-based care initiatives.

- Fastest Growing Region: Asia Pacific is the fastest growing region, driven by rapid healthcare digitization, expanding hospital networks, government e-health programs, and rising chronic disease burden.

- Dominant Segment: Integrated platforms lead the market owing to seamless EHR integration, unified data management, enterprise-wide deployment, and reduced operational complexity for health systems.

- Fastest Growing Segment: Cloud-based deployment is growing rapidly, supported by scalability, lower infrastructure costs, faster implementation, and increasing acceptance of secure cloud healthcare solutions.

| Key Insights | Details |

|---|---|

|

Healthcare Clinical Analytics Market Size (2026E) |

US$ 15.4 Bn |

|

Market Value Forecast (2033F) |

US$ 36.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

13.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.6% |

Market Dynamics

Driver - Accelerating EHR and Data Digitization in Clinical Workflows

The rapid digitization of clinical workflows is a key driver fueling the growth of the healthcare clinical analytics market. Healthcare providers worldwide are increasingly adopting electronic health records, laboratory information systems, and imaging platforms to replace fragmented paper-based documentation. This shift has resulted in the continuous generation of structured and unstructured clinical data across care settings. In 2024, clinical analytics accounted for nearly half of healthcare big data analytics applications, underscoring its importance in transforming routine patient data into meaningful clinical insights that support diagnosis, treatment planning, and care coordination.

In addition, hospitals generate extremely large volumes of clinical information every year, including test results, clinical notes, and imaging data. Advanced analytics platforms are essential for aggregating, standardizing, and interpreting this data at scale. At the same time, reimbursement models are increasingly tied to documented quality outcomes, safety indicators, and care efficiency. As a result, healthcare organizations are under growing pressure from payers and regulators to demonstrate measurable performance improvements. Clinical analytics tools help providers track outcomes, identify gaps in care delivery, and optimize clinical pathways, making them a foundational component of modern, data-driven healthcare systems.

Restraints - Privacy, Security, and Governance Concerns Around Clinical AI

Despite strong adoption, the healthcare clinical analytics market faces significant restraints related to data privacy, security, and governance. Clinical data is highly sensitive, and healthcare organizations must comply with strict regulatory frameworks such as HIPAA in the United States and GDPR in Europe. These regulations impose rigorous standards for patient consent, data access controls, anonymization, and cross-border data transfers. Failure to comply can lead to significant financial penalties and reputational damage, making providers cautious in expanding analytics initiatives.

Additionally, governance expectations around clinical decision-support tools continue to evolve. Healthcare organizations are required to ensure transparency, traceability, and accountability in the generation and application of clinical insights. This often necessitates extensive validation, documentation, and monitoring, increasing deployment complexity. For many providers, especially smaller hospitals, these requirements raise implementation costs and extend procurement timelines. As a result, some organizations limit analytics adoption to select use cases until internal governance structures and compliance capabilities are fully established.

Opportunity - Expansion of Cloud-Based Clinical Analytics Platforms

Cloud-based deployment models represent a major growth opportunity for the healthcare clinical analytics market. Many healthcare organizations, particularly in emerging regions, face constraints related to on-premise infrastructure costs, maintenance complexity, and limited scalability. Cloud platforms offer flexible storage and computing capacity to support large volumes of clinical data without a significant upfront investment. This makes them especially attractive for hospitals seeking to modernize analytics capabilities while controlling capital expenditure.

In recent years, cloud deployments have gained strong traction within the broader clinical data analytics landscape, as providers increasingly rely on centralized platforms to manage diverse clinical datasets. Cloud-based solutions support faster system upgrades, streamlined data governance, and easier integration across multiple hospital sites. They also enable collaboration across networks, supporting research, quality improvement initiatives, and population-level analysis. As healthcare systems move toward unified enterprise data environments that combine clinical, operational, and population health data, demand for secure, compliant, and interoperable cloud analytics platforms is expected to rise significantly, creating sustained growth opportunities through the forecast period.

Category-wise Analysis

By Platform Analysis

Within the platform segment, integrated clinical analytics platforms hold a leading position, accounting for an estimated 55% share of the healthcare clinical analytics market in 2025. Healthcare organizations increasingly favor integrated solutions that align closely with existing electronic health record systems and enterprise data environments. These platforms support consistent data structures, unified dashboards, and centralized oversight across clinical, operational, and financial functions.

By enabling seamless data flow from collection and processing to analysis and reporting, integrated platforms reduce reliance on multiple independent tools and simplify system management. They also support standardized performance tracking and outcome measurement across departments, which is critical for large hospital networks. As health systems pursue enterprise-wide digital transformation strategies, vendors are expanding comprehensive analytics offerings that align with these goals. This approach enhances usability, reduces long-term operational complexity, and positions integrated platforms to continue capturing the majority of new investments over the forecast period.

By Deployment Analysis

Based on deployment model, cloud-based solutions are emerging as both the leading and fastest-growing segment in the healthcare clinical analytics market. Cloud deployment offers flexible computing and storage capabilities that can scale easily with increasing volumes of clinical data. This flexibility allows healthcare providers to manage complex datasets efficiently while avoiding the high costs associated with maintaining extensive on-site infrastructure. Cloud-based platforms also support easier system updates and enable secure access to analytics tools across multiple facilities, improving coordination among distributed care teams.

Healthcare organizations adopting cloud deployments report faster implementation of new analytical use cases, such as outcome benchmarking and performance monitoring across sites. As hybrid and multi-cloud strategies become more common and regulatory frameworks around cloud security continue to mature, confidence in cloud-based clinical analytics is strengthening. This trend is particularly strong among mid-sized hospitals and research-focused institutions seeking scalable, cost-efficient, and future-ready analytics environments.

Region-wise Insights

North America Healthcare Clinical Analytics Market Trends

North America, led by the United States, dominates the healthcare clinical analytics market due to widespread adoption of electronic health records, strong healthcare IT investment, and early movement toward value-based care. Hospitals and health systems in the region have integrated digital tools deeply into clinical workflows, enabling large-scale use of clinical data for performance tracking and outcome improvement. Government policies supporting EHR adoption, quality reporting, and data interoperability have further strengthened analytics usage across care settings. In addition, strong funding for digital health innovation has encouraged rapid development and deployment of advanced analytics solutions.

The region also benefits from a well-developed healthcare innovation ecosystem. Academic medical centers and large hospital networks regularly test and implement advanced clinical decision-support tools within routine care delivery. Many U.S. hospitals now use predictive models within their EHR systems to support early detection of patient deterioration, infection risks, and imaging prioritization. Ongoing efforts to improve data governance and safety standards continue to support sustained market growth.

Asia and Pacific Healthcare Clinical Analytics Market Trends

Asia Pacific is expected to be the fastest-growing region in the healthcare clinical analytics market, supported by rapid digital transformation and rising healthcare demand. Countries such as China, India, Japan, and several Southeast Asian nations are expanding healthcare infrastructure while adopting electronic health records and digital clinical systems. Growing populations, rising chronic disease prevalence, and limited clinical resources are driving the need for analytics solutions to improve efficiency and care quality.

Governments across the region are actively investing in digital health programs, national e-health platforms, and hospital modernization initiatives. These efforts are generating large volumes of clinical data, increasing demand for tools that help clinicians manage workloads and improve decision-making. The region also benefits from lower development costs and a growing local technology ecosystem, enabling the creation of region-specific analytics solutions. Although differences in regulations and digital readiness remain challenges, strong government support and ongoing infrastructure investments position Asia Pacific as a major growth driver for the global clinical analytics market through the next decade.

Competitive Landscape

The healthcare clinical analytics market is moderately concentrated, with a mix of global technology leaders and specialized healthcare IT vendors competing across platforms, deployment models, and clinical use cases. Major players such as IBM Corporation, Oracle Corporation, Cerner Corporation, McKesson Corporation, and Allscripts Healthcare Solutions, Inc., leverage deep portfolios in EHR, data platforms, and AI to provide integrated clinical analytics suites.

At the same time, firms like Optum Inc., Medical Information Technology Inc. (MEDITECH), Hewlett Packard Enterprise Company, QSI Management LLC, and CareCloud Corporation differentiate through domain-specific solutions, cloud-native architectures, and partnerships with providers and payers. Emerging business models increasingly revolve around software-as-a-service, outcome-based contracts, and co-development of predictive models with health systems, while investments in real-world evidence and population health analytics shape long-term product roadmaps.

Key Industry Developments:

- In June 2025, Stanford Health Care introduced ChatEHR, enabling 33 clinicians to access and query patient records using natural language as part of a controlled pilot program.

- In December 2023, MedLM became accessible to Google Cloud customers in the United States via an allowlisted general availability release on the Vertex AI platform.

Companies Covered in Healthcare Clinical Analytics Market

- IBM Corporation

- Cerner Corporation

- McKesson Corporation

- Allscripts Healthcare Solutions, Inc.

- Oracle Corporation

- Optum Inc.

- Medical Information Technology Inc.

- Hewlett Packard Enterprise Company

- Qsi Management LLC

- CareCloud Corporation

- Others

Frequently Asked Questions

The global healthcare clinical analytics market is projected to be valued at US$ 15.4 Bn in 2026.

Rising electronic records adoption, outcome-based reimbursement, expanding clinical data volumes, cost pressures, and demand for care improvements.

The global healthcare clinical analytics market is expected to witness a CAGR of 13.3% between 2026 and 2033.

Cloud platforms, regional digitization programs, analytics services, interoperability mandates, population health initiatives, and multi-hospital collaboration unlock opportunities.

North America is the leading region in the global healthcare clinical analytics market.