- Healthcare Services

- Connected Healthcare Market

Connected Healthcare Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Connected Healthcare Market by Solution Type (mHealth Services, mHealth Devices, e-Prescription), Application (Diagnosis & Treatment, Monitoring Applications, Wellness & Prevention, Healthcare Management, Others), End-user (Hospitals & Clinics, Home Monitoring), by Regional Analysis, 2026 - 2033

Connected Healthcare Market Share and Trends Analysis

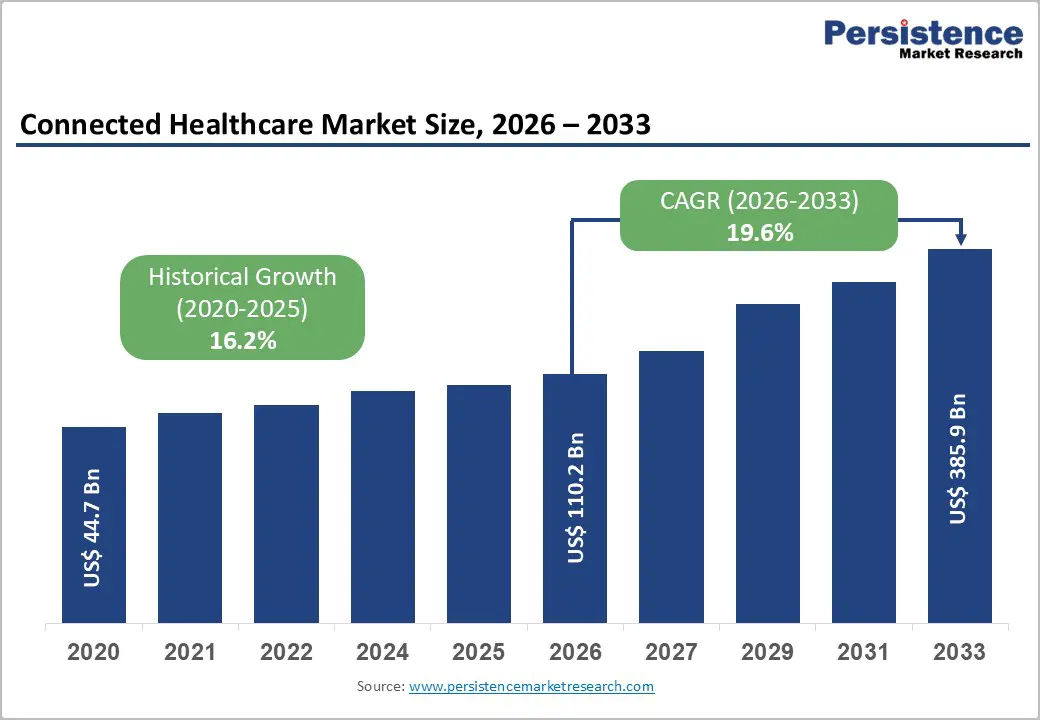

The global connected healthcare market size is expected to be valued at US$ 110.2 billion in 2026 and projected to reach US$ 385.9 billion by 2033, growing at a CAGR of 19.6% between 2026 and 2033. Connected healthcare refers to the integration of technology into healthcare services, enabling real-time communication and data exchange between patients, healthcare providers, and medical devices. The industry is witnessing significant growth driven by several emerging trends. One of the most prominent market trends is the increasing adoption of telehealth solutions, particularly accelerated by the COVID-19 pandemic, which has normalized virtual consultations.

The rise of wearable devices such as smartwatches and fitness trackers is empowering patients to take charge of their health by monitoring vital signs and activity levels. The integration of artificial intelligence (AI) and machine learning (ML) into connected healthcare systems is revolutionizing data analytics. The use of blockchain technology in managing EHRs is also gaining traction as it enhances data security and interoperability.

Key Industry Highlights:

- The demand for connected healthcare solutions especially remote patient monitoring, significantly contributed to market growth.

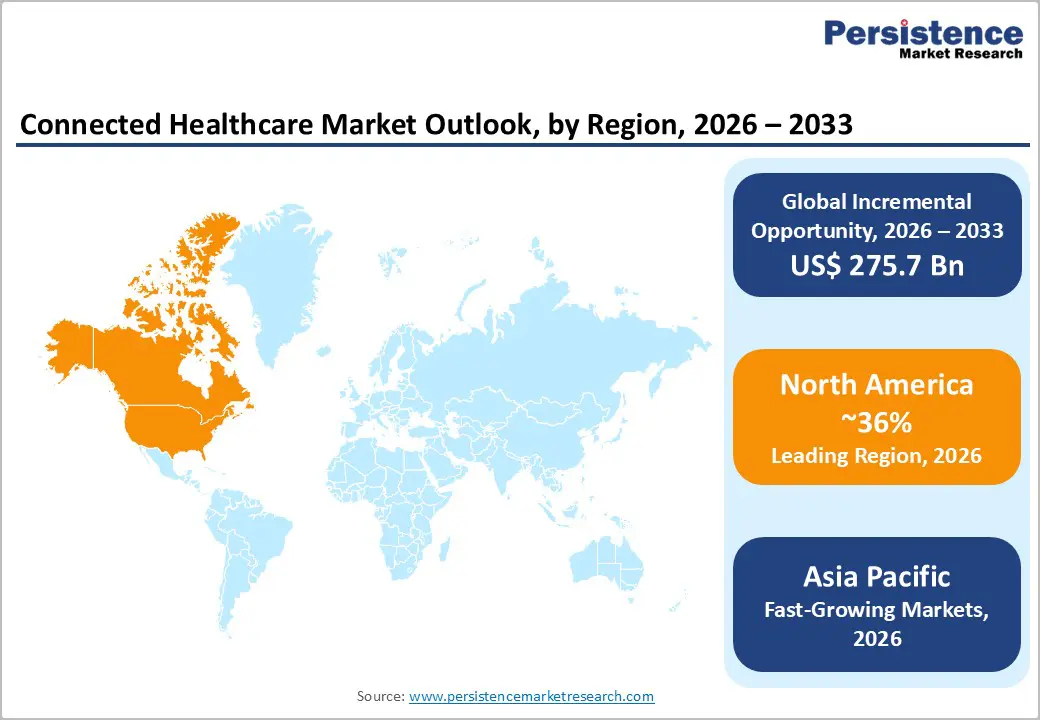

- Europe ranks as the second-largest market for connected healthcare with growth fueled by increased smartphone usage among consumers and healthcare professionals.

- The adoption of remote patient monitoring services in Europe allows for effective tracking of health conditions from a distance.

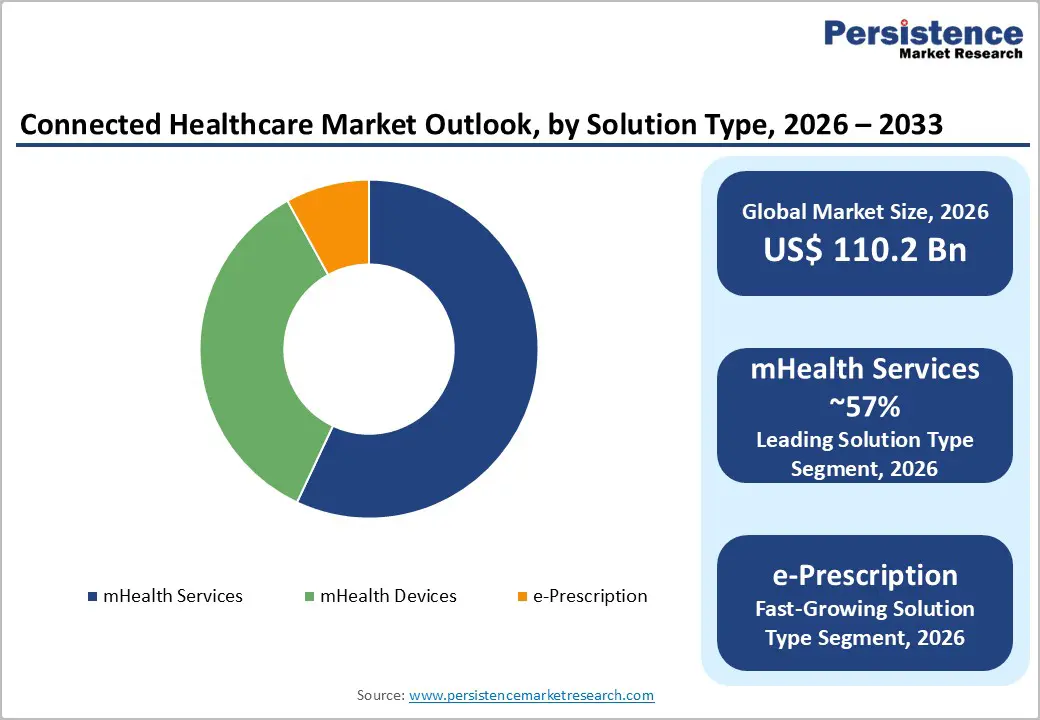

- The mHealth services segment is expected to dominate the market in 2025 driven by the rising use of smartphones and health apps.

- The growth of smartphones facilitates great access to healthcare services boosting the adoption of mHealth services.

- The wellness and prevention segment is projected to lead the market driven by the integration of health technology into social care.

| Key Insights | Details |

|---|---|

|

Connected Healthcare Market Size (2026E) |

US$ 110.2 Bn |

|

Market Value Forecast (2033F) |

US$ 385.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

19.6% |

|

Historical Market Growth (CAGR 2020 to 2024) |

16.2% |

Market Dynamics

Driver - Increasing Demand for Telehealth Services

The growing demand for telehealth services has been a major driver of the connected healthcare market. The COVID-19 pandemic accelerated the adoption of virtual consultations, enabling patients to access medical care without visiting hospitals or clinics. This shift improved convenience and allowed healthcare access for individuals in remote or underserved areas, bridging gaps in traditional healthcare delivery. Patients increasingly prefer remote consultations for routine check-ups, follow-ups, and chronic disease management, which has further fueled market growth.

Advancements in wearable technology have also significantly contributed to the expansion of connected healthcare. Devices such as smartwatches, fitness trackers, and medical-grade monitoring tools allow continuous tracking of vital signs and health metrics, empowering patients to manage their own health. These devices transmit real-time data to healthcare providers, enabling timely interventions and better management of chronic conditions. The ongoing evolution of wearables with features like ECG monitoring, oxygen saturation tracking, and sleep analysis enhances preventive healthcare measures. Together, telehealth adoption and wearable technology are creating a more proactive, patient-centered healthcare ecosystem, driving sustained demand for connected healthcare solutions globally.

Restraints - Data Privacy and Security Concerns

Data privacy and security concerns represent a key restraint limiting the growth of the connected healthcare market. As healthcare systems become increasingly interconnected, sensitive patient data is transmitted and stored digitally, creating heightened risks of breaches and unauthorized access. Patients and providers are often hesitant to share personal health information due to fears of identity theft, data misuse, or exposure of confidential medical records. Inadequate security measures or lack of standardized protocols can reduce trust in connected healthcare technologies, slowing adoption rates.

Regulatory challenges and compliance issues further constrain market growth. Healthcare technologies must adhere to strict regulations regarding patient data management, privacy, and integration with existing systems. Navigating these complex frameworks, which often vary across regions, can be time-consuming and costly for technology developers and healthcare providers. Delays in product deployment, additional compliance costs, and the need for continuous monitoring of regulatory changes add operational challenges. Together, concerns over data security and the complexities of regulatory compliance limit widespread adoption of connected healthcare solutions, particularly in regions with strict privacy laws or underdeveloped legal frameworks.

Opportunity - Integration of AI and ML

The integration of artificial intelligence (AI) and machine learning (ML) into connected healthcare solutions presents a significant growth opportunity. AI and ML technologies enable advanced data analytics, predictive insights, and personalized treatment plans, improving patient outcomes. By analyzing large volumes of health data, AI tools can identify trends, detect early signs of complications, and support proactive interventions. Applications such as automated diagnosis, predictive risk scoring, and personalized medicine are expanding rapidly, creating opportunities for healthcare providers and technology developers to deliver more efficient and precise care.

The rise of remote patient monitoring (RPM) solutions further strengthens market potential. With increasing prevalence of chronic diseases and an aging population, healthcare systems are adopting RPM tools to monitor patients outside traditional clinical settings. Wearable devices and mobile health applications provide continuous tracking of vital signs, enabling timely interventions and better management of long-term conditions. RPM reduces hospital visits, lowers healthcare costs, and improves patient engagement and compliance. As healthcare providers focus on preventive care and digital integration, the combination of AI-driven analytics and RPM technologies is expected to drive substantial growth in the connected healthcare market in the coming years.

Category-wise Analysis

By Solution Type Insights

The mHealth services segment is expected to dominate the connected healthcare market in 2024, driven by the widespread adoption of smartphones and mobile health applications. Mobile-based health solutions enable patients to access healthcare services conveniently from their homes, facilitating teleconsultations, appointment scheduling, medication reminders, and remote monitoring of vital signs. The convenience and accessibility offered by mHealth services are particularly appealing in regions with limited healthcare infrastructure or remote populations.

According to the State of Mobile Internet Connectivity Report 2020, approximately 3.8 billion people were using mobile internet by the end of 2019, an increase of 250 million users from 2018, demonstrating the rapid growth of mobile technology penetration. This proliferation of smartphones and internet connectivity supports the expansion of mHealth services globally. The integration of health apps with wearable devices further strengthens continuous health tracking and patient engagement. As digital health adoption rises, mHealth services are expected to remain the leading solution type, driving overall growth in the connected healthcare market.

By Application Insights

The global connected healthcare market is categorized into Diagnosis & Treatment, Monitoring Applications, Wellness & Prevention, Healthcare Management, and Others. These applications reflect the diverse ways in which digital health technologies are integrated into patient care, preventive health, and healthcare operations.

Among these, the Wellness & Prevention segment dominated the market in 2025 and is expected to emerge as the fastest-growing segment over the forecast period. This growth is driven by the increasing focus on preventive care, fitness tracking, and health management through digital platforms. Connected healthcare solutions are increasingly viewed as an essential part of wellness and social care, bridging the gap between healthcare providers and consumers. For instance, according to NCBI in October 2019, approximately 70% of mHealth applications were designed for the consumer wellness and fitness segment, promoting health awareness, activity tracking, and preventive interventions. The rising adoption of mobile apps and wearable devices, coupled with growing public interest in health and fitness, continues to fuel growth in this segment, positioning it as a key driver for the global connected healthcare market.

Regional Insights

North America Connected Healthcare Market Trends

North America continues to lead the global connected healthcare market, accounting for over 36% of total revenue share in 2025 due to strong healthcare infrastructure, high adoption of digital health technologies, and widespread use of remote patient monitoring solutions. The integration of connected care services such as telehealth, wearable devices, and real-time monitoring has helped providers manage patient care more efficiently and reduce overall healthcare costs. Remote Patient Monitoring (RPM) remains a key focus, with millions of users across the U.S. and Canada leveraging connected solutions for chronic disease management and post-acute care. The region’s mature healthcare ecosystem, coupled with supportive reimbursement frameworks and continuous investments in digital health, reinforces its dominance in the market.

Patient preference for convenient, personalized care delivered outside traditional clinical settings has further fueled demand for connected healthcare technologies. As telehealth and virtual consultations become standard care components, healthcare providers are intensifying digital transformation initiatives to enhance care accessibility, optimize clinical workflows, and improve patient outcomes across diverse settings.

Europe Connected Healthcare Market Trends

Europe holds the second-largest position in the global connected healthcare market, supported by increasing smartphone adoption, rising acceptance of remote patient monitoring services, and strong digital health initiatives across major economies. Countries like Germany and France are advancing their digital health infrastructure, with Germany’s Digital Healthcare Act (DiGA) enabling physicians to prescribe certified digital health applications reimbursed through statutory insurance. This framework has expanded access to digital monitoring tools and has driven broader adoption of connected healthcare solutions.

In addition to regulatory support, European healthcare systems are increasingly focusing on preventive care and chronic disease management through remote monitoring and telehealth services. National reimbursement programs and digital health coverage are facilitating integration of digital tools into standard care pathways, enhancing care continuity and patient engagement. Countries like Belgium have also introduced reimbursement codes for mobile health solutions, signaling stronger institutional backing for connected care technologies. This regulatory momentum, combined with a digitally adept population and expanding healthcare IT infrastructure, is expected to drive sustained growth and adoption of connected healthcare solutions across Europe.

Asia Pacific Connected Healthcare Market Trends

The Asia Pacific connected healthcare market is rapidly expanding, driven by rising healthcare investments, increasing internet penetration, and growing demand for remote patient monitoring and mobile health services. Emerging economies such as China and India are witnessing significant uptake of connected healthcare technologies as healthcare providers strive to bridge care gaps in both urban and rural regions. Technological advancements in wearable devices, telehealth platforms, and health management applications are enabling more patients to access care conveniently and consistently.

Several countries in the region are incorporating digital health initiatives into national healthcare strategies, promoting remote monitoring and telehealth as part of broader efforts to strengthen healthcare delivery. Government policies supporting digital infrastructure and healthcare digitization, along with increased awareness about preventive and personalized care, are fostering greater adoption of connected healthcare solutions. As chronic disease prevalence rises and healthcare systems modernize, the Asia Pacific market is expected to capture significant growth, emerging as one of the fastest-growing regional markets globally for connected healthcare technologies.

Competitive Landscape

The connected healthcare market is characterized by intense competition among key players innovating to enhance patient care. For instance, Philips has launched several innovative products since 2022 including the Philips HealthSuite, a cloud-based platform that integrates data from various health devices to provide personalized health insights. These advancements reflect a broader trend of leveraging technology to improve patient outcomes and streamline healthcare delivery. Consequently, positioning these companies as leaders in the evolving connected healthcare landscape.

Key Industry Developments:

- August 2024, Aster DM Healthcare Limited launched Tele-ICU services under the Aster Connected Care arm in India, leveraging technology to provide comprehensive support to healthcare providers to enhance patient care. The services include expert intensive availability, continuous monitoring of ICUs by qualified staff, 24/7 audio-visual communication, and rapid response alerts.

- May 2024, SpaceX launched a satellite internet service called Starlink for Indonesia's health sector in Bali providing millions of internet access to three health centers. Starlink, SpaceX's project to create a global network of satellites, aims to bridge the digital divide in remote and underserved areas. The service enables telemedicine services, remote patient monitoring, and access to online medical resources, improving healthcare in remote areas.

Companies Covered in Connected Healthcare Market

- Agamatrix

- AirStrip Technologies

- AliveCor Inc

- Allscripts

- Apple Inc.

- Athenahealth

- Boston Scientific Corporation

- Cerner

- GE Healthcare

- Honeywell Life Care Solutions

- Medtronics

- Others

Frequently Asked Questions

The global connected healthcare market is projected to be valued at US$ 110.2 Bn in 2026.

Rising chronic diseases, growing smartphone adoption, digital health awareness, telemedicine expansion, and demand for remote patient monitoring.

The global market is expected to witness a CAGR of 19.6% between 2026 and 2033.

Integration of AI, IoT, wearable devices, and personalized healthcare services in emerging markets with expanding digital infrastructure.

North America is the leading region in the global connected healthcare market.