- Healthcare Services

- Home Healthcare Market

Home Healthcare Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Home Healthcare Market by Product (Therapeutic Devices, Testing, Screening and Monitoring Devices, Mobility Care Devices, Others), Service (Skilled Nursing Services, Rehabilitation Therapy Services, Respiratory Therapy Services, Infusion Therapy Services, Pregnancy Care Services, and Others), Indication (Oncology, Respiratory Diseases, Mobility Disorders, Cardiovascular Diseases, Diabetes, and Others), and Regional Analysis from 2026 to 2033

Home Healthcare Market Share and Trends Analysis

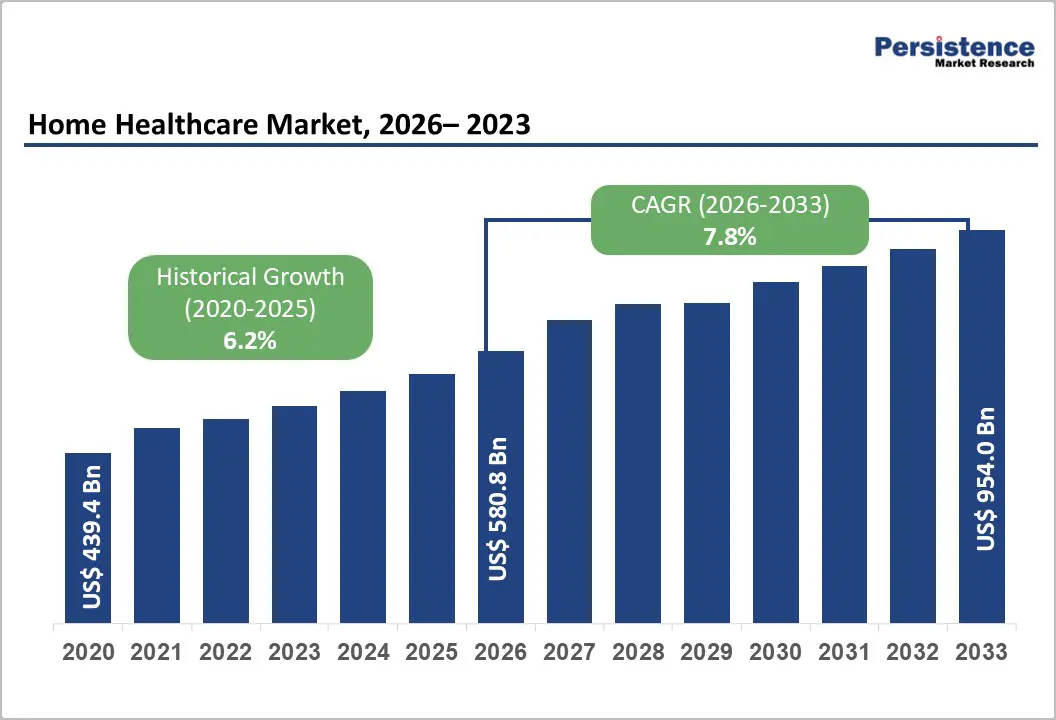

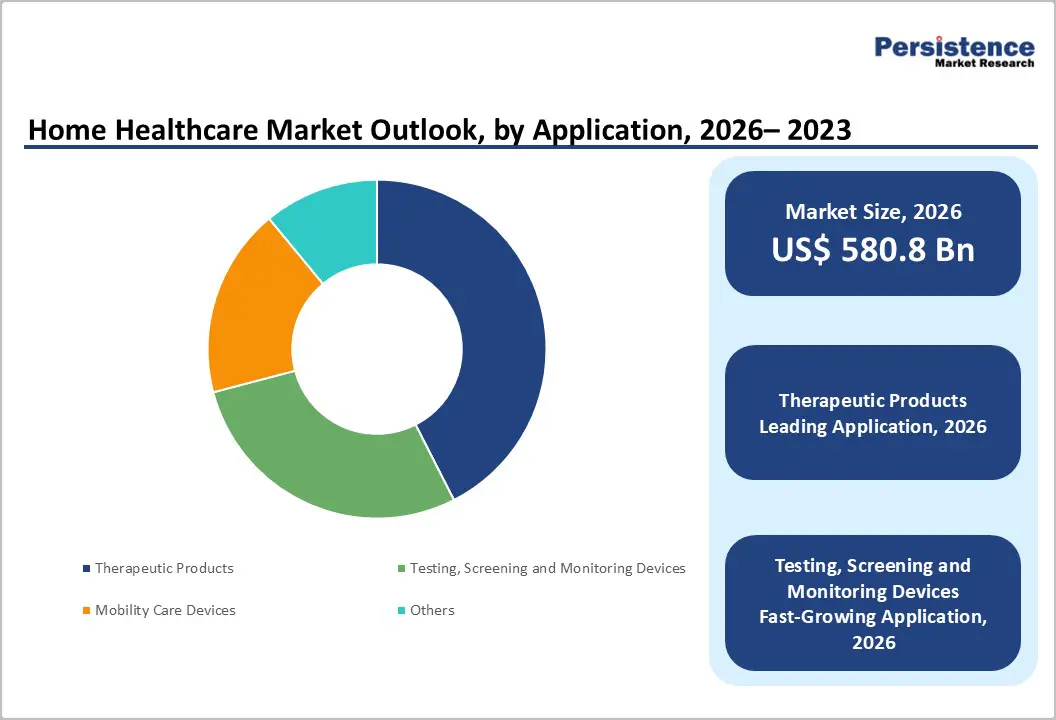

The global home healthcare market size is estimated to grow from US$ 580.8 billion in 2026 to US$ 954.0 billion by 2033. The market is projected to record a CAGR of 7.8% during the forecast period from 2026 to 2033.

Global demand for home healthcare solutions is rising steadily, driven by the growing aging population, increasing prevalence of chronic diseases, and a strong shift toward patient-centric, cost-effective care delivered outside traditional hospital settings. The rising incidence of diabetes, cardiovascular diseases, respiratory disorders, and mobility impairments has significantly increased demand for therapeutic devices, remote monitoring systems, and skilled home-based services. Expansion of home healthcare providers, improved access to medical devices, and higher healthcare spending are accelerating market growth.

Continuous innovation in connected medical devices, telehealth platforms, and remote patient monitoring technologies is enhancing care quality, treatment adherence, and clinical outcomes. Additionally, increasing focus on reducing hospital stays and readmission rates, wider acceptance of digital health solutions, and growing preference for personalized care in home settings are further propelling market expansion.

Key Industry Highlights:

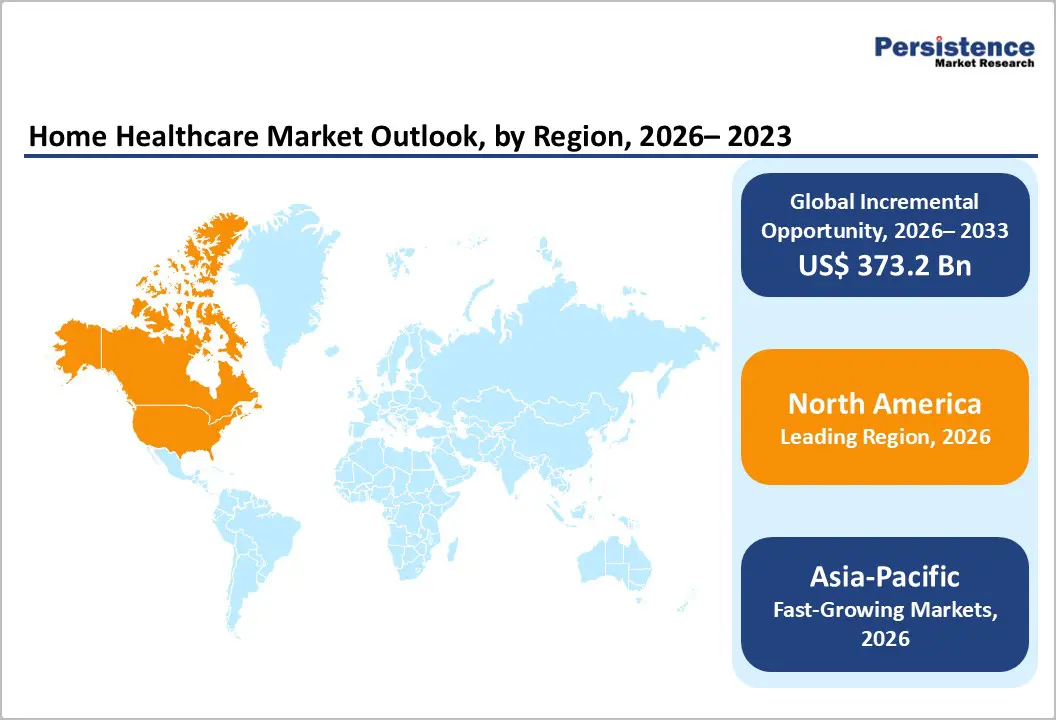

- Leading Region: North America holds the largest share at 48.8%, supported by advanced healthcare infrastructure, high healthcare expenditure, strong reimbursement frameworks, early adoption of home-based care models, and widespread use of digital health technologies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a rapidly aging population, rising prevalence of chronic diseases, improving healthcare access, expanding private healthcare providers, and increasing government support for home-based care.

- Leading Product Segment: Therapeutic devices dominate the market due to their extensive use in chronic disease management, post-acute care, and long-term therapy within home settings.

- Fastest-Growing Product Segment: Testing, screening, and monitoring devices are growing rapidly as adoption of remote patient monitoring and connected diagnostics accelerates.

- Leading Application Segment: Diabetes remains the leading indication due to high reliance on home-based glucose monitoring, insulin delivery, and long-term disease management.

- Fastest-Growing Application Segment: Mobility disorders are expanding quickly as aging populations drive demand for rehabilitation, assistive devices, and continuous home care support.

| Key Insights | Details |

|---|---|

| Home Healthcare Market Size (2026E) | US$ 580.8 Bn |

| Market Value Forecast (2033F) | US$ 954.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Dynamics

Driver - Rising Prevalence of Chronic Diseases, Aging Population, and Shift toward Home-Based Care Driving Market Growth

The home healthcare market is experiencing strong growth momentum driven by the rising global prevalence of chronic diseases and the rapidly aging population. Conditions such as diabetes, cardiovascular diseases, respiratory disorders, cancer, and mobility impairments require long-term monitoring, ongoing therapy, and post-acute care, making home-based healthcare a preferred alternative to hospital-centric treatment. Increasing life expectancy, particularly in developed economies, is expanding the pool of elderly patients who require continuous medical support, skilled nursing, and rehabilitation services at home.

Additionally, healthcare systems worldwide are under pressure to reduce costs and hospital overcrowding. Home healthcare offers a cost-effective care model by lowering inpatient admissions, shortening hospital stays, and minimizing readmission rates. Advancements in medical devices, such as portable therapeutic equipment, remote patient monitoring systems, and connected diagnostic tools, are improving the safety, effectiveness, and scalability of home-based care. Growing acceptance of telehealth and digital health platforms further supports clinical decision-making and patient engagement.

Favorable reimbursement policies and government initiatives promoting value-based and patient-centered care are also accelerating adoption. Together, these demographic, economic, and technological factors are acting as key drivers fueling sustained growth in the global home healthcare market.

Restraints - Workforce Shortages, Reimbursement Challenges, and Operational Complexity Limiting Market Expansion

The home healthcare market faces several structural and operational restraints. One of the primary challenges is the global shortage of skilled healthcare professionals, including nurses, therapists, and trained caregivers. Delivering high-quality home healthcare requires specialized clinical expertise, particularly for complex cases involving wound care, infusion therapy, and chronic disease management. Workforce constraints can limit service availability, increase labor costs, and affect care consistency, especially in rural and underserved regions.

Reimbursement complexity also remains a significant barrier. Variability in coverage policies across regions and payers creates uncertainty around service pricing and profitability.

Moreover, reimbursement rates for home healthcare services and devices remain insufficient to fully cover operational costs, discouraging providers from expanding service offerings. Additionally, administrative burdens related to documentation, compliance, and billing add to operational inefficiencies. Operational challenges such as care coordination, logistics, and quality control further constrain market scalability. Managing multiple patients across dispersed home settings increases complexity compared to centralized hospital care.

Ensuring data security, device interoperability, and consistent clinical outcomes remains critical. These workforce, financial, and operational challenges collectively slow adoption and limit the pace of expansion in the home healthcare market.

Opportunity - Digital Health Integration, Expansion in Emerging Markets, and Growth of Advanced Home-Based Therapies

The home healthcare market presents significant growth opportunities driven by rapid digital health integration and expanding demand for advanced home-based therapies. Increasing adoption of remote patient monitoring, wearable devices, telehealth platforms, and AI-enabled care coordination tools is transforming how care is delivered at home. These technologies improve real-time monitoring, enable early intervention, and enhance clinical outcomes while reducing the burden on healthcare professionals. Integration of data analytics and automation is also improving workflow efficiency and personalized care planning.

Emerging markets represent another major opportunity area. Countries in Asia Pacific, Latin America, and parts of the Middle East are witnessing rising healthcare investments, expanding middle-class populations, and growing awareness of home-based care solutions. Governments in these regions are increasingly promoting home healthcare to reduce pressure on hospitals and improve access to care in remote areas. Additionally, growth of advanced home-based therapies such as infusion therapy, respiratory care, post-surgical rehabilitation, and chronic disease management is expanding the market scope.

Increasing availability of portable, user-friendly medical devices is enabling more complex treatments to be safely administered at home. These trends collectively create strong long-term growth opportunities for home healthcare providers, device manufacturers, and digital health platforms.

Category-wise Analysis

By Product, Therapeutic Devices Lead the Global Home Healthcare Market Due to High Chronic Care Demand

The therapeutic devices segment is projected to dominate the global home healthcare market in 2026, accounting for a revenue share of 42.5%. Segment leadership is driven by widespread use of therapeutic equipment such as infusion pumps, insulin delivery devices, respiratory therapy devices, and home dialysis systems for long-term disease management. These devices play a critical role in managing chronic conditions, post-acute care, and rehabilitation, enabling patients to receive continuous treatment outside hospital settings. Their increasing compatibility with digital health platforms, remote monitoring systems, and automated drug delivery enhances clinical outcomes and patient adherence.

Technological advancements focused on device miniaturization, portability, and connectivity are further improving usability in home environments. Rising prevalence of diabetes, cardiovascular diseases, respiratory disorders, and cancer continues to expand demand. Cost advantages compared to inpatient care and growing preference for home-based treatment models further reinforce the dominance of therapeutic devices in the global home healthcare market.

By Service, Skilled Nursing Services Dominate Driven by Complex Home-Based Clinical Care

The skilled nursing services segment is projected to dominate the global home healthcare market in 2026, accounting for a revenue share of 35.0%. This leadership is primarily driven by rising demand for professional medical care at home, including wound care, medication administration, post-surgical recovery, chronic disease management, and palliative support. Increasing hospital discharge rates and emphasis on reducing inpatient stays are accelerating reliance on skilled nursing services in home settings.

The growing elderly population and higher incidence of mobility limitations and comorbidities further support demand. Skilled nurses play a critical role in monitoring patient conditions, coordinating care plans, and ensuring adherence to prescribed therapies. Integration of digital health tools, electronic health records, and remote patient monitoring is enhancing service efficiency and care quality. Expanding reimbursement coverage and favorable healthcare policies supporting home-based nursing care continue to drive sustained growth of this segment.

By Indication, Diabetes Emerges as the Leading Indication Due to High Home Monitoring Adoption

The diabetes segment is projected to dominate the global home healthcare market in 2026, accounting for a revenue share of 31.4%. This dominance reflects the high global prevalence of diabetes and the strong reliance on home-based monitoring and therapeutic solutions such as glucose monitors, insulin pumps, and continuous glucose monitoring systems. Diabetes management requires frequent testing, medication administration, and lifestyle monitoring, making home healthcare a preferred and cost-effective care setting. Increasing adoption of connected devices and digital diabetes management platforms is improving disease control and patient engagement.

Growing awareness, early diagnosis, and long-term disease management needs further support segment leadership. Healthcare providers and payers are increasingly promoting home-based diabetes care to reduce hospital burden and improve outcomes. Continuous innovation in wearable monitoring devices and smart insulin delivery systems continues to reinforce diabetes as the leading indication in the global home healthcare market.

Regional Insights

North America Home Healthcare Market Trends

The North America home healthcare market is expected to dominate globally with a value share of 48.8% in 2026, led by the United States due to its advanced healthcare infrastructure, high healthcare spending, and early adoption of home-based care models. The region benefits from widespread availability of skilled nursing services, advanced medical devices, and digital health technologies that support remote monitoring and chronic disease management. A rapidly aging population and high prevalence of diabetes, cardiovascular diseases, and respiratory disorders are significantly increasing demand for home healthcare services.

Favorable reimbursement frameworks under Medicare and private insurers continue to encourage home-based treatment over institutional care. Strong presence of leading market players, continuous product innovation, and integration of telehealth platforms further enhance care delivery efficiency. Additionally, rising patient preference for comfort, convenience, and personalized care at home is accelerating market penetration. Government initiatives focused on value-based care and cost reduction continue to reinforce North America’s dominant position.

Europe Home Healthcare Market Trends

The Europe home healthcare market is expected to grow steadily, supported by an aging population, rising chronic disease burden, and increasing emphasis on decentralized care delivery. Countries such as Germany, the U.K., France, Italy, and the Nordic region are key contributors due to well-developed healthcare systems and expanding home care infrastructure. European healthcare providers are increasingly shifting care from hospitals to home settings to reduce costs and improve patient outcomes. Growth is supported by expanding availability of home nursing services, rehabilitation therapies, and remote monitoring devices.

Regulatory support for home-based medical devices and standardized care pathways across the region is further facilitating adoption. Public healthcare systems are increasingly integrating home healthcare into long-term care strategies for elderly and chronically ill patients. Additionally, growing investment in digital health solutions and cross-border collaboration among healthcare providers and technology companies is strengthening market expansion across Europe.

Asia Pacific Home Healthcare Market Trends

The Asia Pacific home healthcare market is expected to register a relatively higher CAGR of around 10.6% between 2026 and 2033, driven by rapid demographic shifts, rising healthcare expenditure, and expanding access to home-based medical services. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are witnessing growing demand due to increasing elderly populations and rising prevalence of chronic diseases. Improving healthcare infrastructure and growing adoption of affordable home medical devices are accelerating market growth. Governments across the region are promoting home healthcare to ease pressure on overcrowded hospitals and reduce healthcare costs.

Expansion of private healthcare providers, increasing penetration of telehealth platforms, and growing awareness of home-based care benefits are further supporting adoption. Local manufacturing, strategic partnerships with global players, and rapid digitalization of healthcare services are improving accessibility and affordability, positioning Asia Pacific as the fastest-growing regional market.

Market Competitive Landscape

The global home healthcare market is highly competitive, with strong participation from Omron Healthcare, Inc., F. Hoffmann-La Roche AG, Koninklijke Philips N.V., Johnson & Johnson, and Abbott. These companies leverage broad global distribution networks, diversified home healthcare product portfolios, and continuous innovation in medical devices, diagnostics, remote monitoring, and connected care solutions to strengthen their market positions.

Key players are increasingly focused on digital health integration, remote patient monitoring platforms, and scalable home-based care technologies to support chronic disease management, diagnostics, and preventive care. Strategic priorities include portfolio expansion, technology integration, cost optimization, and strengthening partnerships with healthcare providers and payers to accelerate adoption and commercialization across home care settings.

Key Industry Developments:

- In January 2026, Dr Odin announced the launch of a new range of smart, app-connected health monitoring devices that enable users to track key health vitals from home using their smartphones, including a digital thermometer, infrared thermometer, pulse oximeter, upper-arm blood pressure monitor, and a foetal doppler, all designed to seamlessly integrate with the Dr Odin Health App to support remote health monitoring and data-driven care management.

- In November 2025, Lords Mark India acquired an 85% stake in Renalyx Health Systems, significantly strengthening its footprint in renal diagnostics and medical technology innovation. The acquisition is expected to enhance the company’s capabilities in advanced diagnostic solutions, expand its medtech portfolio, and support broader adoption of home-based and decentralized renal care technologies across India.

- In July 2025, Abhay HealthTech announced the expansion of its product portfolio to align with India’s transition toward consumer-driven and preventive healthcare, adding rapid diagnostic kits, hygiene products, wellness solutions, and telehealth services to address the rising demand for home-based medical care.

- In May 2024, LG Electronics (LG) unveiled Primefocus Health, a new venture designed to leverage innovative technologies and emerging healthcare therapies to help providers deliver personalized, end-to-end care while empowering individuals to actively manage their health at home. Primefocus Health represents the first new venture launched by LG NOVA, the LG Electronics North America Innovation Center.

Companies Covered in Home Healthcare Market

- Omron Healthcare, Inc.

- F. Hoffmann-La Roche AG

- Koninklijke Philips N.V.

- Johnson & Johnson

- Abbott

- Sunrise Medical

- Medtronic PLC

- Cardinal Health Inc.

- Air Liquide

- Amedisys, Inc.

- Arkray, Inc.

- Drive DeVilbiss Healthcare

- GE HealthCare

- Medline Industries, Inc

- Others

Frequently Asked Questions

The global home healthcare market is projected to be valued at US$ 580.8 Bn in 2026.

Rising aging population and growing burden of chronic diseases are increasing demand for long-term, cost-effective care at home. Additionally, the rapid adoption of telehealth, remote patient monitoring, and favorable reimbursement policies is accelerating home-based care delivery.

The global home healthcare market is poised to witness a CAGR of 7.8% between 2026 and 2033.

Expansion of digital health, IoT-enabled monitoring, and AI-driven care coordination creates strong growth potential. Additionally, rising penetration in emerging markets and scaling of home-based infusion, rehabilitation, and post-acute care services present significant opportunities.

Omron Healthcare, Inc., F. Hoffmann-La Roche AG, Koninklijke Philips N.V., Johnson & Johnson, and Abbott are some of the key players in the home healthcare market.