- Medical Devices

- OTC Consumer Healthcare Market

OTC Consumer Healthcare Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

OTC Consumer Healthcare Market by Product Type (Dermatological Products, Vitamins & Dietary Supplements, Gastrointestinal Products, OphthalmologyProducts, Wound Care Management Products, Others), Form (Solid oral, Liquids, Semi-solid & Topical, Others), Distribution Channel (Retail Pharmacies, Online Pharmacies, Others), and Regional Analysis from 2025 - 2032

OTC Consumer Healthcare Market Share and Trends Analysis

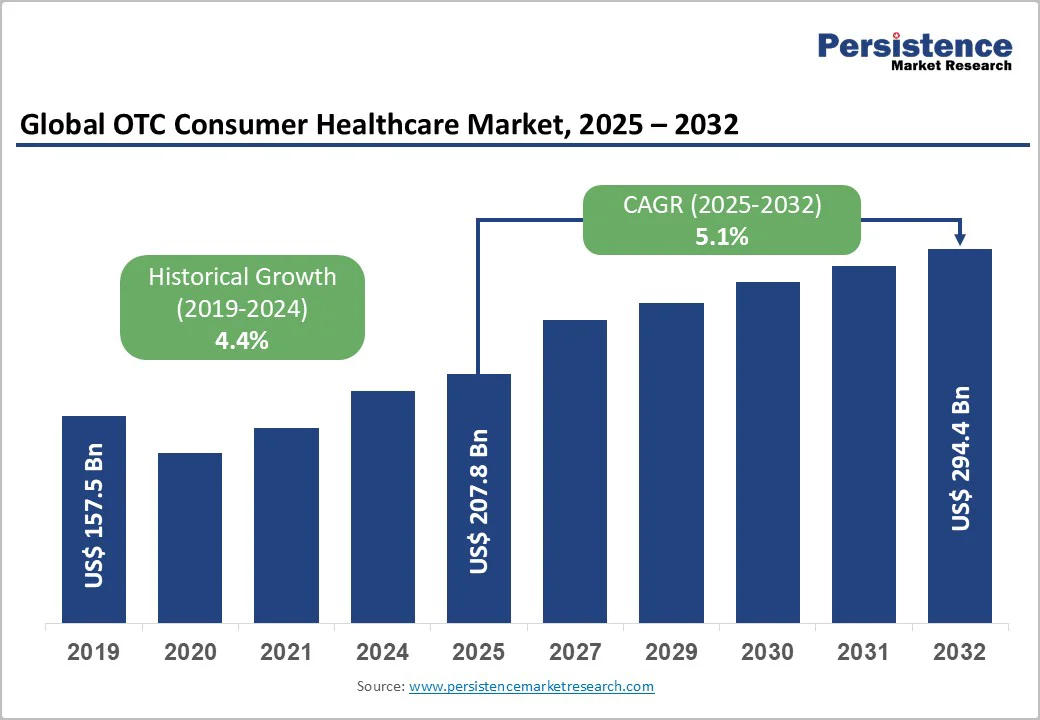

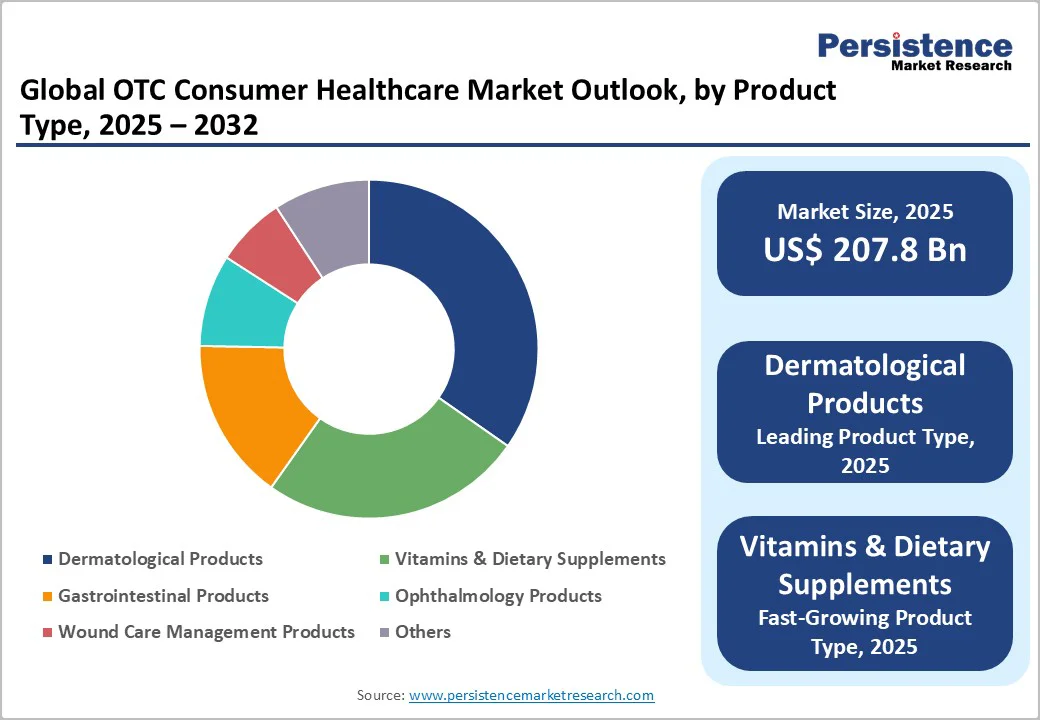

The global OTC consumer healthcare market size is valued at US$207.8 billion in 2025 and is projected to reach US$294.4 billion at a CAGR of 5.1% during the forecast period from 2025 to 2032.

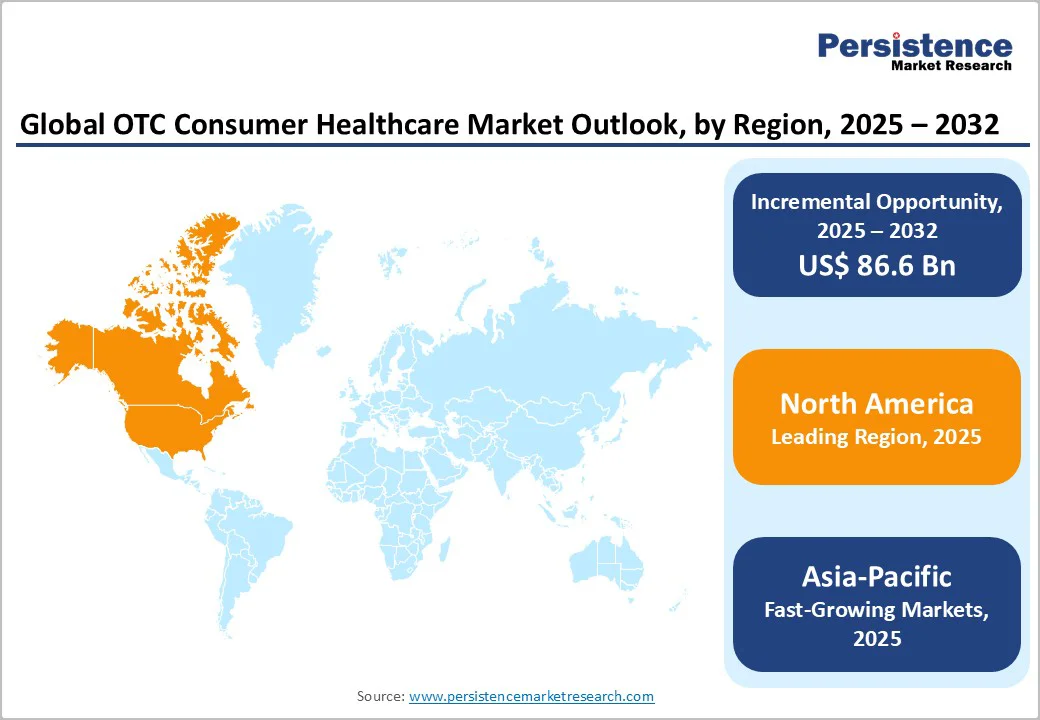

The global OTC consumer healthcare industry is expanding steadily, driven by rising self-medication trends, preventive health awareness, and the growing demand for vitamins, supplements, and skincare products. North America leads due to its strong retail infrastructure, while Asia-Pacific is the fastest-growing region, supported by rising healthcare expenditure and digital pharmacy adoption.

Key Industry Highlights

- Dominant Product Type: Dermatological Products hold about 34.7% share of the OTC Consumer Healthcare Market, driven by rising demand for skincare solutions such as anti-acne creams, antifungal ointments, and wound-healing products. Growing consumer focus on personal care, preventive skincare, and easy access to topical treatments further supports market dominance.

- Dominant From: Solid oral account for around 42.5% share, supported by high consumer preference for tablets, capsules, and chewabless due to ease of intake, convenience, and longer shelf life.

- Dominant Region: North America, contributing roughly 39.7% of global revenue, leads the market owing to strong retail networks, favorable regulatory systems, high healthcare spending, and established brand loyalty for major OTC categories.

- Investment Plans: Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes, digital pharmacy expansion, increasing self-medication culture, and growing investments from multinational and regional OTC manufacturers in new product launches and marketing.

- Market Drivers: Increasing health consciousness, demand for preventive wellness products, easy availability of OTC medicines, growing aging population, and expanding e-commerce distribution channels.

- Market Opportunity: Development of natural and personalized OTC products, innovation in delivery forms (gummies, effervescents), strategic collaborations between pharma and retail brands, and expansion into emerging markets with improving healthcare infrastructure and consumer affordability.

| Key Insights | Details |

|---|---|

|

Global OTC Consumer Healthcare Market Size (2025E) |

US$ 207.8 Bn |

|

Market Value Forecast (2032F) |

US$ 294.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.4% |

Market Dynamics

Driver - Growth of Preventive Healthcare and Wellness Products

The growing focus on preventive healthcare and wellness has become a major driver of the OTC Consumer Healthcare Market. Governments and consumers worldwide are shifting from treatment-based models to proactive health management. According to the U.S. National Institutes of Health, the share of adults using dietary supplements increased from 51.8% in 2011–2012 to 61.4% in 2021–2023, reflecting a strong preference for self-care and immunity-boosting products. Similarly, Eurostat data show that preventive healthcare spending in the European Union rose to 5.5% of total healthcare expenditure in 2022, up from 2.9% in 2019. This surge is supported by growing awareness of chronic disease prevention, rising disposable incomes, and easy access to OTC products through pharmacies and e-commerce. Consumers increasingly seek vitamins, minerals, herbal products, and skincare solutions for daily well-being, fueling steady market expansion and encouraging pharmaceutical companies to diversify OTC portfolios with wellness-oriented formulations.

Restraints - Risk of Misuse and Incorrect Self-Medication

Misuse and incorrect self-medication of OTC products are a growing restraint on the global OTC consumer healthcare market. According to the U.S. Food and Drug Administration (FDA), nearly 53% of adults are unaware of the potential risks associated with OTC medicines, and about 24% admit exceeding recommended dosages. A 2021 systematic review in the Journal of Pharmaceutical Policy and Practice reported that 16.2% of adults misuse OTC drugs, with 7.2% showing dependency symptoms. Older adults are particularly vulnerable; recent research found that 95% of individuals aged 65 and above exhibited at least one form of OTC misuse when purchasing sleep or pain medications.

Such practices lead to side effects, drug interactions, and delayed professional treatment. This rising trend of unsupervised self-medication undermines patient safety and limits the credibility of OTC healthcare products, ultimately posing a challenge to sustainable market expansion.

Opportunity - Rising Demand for Natural and Herbal Products

The rising demand for natural and herbal products presents a substantial opportunity in the OTC consumer healthcare market. In the U.S., a nationally representative survey found that more than one-third (≈ 35 %) of adults reported using botanical dietary supplements. Globally, the World Health Organization estimates that around 80% of the world’s population relies on traditional and herbal medicines.

In Europe, about 52% of consumers take supplements to maintain overall health, and the distribution of OTC and herbal drugs is expanding rapidly. These data show that consumers increasingly view natural, plant-based products as key to preventive health and self-care. For OTC market players, this means that herbal/topical formulations and wellness-oriented products are “low-hanging fruit” for expansion, especially as consumers shift from treatment into proactive wellness.

Category-wise Analysis

By Product Type, Dermatological Products Dominates the OTC Consumer Healthcare Market

The dermatological products dominates the market with 34.7% share in 2025, due to the high global prevalence of skin conditions and rising focus on personal care. According to the World Health Organization (WHO), skin diseases affect more than 900 million people globally, making them one of the most common health issues. The American Academy of Dermatology (AAD) reports that up to 85% of individuals aged 12–24 experience acne, driving strong demand for OTC creams, ointments, and cleansers. Similarly, eczema and dermatitis are increasingly treated through non-prescription topical agents. The growing trend of self-treatment, availability of pharmacist-guided skincare products, and increasing consumer awareness about hygiene and cosmetic appearance further contribute to the dominance of dermatological OTC products worldwide.

By Form, Solid Oral is gaining traction due to convenience, stability, low cost, and patient familiarity.

Solid oral dosage forms (tablets and capsules) lead the OTC consumer healthcare market primarily because they offer convenience, dosing accuracy, and broad consumer acceptance. According to a review of U.S. FDA-approved immediate-release oral drug products, approximately 82.5% of those are solid dosage forms, underscoring their dominance in oral administration.

Tablets alone account for around 64.5% of immediate-release oral forms. Their manufacturing efficiencies support low cost, long shelf life, and ease of logistics. Moreover, because consumers are familiar with tablets and capsules, self-medication becomes simpler, enhancing OTC uptake. These factors combined make solid oral formulations the preferred dosage form in the OTC segment.

Regional Insights

North America OTC Consumer Healthcare Market Trends

North America dominates the OTC consumer healthcare market with 39.7% share in 2025, due to its strong self-care culture, high accessibility of OTC products, and significant cost-savings recognized by the health system. For example, U.S. households spend on average around US $645 annually on OTC products. Moreover, data show that for every US$1 spent on OTC medicines, the U.S. healthcare system saves approximately US$7.33, contributing an estimated US$167 billion in annual savings. Retail accessibility is also extensive: there are over 750,000 retail outlets in the U.S. that sell OTC products. These factors, including high consumer spending, recognized value, and vast distribution infrastructure, together explain why North America dominates the global OTC consumer healthcare market.

Europe OTC Consumer Healthcare Market Trends

Europe is one of the leading regions in the OTC consumer healthcare market because it benefits from a well-established self-care culture, strong regulatory support for non-prescription access, and high consumer health awareness. According to the Association of the European Self-Care Industry (AESGP), Europeans purchased over 9.7 billion packs of non-prescription medicines and around 1 billion packs of vitamins/minerals in one year.

Also, more than 200 distinct active pharmaceutical ingredients in OTC status are available across more than 4,000 products in Europe. Beyond that, the region’s high internet and smartphone penetration enables growing e-pharmacy uptake for OTC products, further enhancing access. These factors together sustain Europe’s leadership in the OTC segment by aligning consumer demand, regulatory environment, and distribution channels.

Asia-Pacific OTC Consumer Healthcare Market Trends

The Asia-Pacific region is the fastest-growing market for OTC consumer healthcare, thanks to multiple favorable dynamics. Rising urbanization and disposable incomes mean more consumers can afford self-care products. For instance, the World Health Organization (WHO) notes that non-communicable diseases account for ~71 % of deaths in the region, driving demand for accessible OTC treatments.

According to regional retail pharmacy data, India’s pharmacy count grew from ~800,000 in 2020 to ~850,000 in 2022, enhancing OTC access. Government policies and large populations also help in China, the national regulator reported thousands of OTC licences in 2022, expanding consumer options. Together, these factors, including large, underserved populations, improving infrastructure, growing internet penetration and self-care awareness, create strong momentum for OTC healthcare growth in Asia-Pacific.

Competitive Landscape

Leading companies in the OTC consumer healthcare market are focusing on product innovation, consumer trust, and global expansion. They are introducing natural and science-backed formulations, investing in digital wellness platforms, and forming retail and e-commerce partnerships. These strategies aim to improve accessibility, enhance self-care awareness, and meet the growing demand for preventive and personalized healthcare solutions.

Key Industry Developments:

- In July 2025, Lupin Limited announced that it had spun off its Consumer Healthcare business into a wholly owned subsidiary to streamline operations and enhance focus on growth segments. The move was aimed at strengthening Lupin’s presence in the OTC space, enabling independent management, faster decision-making, and improved alignment with evolving consumer health trends.

- In March 2025, Leading pharmaceutical companies capitalized on the growing demand for over-the-counter (OTC) drugs to diversify their revenue sources. Firms expanded their OTC portfolios to include vitamins, pain relief, and digestive health products amid increasing consumer preference for self-care solutions. This strategic shift helped reduce dependence on prescription medicines while tapping into the rapidly growing consumer healthcare segment.

Companies Covered in OTC Consumer Healthcare Market

- Sun Pharmaceutical Industries Limited

- Glenmark Pharmaceuticals Ltd.

- Johnson & Johnson Private Ltd, Pfizer, Inc.

- American Health Corporation

- Abbott Laboratories Inc.

- GlaxoSmithKline plc

- Sanofi S.A.

- Piramal Enterprises Ltd.

- Boehringer Ingelheim GmbH

- Bayer AG

- Teva Pharmaceutical Industries Ltd.

- Ipsen SA, BASF SE

- Koninklijke DSM N.V.

- Reckitt Benckiser LLC.

- Lonza Group Ltd.

- Others

Frequently Asked Questions

The global OTC consumer healthcare market is projected to be valued at US$ 207.8 Bn in 2025.

Growing self-care awareness, aging population, easy product accessibility, digital retail expansion, and rising demand for natural and preventive healthcare solutions.

The global OTC consumer healthcare market is poised to witness a CAGR of 5.1% between 2025 and 2032.

Expansion in e-pharmacies, herbal formulations, personalized nutrition, pediatric OTC care, and strategic collaborations for innovative self-care product development.

Glenmark Pharmaceuticals Ltd., Johnson & Johnson Private Ltd, Pfizer, Inc., American Health Corporation, Abbott Laboratories Inc., GlaxoSmithKline plc, Sanofi S.A.