- Healthcare Services

- Europe Modular Construction for Healthcare Market

Europe Modular Construction for Healthcare Market Size, Share and Growth Forecast, 2026 - 2033

Europe Modular Construction for Healthcare Market by Product Type (Permanent, Relocatable), Application (Surgery Rooms and Theaters, Laboratories, Emergency Rooms, Others), and Country Analysis for 2026 - 2033

Europe Modular Construction for Healthcare Market Size and Trends Analysis

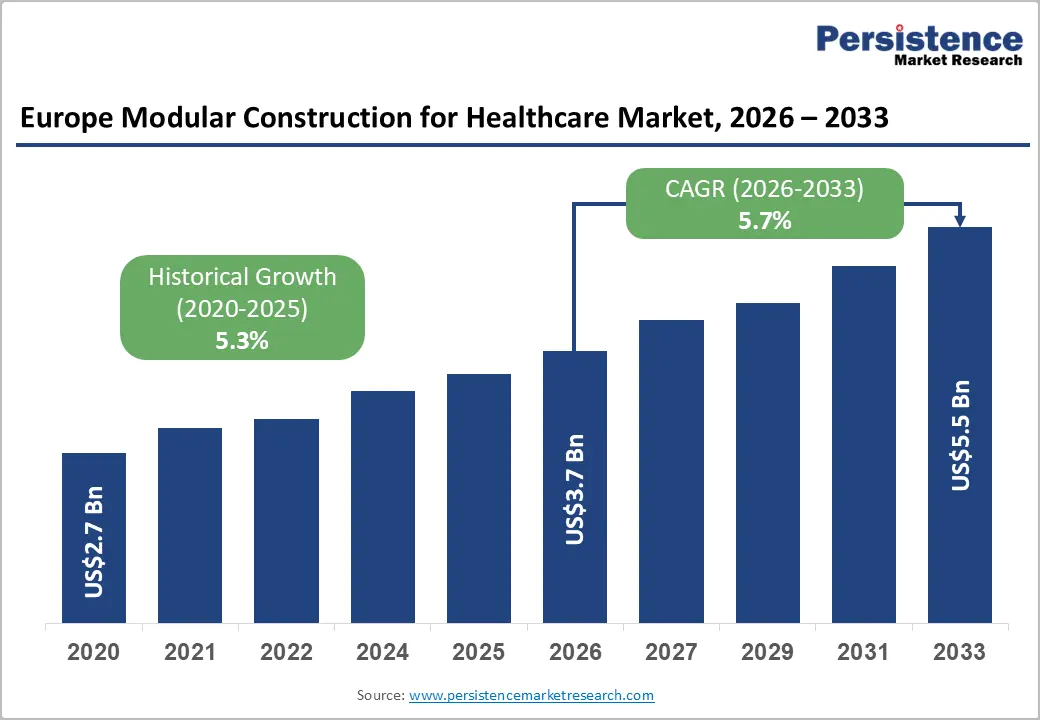

The Europe modular construction for healthcare market size is likely to be valued at US$3.7 billion in 2026 and is projected to reach US$5.5 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033, driven by the rising demand for rapid hospital infrastructure deployment, particularly in post-pandemic healthcare system upgrades across Europe.

Increasing adoption of modular healthcare construction solutions is supported by government investments in healthcare resilience and capacity expansion. Growth is also driven by cost efficiency compared to traditional construction methods and reduced project delivery timelines. Additionally, hospital modernization programs across Germany, the U.K., and France are reinforcing demand for flexible and scalable healthcare infrastructure solutions.

Key Industry Highlights:

- Dominant Construction Type: Permanent modular construction is expected to lead with a 58% share in 2026, while relocatable systems will be the fastest growing at 6.5% CAGR through 2033, driven by demand for rapid hospital deployment and flexible emergency healthcare capacity.

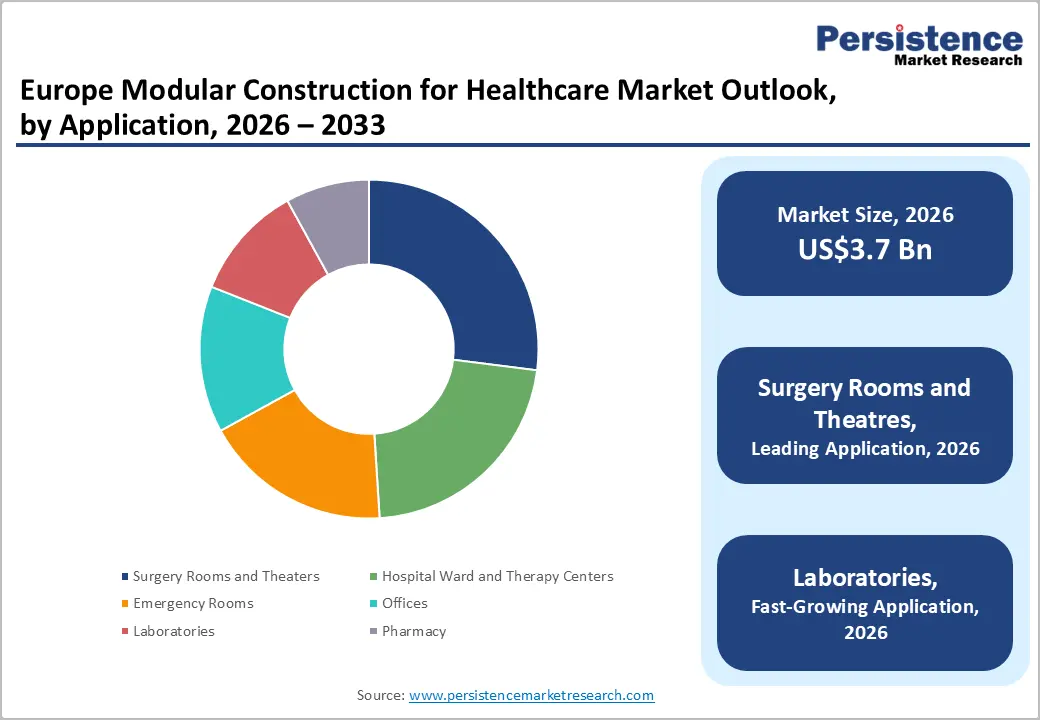

- Leading Application Segment: Surgery rooms and theaters are projected to hold a 27% share in 2026, while laboratories will be the fastest-growing segment at 6.8% CAGR, supported by expanding diagnostics infrastructure and biotech-driven facility expansion across Europe.

- Supporting Care Infrastructure: Hospital wards and therapy centers are anticipated to account for a 22% share in 2026, reflecting sustained demand from aging population needs and continuous hospital expansion programs across key European economies.

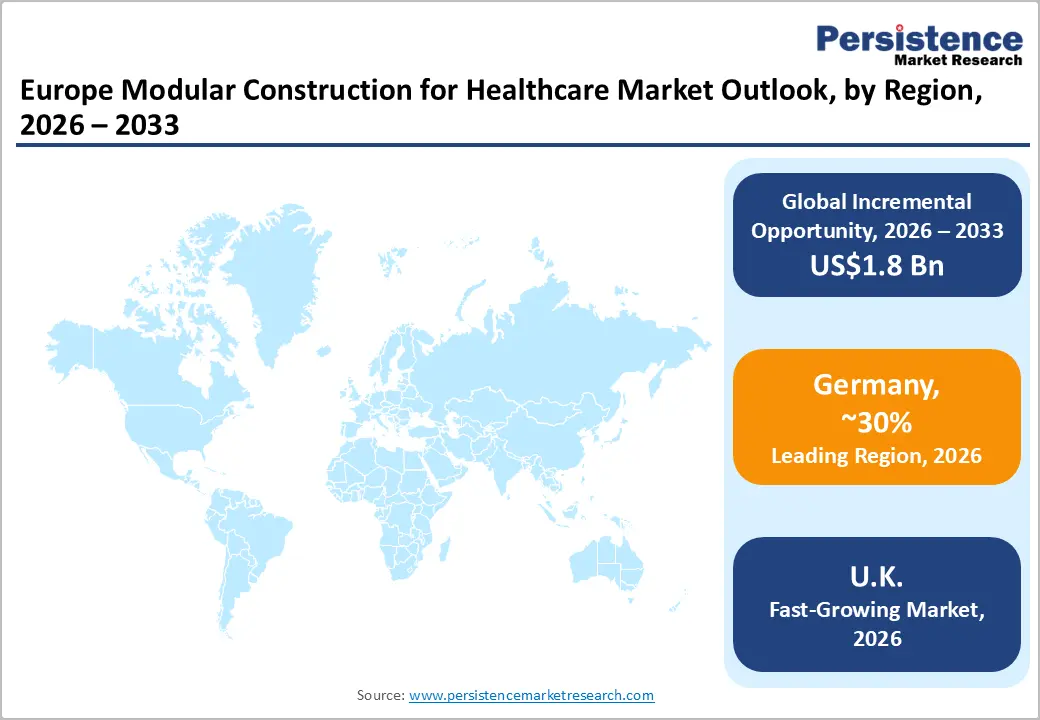

- Regional Leadership: Europe remains the core market, led by Germany, the U.K., and France, driven by strong public healthcare investments, hospital modernization programs, and EU-backed infrastructure resilience initiatives.

- Competitive Environment: Market expansion is driven by players such as Skanska, Laing O’Rourke, and Balfour Beatty, focusing on modular hospital delivery, faster project execution, and public-private partnerships across 2025 healthcare infrastructure programs.

DRO Analysis

Driver - Rising Healthcare Infrastructure Modernization across Europe

Healthcare infrastructure modernization under EU health resilience programs is a key market driver. According to the European Commission and Eurostat, EU member states are increasing healthcare capital expenditure to improve hospital capacity, digital readiness, and emergency preparedness. The European Investment Bank (EIB) has expanded funding support for sustainable hospital infrastructure, particularly energy-efficient modular facilities.

Governments in Germany, France, and the U.K. are prioritizing rapid deployment of healthcare units to reduce patient backlog and expand intensive care availability. The modular healthcare construction market in Europe benefits from shorter construction cycles (30-50% faster than traditional builds) and lower lifecycle disruption costs. This structural shift is significantly increasing adoption of prefabricated hospitals, laboratories, and emergency units across both public and private healthcare systems.

Restraint - High Initial Investment and Regulatory Complexity

High upfront capital costs and fragmented regulatory approvals remain key restraints in the Europe modular construction for healthcare market. Despite long-term savings, modular hospital units require significant initial investment in prefabrication facilities, logistics, and installation systems. Additionally, regulatory compliance varies across European countries, creating delays in the cross-border deployment of standardized modular healthcare units.

Building codes, medical facility certification standards, and infection control requirements differ between Germany, France, and Southern Europe, increasing project complexity. According to EU construction industry associations, approval timelines for healthcare infrastructure projects can be 20-35% longer in multi-country projects. This regulatory fragmentation increases risk for developers and slows the scalability of modular healthcare infrastructure solutions, particularly for small and mid-sized contractors.

Opportunity - Expansion of Temporary and Emergency Healthcare Facilities

Growing demand for temporary and emergency healthcare infrastructure presents a major opportunity in the modular healthcare construction market. Europe is increasingly investing in surge-capacity hospitals, isolation wards, and emergency response units following lessons from COVID-19 and seasonal epidemic pressures. The European Centre for Disease Prevention and Control (ECDC) has emphasized scalable healthcare infrastructure as part of pandemic preparedness frameworks.

Modular systems enable rapid deployment of relocatable healthcare facilities, reducing setup time from years to weeks. This creates strong opportunities in emergency rooms, mobile surgical units, and temporary hospital wards. The addressable opportunity is estimated at multi-billion-dollar expansion potential within public procurement cycles, especially in urban areas facing hospital overcrowding and aging infrastructure replacement needs.

Category-wise Analysis

Product Type Insights

Permanent modular construction leads the Europe healthcare modular construction market with around 58% share in 2026, driven by large-scale hospital modernization programs across Germany, France, and the U.K. It is widely used in surgical centers, diagnostic labs, and hospital expansions, where strict EU compliance and durability are critical. EU healthcare infrastructure upgrades and NHS capacity expansion programs are accelerating adoption, as modular delivery reduces construction time by 30-50% versus conventional builds. Its dominance is reinforced by lifecycle cost efficiency and integration with smart hospital systems such as digital monitoring and infection-control technologies.

Relocatable modular construction is the fastest-growing segment at a 6.5% CAGR through 20233, driven by demand for rapid and flexible healthcare capacity. These units are used for emergency wards, vaccination centers, and temporary diagnostic facilities, especially during outbreak surges. Their relevance increased significantly during COVID-19, when multiple European countries deployed temporary modular hospitals in Italy and Spain. Growth is further supported by ECDC-backed preparedness frameworks and rising rural healthcare gaps, making them a key solution for scalable and mobile healthcare infrastructure.

Application Insights

Surgery rooms and theaters account for approximately a 27% share in 2026, driven by strict sterility, airflow, and compliance requirements in EU hospitals. Germany and the U.K. are leading adoption through NHS and public hospital modernization programs aimed at reducing surgical waiting lists. Modular operating rooms enable faster deployment with integrated HVAC and infection-control systems, reducing construction downtime significantly compared to traditional infrastructure. Rising elective surgeries and capacity expansion initiatives continue to support steady demand.

Laboratories are expected to be the fastest-growing application at a 6.8% CAGR (2026 - 2033), driven by expansion in diagnostics, biotech R&D, and pharmaceutical testing. Growth is supported by EU Horizon Europe funding and post-pandemic investments in decentralized testing infrastructure. Modular labs enable rapid setup for PCR, genomics, and clinical trials, improving turnaround time and scalability. Increasing collaboration between biotech firms, universities, and public health agencies is accelerating adoption, particularly in Germany, France, and the Nordic research clusters.

Country Insights

Germany Modular Construction for Healthcare Market Trends

Germany is expected to lead the Europe modular healthcare construction market with around 30% share in 2026, driven by strong hospital modernization programs and sustained healthcare infrastructure investment. A key trend is the shift toward climate-neutral and digitally enabled hospitals, aligned with national sustainability targets and long-term healthcare transformation plans. Modular construction is widely used for surgical units, diagnostic laboratories, and hospital expansions, especially in urban areas facing capacity pressure.

Federal hospital reform programs and strict energy-efficiency requirements are accelerating the replacement of aging infrastructure. In response, Germany is prioritizing permanent modular healthcare systems integrated with BIM-based digital planning and smart hospital technologies, improving construction speed, efficiency, and compliance across public healthcare networks.

U.K. Modular Construction for Healthcare Market Trends

The U.K. is estimated to account for around 20% of Europe’s modular healthcare construction market in 2026, driven by NHS pressure and persistent surgical waiting lists exceeding 7 million patients. A key trend is the rapid deployment of fast-build modular healthcare infrastructure, including operating theaters, emergency departments, and outpatient units to reduce system bottlenecks.

The NHS New Hospital Programme and ongoing capital investment initiatives are accelerating the replacement of outdated hospital estates built before 1980. In response, the U.K. is focusing on cost-efficient, time-optimized modular construction solutions, enabling faster delivery timelines and improved healthcare capacity utilization across overstretched hospital systems.

Spain Modular Construction for Healthcare Market Trends

Spain is expected to hold approximately 10% of Europe’s modular healthcare construction market in 2026, driven by growing demand for urban hospital expansion and healthcare system modernization. A key trend is increasing focus on surge-capacity infrastructure, particularly in emergency rooms, outpatient centers, and diagnostic facilities in high-density urban regions.

Post-pandemic healthcare reforms and EU-supported infrastructure funding are accelerating the deployment of modular healthcare units across regional hospitals. In response, Spain is prioritizing rapid-deployment modular solutions, improving emergency care capacity, reducing service delays, and strengthening overall healthcare system resilience.

Competitive Landscape

The Europe modular construction for healthcare market is moderately consolidated, with major players such as Skanska, Balfour Beatty, Laing O’Rourke, Bouygues Construction, and VINCI Construction accounting for a significant revenue share. These firms benefit from strong government healthcare contracts and expertise in design-build delivery, off-site prefabrication, and integrated hospital infrastructure projects, enabling faster execution of complex healthcare facilities across Europe.

Alongside them, specialized and regional players such as Algeco, Portakabin, and Modulaire Group focus on relocatable hospitals, emergency care units, and rapid-deployment modular solutions. High regulatory standards, strict hospital compliance requirements, and complex integration needs create strong entry barriers for new players. However, increasing use of BIM, digital construction tools, and modular automation is encouraging collaboration between contractors and technology providers. The market is expected to consolidate further through acquisitions and strategic partnerships to expand geographic reach and healthcare project capabilities.

Key Industry Developments:

- In February 2025, Skanska entered into a binding Share Purchase Agreement (SPA) to sell its modular factory, BoKlok Byggsystem AB, located in Gullringen, Sweden. The buyer is Surewood Housing AB, a company affiliated with Gelba and Active Invest. The transaction will be reported under Central in the first quarter of 2025, with the factory handover scheduled for 20th February 2025.

- In January 2024, Bouygues Construction launched a new line of modular healthcare units designed for rapid deployment in emergencies.

Companies Covered in Europe Modular Construction for Healthcare Market

- Skanska

- Balfour Beatty

- Laing O’Rourke

- Kiewit Corporation

- Larsen & Toubro

- Bouygues Construction

- VINCI Construction

- ACS Group

- Turner Construction

- Algeco

- Portakabin

- Elematic

- CIMC Modular Building Systems

- Red Sea International

- Modulaire Group

Frequently Asked Questions

The Europe modular construction for healthcare market is valued at US$3.7 billion in 2026.

Rising demand for rapid hospital expansion, aging population pressures, and EU-backed healthcare modernization programs drive the market.

The Europe modular construction for healthcare market is expected to grow at a CAGR of 5.7% from 2026 to 2033.

Opportunities include expansion of modular emergency care facilities, hospital redevelopment programs, and rising adoption of relocatable healthcare infrastructure.

Key players include Skanska, Balfour Beatty, Laing O’Rourke, Bouygues Construction, and VINCI Construction.