- Medical Devices

- Digital Pathology Market

Digital Pathology Market Size, Share, and Growth Forecast 2026 - 2033

Digital Pathology Market by Product Type (Digital Pathology Equipment, Digital Pathology Software, Digital Pathology Services), by Application (Clinical Pathology, Molecular Diagnostics, Basic and Applied Research, Drug Development, Others), End-user (Hospitals, Diagnostic Laboratories, Pharmaceutical and Biotechnology Companies, Forensic Laboratories, Research Institutes, Contract Research Organizations (CROs), Clinics), and Regional Analysis, 2026 - 2033

Digital Pathology Market Share and Trends Analysis

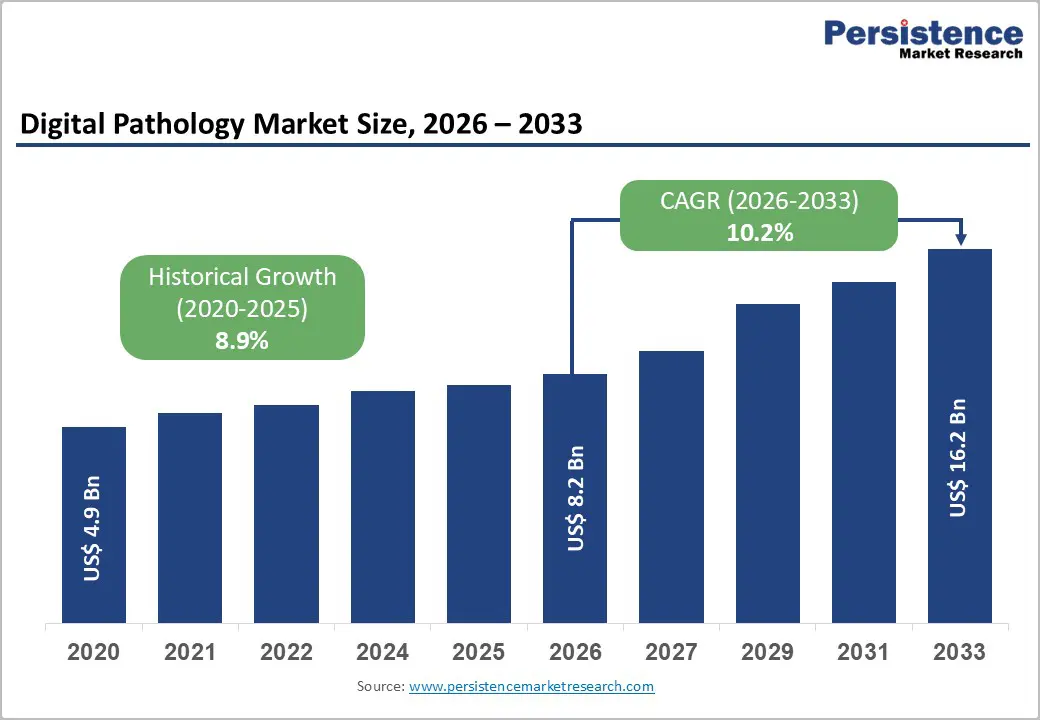

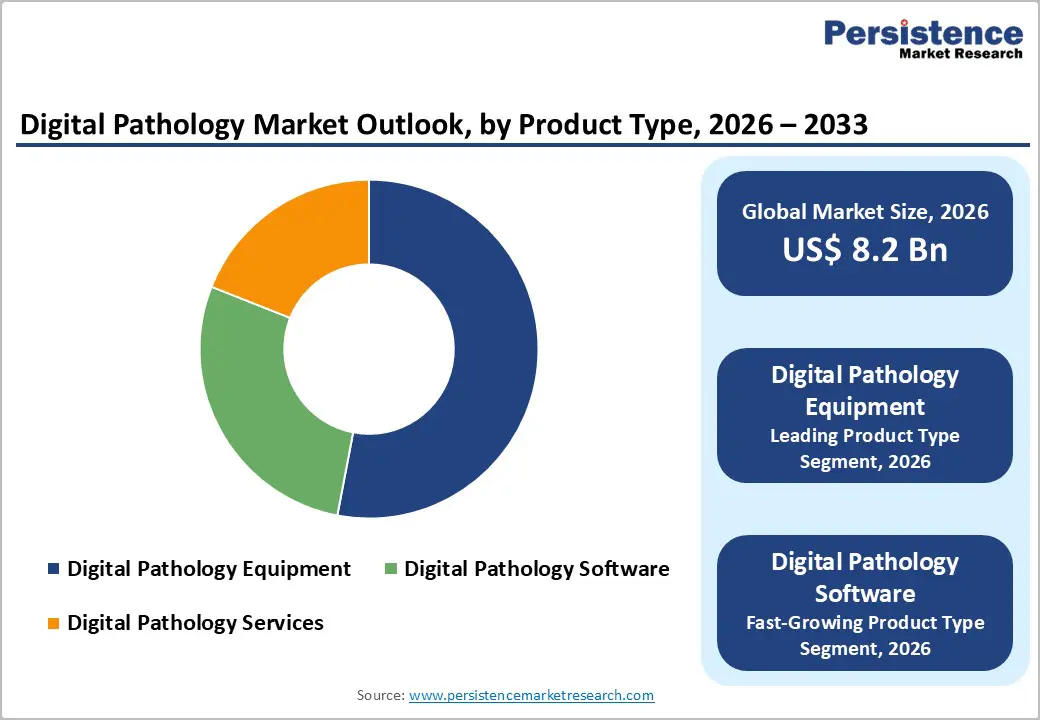

The global digital pathology market size is expected to be valued at US$ 8.2 billion in 2026 and projected to reach US$ 16.2 billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

The primary growth catalysts include the escalating global cancer burden, with the American Cancer Society projecting approximately 2,041,910 new cancer diagnoses in the United States in 2025 alone, combined with rapid integration of artificial intelligence and machine learning technologies into diagnostic pathology workflows. FDA regulatory approvals and the shift toward personalized medicine are accelerating adoption in both clinical laboratories and pharmaceutical research settings, driving demand for efficient, high-throughput diagnostic solutions across hospitals, diagnostic laboratories, and pharmaceutical and biotechnology companies.

Key Highlights

- Development of accurate and efficient diagnostic tools is required due to the rising incidence of chronic illnesses, such as cancer and heart disease.

- Innovations in whole-slide imaging, image analysis software, and AI have significantly improved diagnostic precision and operational efficiency.

- Telepathology solutions enable real-time global consultation and real-time case review, while healthcare IT adoption streamlines processes and reduces costs.

- Adoption of digital pathology is fueled by the globalization of healthcare services, emphasizing patient-centered care and efficiency enhancement.

- In 2024, hospitals are estimated to attain a market share of 26.8% due to rising admissions.

- Based on applications, the clinical pathology segment is projected to account for a market share of 23.3% in 2024 due to rising prevalence of cancer.

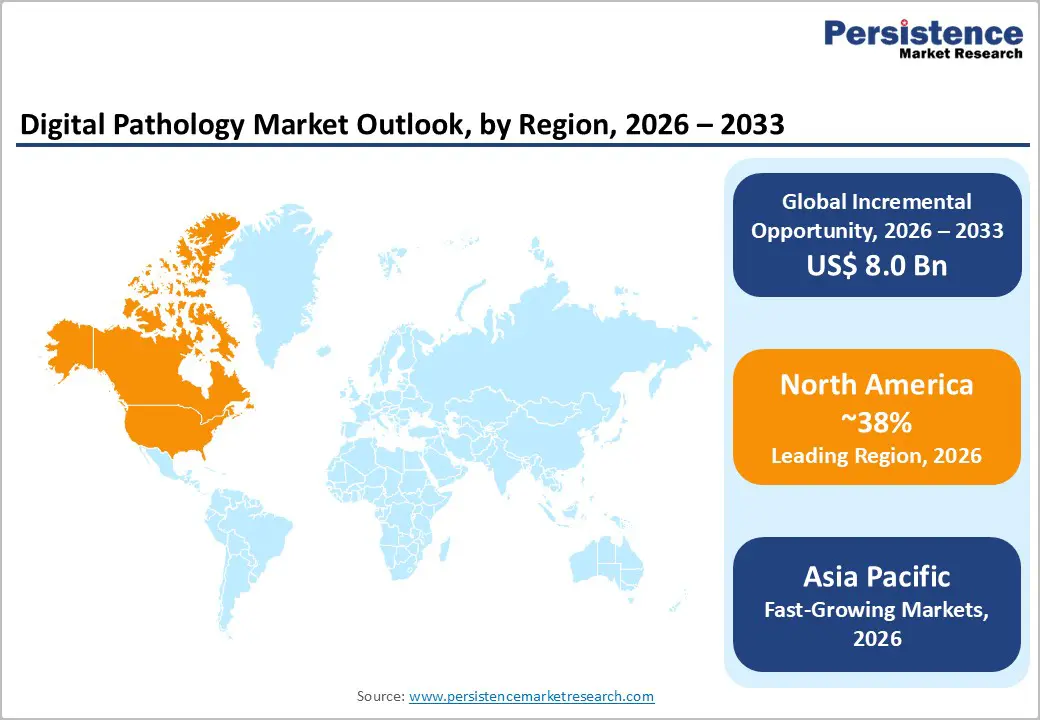

- Owing to research and development investments, North America is estimated to attain a market share of 44.2% in 2024.

- Europe is anticipated to capture a market share of 28.3% in 2024 with developments in healthcare technology.

| Global Market Attributes | Key Insights |

|---|---|

| Digital Pathology Size (2026E) | US$ 8.2 billion |

| Market Value Forecast (2033F) | US$ 16.2 billion |

| Projected Growth CAGR(2026-2033) | 10.2% |

| Historical Market Growth (2020-2025) | 8.9% |

Market Dynamics Analysis

Drivers - Accelerating Cancer Burden Driving Diagnostic Demand

Rising global cancer incidence represents the foremost growth driver for digital pathology, with cancer cases in the United States alone expected to reach approximately 2,041,910 diagnoses in 2025, equivalent to about 5,600 cases daily according to the American Cancer Society. Digital pathology systems enable pathologists to process significantly higher case volumes through automated image analysis and AI-driven quantification, reducing turnaround times and improving diagnostic accuracy in oncology applications. The World Cancer Research Fund reports that breast cancer, lung cancer, and colorectal cancer comprise over 51% of female cancer diagnoses and 48% of male diagnoses, necessitating high-throughput diagnostic infrastructure. Hospital-based laboratory segments hold 53.7% of clinical laboratory services market share, with digital pathology becoming critical for managing rising patient volumes and ensuring consistent diagnostic quality across major medical centers.

FDA Regulatory Approvals and Clinical Integration

FDA clearances for digital pathology systems have accelerated adoption in clinical practice, with multiple whole-slide imaging scanners and AI-enabled diagnostic software receiving regulatory approval for primary diagnosis. In 2024, Roche received FDA 510(k) clearance for its VENTANA DP 200 whole-slide imaging system, while February 2024 saw Proscia obtain FDA approval for its Concentriq AP-Dx diagnostic software. These regulatory milestones validate the clinical utility of digital workflows and build pathologist confidence in adopting scanner-based diagnostics. The integration of digital pathology systems with laboratory information systems (LIS) enables real-time data sharing, reduces human error, and decreases specimen handling times. Studies published in JAMA Network Open demonstrate that AI-assisted diagnostic models increase pathologist efficiency by over 20% without compromising diagnostic accuracy, making regulatory approval pathways increasingly attractive for hospital adoption.

Restraint - High Capital Investment and Infrastructure Costs

Substantial upfront expenditures for whole-slide imaging scanners, enterprise storage solutions, and software licensing systems present significant barriers to adoption, particularly for smaller diagnostic laboratories and community hospitals. Digital pathology equipment requires specialized infrastructure including gigapixel image storage, robust network connectivity, and trained personnel, with systems costing hundreds of thousands of dollars per installation. The absence of comprehensive reimbursement codes in many healthcare systems creates unfavorable return-on-investment scenarios, limiting adoption in budget-constrained institutions. Interoperability challenges between proprietary scanner platforms and legacy laboratory information systems require substantial integration services and consulting expenditures, further elevating implementation barriers.

Data Security and Regulatory Compliance Burden

Managing sensitive patient tissue data and imaging files across digital platforms presents complex cybersecurity and regulatory compliance challenges under HIPAA in the United States, GDPR in Europe, and various national healthcare data protection regulations. The transition to EU IVDR (In Vitro Diagnostic Regulation) compliance requires vendors to obtain CE marking through notified bodies, extending product development timelines and increasing certification costs. Pathology laboratories must implement robust data governance frameworks, encryption protocols, and audit trails to maintain regulatory compliance, creating operational complexity and ongoing compliance expenses. Organizations implementing digital pathology require substantial investments in cybersecurity infrastructure, staff training, and validation protocols to ensure data protection and regulatory adherence.

Opportunity - AI-Driven Drug Discovery and Precision Medicine Expansion

Pharmaceutical and biotechnology companies represent the fastest-growing end-user segment, leveraging digital pathology for accelerated drug discovery, biomarker validation, and clinical trial optimization. AI-enabled tissue analysis reveals hidden patterns in histology slides, enabling more robust therapeutic target identification and improving drug development success rates. The integration of multi-omics data with digital pathology images allows researchers to correlate genomic, proteomic, and morphological features, advancing precision medicine applications. Contract research organizations (CROs) increasingly adopt cloud-based digital pathology platforms to support global clinical trials and standardize biomarker assessment across multiple sites, creating substantial market opportunities for vendors offering interoperable, scalable solutions.

Telepathology and Remote Diagnostics for Underserved Regions

Digital pathology enables telepathology services, addressing critical pathologist shortages in rural and underserved areas by facilitating remote expert consultations and second opinions without physical slide transport. Asian healthcare systems are investing heavily in telepathology infrastructure under government digitization mandates, with China’s “Healthy China 2030” plan requiring county-level telepathology connectivity and allocating significant funding for scanner deployment. India’s Ayushman Bharat Digital Mission allocated INR 15 billion for digital health infrastructure in 5,000 hospitals, creating substantial demand for remote diagnostic capabilities. Cloud-based image repositories enable seamless cross-border collaboration and support high-throughput screening programs in emerging markets, unlocking significant revenue opportunities for platforms supporting distributed pathology workflows.

Category-wise Analysis

Product Type Insights

Digital Pathology Equipment dominates with 53% market share in 2025, primarily driven by whole-slide imaging scanners essential for converting traditional glass slides into high-resolution digital images suitable for clinical diagnosis and research applications. Whole-slide imaging technology has progressed substantially, with systems capable of scanning and storing gigapixel-resolution images enabling detailed tissue analysis and facilitating remote consultations. The regulatory pathway for FDA approval validates equipment reliability and clinical safety, as evidenced by Roche’s VENTANA DP 200, Hamamatsu’s NanoZoomer, and other cleared systems gaining adoption in hospital pathology departments. Equipment segments continue commanding market leadership due to their foundational role in establishing digital infrastructure, with 53.7% of hospital-based laboratory services investing in scanner acquisitions to support high-volume diagnostic workflows.

Application Insights

Clinical Pathology represents the leading application segment with approximately 29.9% market share in 2025, driven by essential diagnostic needs for cancer detection, chronic disease management, and rapid case turnaround in hospital settings. Digital workflows enable high-resolution image analysis, automated quantification of biomarkers, and integration with artificial intelligence algorithms for tumor grading and prognostic assessment. WHO epidemiological data documenting over 20 million annual cancer cases globally creates persistent demand for accurate, timely pathology diagnostics supporting oncology treatment decisions. The shift toward personalized medicine emphasizes precise biomarker identification and tissue-based patient stratification, reinforcing clinical pathology’s market leadership position through 2033.

End-user Insights

Hospitals represent the dominant end-user segment with approximately 53.7% share of clinical laboratory services market in 2025, benefiting from integrated infrastructure enabling rapid patient specimen processing and urgent diagnostic turnaround. Large hospital networks achieve economies of scale in digital pathology adoption, supporting high daily scanning volumes exceeding hundreds of cases across multiple departments including oncology, surgical pathology, and hematopathology. Hospital-based laboratory advantage stems from established relationships with clinicians, insurance reimbursement agreements, and centralized IT infrastructure supporting enterprise-level digital pathology deployments. Integration of digital pathology with electronic health records (EHRs) and laboratory information systems streamlines clinician-pathologist communication and enables automated result notification, reinforcing hospital leadership in digital pathology adoption.

Regional Insights

North America Digital Pathology Market Trends

North America commands market leadership with 38% global share in 2025, anchored by the United States healthcare system’s advanced infrastructure, robust FDA regulatory framework, and substantial investment in diagnostic innovation. The American Cancer Society reports approximately 2,041,910 new cancer diagnoses annually in the United States, creating strong demand for efficient pathology workflows supported by digital scanning and AI-assisted analysis. FDA regulatory approvals for whole-slide imaging systems continue accelerating, with June 2024 seeing Roche VENTANA DP 200 clearance and subsequent approvals validating clinical safety and diagnostic accuracy.

North America’s dominance reflects well-established reimbursement models, early regulatory approvals, and the presence of major technology leaders, including Roche, Philips, Leica Biosystems (part of Danaher Corporation), and Hamamatsu. Hospital networks increasingly adopt digital pathology to reduce turnaround times, improve diagnostic consistency, and meet rising case volumes, supported by investment in infrastructure modernization and AI integration. The region’s innovation ecosystem fosters partnerships between pathology organizations, academic medical centers, and digital health vendors, accelerating technology adoption and standardization.

Asia Pacific Digital Pathology Market Trends

Asia Pacific digital pathology market is emerging as one of the fastest growing regional markets globally, driven by expanding healthcare infrastructure, rising prevalence of chronic diseases such as cancer, and increasing demand for advanced diagnostic technologies. Healthcare providers across China, India, Japan, and Southeast Asia are adopting digital pathology solutions to improve diagnostic accuracy, enable remote consultations, and streamline pathology workflows, particularly in cancer diagnostics and telemedicine applications. Government initiatives and investments in digital health frameworks are further accelerating adoption, while AI powered imaging and cloud based platforms enhance efficiency and collaboration across institutions. India, with its telepathology expansion and rural healthcare digitization efforts, is among the fastest growing national markets in the region. Challenges such as regulatory inconsistencies and shortages of skilled personnel remain, but overall growth is supported by increasing healthcare spending, technological innovation, and the growing importance of precision medicine in the Asia Pacific.

Competitive Landscape

The digital pathology market is moderately consolidated with a mix of established global players and emerging innovators driving competition. Firms compete on technology integration, particularly AI enabled analytics, cloud based workflow platforms, and improved interoperability, pushing the market toward seamless, end to end digital solutions. Competitive strategies include strategic partnerships, R&D investments, bundled hardware software offerings, and service expansion to capture broader clinical and research use cases. Differentiation increasingly centers on workflow efficiency, regulatory compliance, and platform flexibility, with emphasis on vendor neutral and scalable architectures to support multi site deployments.

Key Market Developments

- In November 2024, South Korea-based Lunit and the U.K.-based AstraZeneca collaborated to develop an AI-powered digital pathology tool, the Lunit SCOPE Genotype Predictor. It predicts the likelihood of NSCLC driver mutations in tumors, improving detection speed and accuracy.

- In November 2024, India-based Molbio Diagnostics invested US$ 30 Mn in OptraSCAN, a San Jose-based diagnostics company, to enhance digital pathology solutions. It aims to make novel diagnostics more accessible to underserved communities.

- In September 2024, Roche, based in Switzerland, partnered with eight new collaborators to integrate over 20 AI algorithms into its digital pathology environment. It aims to revolutionize cancer research, diagnosis, and treatment, ultimately improving patient outcomes.

Companies Covered in Digital Pathology Market

- Danaher Corporation

- F. Hoffmann-La Roche AG

- Huron Technologies International Inc.

- Koninklijke Philips N.V.

- Olympus Corporation

- Hamamatsu Photonics K.K.

- Carl Zeiss AG

- Nikon Corporation

- 3DHISTECH Ltd.

- Hologic Inc.

- PerkinElmer, Inc.

- Visiopharm

- OptraSCAN, Inc.

- Inspirata, Inc.

- Sectra AB

Frequently Asked Questions

The global Digital Pathology market is expected to reach US$ 8.2 billion in 2026, with projections extending to US$ 16.2 billion by 2033, reflecting a CAGR of 10.2% between 2026 and 2033.

Rising global cancer burden represents the foremost growth driver, with the American Cancer Society projecting approximately 2,041,910 new cancer diagnoses in the United States in 2025, necessitating efficient, high-throughput diagnostic solutions and accelerating digital pathology adoption in hospitals and diagnostic laboratories.

North America dominates with 38% global market share in 2025, anchored by the United States healthcare system’s advanced infrastructure, FDA regulatory approvals for whole-slide imaging systems, and strong adoption in hospital pathology departments and academic medical centers.

AI-driven drug discovery and precision medicine applications in pharmaceutical research present significant opportunities, with pharmaceutical and biotechnology companies increasingly leveraging digital pathology for accelerated clinical trials, biomarker validation, and personalized medicine development across global research networks.

Market leaders include Danaher Corporation, F. Hoffmann-La Roche AG, Koninklijke Philips N.V., Hamamatsu Photonics K.K., Carl Zeiss AG, Hologic Inc., PerkinElmer, Inc., and emerging companies including PathAI and Proscia, with competitive advantages based on FDA/CE regulatory approvals, AI algorithm accuracy, and enterprise integration capabilities.