- Healthcare IT

- Mobile Health Apps and Solutions Market

Mobile Health Apps and Solutions Market Size, Share, and Growth Forecast, 2026-2033

Mobile Health Apps and Solutions Market by Solution (Fitness & Wellness Apps, Chronic Disease Management Apps, Mental Health & Therapy Apps, Women’s Health Apps, Medication Reminder Apps, Teleconsultation Apps, others), Application (Chronic Disease Management, Mental & Behavioral Health, Preventive & Wellness, Medication Management, Rehabilitation Care, Others), End-User (Patients, Healthcare Providers, Athletes, Pharmaceutical Companies), and Regional Analysis for 2026-2033

Mobile Health Apps and Solutions Market Share and Trends Analysis

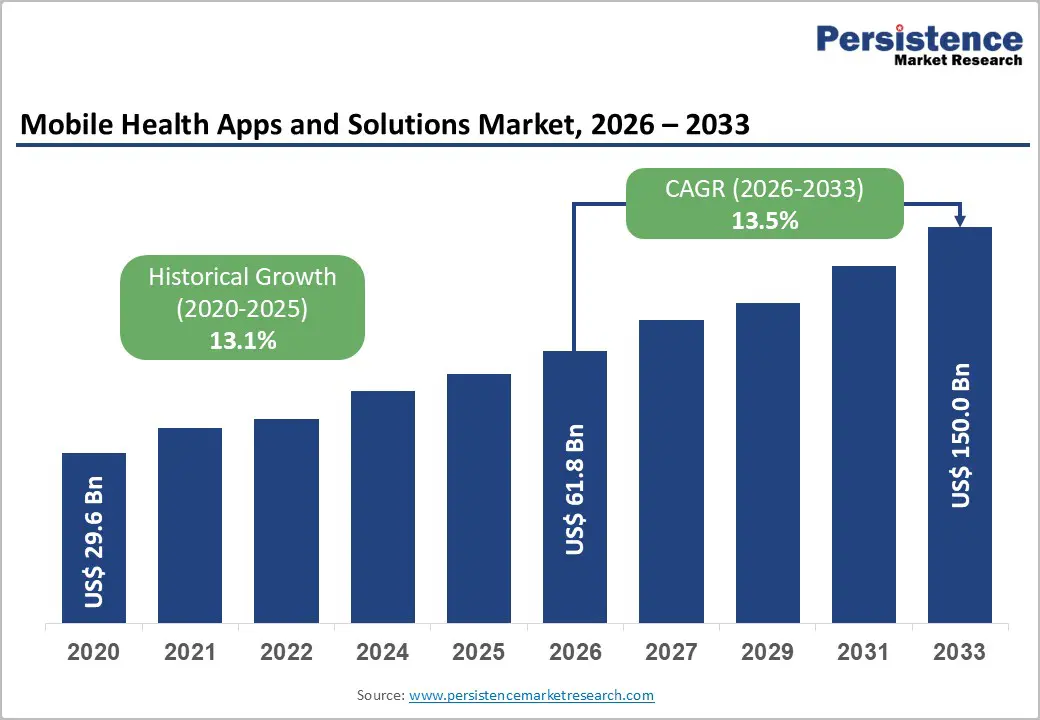

The global mobile health apps and solutions market size is likely to be valued at US$ 61.8 billion in 2026, and is projected to reach US$ 150.0 billion by 2033, growing at a CAGR of 13.5% during the forecast period 2026–2033. Market expansion is being driven by accelerated smartphone adoption, increasing prevalence of chronic diseases, and formal digitization mandates within healthcare systems across developed and emerging economies.

Governments and payers are promoting digital integration to improve access to care, reduce system burden, and enhance data continuity. Structural transitions toward remote patient monitoring (RPM), value-based care (VBC), and preventive health management are positioning mobile health platforms as essential infrastructure rather than supplementary tools. As digital connectivity improves, healthcare providers are integrating application-based monitoring into routine clinical pathways to improve adherence and early intervention. Mobile health applications are increasingly supporting telehealth services, digital therapeutics (DTx), and integrated patient engagement platforms.

Regulatory frameworks in several regions are recognizing digital therapeutics as reimbursable interventions, thereby strengthening their commercial viability. Reimbursement-backed virtual consultation models are expanding adoption among providers and patients, particularly for chronic disease management and behavioral health services. Healthcare organizations are leveraging real-time data analytics and interoperable systems to enhance outcome measurement and personalized treatment pathways. As healthcare systems continue transitioning toward outcome-driven reimbursement structures, mobile health ecosystems are becoming central to cost optimization and patient-centered care delivery.

Key Industry Highlights

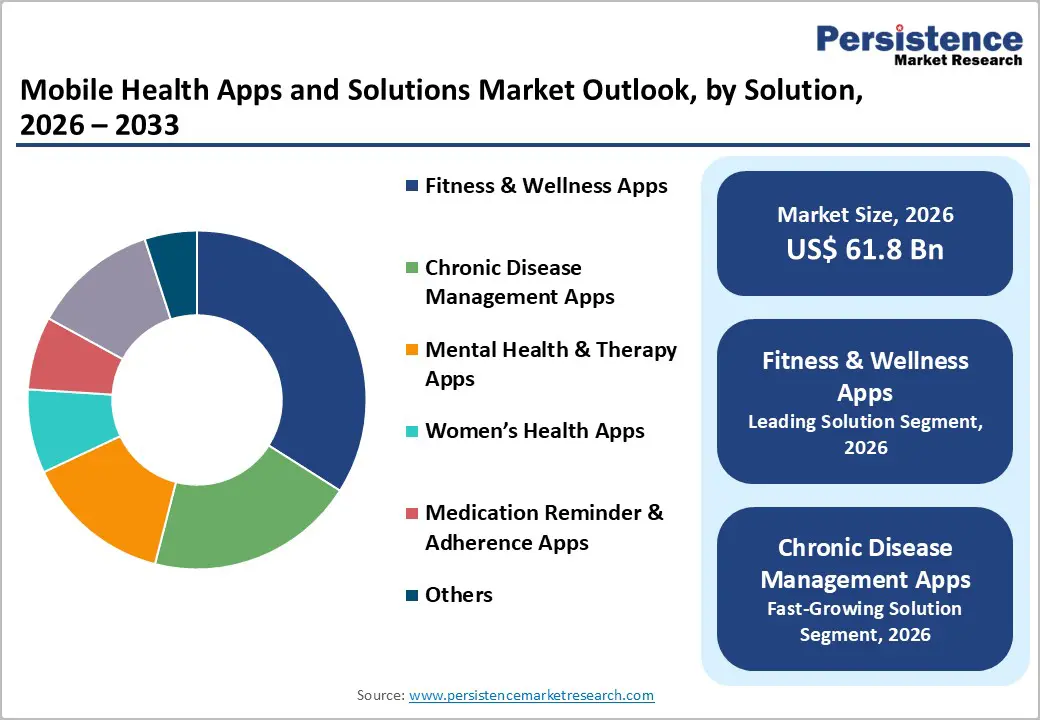

- Dominant Solution: Fitness & wellness apps are expected to lead with an estimated 34% revenue share in 2026 due to broad consumer adoption, while chronic disease management apps are projected to grow fastest at roughly 15.2% CAGR through 2033, driven by reimbursement-backed remote care.

- Leading Application Area: Preventive & wellness applications are anticipated to dominate, with about 31% share in 2026, reflecting proactive health trends, while mental & behavioral health applications are expected to expand at approximately a 16.1% CAGR, supported by digital therapy uptake.

- Primary End-User Group: Patients are projected to generate an approximate 48% of market revenues in 2026, owing to direct-to-consumer (D2C) access, while healthcare providers are expected to post the highest CAGR of 14.6%, as telehealth integrates into care delivery.

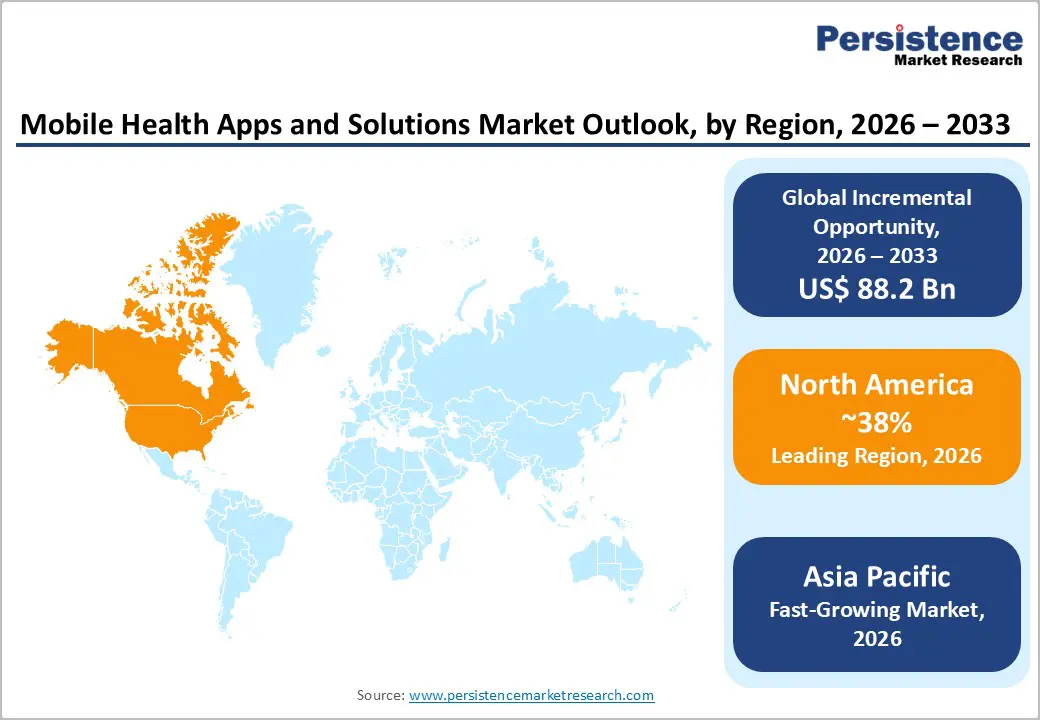

- Regional Leadership: North America is expected to lead with a roughly 38% share in 2026, backed by supportive reimbursement and innovation policies, while Asia Pacific is projected to grow fastest at nearly 15.8% CAGR, driven by mobile-first healthcare adoption.

- Investment and Innovation Focus: AI, telehealth, and remote patient monitoring remain key investment areas, enabling scalable and personalized digital health solutions.

| Global Market Attributes | Key Insights |

|---|---|

| Mobile Health Apps and Solutions Market Size (2026E) | US$ 61.8 Bn |

| Market Value Forecast (2033F) | US$ 150.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Chronic Disease Burden, Ageing Populations, and Digital Healthcare Enablement

The increasing prevalence of noncommunicable diseases (NCDs), including cardiovascular diseases, diabetes, cancers, and chronic respiratory illnesses, is a major driver of growth in the mobile health apps and solutions market. According to the World Health Organization (WHO), NCDs account for about 74% of all global deaths, with more than 40 million fatalities annually, imposing significant pressure on healthcare systems and escalating long-term care costs. These persistent conditions require frequent monitoring and management, driving uptake of mobile health solutions that enable continuous disease tracking, remote interventions, and medication adherence support outside traditional care settings. NCD mortality and morbidity are closely tied to ageing demographics, as older populations are significantly more likely to experience multiple chronic conditions.

The global population ageing is accelerating. As per WHO projections, by 2030, one in six people worldwide will be aged 60 or older, up from one in seven in 2019, and the number of people in this age group is projected to rise from 1 billion in 2020 to 1.4 billion by 2030, intensifying the demand for scalable, patient-centric digital care. Older adults often require continuous health monitoring, making mobile health solutions an efficient alternative to frequent clinical visits. Alongside demographic shifts, expanding smartphone and mobile internet penetration support real-time health data exchange and broaden access to digital health tools across populations. Meanwhile, supportive healthcare policies and reimbursement frameworks continue to accelerate clinical adoption and enterprise-scale deployment of mobile health platforms.

Regulatory Scrutiny, Security Vulnerabilities, and Interoperability Constraints

The growth of the mobile health apps and solutions market is significantly constrained by heightened regulatory scrutiny, inconsistent clinical validation standards, and concerns about data security. Apps that influence diagnosis, treatment decisions, or patient behavior are subject to stringent health software and medical device regulations, requiring demonstrable clinical evidence for safety and effectiveness. Several existing solutions do not meet these evidence thresholds, limiting acceptance by healthcare providers and payers and delaying or disqualifying reimbursement eligibility. Fragmented interoperability with electronic health record (EHR) systems disrupts clinician workflows and reduces the practical utility of mobile health data, thereby constraining large-scale institutional deployment and extending it into core clinical infrastructure.

Recent real-world incidents have underscored these constraints. In late 2025, for example, the ManageMyHealth patient portal in New Zealand suffered a major cybersecurity breach, with unauthorized access to the “My Health Documents” module compromising the sensitive medical documents of over 120,000 users and prompting government-ordered reviews and regulatory involvement to assess data protection failures. The breach highlighted persistent security vulnerabilities in third-party health solutions and amplified provider and patient concerns about data privacy, accelerating scrutiny by privacy commissioners and national cybercrime units. Limited integration safeguards and weak interoperability protocols continue to expose institutional risk, slowing enterprise procurement cycles and inhibiting trust in mobile health platforms as core clinical tools.

Expansion through Emerging Markets, Digital Integration, and Life-Saving Applications

The market presents multiple high-value opportunities for growth and monetization. Rising demand exists for chronic disease management, preventive care, mental health support, and women’s health solutions, all of which can be delivered via mobile platforms. Emerging markets offer scalable adoption due to mobile-first populations and expanding healthcare infrastructure. Additionally, there are opportunities in enterprise wellness programs, teleconsultation services, and subscription-based digital health models, enabling recurring revenue streams. Integration with AI and wearables allows predictive health insights and personalized interventions, creating new services for patients, providers, and insurers. These areas collectively position the market as a rapidly expanding, multi-segment revenue opportunity during the forecast period.

However, AI integration, wearables, and remote monitoring unlock transformative opportunities in predictive and personalized care. An incident reported by TOI, in October 2025, where a 26-year-old in Madhya Pradesh, India, received a critical heart-rate alert from his Apple Watch Series 9, prompting immediate medical intervention that likely prevented a life-threatening stroke and severe hypertensive episode. This demonstrates the life-saving potential of mobile health apps when integrated with wearable devices and real-time analytics. Thus, the combination of employer-backed wellness programs and preventive care initiatives positions mobile health solutions as essential tools for value-based care, early intervention, and population health management worldwide.

Category-wise Analysis

Solution Insights

The fitness & wellness apps segment is projected to be the leading solution category, with an estimated 34% revenue share in 2026. This is supported by high consumer adoption, widespread integration of wearables, and subscription-based monetization models. The growth drivers include demand for activity tracking, personalized fitness guidance, and preventive health insights. A notable example is Samsung Health expanding its platform to include virtual doctor visits and prescription tracking, demonstrating how preventive and clinical capabilities can increase engagement. These integrations are expected to further reinforce its leadership position in the revenue-generating category. Consumer preference for convenient, integrated health tools will continue to sustain adoption and monetization throughout the forecast period.

Chronic disease management apps are expected to be the fastest-growing solution segment, with a projected 15.2% CAGR between 2026 and 2033. Growth is driven by rising prevalence of chronic conditions, payer-supported remote monitoring programs, and integration with clinical workflows, which market players are leveraging. For instance, NowPatient partnered with Lifelight to deliver smartphone-based blood pressure measurement, enabling remote monitoring and virtual care management. This enhances adherence, reduces hospital visits, and supports reimbursement models. The segment is expected to gain market share as healthcare providers and patients increasingly rely on mobile platforms for chronic disease management. Its scalable, outcome-focused solutions make it a critical growth driver.

Application Insights

Preventive & wellness applications are projected to account for approximately 31% of the mobile health apps and solutions market revenue in 2026, driven by trends in proactive health management and corporate wellness programs. These applications provide predictive health insights and continuous monitoring to identify risks early, enabling cost reduction and population health management. Integration with telehealth platforms and wearable devices further strengthens their value proposition. These solutions support long-term engagement by promoting behavior change, habit tracking, and lifestyle management. Their scalability and applicability across individual and enterprise settings drive adoption, making this segment a foundation for revenue generation and long-term market growth.

Mental & behavioral health applications are expected to be the fastest-growing application segment, with an estimated 16.1% CAGR through 2033, driven by rising anxiety, depression, and post-pandemic stress prevalence. Digital therapy adoption and reimbursement support facilitate institutional and consumer uptake. Cope Notes, which provides psychology-reviewed daily messaging and mental health prompts, was included in UnitedHealthcare’s Florida Medicaid program, reflecting institutional validation and potential for scale. These apps increase access to mental health support, complement traditional therapy, and enable continuous monitoring of mood and behavior. Integration with mobile devices and telehealth platforms further accelerates adoption in both consumer and clinical contexts.

End-User Insights

Patients are poised to remain the largest end-user group, accounting for an estimated 48% of the mobile health apps and solutions market in 2026, supported by direct-to-consumer access and rising health literacy. Patients leverage mobile apps for fitness tracking, preventive care, chronic disease monitoring, and teleconsultations. For example, Samsung Health’s 2025 enhancements enabled patients to manage virtual appointments and prescriptions within a single platform, reinforcing engagement and sustained use. The integration of wearable data, predictive insights, and user-friendly interfaces strengthens adoption across demographics. The patient-focused segment continues to drive volume and revenue growth, providing a consistent base for market expansion over the forecast period.

Healthcare providers are expected to be the fastest-growing end-user segment, with a projected 14.6% CAGR from 2026 to 2033, as providers increasingly adopt mobile platforms for care coordination, remote monitoring, and workflow optimization. In early 2026, OneStep, a smartphone-based gait analysis platform, enabled clinicians to remotely track rehabilitation progress and detect fall risks in real-time. Provider-focused solutions improve clinical efficiency, optimize resource allocation, and expand telehealth adoption. Institutional deployment in hospitals, clinics, and senior care facilities is expected to accelerate segment growth. The convergence of digital tools and clinical practice positions this segment as a key driver of market expansion.

Regional Insights

North America Mobile Health Apps and Solutions Market Trends

North America is projected to be the largest regional market for mobile health apps and solutions, spearheaded by the U.S., capturing an estimated share of 38% in 2026. The region’s advanced digital infrastructure, high smartphone penetration, and robust broadband connectivity support widespread adoption of mobile health solutions. Regulatory clarity and reimbursement for telehealth, remote monitoring, and digital health integration continue to strengthen provider and patient uptake. In 2025, for example, Cedars-Sinai Health System expanded its AI-powered virtual care platform, CS Connect, demonstrating real-world institutional use of mobile health technology to provide 24/7 virtual care and symptom assessment, serving over 42,000 patients and improving guideline-based care recommendations.

Regional market growth is also being bolstered by investments in clinician-centric digital tools that improve care coordination and operational efficiency. Expanded use of mobile platforms for chronic condition management, AI-assisted patient intake, and virtual triage enhances clinical workflows and accelerates institutional adoption. Continued expansion in enterprise digital health, remote care models, and preventive health management is expected to sustain North America’s leadership in revenue and innovation throughout the forecast period. Close partnerships between health systems, insurers, and tech developers further reinforce the region’s dominant position.

Europe Mobile Health Apps and Solutions Market Trends

The Europe mobile health apps market growth is driven by public healthcare digitization and harmonized data protection frameworks such as the General Data Protection Regulation (GDPR). National health services in Germany, the U.K., and France are integrating mobile solutions into mainstream care delivery, improving access and operational efficiency, particularly for preventive care and chronic disease management. Interoperability standards and secure governance frameworks support cross-border innovation and foster provider confidence in mobile health adoption. Investments in compliant digital health infrastructure, combined with increasing patient and provider digital literacy, underpin steady regional expansion. Enhanced telehealth, remote monitoring, and preventive care platforms are central to this market’s growth trajectory.

Teleconsultation platforms with extensive operations in Europe, such as Doctolib, are expected to continue expanding across Southern and Eastern Europe, enhancing multilingual access and streamlining appointment scheduling. These developments illustrate how mobile health solutions are aligning with national insurance coverage models and clinician workflows to reduce administrative burdens. Integration with electronic health records and patient management systems further drives adoption among providers and consumers. Public-private partnerships, digital health networks, and employer wellness programs support broader use across age groups. These advancements are expected to sustain Europe’s steady market growth throughout the forecast period.

Asia Pacific Mobile Health Apps and Solutions Market Trends

Asia-Pacific is projected to be the fastest-growing regional market for mobile health apps and solutions, with an anticipated 17.5% CAGR from 2026 to 2033, driven by large mobile adoption. first populations, rising healthcare demand, supportive government policies, and rapid digital adoption. High smartphone and mobile internet penetration acceleratethe uptake of mobile health solutions for preventive care, chronic disease management, and telehealth access in both urban and rural areas. A key development illustrating regional innovation is the rapid growth of Health2Sync’s “SugarGenie” digital disease management platform in South Korea, which is being adopted by more than 100 healthcare institutions for diabetes and hypertension care, thereby improving patient monitoring and personalized guidance.

The growth momentum is further bolstered by consolidation of digital health systems and platform standardization initiatives. In early 2026, Malaysia-based Kumo’s cloud healthcare platform was adopted by more than 2,500 clinics across Malaysia, Indonesia, and Thailand, streamlining clinical operations, EHR access, billing, and third-party integrations, underscoring the region’s drive toward interoperable digital ecosystems. Public health digitization initiatives and national digital health missions in India, China, and other regional economies complement private-sector innovations, creating a conducive environment for scalable mobile health adoption. These multi-dimensional drivers are expected to position Asia Pacific as a high-growth regional opportunity through 2033.

Competitive Landscape

The global mobile health apps and solutions market structure is moderately consolidated, with leading players, including Apple, Google, Samsung, and Teladoc Health, controlling a significant portion of the revenue. These incumbents leverage broad consumer ecosystems, healthcare partnerships, and cross-platform integration to strengthen adoption. They invest heavily in R&D to maintain technological leadership in AI-driven health analytics, remote monitoring, and personalized care solutions, while continuously enhancing interoperability and user engagement. Strategic platform expansions, device integration, and enterprise collaborations further reinforce their market position and competitive moat.

Regional and niche developers such as Health2Sync, OneStep, and Cope Notes focus on specialized applications such as chronic disease management, mental health support, and preventive care. Barriers, including data privacy regulations, clinical validation, and EHR integration complexity, limit new entrants, but cloud-based platforms and AI-enabled tools allow software-centric companies to compete. Market consolidation is expected to rise gradually as global leaders acquire smaller innovators, while partnerships and integration agreements continue to drive solution interoperability and geographic expansion.

Key Industry Developments

- In January 2026, Teladoc launched Wellbound, a mental health-centric employee assistance program, expanding its virtual care offerings for workplace wellness. The platform integrates teletherapy, coaching, and digital resources to proactively support employees. This reflects rising corporate adoption of mobile health solutions for mental and behavioral health. Wellbound strengthens Teladoc’s presence in preventive care and employee wellness markets.

- In October 2025, Samsung announced the acquisition of Xealth, to integrate consumer wearables with clinical workflows and EHR systems. Xealth’s platform connects with over 500 U.S. hospitals and 70+ digital health solutions, enabling doctors to prescribe apps and tools. This acquisition strengthens Samsung’s connected care ecosystem, emphasizing preventive and proactive care.

- In August 2025, Mountain View-based Twin Health secured US$ 53 million in Series E funding to scale its AI-driven “Whole-Body Digital Twin” platform for personalized metabolic care. The platform provides guidance on nutrition, sleep, and activity to reverse type 2 diabetes and obesity. With over US$ 250 million in total financing and a US$ 950 million valuation, this funding underscores investor confidence in AI-powered mobile health solutions.

Companies Covered in Mobile Health Apps and Solutions Market

- Apple Inc.

- Samsung Electronics

- Teladoc Health

- Fitbit

- Philips Healthcare

- Cerner Corporation

- Epic Systems

- MyFitnessPal

- Omada Health

- Practo

Frequently Asked Questions

The global mobile health apps and solutions market is projected to reach US$ 61.8 billion in 2026.

Increasing prevalence of chronic diseases, rising smartphone penetration, and growing adoption of telehealth and remote monitoring solutions are driving the market.

The market is poised to witness a CAGR of 13.5% from 2026 to 2033.

Widening acceptance of telehealth platforms in emerging ecomomies, integration with AI, wearables, and digital therapeutics, and employer-sponsored health programs are key opportunities.

Apple, Google, Samsung, Teladoc Health, Health2Sync, OneStep, Cope Notes are some of the key players in the market.