- Medical Devices

- Diagnostic Imaging Devices Market

Diagnostic Imaging Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Diagnostic Imaging Devices Market by Product Type (X-ray Equipment, Ultrasound Imaging Systems, Nuclear Imaging Systems, Magnetic Resonance Imaging (MRI), Computed Tomography (CT) Scanners, Others), by Application, by End-use, and Regional Analysis from 2026 to 2033

Diagnostic Imaging Devices Market Share and Trends Analysis

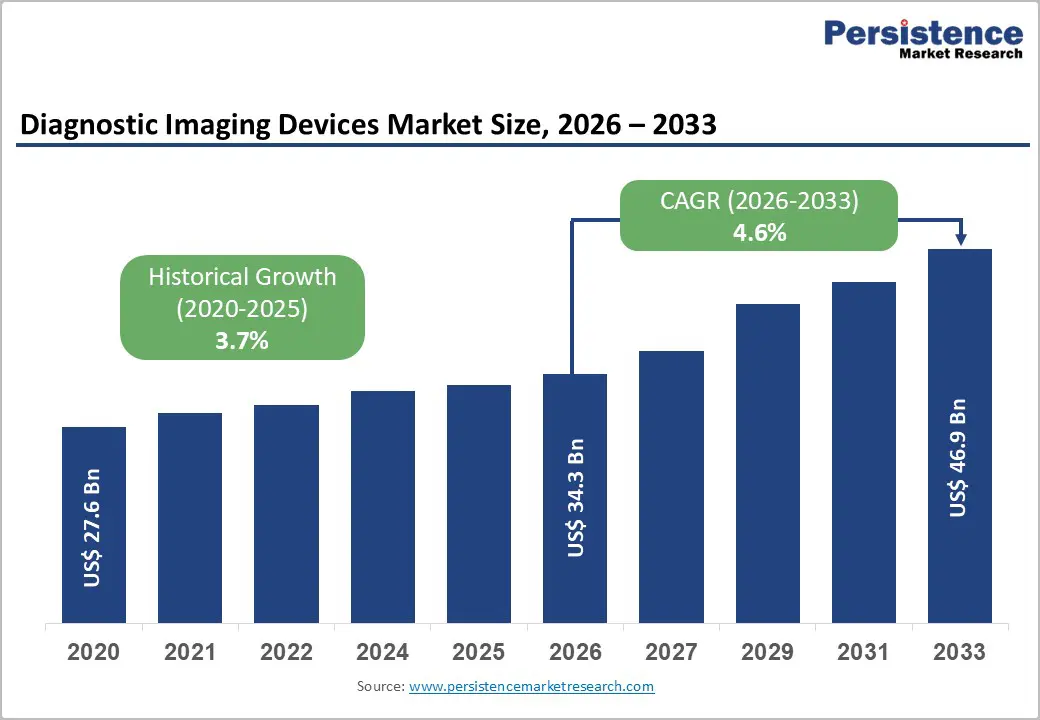

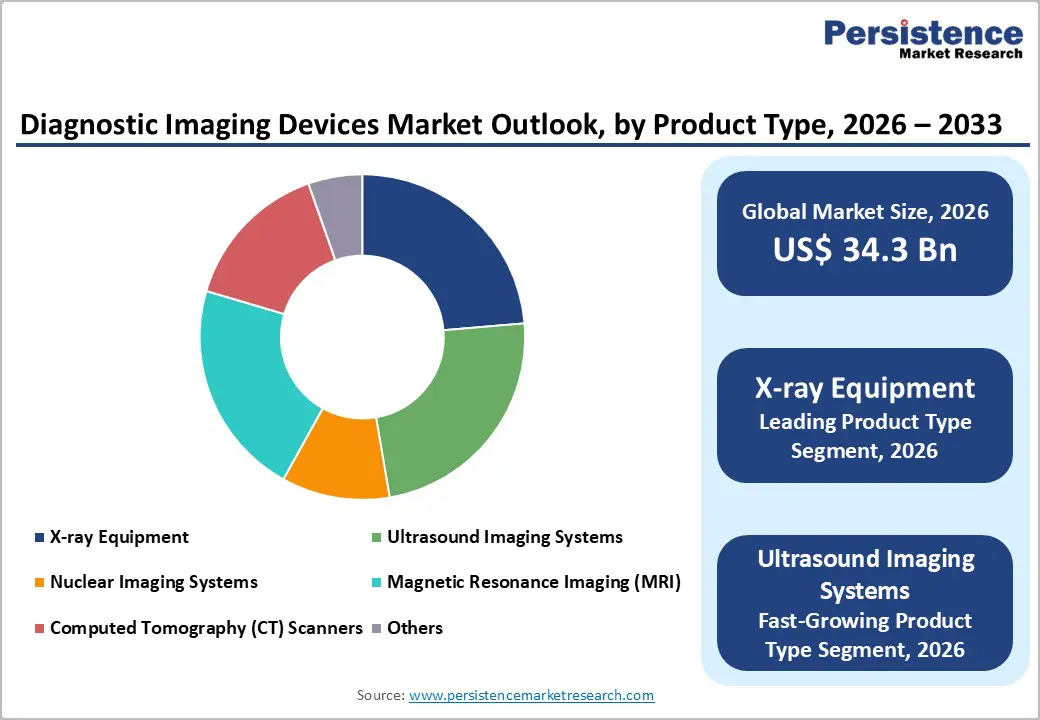

The global diagnostic imaging devices market size is expected to be valued at US$ 34.3 billion in 2026 and projected to reach US$ 46.9 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033.

Diagnostic imaging devices play a critical role in modern healthcare by enabling early, accurate disease detection and guiding treatment decisions. These devices include X-ray, ultrasound, CT, MRI, and nuclear imaging systems used across hospitals, diagnostic centers, and outpatient clinics. Market growth is driven by the rising burden of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions, along with a rapidly aging global population. More than 60% of clinical diagnoses rely on medical imaging, underscoring its essential role in patient care.

Key trends include increasing adoption of advanced imaging technologies and digital solutions. AI-enabled imaging is improving workflow efficiency and diagnostic accuracy, while portable and point-of-care imaging systems are expanding access in emergency and remote settings. CT and MRI demand continues to rise due to higher imaging volumes, while ultrasound remains the fastest-growing modality due to affordability and safety. Emerging economies are also witnessing strong growth supported by expanding healthcare infrastructure.

Key Industry Highlights:

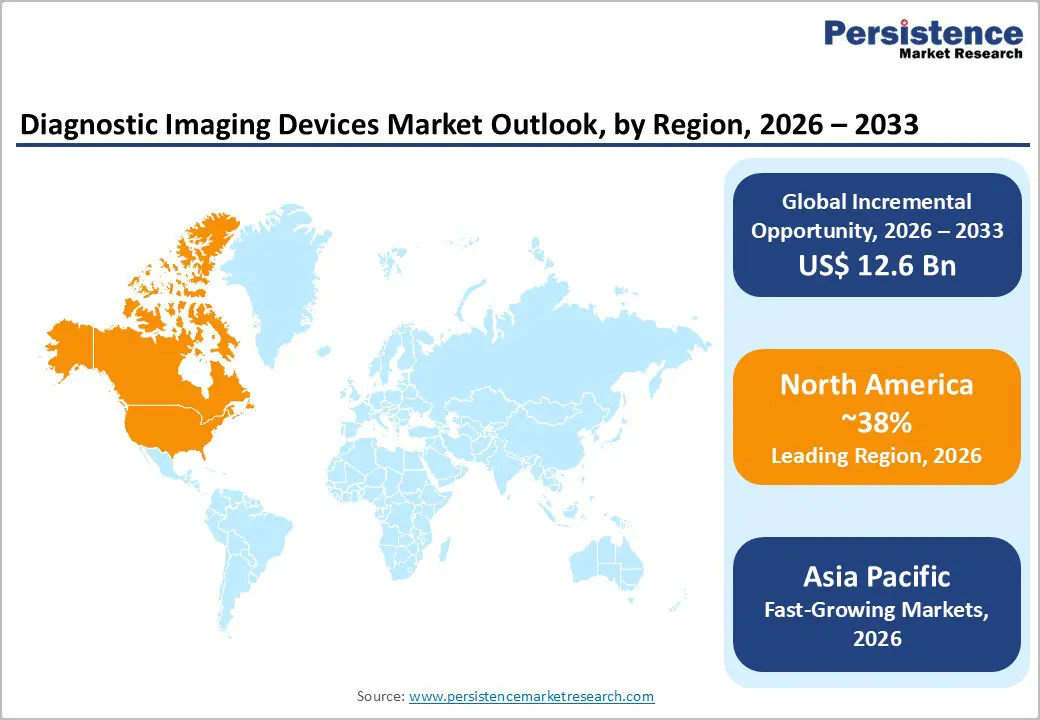

- Leading Region: North America dominates the global diagnostic imaging devices market, supported by advanced healthcare infrastructure, high imaging procedure volumes, and strong adoption of CT and MRI systems.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by expanding healthcare infrastructure, large patient populations, government investments, and rising demand for affordable diagnostic services.

- Dominant Segment: X-ray imaging systems remain the dominant product segment due to widespread availability, cost-effectiveness, and routine use in hospitals and diagnostic centers.

- Market Expansion: Emerging economies, particularly China, India, and Southeast Asia, are expected to drive market growth through increased hospital construction, expansion of diagnostic chains, and a rising focus on early disease detection.

| Key Insights | Details |

|---|---|

| Diagnostic Imaging Devices Market Size (2026E) | US$ 34.3 billion |

| Market Value Forecast (2033F) | US$ 46.9 billion |

| Projected Growth CAGR (2026 - 2033) | 4.6% |

| Historical Market Growth (2020 - 2025) | 3.7% |

Market Dynamics

Driver - Technological Advancements in Imaging Modalities to Enable Efficient and Cost-effective Diagnostics

Technological advancements in imaging modalities are transforming diagnostic imaging devices, enabling accurate, rapid, and cost-effective diagnosis across a range of medical conditions. Recent advancements in MRI technologies focus on enhancing image resolution and decreasing scanning times. MRI is estimated to hold a share of 28.2% for efficient and accurate diagnosing.

High-field MRI scanners, such as 7T MRI, offer ultra-high-resolution images with high detail, which is especially useful for detecting small lesions, neurological disorders, and tumors. Advances in computed tomography technology focus on reducing radiation exposure while enhancing image quality and scan speed. New dual-energy CT and high-definition CT scanners enable swift and detailed imaging with lower radiation doses, which is especially important for pediatric and sensitive patient groups. Iterative reconstruction algorithms decrease the radiation dose needed for CT scans while maintaining superior image quality.

Diversification of Imaging Applications to Boost Expansion

Diagnostic imaging solutions are no longer limited to conventional applications; they are increasingly used across a diverse range of medical conditions and specialties. According to the World Health Organization (WHO), cancer is the second leading cause of death worldwide.

As the global incidence of cancer continues to rise, the demand for advanced imaging technologies to detect, diagnose, and monitor cancer is growing. By 2040, the number of cancer cases globally is estimated to reach 29.5 million. Diagnostic imaging techniques such as MRI, PET-CT, and mammography are vital for early cancer detection, staging, and monitoring of treatment response. A WHO report states that cardiovascular diseases accounted for 17.9 million deaths globally, thereby representing 31% of all global deaths in the past few years. Advances in cardiovascular imaging have substantially improved the diagnosis and management of heart diseases. CT Angiography has become a standard imaging technique for evaluating blood vessels, specifically in patients with suspected coronary artery disease.

Diagnostic imaging devices are increasingly used in dental and veterinary imaging. 3D imaging and cone beam CT (CBCT) are a significant growth area in dental imaging applications. Advanced technologies such as MRI, CT scans, and ultrasound are used to diagnose animals, particularly pets and livestock.

Restraints - Shortage of Skilled Professionals to Emerge as a Critical Challenge

A shortage of skilled professionals, particularly radiologists and imaging technicians, is a critical challenge for the industry. This shortage not only limits the use of advanced imaging technologies but also delays diagnosis and treatment, thereby adversely affecting patient outcomes. A 2023 survey conducted by the Royal College of Radiologists (RCR) found a 34% shortfall of radiologists in the U.K., with an estimated 2,000 additional radiologists required to meet current demand. This shortage results in patients experiencing delays in obtaining diagnostic imaging results.

For instance, almost 75% of radiology departments in the U.K. reported delays exceeding one month for routine imaging procedures. The American College of Radiology (ACR) highlighted that radiologists are overburdened, with a few handling double the recommended caseload to meet rising demand, resulting in a high rate of errors and burnout.

The WHO noted a shortage of technicians, particularly in low- and middle-income countries. In high-income countries like the U.S., imaging technicians face high turnover rates owing to workload pressures and insufficient pay. A survey by the Bureau of Labor Statistics in 2022 noted a 7% decline in the number of new graduates entering imaging technician workforce compared to a decade ago.

Opportunity - Integration of Imaging Devices with IT Solutions

The integration of diagnostic imaging devices with IT solutions is a transformative trend revolutionizing the healthcare sector. This integration helps in improving efficiency, accuracy, and accessibility of diagnostic imaging by enabling seamless data management, supporting advanced analytics, and facilitating real-time sharing.

The increasing need for rapid and accurate diagnostics, along with the shift toward value-based care, is essential to enhancing healthcare delivery. Picture Archiving and Communication Systems (PACS) is one of the most significant IT integrations in diagnostic imaging as they store, retrieve, manage, and share medical images electronically.

Use of PACS enhances efficiency by minimizing the time spent on retrieving images and decreasing costs related to storing physical films. Integration of imaging devices with Electronic Health Records (EHRs) enables real-time sharing of imaging results with other patient health data.

Sustainability and Eco-friendly Innovations to Benefit Healthcare Providers

Growth in environmental concerns has led healthcare systems to strive to decrease their carbon footprints, thereby increasing their focus on sustainability and eco-friendly innovations. Companies are adapting to regulatory pressures and market demands by creating energy-efficient and environmentally responsible imaging solutions. These innovations contribute to global sustainability goals while benefiting healthcare providers by reducing operational costs, increasing the efficiency of diagnostic procedures, and enhancing patient safety.

Companies are reducing energy consumption by developing energy-efficient models that use less power and operate more efficiently. For instance, GE Healthcare introduced an energy-efficient MRI scanner that decreases energy consumption by 40% compared to previous models. Philips also launched energy-efficient versions of their MRI and CT machines with a few systems using 30% less energy compared to old versions.

The broad trend toward sustainability has led diagnostic imaging companies to incorporate recyclable materials in their devices while decreasing the use of hazardous substances. According to Siemens Healthineers, approximately 70% of the materials used in its imaging devices are recyclable. Canon Medical Systems has implemented water-saving technologies in its manufacturing processes, including water-recycling systems that reduce water consumption by 40%.

Category-wise Analysis

Product Type Insights

Diagnostic imaging devices are broadly categorized into X-ray systems, ultrasound imaging systems, computed tomography (CT) scanners, magnetic resonance imaging (MRI) systems, nuclear imaging systems, and other emerging modalities. X-ray equipment continues to account for the largest share of the market due to its wide availability, lower cost, and routine use in trauma, orthopedic, dental, and chest examinations. Ultrasound systems constitute a rapidly expanding segment, owing to their non-ionizing nature, real-time imaging capability, and increasing use in point-of-care and obstetric applications. CT scanners remain in high demand in emergency care, oncology, and cardiovascular diagnostics, where rapid and detailed imaging is critical. MRI systems, although capital-intensive, are widely adopted for neurological, musculoskeletal, and soft-tissue imaging owing to their superior image quality. Nuclear imaging systems hold a smaller but important share, particularly in oncology and cardiology, for functional and metabolic assessments. Continuous technology upgrades, including digital detectors, hybrid imaging, and workflow optimization, are shaping adoption patterns across all product categories.

End-user Insights

Hospitals and clinics represent the largest end-use segment in the diagnostic imaging devices market, driven by high patient volumes, emergency care requirements, and the availability of advanced imaging infrastructure. These facilities routinely utilize X-ray, CT, MRI, and ultrasound systems for diagnosis, treatment planning, and patient monitoring across multiple specialties. Diagnostic centers form the second major segment, benefiting from the growing preference for specialized, outpatient imaging services that offer faster turnaround times and cost efficiency. The expansion of standalone diagnostic chains and imaging networks has strengthened demand in this segment. Research institutes account for a smaller but strategic share, using advanced imaging technologies for clinical trials, disease research, and technology development. Ongoing investments in academic and medical research support the steady adoption of this category. Other end-userrs, including mobile imaging units and veterinary facilities, contribute modestly to overall demand. The growing shift toward outpatient diagnostics and decentralized healthcare delivery continues to influence end-use dynamics across regions.

Regional Insights

North America Diagnostic Imaging Devices Market Trends

North America holds a leading position in the global diagnostic imaging devices market, driven by advanced healthcare infrastructure, high healthcare spending, and early adoption of innovative technologies. The United States dominates the region due to high volumes of imaging procedures and strong demand for early disease detection in cancer, cardiovascular, and neurological disorders. Hospitals and diagnostic centers continue to invest in advanced CT and MRI systems to improve diagnostic accuracy and workflow efficiency. Favorable reimbursement policies and widespread insurance coverage support patient access to imaging services.

The region is also witnessing rapid integration of artificial intelligence in imaging software to enhance image interpretation, reduce reading time, and support radiologists. Growing use of portable and point-of-care imaging devices in emergency departments and outpatient settings is another key trend. Additionally, replacement of aging imaging equipment with digitally advanced systems is sustaining demand. Canada contributes steadily through public healthcare investments and the modernization of hospital imaging facilities, reinforcing regional market strength.

Asia Pacific Diagnostic Imaging Devices Market Trends

Asia Pacific is the fastest-growing region in the diagnostic imaging devices market, supported by expanding healthcare infrastructure, rising disease burden, and increasing access to diagnostic services. Countries such as China, India, Japan, and South Korea are witnessing strong growth due to large patient populations and rising incidence of chronic diseases. Government initiatives to improve healthcare access and diagnostic capacity are driving installations of X-ray, ultrasound, and CT systems, particularly in public hospitals. Ultrasound imaging is gaining strong traction due to its affordability and suitability for rural and semi-urban healthcare settings. Rapid urbanization and the growth of private diagnostic centers are further supporting market expansion. Technological advancements and local manufacturing are helping reduce equipment costs, improving adoption rates. Japan remains a key market for high-end MRI and CT systems, while India and Southeast Asia are experiencing rising demand for mid-range and portable imaging devices. These factors position the Asia Pacific as a major growth engine for the global market.

Competitive Landscape

The companies are continuously investing in the development of modern technologies like AI-powered imaging, 3D imaging, and enhance MRI or CT scanners. Investment is made to provide precise diagnostics, efficient processing, and improved patient outcomes. Portable ultrasound devices, handheld imaging solutions, and small equipment for point-of-care diagnostics are gaining traction as companies are looking to cater to developing markets and hospitals having limited space. Leading companies in the diagnostic imaging space market usually acquire small and innovative firms to gain access to new technologies to expand their product portfolios. Businesses are progressively partnering with hospitals, clinics, and research institutions to understand the requirements of their target audience and enhance their product design while boosting product adoption.

Key Industry Developments:

- In October 2024, GE Healthcare, headquartered in Illinois, launched a new Versana Premier™, a versatile ultrasound system. This system offers automation and AI-enabled productivity tools to improve workflow across diverse clinical specialties and care areas, including general practice, OBGYN, musculoskeletal (MSK), and cardiology.

- In October 2024, Ontario-based Arrayus Technologies Inc. received Health Canada's approval for its MRI-guided focused ultrasound system for the ablation of uterine fibroid tissue.

- In September 2024, Samsung Medison, based in Seoul, acquired Sonio SAS, a fetal ultrasound AI software company.

- In July 2024, Philips India partnered with Star Imaging to launch the first MRI training school in India to provide international standard training on MRI technologies across 17 sub-specialties

- In March 2024, Amsterdam-based Philips collaborated with Synthetic MR to develop AI-driven quantitative brain imaging tools. The tool will help diagnose disorders such as multiple sclerosis (MS), traumatic brain injury, and dementia.

Companies Covered in Diagnostic Imaging Devices Market

- General Electric Company

- Hitachi Ltd.

- Hologic, Inc.

- Koninklijke Philips N.V.

- Samsung Medison Co., Ltd.

- Shimadzu Medical Pvt. Ltd.

- CANON MEDICAL SYSTEM CORPORATION

- ESAOTE SPA

- Allengers

- Siemens Healthcare Private Limited

- Neusoft Corporation

- NP JSC AMICO

- Shanghai Lianying Medical Technology Co., Ltd.

- FUJIFILM Corporation

- Others

Frequently Asked Questions

The global diagnostic imaging devices market is projected to be valued at US$ 34.3 Bn in 2026.

Rising chronic diseases, aging population, increasing diagnostic accuracy demand, technological advancements, early disease detection, and expanding hospital infrastructure worldwide.

The global market is poised to witness a CAGR of 4.6% between 2026 and 2033.

AI-enabled imaging, portable and point-of-care systems, emerging market expansion, hybrid imaging technologies, and growing outpatient diagnostic centers.

General Electric Company, Hitachi Ltd., and Hologic, Inc. are the leading companies in the market.