- Biotechnology

- Digital PCR Market

Digital PCR Market Size, Share, and Growth Forecast 2026 - 2033

Digital PCR Market by Product Type (Instrument, Consumables, Services), by Application (Clinical Diagnostics, Basic Research, Applied Research, Forensic Testing), by End User (Pharmaceutical Companies, Research Institutes, Forensic Labs, Agriculture Companies), by Regional Analysis, 2026 - 2033

Digital PCR Market Size and Trend Analysis

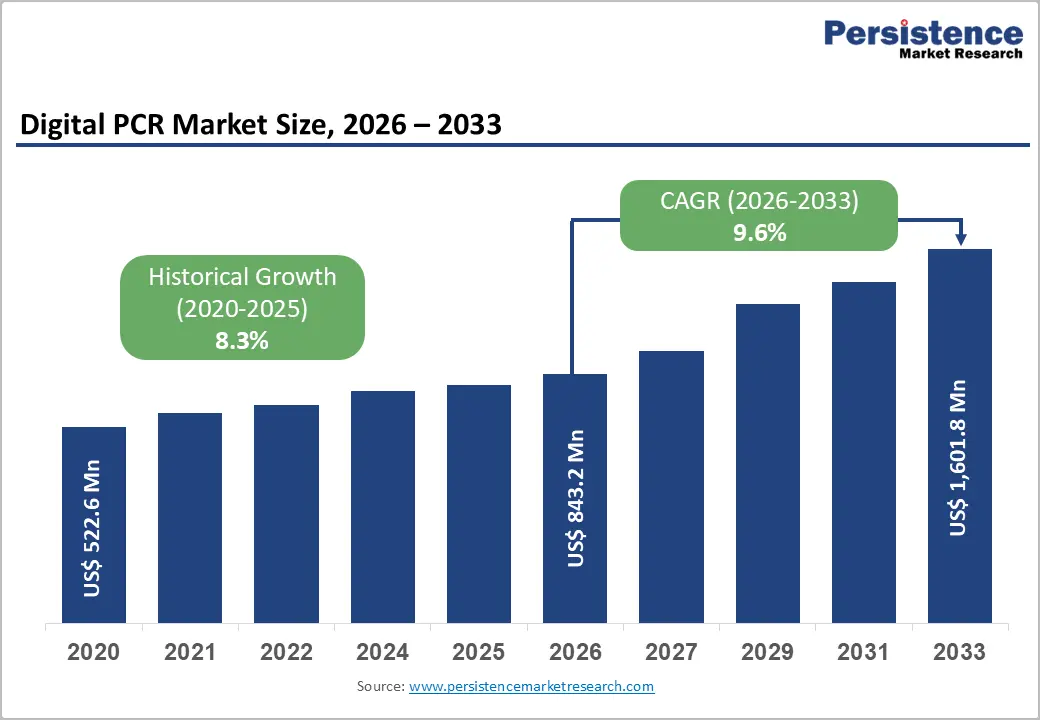

The global Digital PCR Market size is expected to be valued at US$ 843.2 million in 2026 and projected to reach US$ 1,601.8 million by 2033, growing at a CAGR of 9.6% between 2026 and 2033.

Rising demand for precise nucleic acid quantification in oncology, infectious disease monitoring, and genetic research drives this expansion, supported by advancements in droplet digital PCR technology that offer absolute quantification without standards. Increasing adoption in pharmaceutical R&D for gene therapy validation and clinical diagnostics for rare mutation detection further accelerates growth, as evidenced by expanding use in precision medicine initiatives.

Key Market highlights

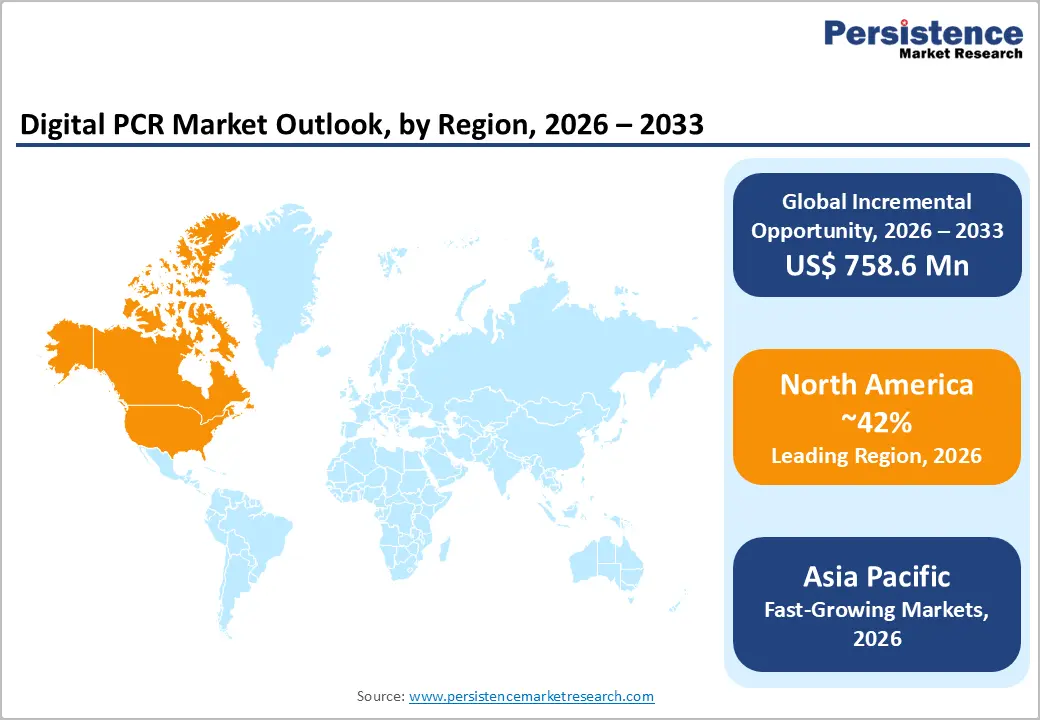

- North America leads Digital PCR with 42% share in 2025, driven by U.S. FDA approvals and biotech innovation hubs fueling diagnostics growth.

- Asia Pacific fastest-growing region at highest CAGR 2025-2032, propelled by China-India genomics investments and manufacturing scale.

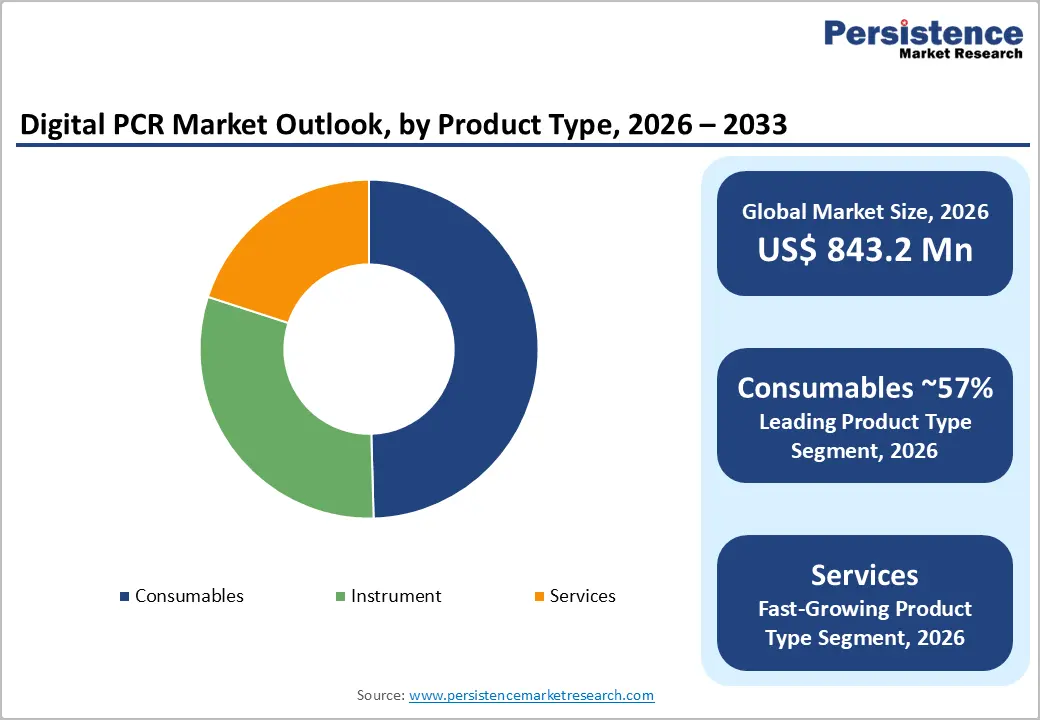

- Consumables dominate product type with 57% share, essential for recurring high-throughput assays in pharma R&D.

- Services emerge fastest-growing product segment, as labs outsource complex validation workflows.

- Key opportunity in gene-cell therapy expansion, with digital PCR enabling precise AAV titering amid 3,000+ global trials.

| Key Insights | Details |

|---|---|

|

Digital PCR Size (2026E) |

US$ 843.2 million |

|

Market Value Forecast (2033F) |

US$ 1,601.8 million |

|

Projected Growth CAGR (2026-2033) |

9.6% |

|

Historical Market Growth (2020-2025) |

8.3% |

Market Dynamics

Driver - Advancements in Precision Diagnostics

Technological advancements in digital PCR (dPCR) are driving significant growth in the market by enabling highly precise and sensitive molecular diagnostics. Innovations such as droplet-based partitioning allow absolute quantification of target DNA, achieving detection limits as low as 0.001%. This capability is particularly critical for liquid biopsy applications in oncology, where rare mutations must be accurately identified for personalized treatment decisions. Since 2020, over 20 FDA-approved companion diagnostic assays have incorporated dPCR for oncology and infectious disease applications, highlighting regulatory validation and clinical adoption. High reproducibility, often exceeding 99%, reduces false negatives and builds confidence among clinical laboratories, increasing routine implementation for both research and diagnostic workflows.

The rising global burden of infectious diseases further amplifies the demand for dPCR solutions. Post-COVID surveillance and recurrent viral outbreaks require accurate viral load monitoring to guide treatment and public health interventions. WHO reports indicate over 1.8 billion individuals are affected annually by respiratory infections, creating a critical need for inhibitor-tolerant assays. dPCR’s resilience to PCR inhibitors, which are present in 30–40% of clinical samples, ensures reliable testing in complex matrices such as saliva and wastewater. Pharmaceutical companies also utilize dPCR in vaccine efficacy trials, enhancing adoption and expanding market pull through validated, reproducible protocols.

Restraint - High Instrument Costs

High instrument costs remain a key restraint for the digital PCR market. Individual systems often exceed US$ 100,000, and additional maintenance, calibration, and operator training can add 20–30% to annual expenditures. Such capital intensity limits accessibility for smaller laboratories, especially in emerging regions, where cost-effective alternatives like qPCR are sufficient for routine testing. Furthermore, technical complexity including droplet generation, multi-step workflows, and thermal cycling requirements raise operational challenges. Variability and coalescence errors affecting 5–10% of partitions necessitate specialized personnel, increasing error risk and reducing scalability. These factors collectively slow market penetration despite the superior analytical performance of dPCR.

Technical Complexity

A significant restraint in the digital PCR (dPCR) market is the inherent technical complexity of the technology. Droplet generation and reading involve multi-step workflows that are prone to variability, with coalescence errors impacting 5–10% of partitions, potentially affecting result accuracy. Thermal cycling requirements add further challenges, as specialized laboratory space and controlled environments are necessary, making integration into standard clinical or research labs difficult. These complexities increase the risk of procedural errors and necessitate highly trained personnel to manage experiments effectively. Small or resource-limited laboratories may struggle to implement dPCR, slowing adoption. Despite its superior sensitivity and precision compared to conventional PCR, the operational challenges and intensive training requirements hinder scalability and limit the technology’s accessibility in emerging and mid-tier markets.

Opportunity - Expansion in Gene and Cell Therapy

The global expansion of gene and cell therapy presents a major opportunity for the digital PCR (dPCR) market. Over 3,000 clinical trials are ongoing worldwide, according to NIH data, necessitating precise vector titering, residual DNA detection, and accurate lot-release testing to meet FDA guidelines. Digital PCR provides a broad dynamic range, enabling reliable quantification across multiple orders of magnitude, which is critical for viral vector-based therapies such as AAV and lentiviral platforms. The Alliance for Regenerative Medicine projects approximately 20% annual growth in therapies requiring such assays, highlighting a rapidly increasing demand. Companies focusing on AAV capsid quantification and genome editing validation can capitalize on multi-billion-dollar revenue potential, as pharmaceutical and biotech firms increasingly integrate dPCR into gene therapy development and regulatory compliance workflows.

Emerging Markets in Oncology Research

Rising cancer incidence in Asia Pacific, with nearly 10 million new cases annually according to WHO, is driving the adoption of digital PCR for oncology research and early screening. dPCR enables low-level circulating tumor DNA (ctDNA) detection, providing high sensitivity for minimal residual disease monitoring and early diagnosis. Studies report 95% concordance with next-generation sequencing at a fraction of the cost, making dPCR an attractive alternative for research and clinical labs. Policy initiatives, such as India’s US$ 75 million genomics mission, further support molecular diagnostics infrastructure, funding the acquisition of dPCR systems in academic and clinical institutions. Growing awareness of precision oncology, combined with increasing investments in research and screening programs across emerging markets, positions the Asia Pacific region as a key growth opportunity for digital PCR adoption.

Category-wise Insights

Product Type Analysis

Consumables are the largest product segment in the digital PCR market, accounting for approximately 57% of global revenue in 2025. Their dominance is driven by the recurring demand for partition kits, reagents, and specialized droplet-stabilizing solutions in high-throughput laboratories. These consumables are critical for ensuring reproducibility and accuracy, as most assays require validated kits for every run, leaving little room for generic alternatives. Oncology-focused workflows particularly contribute to consistent consumption, with laboratories processing over 100 samples weekly for cancer panels.

The steady usage of consumables across research and clinical settings, combined with their non-substitutable nature, ensures continuous revenue generation. Additionally, pharmaceutical companies, diagnostic laboratories, and academic research centers maintain bulk inventories to support uninterrupted experimental pipelines. As dPCR adoption grows in precision medicine, infectious disease monitoring, and viral quantification, the consumables segment continues to benefit from both volume and regulatory compliance requirements, reinforcing its leading position over instruments and services in the market.

Application Analysis

Clinical diagnostics represents the leading application segment in the digital PCR market, capturing the largest share in 2025. Its prominence is fueled by superior sensitivity, accuracy, and reproducibility, making dPCR ideal for pathogen quantification, oncology panels, and prenatal screening. FDA-cleared assays enable detection of ultra-low viral loads in newborn screening and oncology monitoring, with reproducibility exceeding 99%, outperforming traditional qPCR methods. Infectious disease testing also contributes significantly, accounting for roughly 40% of the sub-segment share, supported by post-pandemic surveillance and ongoing monitoring of emerging pathogens.

Oncology applications benefit from high-throughput lab integration, allowing simultaneous testing of multiple gene targets in tumor profiling and minimal residual disease detection. The segment’s growth is further reinforced by stringent regulatory requirements, including validated assay workflows, and the rising adoption of molecular diagnostics in hospitals and reference laboratories. Overall, clinical diagnostics continues to dominate due to its broad applicability, regulatory acceptance, and ability to address unmet needs in precision medicine and public health.

Regional Insights

North America Digital PCR Market Trends and Insights

North America is the leading market for digital PCR (dPCR), holding an estimated 42% of the global share in 2025. The United States drives this dominance, supported by extensive investments in precision medicine and genomics research. Regulatory approvals, including FDA clearance of over 20 dPCR assays since 2020, have enabled widespread use in oncology, particularly for liquid biopsy applications. Funding from institutions such as the NIH has strengthened genomic centers, while advanced laboratory infrastructure and established biotech hubs in Boston and San Francisco have facilitated integration of dPCR into companion diagnostics.

Public-private partnerships foster innovation, accelerating technology adoption across hospitals and research institutions. High revenue contributions reflect both clinical and research demand, with strong engagement from pharmaceutical and biotech companies developing targeted therapies. Continuous expansion of diagnostic services, combined with skilled personnel and robust supply chains, ensures sustained market leadership and positions North America as the most influential region in the global dPCR landscape.

Asia Pacific Digital PCR Market Trends and Insights

Asia Pacific is the fastest-growing regional market for digital PCR, driven by rising healthcare infrastructure, biotechnology research, and governmental initiatives across China, India, Japan, and ASEAN countries. China leads with significant local manufacturing of droplet-based dPCR systems, reducing costs and enhancing accessibility for clinical and research applications. India’s national genomics mission supports affordable testing, expanding adoption across hospitals and diagnostic laboratories. Japan demonstrates strong demand in oncology assays, complemented by growing use in infectious disease monitoring, contributing to an estimated 11% regional CAGR.

South Korea benefits from lower production costs, enabling competitive exports of dPCR systems and reagents. Emerging markets within Southeast Asia are increasingly incorporating dPCR for molecular diagnostics and precision medicine, supported by strategic investments and partnerships. Overall, the combination of cost-effective manufacturing, rising disease burden, government-backed genomics initiatives, and growing research funding drives rapid market expansion, positioning Asia Pacific as the key growth engine for digital PCR globally.

Competitive Landscape

The Digital PCR market remains moderately consolidated, with top players like Bio-Rad Laboratories and Thermo Fisher Scientific holding over 50% share through innovation and acquisitions. Leaders pursue R&D for multi-target panels and AI analytics, differentiating via workflow automation. Expansion strategies include partnerships for gene therapy kits; emerging models emphasize SaaS software for data analysis, reducing hardware dependency.

Key Market Developments

- In February 2025: Bio-Rad Laboratories announced acquisition of Stilla Technologies to enhance droplet digital PCR capabilities for rare mutation detection.

- In January 2025: QIAGEN expanded QIAcuity system for two-fold more targets, boosting infectious disease and oncology applications.

- In June 2024: Thermo Fisher Scientific acquired Combinati for high-resolution counting tech integration.

Companies Covered in Digital PCR Market

- Bio-Rad Laboratories, Inc.

- Thermo Fisher Scientific Inc.

- Fluidigm Corp.

- Formulatrix, Inc.

- JN Medsys.

- STILLA TECHNOLOGIES

- Avance Bioscience

- Fluidgm corporation,

- jn medsys

- Merck KGAA

- Precigenome LLC

- QIAGEN N.V

- Sysmex corporation

- Others

Frequently Asked Questions

The global Digital PCR Market is expected to reach US$ 843.2 million in 2026.

Advancements in precision diagnostics for oncology and infectious diseases drive demand, with digital PCR offering superior rare mutation detection.

North America leads with 42% share in 2025, supported by U.S. regulatory approvals and innovation.

Expansion in gene and cell therapy validation, meeting FDA needs for precise nucleic acid quantification in growing pipelines.

Leading players include Bio-Rad Laboratories, Thermo Fisher Scientific, and QIAGEN, driving innovation through acquisitions and product launches.