- Media & Entertainment

- Digital Commerce Applications Market

Digital Commerce Applications Market Size, Share, and Growth Forecast, 2026 - 2033

Digital Commerce Applications Market by Solution Type (Online Storefront / eCommerce Platform, Mobile Commerce Application, Marketplace Solutions, Digital Payments Integration, Order Management (OMS), Customer Experience & Personalization, Security & Fraud Prevention, Misc.), Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)), Deployment Mode (Cloud, On-Premises, Hybrid), End Use Industry (Retail & eTail, Consumer Goods, BFSI, Telecom & IT Services, Healthcare & Pharmaceuticals, Manufacturing, Misc.) and Regional Analysis for 2026 - 2033

Digital Commerce Applications Market Size and Trends Analysis

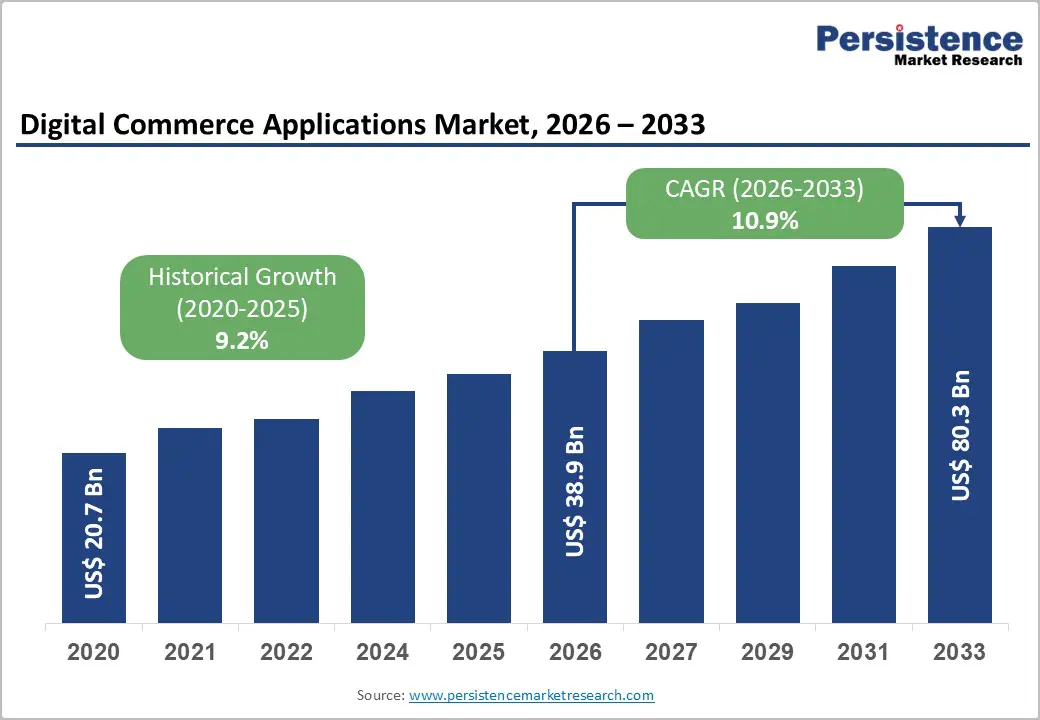

The Global Digital Commerce Applications Market size was valued at US$ 38.9 Billion in 2026 and is projected to reach US$ 80.3 Billion by 2033, growing at a CAGR of 10.9% between 2026 and 2033. Market expansion is driven by the accelerating adoption of mobile commerce, with smartphone penetration expected to reach 7.7 billion users by 2027. Artificial intelligence-powered personalisation engines are projected to deliver a 35 per cent sales attribution contribution, and cloud-based platform standardisation is enabling enterprise omnichannel integration.

Online storefront platforms maintain market leadership through diversified vertical deployment, while mobile commerce applications demonstrate the fastest segment growth driven by mobile Black Friday participation. The convergence of real-time AI personalisation, social commerce integration with livestream shopping, generating USD 480 billion in China, and SME digitalisation through open commerce networks establishes sustained market momentum throughout the forecast period.

Key Industry Highlights:

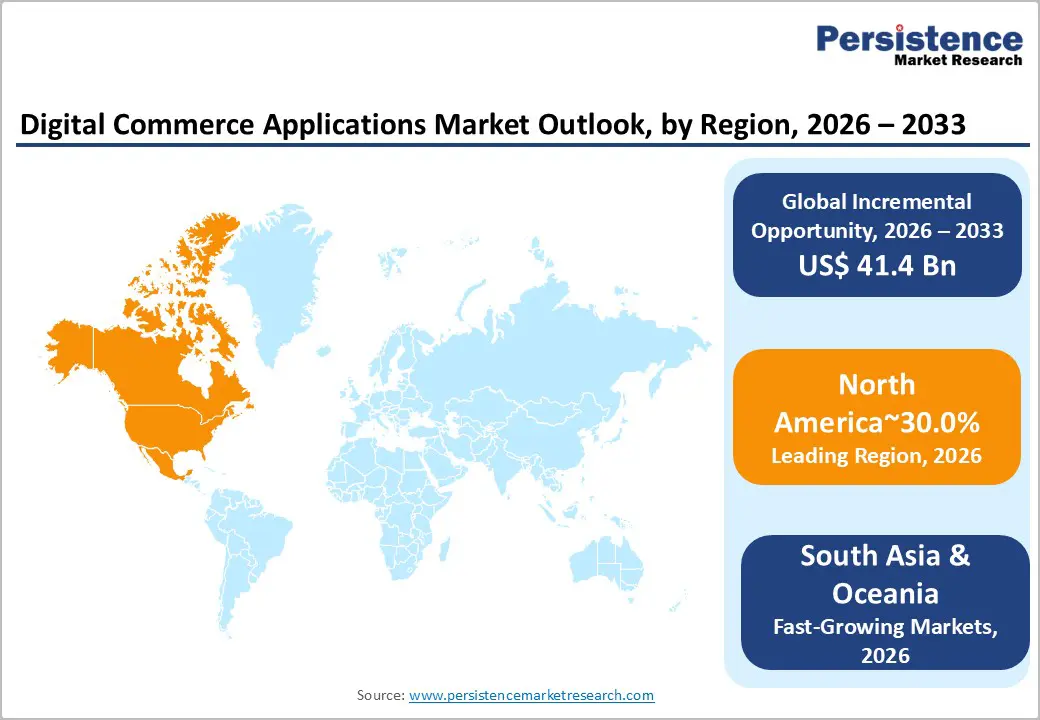

- Regional Leadership: East Asia holds the global Digital Commerce Applications Market with 25% share, driven by China’s advanced commerce infrastructure, mobile-first consumer adoption, and social commerce sophistication, including livestream shopping.

- Strong North American Presence: North America accounts for 30% of the market, supported by mature digital infrastructure, AI-powered personalisation, high mobile commerce adoption, and SME digitalisation initiatives.

- Significant European Market: Europe holds 22% share, fueled by GDPR-driven privacy standards, advanced BFSI sector engagement, AI-enabled personalisation adoption, and strong omnichannel retail integration.

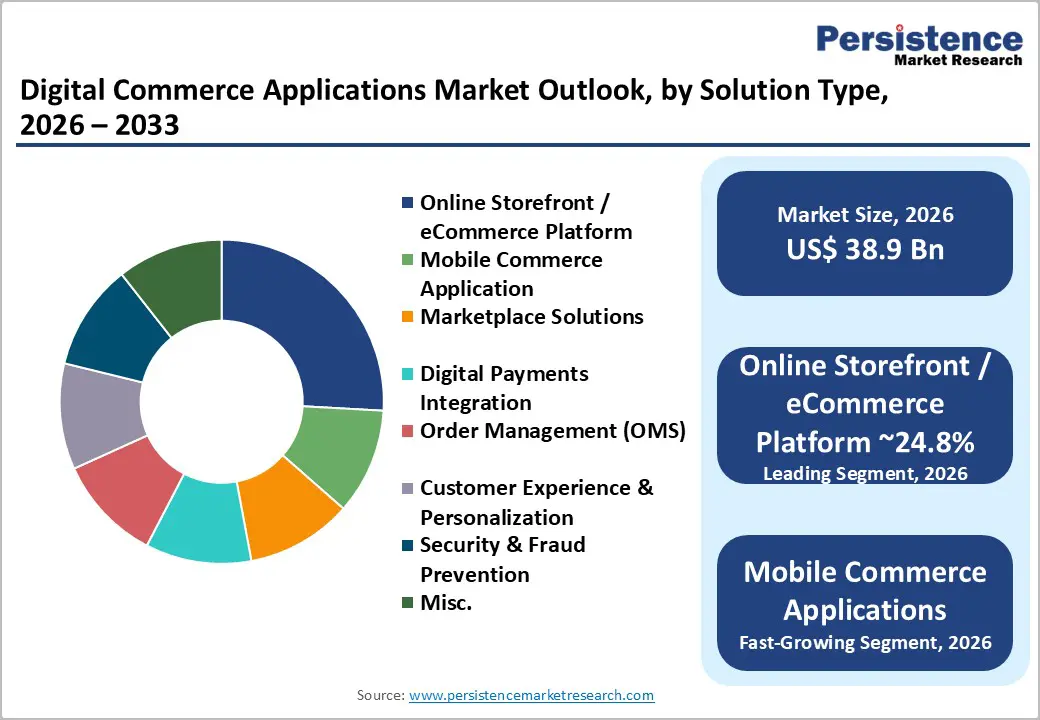

- Leading Solution Segment: Online storefront platforms dominate with around 24.8% share, benefiting from technology maturity, omnichannel capability, established payment integrations, and broad merchant accessibility.

- Leading End-Use Industry: Retail and e-tail sectors command 35.7% market share, supported by digitised product catalogues, omnipresent e-commerce platforms, and integrated online-offline shopping experiences.

| Key Insights | Details |

|---|---|

|

Digital Commerce Applications Market Size (2026E) |

US$ 38.9 Bn |

|

Market Value Forecast (2033F) |

US$ 80.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.9% |

Market Dynamics

Growth Drivers

Mobile-First Consumer Commerce Adoption and Smartphone Ubiquity

Global smartphone proliferation establishes a fundamental catalyst for digital commerce transformation, with connected device penetration exceeding 6.9 billion units in 2023 and projected expansion to 7.7 billion by 2027. Digital Commerce Applications Market demonstrates a responsive growth trajectory aligned with mobile device accessibility, enabling consumers to execute transactions independent of geographic or temporal constraints. Southeast Asian smartphone adoption surpassing 75 percent in 2023 correlates directly with 34 percent year-over-year mobile-first retail transaction acceleration, exemplifying emerging market commercial behavior transformation. 5G network expansion, enabling richer commerce experiences with global 5G coverage reaching 35 percent population penetration, supports advanced multimedia shopping capabilities, including livestream commerce and augmented reality product visualisation.

China's livestream shopping phenomenon, generating USD 480 billion during the 2023 Singles' Day event, exemplifies commercial infrastructure maturation supporting advanced mobile commerce experiences. India's Unified Payments Interface is processing 10 billion monthly transactions, demonstrating policy-driven ecosystem impact, establishing payment infrastructure standardization supporting mobile transaction accessibility.

Mobile device optimisation reduces cart abandonment through biometric authentication and one-click checkout features, establishing friction reduction supporting transaction completion. Mobile commerce revenue share projected to reach 63 percent by 2028 compared to 43 percent in 2018, demonstrating structural commerce channel reallocation. Black Friday data indicates 69 percent mobile transaction participation confirms mobile-first shopping dominance.

SME Digitalisation and Open Commerce Network Standardisation

AI-driven personalised engines are establishing competitive differentiation through customer data analytics, enabling hyper-targeted product recommendations with documented conversion improvement of 30-35 percent relative to non-personalised experiences. Amazon's attribution model demonstrates 35 percent total sales revenue generation through AI-powered recommendation engines exemplifies platform-level personalization impact quantification.

The Market benefits directly from machine learning algorithm advancement, enabling real-time customer behaviour analysis, supporting dynamic pricing optimisation, automated cross-selling protocols, and personalised marketing message delivery. Natural language processing capability enhancement, enabling chatbot sophistication improvement, supporting customer support automation and conversational commerce interaction. Epsilon consumer research indicates 80 percent customer purchase propensity enhancement when brands implement personalised experiences and establish quantifiable behavioural modification through algorithmic targeting.

Predictive personalisation capability advancement enabling anticipatory product recommendations addressing customer needs before explicit articulation. Hyper-personalisation technology maturation supporting comprehensive customer journey touchpoint optimisation through emotional cue analysis and behavioural context integration. Real-time data adaptation supporting continuous AI model refinement, responding to preference fluctuation and seasonal trend variation.

Market Restraining Factors

Cybersecurity Vulnerabilities and Digital Payment Fraud Risk Management Complexity

Advanced cyber threat sophistication targeting commerce application infrastructure creates elevated operational risk exposure requiring substantial security investment deployment. Payment card industry compliance complexity and multi-jurisdictional regulatory requirement harmonisation establish an operational burden constraining smaller platform providers. Data breach incident propagates across interconnected commerce ecosystems, creating systemic risk exposure throughout the supply chain network. Customer confidence erosion following security incidents establishes demand destruction, impacting platform adoption trajectory and transaction value generation.

Regulatory Fragmentation and Data Privacy Compliance Burden

GDPR, CCPA, and emerging jurisdictional data protection frameworks are establishing variable compliance requirement complexity across geographic markets. The absence of regulatory harmonisation across APAC, North America, and Europe is creating operational complexity and compliance cost multiplication. Privacy-first architecture implementation demands establishing development resource requirements and platform re-architecture necessity. Cross-border commerce regulatory uncertainty is limiting multinational enterprise market expansion strategy and platform interoperability capability.

Key Market Opportunities

Social Commerce Integration and Influencer-Led Direct-to-Consumer Channel Expansion

Social media platform commerce integration is establishing hybrid entertainment-transactional spaces, transforming consumer shopping behaviour and discovery patterns. Shoppable Instagram features enabling passive content consumption conversion to active purchasing, driving 130 percent year-over-year social-driven mobile transaction acceleration. TikTok LIVE Shopping events demonstrate a 4x conversion rate superiority relative to traditional e-commerce interfaces, establishing social commerce commercial viability validation. Short-form video content influences 39 percent unplanned purchase decisions through emotional engagement and scarcity marketing mechanisms.

Augmented reality integration within social platforms, enabling virtual product trials, reducing return rates and fraud susceptibility through experiential commerce. Snapchat AR lenses are achieving 26 percent return rate reduction for apparel through virtual fitting capability, demonstrating technology-driven consumer confidence enhancement. Direct-to-consumer brand development, establishing premium positioning and a margin optimisation opportunity, complementing traditional retail channel distribution. Micro-influencer ecosystem development enabling niche market targeting with authenticity-driven community engagement supporting brand loyalty formation. Social commerce accounts for 28 percent global mobile commerce revenue, compared to 18 percent demonstrating structural channel reallocation and market share concentration.

Headless Commerce Architecture and API-First Platform Customization

Headless commerce architecture enabling decoupled presentation layer and backend commerce functionality supporting flexible storefront customisation and omnichannel deployment. API-first platform design supporting third-party developer ecosystem integration, enabling specialised vertical solution development and rapid feature deployment. Microservices architecture enabling modular capability scaling, supporting variable demand accommodation and operational cost optimisation. The Digital Commerce Applications Market benefits from architectural modernization supporting enterprise agility and competitive differentiation through specialised application development.

Composable commerce model enabling enterprise selection of best-of-breed component solutions supporting flexible vendor sourcing and proprietary capability development. Real-time data analytics platform integration enabling business intelligence infrastructure development supporting data-driven decision-making. Metaverse commerce integration opportunity addressing immersive shopping experience development and virtual commerce channel expansion. Voice-assisted shopping technology deployment supporting accessibility enhancement and emerging interface modality adoption. Blockchain-based transaction security enabling decentralised commerce infrastructure development, supporting fraud prevention and transaction transparency. Enterprise integration capability advancement supporting legacy system preservation while enabling modern commerce capability deployment.

Category-wise Analysis

Solution Type Insights

Online storefront platforms maintain dominant shares of around 24.8% through proven technology maturity, broad merchant accessibility across verticals, established payment gateway integration infrastructure, and diversified revenue model flexibility supporting subscription, transaction-based, and marketplace commission pricing structures. Cloud-based storefront platform standardization reducing capital investment barriers, enabling merchant accessibility across enterprise and SME segments. Multitenant architecture supporting operational scale efficiency and rapid customer onboarding. Established payment processor partnerships, ensuring transaction settlement reliability and merchant capital optimization. Third-party application marketplace integration supporting functional customization without platform provider engineering resource consumption. Digital Commerce Applications Market dominance reflects platform standardization supporting rapid adoption across retail, healthcare, BFSI, and manufacturing verticals. Omnichannel capability maturation, integrating online storefronts with point-of-sale systems and inventory management infrastructure supporting unified commerce operations.

Mobile commerce applications demonstrate accelerating adoption momentum driven by smartphone ubiquity, establishing universal consumer access, progressive web application technology reducing installation friction, native application notification capability supporting customer re-engagement, and responsive user interface design optimizing transaction completion on constrained mobile displays. Mobile application personalisation capability supporting real-time recommendation delivery aligned with individual user preferences.

End Use Industry Insights

Retail and e-tail sectors command 35.7% market leadership through established online sales infrastructure, extensive product catalog digitization, substantial consumer accessibility through omnipresent e-commerce platforms, and competitive pricing pressure driving platform adoption and operational efficiency optimization. Traditional retail sector transformation requires digital commerce capabilities supporting customer expectations for seamless online-offline shopping experiences. Fashion, hobby, and leisure product categories demonstrate large e-commerce transaction volumes, establishing sector innovation leadership.

Omnichannel retail strategy implementation mandating integrated inventory management and customer data unification across physical and digital channels. E-commerce platform competition is intensifying, requiring continuous capability enhancement and customer experience optimisation. North America and Europe's retail sector digital commerce maturity is establishing operational benchmarks for emerging market adoption trajectories. China's retail sector dominance demonstrates 52 percent online sales penetration, establishing an advanced commerce capability deployment exemplar.

Consumer goods sector demonstrates fastest adoption momentum driven by accelerating direct-to-consumer brand strategy implementation, bypassing traditional retail intermediation, premium product positioning supporting margin optimisation, and omnichannel distribution requirement supporting seamless purchase experience across channels. FMCG brand digitalization supporting supply chain visibility and demand forecasting precision enhancement.

Regional Insights and Trends

North America Market Trend

North America represents a mature digital commerce market with 30% global revenue share characterized by high digital penetration, advanced payment infrastructure, substantial SME digital commerce adoption, and innovation leadership in AI-powered personalisation and social commerce integration. The United States e-commerce market is demonstrating sustained expansion, with mobile commerce transactions representing the primary transaction channel.

Digital Commerce Applications Market benefits from North American enterprise IT investment supporting platform modernisation and omnichannel capability deployment. Retail, BFSI, and consumer goods sectors are establishing commercialisation leadership and establishing deployment precedents for emerging market adoption.

AI-powered capability advancement enabling conversion rate optimisation, social commerce integration with influence-led direct-to-consumer channel expansion, mobile commerce maturation with 69 percent Black Friday mobile participation, and enterprise modernisation supporting headless commerce architecture adoption.

CCPA privacy framework establishes a state-level data protection mandate, creating complexity compliance. FTC e-commerce guidance establishing consumer protection standards. PCI-DSS payment security framework supporting transaction integrity assurance.

Shopify, Adobe Commerce, and Salesforce Commerce Cloud are establishing platform market dominance. Digital-native brands establish direct-to-consumer model deployment. Established retailers implementing omnichannel capability supporting competitive positioning.

East Asia Market Trend

East Asia demonstrates the fastest regional growth trajectory with 25% global market share driven by China's advanced commerce infrastructure, massive consumer population establishing transaction volume scale, mobile-first commerce adoption, and social commerce sophistication, including livestream shopping, generating USD 480 billion annual turnover.

China representing dominant APAC market with 52 percent retail sales online penetration, establishing an advanced commercial practices adoption exemplar. India's telecom sector growth, with 979 million internet users and 86.09 percent tele-density, establishes an emerging commerce infrastructure foundation. Digital Commerce Applications Market benefits from APAC B2B eCommerce dominance with 80 percent global GMV concentration supporting manufacturing and supply chain digitalisation. SME digitalisation accelerates across Southeast Asia, supporting emerging market platform adoption.

Mobile-first consumer behaviour with 7.7 billion smartphone users by 2027, establishing commerce accessibility, government digitalisation initiatives, including India's ONDC platform enabling SME participation, Unilever eB2B platform deployment connecting 500,000 retailers and processing 75,000 daily orders, and 5G network expansion enabling advanced multimedia commerce experiences.

Variable national frameworks create compliance complexity. India's Unified Payments Interface standardization supporting payment infrastructure modernisation. China's regulatory environment is establishing e-commerce supervision standards. ASEAN cross-border commerce harmonization supporting regional platform development.

Europe Market Trend

Europe represents a mature digital commerce market with 22% global revenue share characterized by GDPR regulatory leadership establishing privacy standards, strong BFSI sector engagement, and advanced AI-powered personalisation capability adoption supporting competitive differentiation. The EU information and communication services sector generates EUR 667 billion value added, with 7.2 million employees supporting digital commerce infrastructure development. Computer programming and IT services representing 60% sectoral employment, demonstrating technology infrastructure investment concentration. Germany is contributing 22 percent EU-wide value added, establishing regional technology leadership positioning.

GDPR compliance capability supporting trusted commerce environment development, advanced payment infrastructure enabling cross-border commerce transaction settlement, SME digitalization supporting competitive positioning against large retailers, and social commerce integration with influencer-led campaign deployment.

Competitive Landscape

The Global Digital Commerce Applications Market is oligopolistic at the top, with a few dominant players like Shopify, Adobe (Magento Commerce), Salesforce Commerce Cloud, SAP Commerce Cloud, BigCommerce, and WooCommerce commanding significant market share through broad solution portfolios and global reach. These leading companies compete on innovation, AI capabilities, scalability, and omnichannel support, creating high barriers for new entrants

Regional and niche players in mobile commerce, social commerce, and personalisation tools contribute to market fragmentation and foster innovation. Market competition is further influenced by tech giants like Amazon and Alibaba, whose integrated commerce ecosystems drive adoption and set industry standards. Overall, while the top tier reflects concentrated leadership, the market remains dynamic with opportunities for specialised solutions.

Key Industry Developments

- 16 April 2025, Unilever launched and scaled its cloud-based eB2B digital commerce platform across five emerging Asian markets, integrating AI-enabled ordering, fulfilment, and sales execution tools to connect 500,000 retailers, 600 distributors, and 6,000 sales reps, processing 75,000 orders daily and targeting 1.5 million micro-retailers for €4 billion annual turnover by digitising end-to-end distributive trade operations.

- March 23, 2023, Shopify and Google Cloud announced a global AI integration enabling retailers using Shopify Commerce Components to deploy Google Cloud’s Discovery AI for enhanced digital commerce capabilities, including AI-driven search, browsing, and personalisation features. The integration allows enterprise merchants to reduce search abandonment and improve product discovery, with early adopter Rainbow Shops reporting a 48 percent increase in search volume and a threefold reduction in bounce rates on its ecommerce platforms.

Companies Covered in Digital Commerce Applications Market

- Shopify

- BigCommerce

- Adobe Commerce (Magento)

- Salesforce Commerce Cloud

- SAP Commerce Cloud

- Oracle Commerce

- VTEX

- Lightspeed Commerce

- Wix eCommerce

- Commercetools

- Elastic Path

- Spryker Systems

Frequently Asked Questions

The global Digital Commerce Applications Market is projected to be valued at US$ 38.9 Bn in 2026.

The Online Storefront / eCommerce Platform segment is expected to account for approximately 24.8% of the Global Digital Commerce Applications Market by Solution Type in 2026.

The market is expected to witness a CAGR of 10.9% from 2026 to 2033.

Digital Commerce Applications Market growth is driven by mobile-first consumer adoption, smartphone ubiquity, 5G-enabled commerce experiences, AI-driven personalization, SME digitalization, and standardized open commerce networks.

Key market opportunities in the Digital Commerce Applications Market lie in social commerce and influencer-led D2C expansion, augmented and immersive reality shopping, headless and API-first commerce architectures, composable commerce adoption, voice-assisted shopping, blockchain-enabled security, and real-time data-driven platform integration.

Key players in the Digital Commerce Applications Market include Shopify, BigCommerce, Adobe Commerce (Magento), Salesforce Commerce Cloud, SAP Commerce Cloud, Oracle Commerce.