- Healthcare Services

- Digital Health Market

Digital Health Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Digital Health Market by Product Type (Hardware, Software, Services), Technology (Digital Health Systems, mHealth, Tele-healthcare, Healthcare Analytics, Others), Application (Chronic Disease Management, Health & Fitness, Behavioral Health, Others), End-user (Payers, Providers, Patients, Others), and Regional Analysis from 2026 to 2033

Digital Health Market Share and Trends Analysis

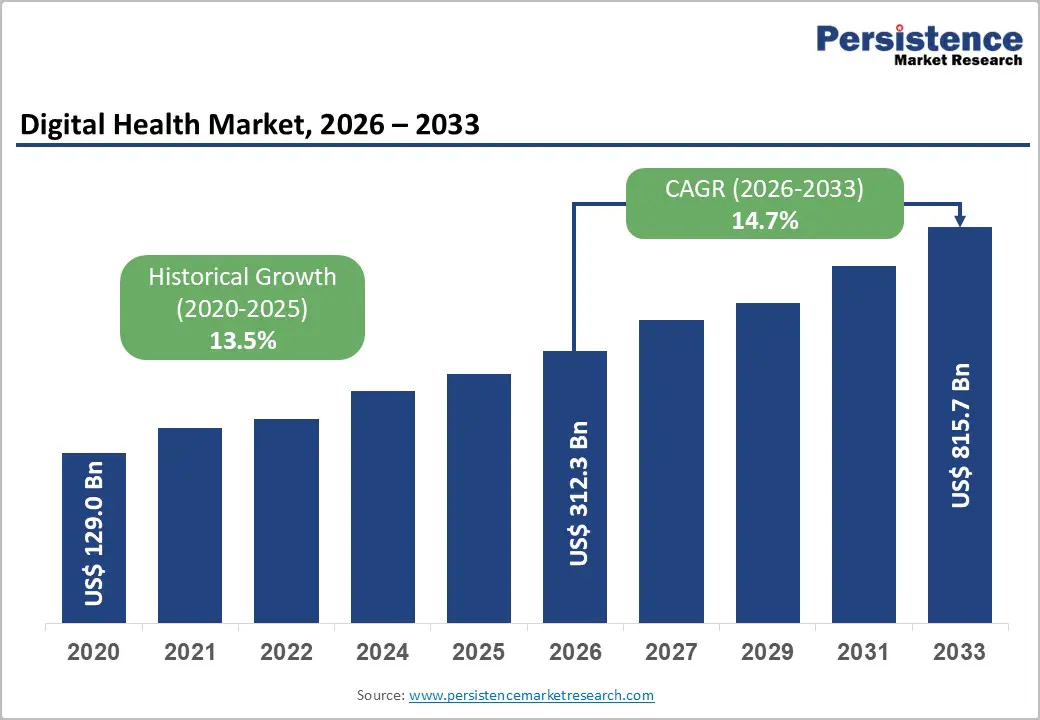

The global digital health market is estimated to grow from US$ 312.3 Bn in 2026 to US$ 815.7 Bn by 2033. The market is projected to record a CAGR of 14.7% during the forecast period from 2026 to 2033.

The global digital health market is expanding steadily, driven by rising adoption of telehealth, mHealth, and healthcare analytics. North America holds the largest share, while the Asia Pacific grows fastest due to expanding infrastructure, increasing digital health adoption, government initiatives, and rising patient awareness. Growth is supported by investments in software, services, and advanced remote monitoring solutions.

Key Industry Highlights

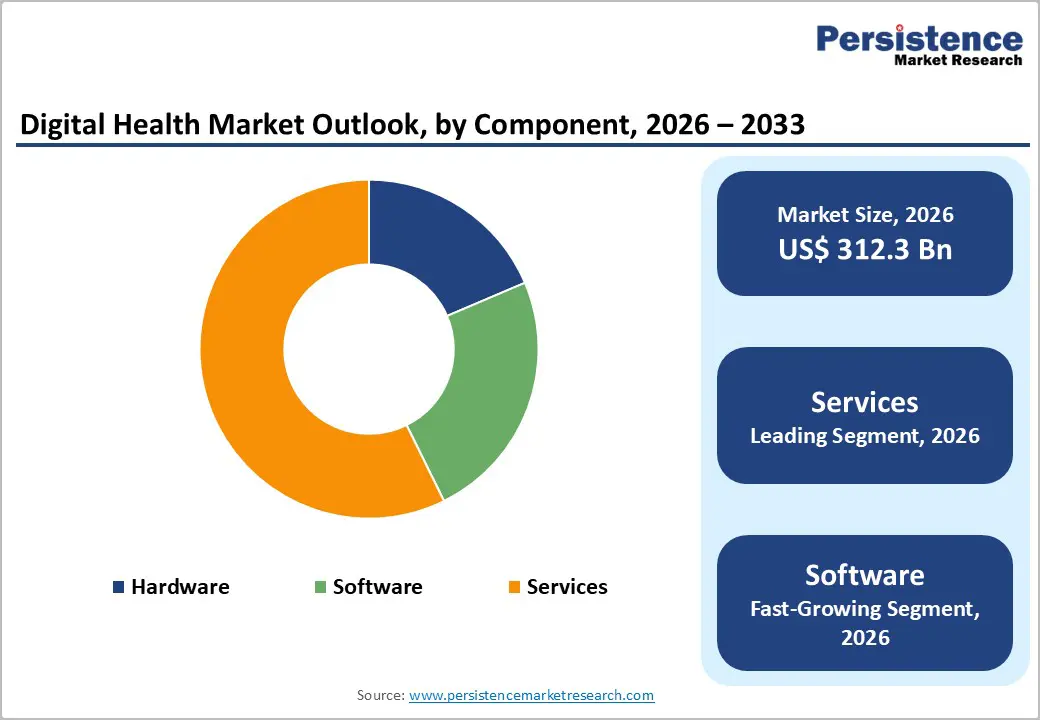

- Dominant Segment: Services account for 57.3% share of the Digital Health Market in 2025, driven by demand for implementation, integration, training, maintenance, and managed services. Growth is fueled by hospitals, clinics, and remote care providers seeking professional support for software deployment, system interoperability, data management, and cybersecurity, ensuring seamless operation of telehealth, mHealth, and analytics platforms.

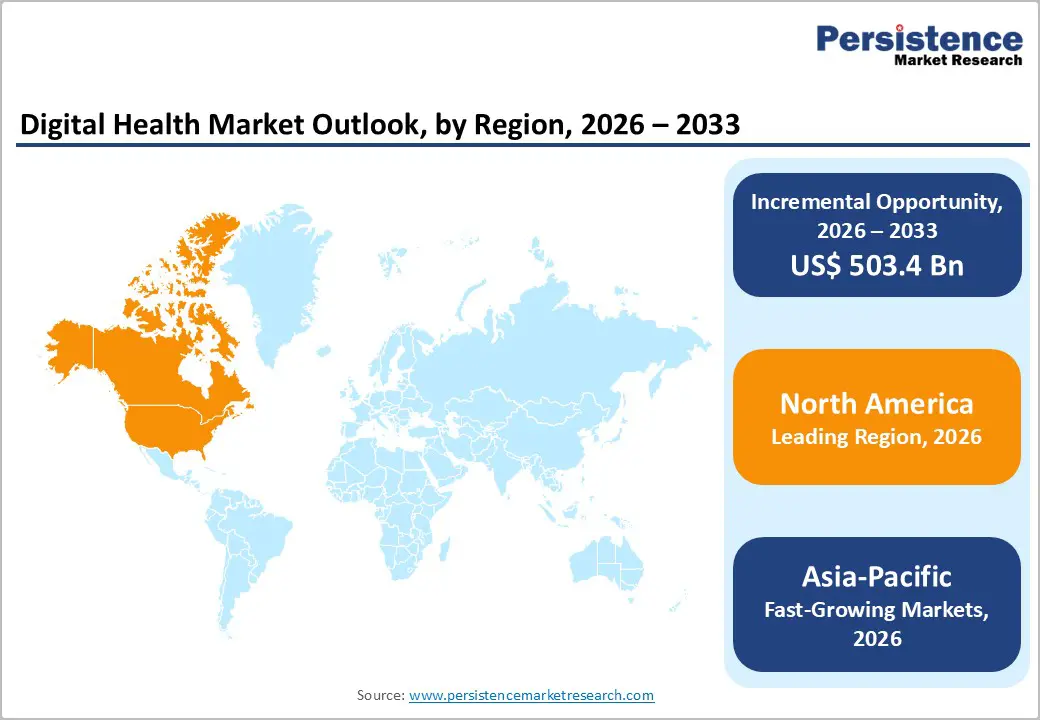

- Dominant Region: North America leads with 41.0% share due to advanced infrastructure, high technology adoption, and strong reimbursement frameworks. Asia Pacific is the fastest-growing region, supported by expanding digital health infrastructure, rising patient awareness, government initiatives, and increasing smartphone penetration.

- Market Drivers: Growth is driven by increasing chronic disease burden, rising telehealth adoption, need for efficient care delivery, regulatory support, and advancements in AI, cloud, and mobile health technologies.

- Market Opportunity: Key opportunities include AI-enabled diagnostics, cloud-based platforms, wearable health devices, predictive analytics, personalized care solutions, remote monitoring, and expansion in emerging economies with improved healthcare access.

| Key Insights | Details |

|---|---|

| Digital Health Market Size (2026E) | US$ 312.3 Bn |

| Market Value Forecast (2033F) | US$ 815.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.5% |

Market Dynamics

Driver: Increasing adoption of telehealth, mHealth, and remote patient monitoring

The increasing adoption of telehealth and remote patient monitoring is a key driver of growth in the Digital Health Market, as virtual care becomes central to modern healthcare delivery. According to the U.S. Centers for Disease Control and Prevention (CDC), telemedicine use among physicians increased from approximately 43% before the COVID-19 pandemic to 88% during the pandemic, reflecting a major shift toward remote care. National data show telehealth visits among Medicare beneficiaries increased from roughly 5 million to over 53% early in the pandemic, and over 80% of physicians intend to continue telehealth use. This sustained adoption highlights telehealth’s role in expanding patient access and care continuity.

Mobile health (mHealth) and digital monitoring tools further substantiate telehealth’s impact on the Digital Health Market, as patients and providers increasingly adopt digital engagement. CDC definitions underscore mHealth’s use of mobile phones and other smart devices to transmit health information, thereby enabling chronic disease management and patient communication. Remote patient monitoring devices and apps are increasingly integrated into care, with publicly available data indicating that telehealth encounters accounted for a substantial share of clinical care during peak periods and continue to be used for chronic disease management and follow-up. National health objectives identify expanded telemedicine use as a priority for improving access and outcomes, reinforcing its market significance.

Restraints: Data privacy and cybersecurity concerns in digital health systems

Data privacy and cybersecurity concerns are significant constraints on the growth of the digital health market, as breaches undermine trust and expose sensitive patient information. U.S. government data show that in 2024 more than 700 healthcare data breaches were reported involving over 180 million compromised records, including names, contact details, and medical information, as tracked by the Department of Health and Human Services Office for Civil Rights. Between 2018 and 2023, hacking-related incidents increased by %, driven by ransomware and IT attacks, highlighting systemic vulnerabilities in digital health systems that must be addressed to protect Protected Health Information (PHI).

Beyond privacy risks, cyberattacks affect healthcare operations and patient care, limiting digital health adoption. Surveys indicate that approximately 93% of U.S. healthcare organizations experienced at least one cyberattack in the past year, and 72% reported disruptions to patient care due to these attacks. Ransomware and hacking not only compromise data but also delay procedures, extend hospital stays, and increase clinical risk, creating reluctance among providers to fully digitize systems without stronger security. These realities illustrate how persistent cybersecurity challenges restrain broader digital health investment and integration across care settings.

Opportunity: Growth of mobile health apps, wearable devices, and patient engagement tools

The expansion of mobile health apps presents a clear opportunity for the digital health market by increasing patient engagement and self-management. In the United States, about 43% of adults reported using a health app in 2024, demonstrating widespread consumer adoption of digital health tools. Globally, more than 350,000 digital health apps are available on major app stores, with tens of thousands added annually, reflecting rapid development and diversity of health-focused applications. Additionally, a substantial portion of smartphone users employ these apps for exercise, nutrition, and vital tracking, underscoring how mobile technologies empower individuals to monitor and manage their health.

Wearable health devices and patient engagement tools further strengthen the opportunity for digital health growth by enabling continuous monitoring and deeper patient involvement. National survey data indicate that wearable device use among adults increased from about 28% in 2019 to over 36% in 2022, reflecting rising comfort with personal health tracking technologies. Moreover, a majority of wearable users are willing to share health data with providers, supporting integration into clinical care. These trends indicate that as wearables and connected apps deliver real-time insights and encourage proactive health behavior, digital health platforms can leverage this engagement to improve outcomes and expand adoption.

Category-wise Analysis

By Component Insights

Services occupies 57.3% share of the global market in 2025, because healthcare providers require professional support to implement, integrate, and maintain complex digital systems effectively. With widespread adoption of electronic health records (EHRs), telehealth platforms, and analytics tools, hospitals and clinics rely on services such as system customization, data migration, staff training, and cybersecurity management to ensure smooth operation. In the U.S., nearly 96% of non-federal acute care hospitals and 78% of office-based physicians have adopted certified EHR systems, reflecting extensive digitization. Government initiatives like India’s Ayushman Bharat Digital Mission further drive demand for services by promoting interoperable health infrastructure. Continuous support, compliance assurance, and optimization make services essential, securing their dominant market share.

By Technology

Tele-healthcare dominates the digital health market because virtual care has become an integral part of healthcare delivery, significantly expanding access and utilization. In the United States, telemedicine use among office-based physicians increased dramatically from 15.4% in 2019 to 85.9% in 2021, indicating the rapid incorporation of virtual care into routine practice. More than one-third of U.S. adults (37%) reported having a telemedicine visit in the past year, illustrating widespread patient engagement with remote services. During the COVID-19 pandemic, Medicare telehealth visits increased 63-fold, from approximately 840,000 in 2019 to 52.7 million in 2020, demonstrating telehealth’s capacity to preserve care continuity when in-person visits were constrained. Continued high adoption reflects telehealthcare’s central role in expanding access, convenience, and care-delivery efficiency.

Regional Insights

North America Digital Health Market Trends

North America dominates the digital health market with 41.0% share in 2025, because of its advanced healthcare infrastructure, high technology adoption, and supportive public policy. Government actions such as the HITECH Act have driven digital transformation, with over 96% of U.S. hospitals implementing EHR systems, facilitating interoperable care and data exchange. Telemedicine integration accelerated markedly during the COVID-19 pandemic. Telehealth visits increased more than 50-fold compared with pre-pandemic levels, expanding access to virtual care even in rural areas. Regulatory flexibility and reimbursement support from agencies like CMS have sustained telehealth and remote monitoring adoption. Canada’s federally supported agencies, such as Canada Health Infoway, have also expanded digital health solutions nationwide. These structural, regulatory, and technological advantages underpin North America’s market leadership.

Europe Digital Health Market Trends

Europe is a key region in the digital health market due to strong government support, advanced infrastructure, and widespread digital health adoption. As of 2024, the EU-27 average eHealth maturity score reached 83%, with 85% of member states providing online access to health data for most of their populations, indicating high interoperability and digital record coverage. Telehealth and remote monitoring are integrated into national health strategies across 40 European countries, improving access and care efficiency. Initiatives like the European Health Data Space (EHDS) facilitate secure cross-border data exchange, supporting research, innovation, and continuity of care. These structured policies, digital infrastructure, and coordinated implementation make Europe an important driver and adopter in the global digital health landscape.

Asia Pacific Digital Health Market Trends

Asia Pacific’s status as the fastest-growing region in the digital health market is supported by global adoption trends in digital health technologies. Worldwide, over 1.4 billion people are projected to use digital health tools, such as telemedicine, mobile apps, and wearable devices by 2025, reflecting broad consumer engagement with digital health solutions across regions. Telehealth usage has expanded rapidly, with more than 200 million people expected to use telehealth services annually by 2024, demonstrating substantial global adoption of virtual care modalities. Approximately 38.5% of people globally now access mHealth services, indicating rising mobile health engagement, while wearable device adoption continues to grow for remote monitoring and self-care. These global usage patterns underscore why Asia Pacific, with rising internet penetration and mobile adoption, is outpacing other regions in digital health growth.

Market Competitive Landscape

Leading digital health market companies focus on software, services, and connected devices, emphasizing interoperability, security, and user-friendly solutions. Investments target AI-enabled analytics, telehealth platforms, and patient engagement tools. R&D prioritizes efficiency, data accuracy, and care continuity, while collaborations with healthcare providers and regulators enhance adoption, drive innovation, and expand global integration of digital health technologies.

Key Industry Developments:

- In December 2025, Philips unveiled new advances in its AI-driven imaging systems and expanded its radiation-free, light-based navigation technologies. The company highlighted enhancements that improve imaging accuracy, workflow efficiency, and patient safety, emphasizing the integration of artificial intelligence to support clinical decision-making.

- In December 2025, GE Healthcare launched its next-generation Signa MRI technology to enhance the patient experience. The new system featured advanced imaging capabilities, faster scan times, and improved patient comfort during procedures.

Companies Covered in Digital Health Market

- Koninklijke Philips N.V.

- GE Healthcare

- Abbott

- Teladoc Health, Inc.

- Siemens Healthineers AG

- Masimo

- AT & T, Inc.

- Medtronic

- Dexcom, Inc.

- iHealth Labs Inc.

- Qardio, Inc.

- AdvancedMD, Inc

- Others

Frequently Asked Questions

The global digital health market is projected to be valued at US$ 312.3 Bn in 2026.

Rising chronic diseases, telehealth adoption, technological advancements, government support, and increasing demand for accessible healthcare.

The global digital health market is poised to witness a CAGR of 14.7% between 2026 and 2033.

AI-driven diagnostics, wearable devices, telehealth expansion, mobile apps, cloud platforms, patient engagement, and emerging markets growth.

Koninklijke Philips N.V., GE Healthcare, Abbott, Teladoc Health, Inc., Siemens Healthineers AG, Masimo.