- Home Appliances

- Digital Camcorders Market

Digital Camcorders Market Size, Share, and Growth Forecast 2026 - 2033

Digital Camcorders Market by Resolution (Full HD (1920 x 1080) 1080p, UHD (3840 x 2160) 2160p), by Camera (Integration Camera, Bridge Camera, Compact Digital Camera), End-user (Individual Consumers, Media and Entertainment Professionals, Corporate and Educational Institutions), and Regional Analysis, 2026 - 2033

Digital Camcorders Market Size and Trend Analysis

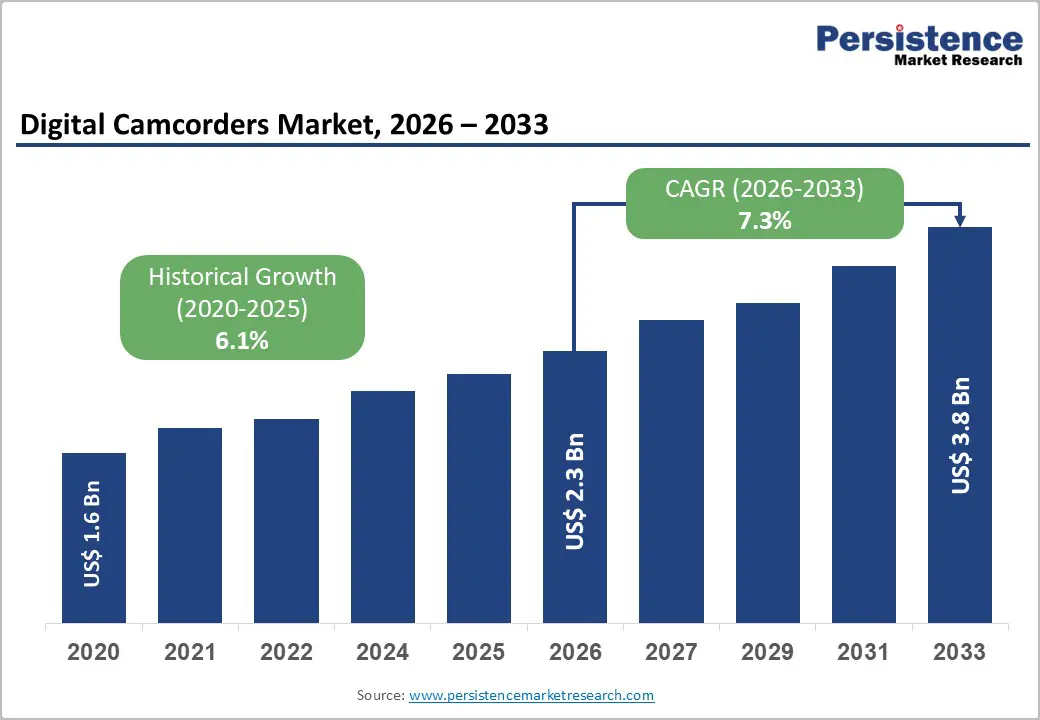

The global digital camcorders market size is likely to be valued at US$ 2.3 billion in 2026 and is expected to reach US$ 3.8 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 and 2033. Rising demand for high-resolution 4K/Ultra HD video content, along with the proliferation of streaming platforms and social media, is driving sustained upgrades from legacy camcorders to modern devices with AI-assisted autofocus, better low-light performance, and advanced image stabilization.

Key Market Highlights

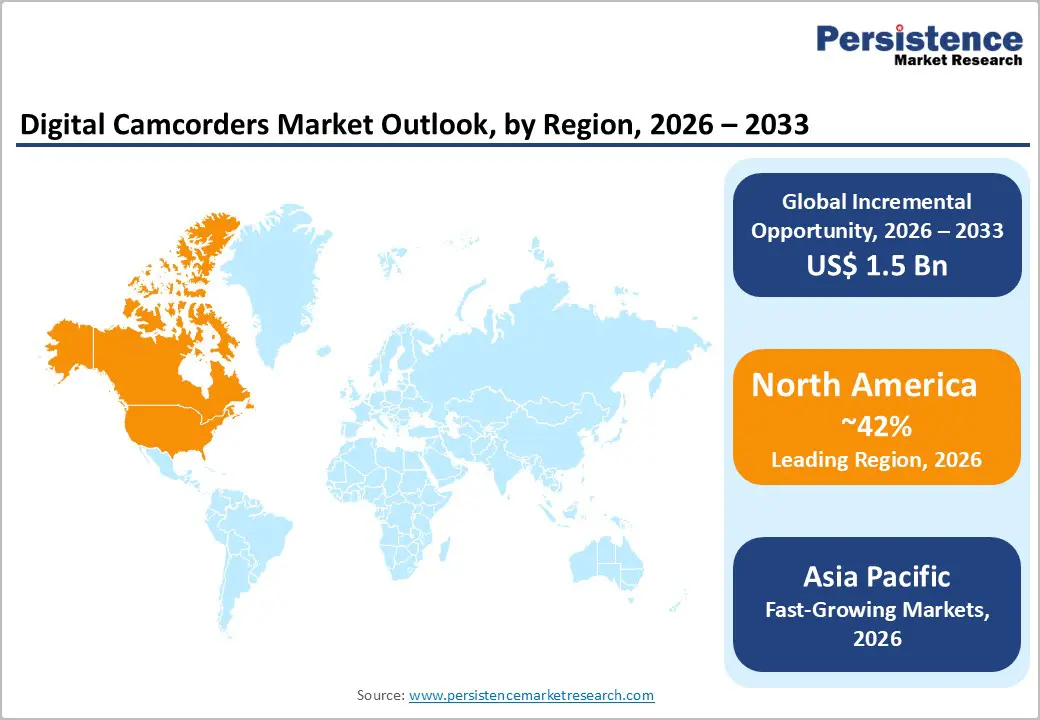

- Leading Region: North America is a leading region in the digital camcorders market with 42% global share, supported by the U.S. dominance in OTT platforms, sports broadcasting and live event production, along with the strong presence of global imaging brands and advanced innovation ecosystems.

- Fastest-Growing Region: Asia Pacific is expected to be the fastest-growing region with rising CAGR of 9.7%, propelled by expanding video production industries in China, Japan, India and ASEAN, rising adoption of 4K workflows and cost-competitive manufacturing capabilities for cameras and components.

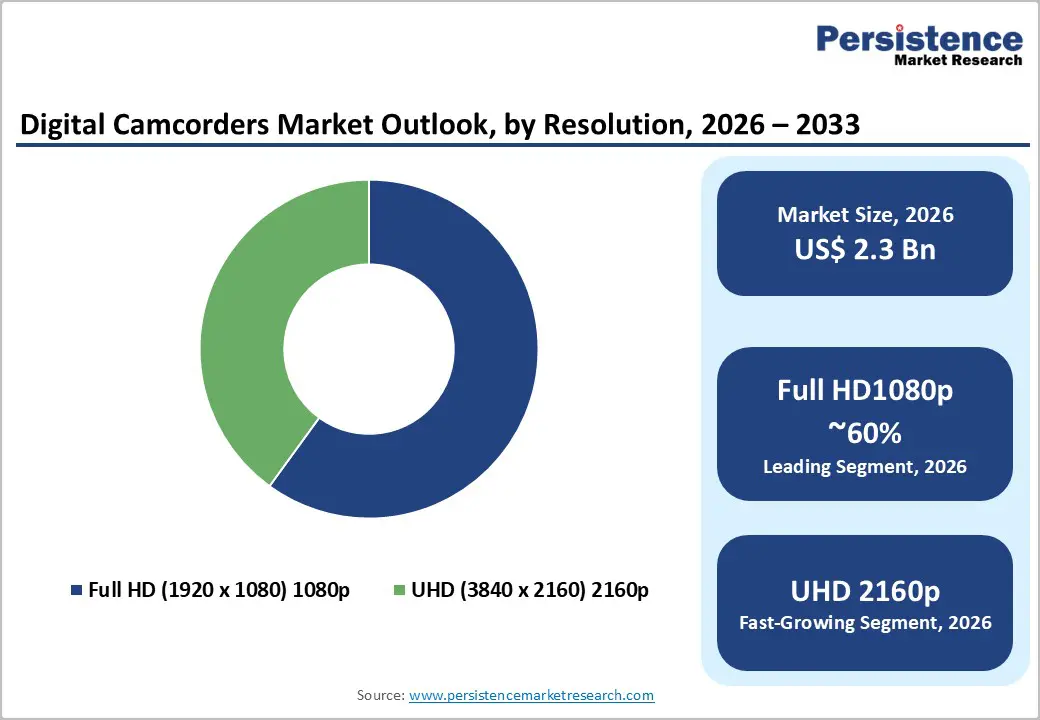

- Leading Segment: The UHD (3840 x 2160) 2160p resolution segment is emerging as the dominant category, holding 60% share, as broadcasters, streamers and professionals standardize on 4K for future-proof production and prioritize camcorders with higher frame rates and advanced stabilization.

- Fastest-Growing Segment: Media and entertainment professionals represent the dominant end-user segment, as broadcasters, production houses and independent creators invest in multi-camera 4K setups, professional audio, and connectivity features for live and on-demand content creation.

- Key Market Opportunities lie in AI-enabled 4K camcorders and networked production workflows, enabling small teams, educational institutions, and corporate studios to deliver broadcast-grade content with fewer operators and tighter integration into IP and cloud-based environments.

| Key Insights | Details |

|---|---|

|

Digital Camcorders Market Size (2026E) |

US$ 2.3 Billion |

|

Market Value Forecast (2033F) |

US$ 3.8 Billion |

|

Projected Growth CAGR (2026-2033) |

7.3% |

|

Historical Market Growth (2020-2025) |

6.1% |

Market Dynamics

Drivers - Rising Shift Toward 4K, High-Frame-Rate Streaming Drives Strong Replacement Demand for Professional UHD Camcorders

The rapid expansion of the digital video ecosystem is a major growth driver for the digital camcorders market, as content platforms increasingly prioritize 4K and high-frame-rate formats. Sports broadcasting, live events, documentaries, and OTT streaming services are steadily shifting toward 4K resolution to enhance viewer experience and content differentiation. As a result, broadcasters and independent creators are upgrading to camcorders capable of delivering 4K 60p and 120p recording, wide-angle to telephoto zoom ranges, and professional-grade codecs that integrate seamlessly into existing workflows.

This transition is significantly strengthening demand for UHD (3840 × 2160) 2160p camcorders among media and entertainment professionals. New product launches, including Sony’s HXR-NX800 and PXW-Z200, feature AI-powered subject recognition, advanced image stabilization, and high dynamic range recording. These enhancements improve efficiency and output quality, making such camcorders ideal for live streaming, corporate video, and documentary production, thereby supporting sustained replacement cycles.

Expansion of Hybrid Work, E-Learning, and Virtual Events Accelerates Institutional Adoption of Dedicated 4K Camcorders

The expansion of hybrid work models, e-learning platforms, and virtual events is driving increased adoption of digital camcorders across education, corporate, and institutional environments. Universities, training centers, enterprises, and public organizations are investing in dedicated camcorders for lecture capture, virtual conferences, internal communications, and live-streamed events. Compared with webcams or smartphones, digital camcorders offer superior reliability, extended zoom capabilities, better audio inputs, and long-form recording without overheating, which is critical for lecture halls, houses of worship, and government facilities.

Vendors are increasingly positioning 4K handheld camcorders specifically for education and corporate use by bundling features such as network connectivity, SDI and HDMI outputs, remote operation, and centralized control. These tailored offerings make camcorders easier to deploy at scale, improving production quality while reducing operational complexity. As a result, corporate and educational institutions are emerging as a clearly defined and fast-growing end-user segment within the digital camcorders market.

Restraint - Advanced Smartphone Cameras and Compact Action Devices Reduce Entry-Level Camcorder Demand among Consumers

The rapid advancement of smartphone camera technology presents a significant restraint to the digital camcorders market, particularly at the entry and consumer levels. High-end smartphones now feature multi-lens systems, advanced image sensors, and powerful computational photography that meet the everyday video needs of a broad user base. This reduces demand for basic camcorders among casual users. At the same time, the growing popularity of action cameras further diverts consumer spending.

Brands such as GoPro and DJI offer compact, rugged devices capable of recording 4K or even 5.3K video, appealing strongly to adventure, travel, and sports enthusiasts who prioritize portability and ease of use. Younger consumers, in particular, are more inclined toward lightweight, multi-purpose devices. As a result, traditional camcorder manufacturers face pricing pressure and commoditization risks. To remain competitive, vendors must emphasize clear differentiation through long optical zoom, professional audio support, extended recording time, and superior ergonomics that smartphones and action cameras cannot fully replicate.

Long Capital Cycles and Budget Constraints Limit Upgrade Frequency across Professional and Institutional Buyers

Budget limitations and extended replacement cycles among professional and institutional buyers continue to restrain growth in the digital camcorders market. Broadcast stations, educational institutions, and public-sector organizations typically operate under multi-year capital expenditure plans, which slow the pace of new equipment purchases. Even when newer camcorder models offer significant improvements in resolution, AI features, or connectivity, many organizations prefer to maximize the lifespan of existing assets.

Professional video equipment is often amortized over long periods, and buyers may choose refurbishment, maintenance, or partial upgrades instead of full replacement. This trend is especially pronounced in regions with constrained media or education budgets. As a result, overall unit shipment growth remains moderate, while competition intensifies around pricing, service contracts, warranties, and total cost of ownership. Vendors must increasingly justify upgrades through operational efficiency, reduced staffing needs, and compatibility with IP-based production systems to overcome procurement inertia in B2B segments.

Opportunity - AI-Powered Autoframing and IP-Based Workflows Create New Growth Pathways for Networked Camcorder Deployments

The integration of artificial intelligence into digital camcorders presents a major growth opportunity, particularly for small teams, solo creators, and institutional users. AI-driven features such as subject recognition, auto-tracking, intelligent autofocus, and scene-based exposure control significantly simplify video production. Modern 4K camcorders equipped with dedicated AI processing units and advanced image engines can automatically keep speakers centered, in focus, and properly exposed, even during movement.

This capability reduces the need for skilled camera operators in lecture halls, corporate studios, and live streaming environments. At the same time, the industry is rapidly shifting toward IP-based production and remote workflows, including NDI-style connectivity and cloud-based editing. Camcorders that integrate seamlessly into networked control rooms and remote production setups are increasingly preferred. As media and corporate environments scale multi-camera operations efficiently, demand for AI-enabled, network-ready camcorders is expected to grow strongly among professional users.

Premium UHD Niches Such as Events, Regional Media, and Faith Broadcasting Offer High-Margin Growth Opportunities

Premium and niche professional segments continue to offer attractive growth opportunities for digital camcorder manufacturers. Documentary filmmakers, religious broadcasters, regional news channels, and event production companies consistently favor dedicated camcorders due to their reliability, ergonomic design, and long optical zoom capabilities. UHD (3840 × 2160) 2160p camcorders remain particularly attractive in these segments, as they deliver high image quality while supporting long recording sessions.

Vendors are increasingly launching compact 4K camcorders featuring 20x or higher optical zoom, large 1.0-inch-type CMOS sensors, and support for 4K 60p or 120p recording. These specifications address the need for cinematic depth of field, strong low-light performance, and ENG-style usability. As streaming platforms commission more regional and live content worldwide, these professional niches provide higher margins and recurring revenue from accessories such as batteries, microphones, and storage, reinforcing camcorders’ role in professional video ecosystems.

Category-wise Analysis

By Resolution Insights

Based on resolution, UHD (3840 × 2160) 2160p camcorders are emerging as the dominant segment in the digital camcorders market. This category is estimated to account for approximately 60% of new professional and prosumer shipments, as creators and organisations increasingly standardize on 4K production workflows. Major manufacturers have significantly expanded their 4K product portfolios across handheld and compact form factors, incorporating features such as high-bit-rate codecs, oversampled sensors, and improved color science.

These advancements deliver noticeably sharper and more detailed output on modern 4K televisions, monitors, and streaming platforms. As OTT services and social media platforms prioritize 4K content for premium offerings, buyers are becoming less willing to invest in new Full HD (1920 × 1080) devices. This shift reinforces UHD camcorders as the preferred choice for replacement purchases and long-term professional equipment planning across media, corporate, and educational applications.

By Camera Type Insights

By camera type, integrated and bridge-style camcorders with fixed long-zoom lenses account for a substantial share of professional-oriented volumes. Bridge-type and professional handheld camcorders are estimated to represent around 55% of total shipments within professional segments. These devices are widely used in news gathering, event coverage, and educational environments because integrated optics reduces downtime associated with lens changes while still offering 20x or higher optical zoom and strong image stabilization.

Their video-optimized ergonomics, balanced form factors, and reliable autofocus make them well-suited for extended shooting sessions. Compact digital camera-style camcorders are more popular among consumers and vloggers, but they typically generate lower average selling prices. In contrast, integrated and bridge camcorders offer higher value, longer usage life, and stronger accessory attachment rates, making them the primary revenue contributors in B2B-focused digital camcorder deployments.

By End-user Insights

Among end-users, media and entertainment professionals represent the largest share of market value, accounting for approximately 50% or more of total revenue. Broadcasters, production houses, and independent filmmakers require advanced camcorders with professional audio inputs, multi-camera compatibility, and reliable connectivity, which drives higher per-system spending. These users also invest heavily in accessories and workflow integration, further increasing market value.

Corporate and educational institutions form another rapidly expanding end-user group, supported by growing investments in lecture capture systems, internal communication studios, and live streaming infrastructure. In contrast, individual consumers increasingly rely on smartphones or hybrid cameras for casual video recording, keeping their participation more volume-driven than value-driven. As a result, professional and institutional buyers continue to shape product development priorities and pricing strategies, reinforcing the importance of feature-rich, reliable camcorders in high-value end-user segments.

Regional Insights

North America Digital Camcorders Market Trends

North America remains a leading region in the global digital camcorders market, supported by a strong concentration of broadcasters, sports leagues, and content platforms that have standardized on 4K and HDR production. The U.S. market benefits from high OTT penetration, robust advertising spending, and early adoption of IP-based production workflows. These factors encourage broadcasters and live event companies to regularly refresh equipment fleets with AI-enabled 4K camcorders.

The region also hosts major subsidiaries and operational hubs for leading brands such as Sony, Canon, Panasonic, GoPro, and DJI, ensuring strong distribution networks and after-sales support. Additionally, a stable regulatory environment around broadcasting standards and workplace safety enables long-term investment planning. Government grants, tax incentives, and funding for educational and community media further support adoption among universities, corporate users, and public institutions across the U.S. and Canada.

Europe Digital Camcorders Market Trends

Europe demonstrates steady demand for digital camcorders, driven primarily by public and private broadcasters in countries such as Germany, the U.K., France, and Spain. These broadcasters continue to invest in 4K and hybrid production infrastructures to meet evolving content standards. Public service broadcasters often procure professional camcorders through multi-year framework agreements, which provide a stable baseline of demand even during periods of economic uncertainty.

Regulatory harmonization under EU audiovisual directives supports cross-border content distribution, encouraging production houses to maintain high technical quality. Growth in live sports, cultural programming, and regional news further sustains demand for UHD camcorders. The strong presence of manufacturers such as Canon, Panasonic, Blackmagic Design, Leica Camera AG, and Olympus enhances local availability and technical support, reinforcing Europe’s gradual but consistent transition toward IP-connected, UHD-enabled camcorder platforms.

Asia Pacific Digital Camcorders Market Trends

Asia Pacific is one of the fastest-growing regions in the digital camcorders market, supported by large populations and rapidly expanding professional video ecosystems. China, Japan, India, and ASEAN countries are witnessing increased demand from broadcasters, online video platforms, and e-commerce live streaming services. In China and Southeast Asia, affordable yet capable 4K camcorders are widely adopted for digital news and commercial streaming, supported by local manufacturing and competitive pricing.

Japan and South Korea serve as key innovation centers, with companies such as Sony, Panasonic, Nikon, Fujifilm, and Sharp advancing sensor and optics technologies used globally. Meanwhile, India and emerging ASEAN markets are experiencing growth in regional OTT platforms, digital news channels, and education technology. These trends are driving new investments in entry-to-mid-range professional camcorders by schools, religious institutions, and small production companies.

Competitive Landscape

The global digital camcorders market is moderately concentrated, with a small number of established imaging brands accounting for a significant share of professional and prosumer shipments. Leading companies include Sony Corporation, Canon Inc., Panasonic Corporation, JVC, Blackmagic Design, Nikon Corporation, Fujifilm Holdings Corporation, Samsung Electronics Co., Ltd., and Sharp Corporation. Competition centers on sensor performance, lens quality, 4K and emerging 8K capabilities, AI-driven features, and seamless integration with editing and streaming workflows.

Strategic priorities across the industry include expanding future-ready product portfolios, strengthening connectivity options such as Wi-Fi, SDI, and IP streaming, and investing in advanced autofocus and auto-framing technologies. Vendors are also increasingly offering ecosystem-based solutions that bundle hardware with software, services, and accessories. This approach enhances customer retention, increases recurring revenue, and positions camcorder brands as long-term partners in professional video production.

Key Market Developments

- June 2024: Sony Corporation announced the HXRNX800 and PXWZ200 4K handheld camcorders with AI recognition, 20x optical zoom and advanced autofocus aimed at broadcast, corporate and education applications.

- August, 2024: Independent reviews highlighted the new Sony PXW-Z200 4K camcorder’s enhanced image quality, AI-assisted features and improved ergonomics, reinforcing its positioning for documentary and event filmmakers.

- February, 2024: Canon Inc. celebrated maintaining the No. 1 share of the global interchangeable-lens digital camera market for 21 consecutive years, underscoring its strong imaging ecosystem that supports its professional camcorder offerings.

Companies Covered in Digital Camcorders Market

- Sony Corporation

- Canon Inc.

- Panasonic Corporation

- JVC

- GoPro, Inc.

- DJI

- Blackmagic Design

- Samsung Electronics Co., Ltd

- Nikon Corporation

- Olympus Corporation

- Fujifilm Holdings Corporation

- Ricoh Company, Ltd

- Leica Camera AG

- Sharp Corporation

- Toshiba Corporation

- Insta360

- Garmin Ltd.

- Akaso, Kodak

Frequently Asked Questions

The global Digital Camcorders Market is projected to reach about US$ 2.3 Billion in 2026 and approximately US$ 3.8 Billion by 2033, reflecting a forecast CAGR of around 7.3% from 2026-2033.

Key demand drivers include rapid adoption of 4K/UHD production and streaming, growth in OTT and social video platforms, and increased use of camcorders in education, corporate communications and live event coverage requiring high reliability and advanced zoom capabilities.

The UHD (3840 x 2160) 2160p resolution segment and media and entertainment professionals end‑user group lead the market, together accounting for the majority of value due to strong 4K standardization and higher‑priced professional equipment purchases.

North America, led by the U.S., currently leads the digital camcorders market, supported by advanced broadcast and OTT ecosystems, high spending on sports and live events, and strong presence of global imaging manufacturers and professional distributors.

A major opportunity lies in AI‑enabled, networked 4K camcorders that integrate auto‑tracking, intelligent autofocus and IP streaming, allowing small teams, educational institutions and enterprises to produce broadcast‑quality content more efficiently.