- Media & Entertainment

- Digital Terrestrial Television (DTT) Market

Digital Terrestrial Television (DTT) Market Size, Share, and Growth Forecast, 2026 - 2033

Digital Terrestrial Television (DTT) Market by Technology (DVB-T/T2, ATSC, ISDB-T, DTMB), Component (Set-Top Boxes, Integrated Digital TVs, Conditional Access Systems), End-User (Residential, Commercial, Government/Public Broadcasting), and Regional Analysis for 2026 - 2033

Digital Terrestrial Television (DTT) Market Share and Trends Analysis

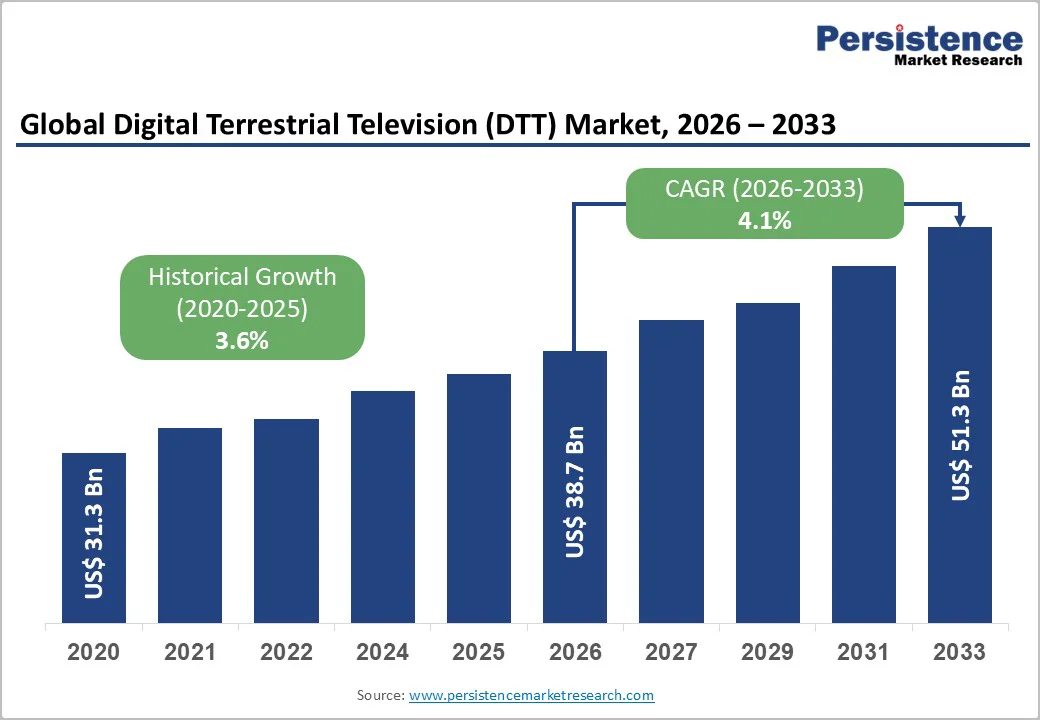

The global digital terrestrial Television (DTT) market is projected to reach US$38.74 billion in 2026 and US$51.3 billion by 2033, growing at a CAGR of 4.1% during the forecast period 2026 - 2033.

Widespread government-mandated analog switch-offs, rising adoption of high-definition and ultra-high-definition content, and accelerating deployment of next-generation broadcast standards worldwide are the main factors aiding market growth. Continued infrastructure investments and consumer demand for high-quality, cost-effective terrestrial broadcast services support steady growth.

Key Industry Highlights

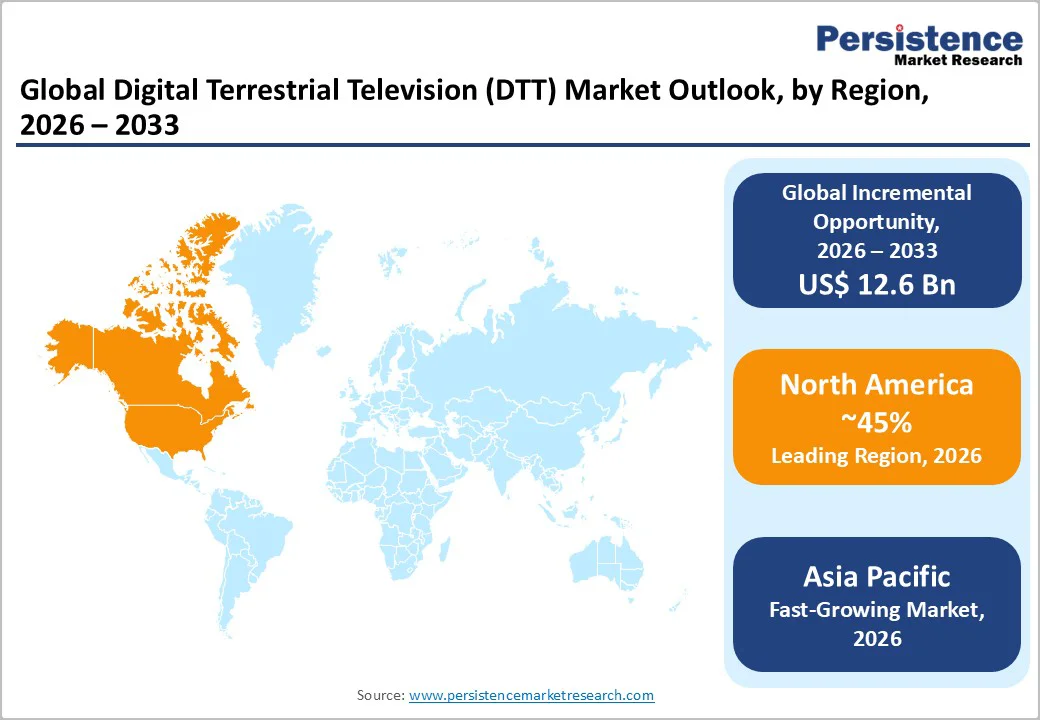

- Dominant Region: North America is projected to lead the DTT market with a 45% share in 2026, driven by advanced telecom infrastructure and targeted, high-quality broadcasting services.

- Fastest-growing Regional Market: Asia Pacific is slated to be the fastest-growing DTT market through 2033, owing to digital policy reforms, spectrum reallocation, and increased regional content catering to local languages and cultures.

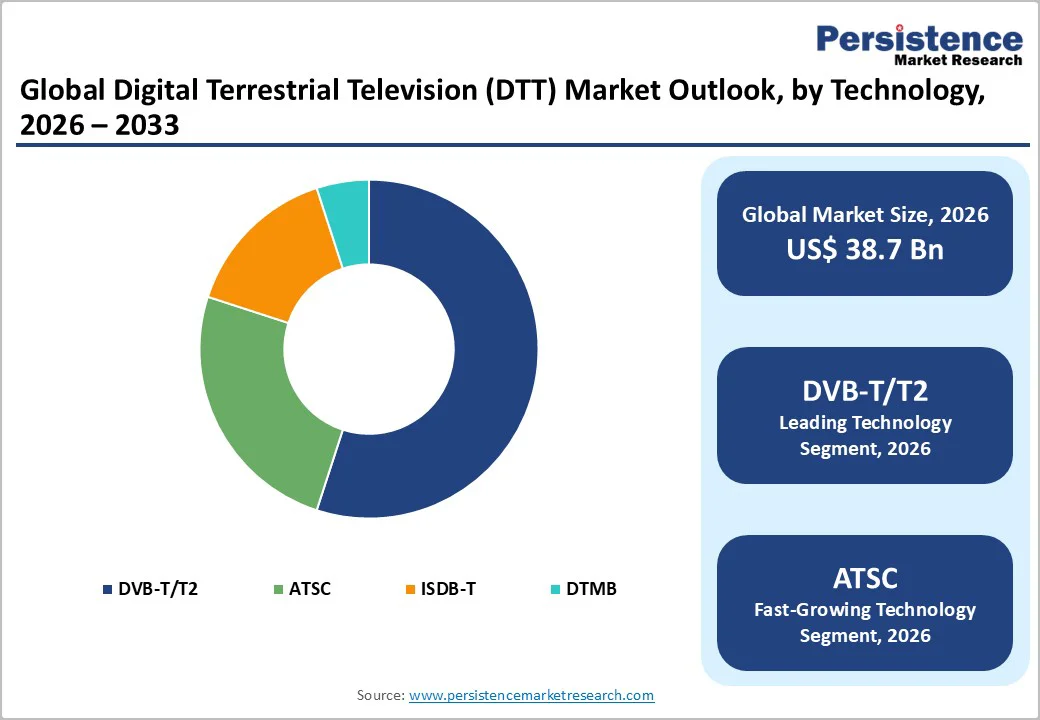

- Leading Technology: DVB-T/T2 is projected to lead the market with a 55% share in 2026, due to global adoption, technical reliability, and efficient multi-channel HD broadcasting.

- Fastest-growing Technology: Advanced Television Systems Committee (ATSC) is expected to be the fastest-growing technology, driven by UHD, immersive audio, interactive services, and targeted advertising in North America and select regions.

| Key Insights | Details |

|---|---|

| Digital Terrestrial Television Market Size (2026E) | US$38.74 Bn |

| Market Value Forecast (2033F) | US$51.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.1% |

| Historical Market Growth (CAGR 2020 to 2024) | 3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Government Initiatives for Digital Infrastructure Expansion

Government-led expansion of digital infrastructure is critical to enabling widespread access to high-quality television services. Investments in upgrading transmission networks, modernizing broadcast towers, and allocating spectrum for digital use create the foundation for efficient and reliable signal delivery.

These initiatives reduce technological barriers for service providers, allowing for broader coverage in urban and rural areas, improving service reliability, and supporting the deployment of high-definition and interactive features. By strengthening the underlying infrastructure, governments ensure that more households can adopt digital platforms, fostering audience growth and enhancing content accessibility.

Supportive policies and funding programs stimulate private sector participation and attract investment in broadcasting technologies. Incentives for network upgrades and regulatory support for spectrum management encourage broadcasters to expand their offerings and reach.

Such coordinated efforts enhance competitive advantage, drive technological innovation, and accelerate consumer adoption, creating a favorable environment for sustainable growth and long-term service expansion.

High Infrastructure Deployment Costs

The prohibitive costs of infrastructure deployment stem from the need for extensive network upgrades and modern broadcasting equipment. Transitioning from analog to digital requires investment in transmitters, signal towers, and distribution networks capable of handling high-capacity digital signals.

Existing infrastructure often cannot support advanced technologies such as HD or 4K broadcasting, necessitating complete overhauls in some regions. The procurement and installation of advanced encoders, modulators, and receivers contribute significantly to initial capital expenditure.

Expanding coverage to remote and rural areas further increases financial demands. Establishing a robust transmission network requires land acquisition, regulatory approvals, and skilled technical personnel, all of which escalate operational costs.

Maintenance of these networks also involves recurring expenses, including software updates and hardware replacements. High upfront and ongoing investments can slow deployment, limit adoption, and impact return on investment, presenting a substantial challenge to widespread digital transition initiatives.

Emerging Markets and Rural Penetration

Emerging economies present a significant growth avenue due to expanding population bases, rising disposable incomes, and increasing access to electricity and communication infrastructure. Many households in semi-urban and rural areas continue to rely on free-to-air television as a primary source of information and entertainment.

This demographic shift creates an opportunity to capture a large untapped audience with digital signals that offer better picture quality and more channels within the same frequency spectrum. The transition from analog to digital technology enhances content accessibility while supporting local broadcasters in delivering region-specific programming efficiently.

Rural penetration of DTT services has further market horizons, driven by affordability and accessibility. Low-cost set-top boxes and simple antennas allow households with limited purchasing power to access multiple channels without subscription fees.

Expanding network coverage into underserved regions enables broadcasters to reach audiences previously limited by analog transmission constraints. This expansion increases viewership, creates advertising opportunities, and strengthens brand loyalty, establishing a foundation for sustainable revenue growth across dispersed populations.

Category-wise Analysis

Technology Insights

DVB-T/T2 is projected to maintain its position as the leading segment, capturing an estimated 55% of the digital terrestrial television market revenue share in 2026. Its dominance is expected to continue due to extensive global adoption, technical reliability, and compatibility with existing broadcast infrastructure.

Broadcasters and consumers are expected to favor DVB-T/T2 for efficient spectrum usage, support for multiple channels, and consistent high-definition delivery, establishing it as the benchmark standard across mature and developing markets.

ATSC is expected to be the fastest-growing segment, driven by its widespread adoption in North America and in select international regions seeking advanced broadcasting capabilities.

Its growth is fueled by features such as ultra-high-definition transmission, immersive audio, and interactive services, as well as targeted advertising opportunities. The standard’s flexibility and enhanced efficiency enable broadcasters to offer premium content and innovative services, supporting accelerated uptake and market expansion.

Component Insights

Set-top boxes are projected to remain the leading component segment, holding an estimated 60% market share in 2026. Their dominance stems from their widespread adoption among households with existing televisions, enabling seamless conversion of digital signals.

Set-top boxes provide access to multiple channels, high-definition content, and interactive features, making them an essential device for both consumers and broadcasters in established and emerging markets.

Integrated digital TVs are expected to be the fastest-growing segment from 2026 to 2033, driven by rising smart TV penetration. These TVs come with built-in DTT receiving capabilities, eliminating the need for standalone set-top boxes and simplifying access to digital services.

The convenience of direct adoption, combined with growing consumer preference for multifunctional devices, is expected to accelerate uptake, enhance viewership, and support broader adoption of digital broadcasting solutions.

End-User Insights

The residential end-user segment is projected to remain the leading segment, capturing an estimated 65% of the DTT market share in 2026. Its dominance is rooted in the massive consumer demand for affordable and high-quality broadcasting content.

Households continue to prioritize access to diverse channels, HD programming, and interactive features, making residential consumption the primary revenue driver for broadcasters and service providers globally.

Government and public broadcasting are anticipated to be the fastest-growing segments during the 2026 - 2033 forecast period, supported by ongoing digital migration programs and public service initiatives. Investments in modernized transmission infrastructure and efforts to expand outreach to underserved populations are expected to accelerate adoption.

This growth enables governments to deliver educational, informational, and cultural content efficiently, enhancing public engagement while driving the transition from analog to digital broadcasting across multiple regions.

Regional Insights

North America Digital Terrestrial Television (DTT) Market Trends

North America is projected to dominate by capturing an estimated 45% of the digital terrestrial television market share in 2026. This leadership is driven by the widespread adoption of advanced broadcasting standards, including ATSC, which offers ultra-high-definition video, immersive audio, and enhanced interactivity.

The region benefits from highly developed infrastructure, robust spectrum management, and a regulatory environment that actively supports digital transition initiatives. Broadcasters in the U.S. and Canada leverage these technical capabilities to deliver differentiated content, including targeted advertising and location-specific programming, which strengthens consumer engagement and loyalty.

Another key factor sustaining North America’s dominance is the integration of DTT capabilities into consumer electronics. High penetration of smart TVs with built-in digital tuners reduces dependency on additional hardware, simplifying user access to digital content. Coupled with strong consumer purchasing power and a mature advertising ecosystem, these factors create a sustainable revenue model for broadcasters.

Ongoing government support for public and emergency broadcasting ensures comprehensive coverage, further reinforcing the region’s leadership in both urban and semi-urban markets. This combination of technological innovation, infrastructure maturity, and consumer readiness underpins North America’s continued market dominance.

Europe Digital Terrestrial Television (DTT) Market Trends

Europe is projected to remain a key market for DTT due to its mature infrastructure, high consumer adoption, and early completion of analog-to-digital migration. Countries such as the U.K., Germany, and France have established efficient broadcasting networks and standardized DVB-T/T2 adoption, ensuring consistent high-definition content delivery and broad channel availability.

Strong regulatory frameworks support spectrum efficiency, multiservice broadcasting, and public service content, reinforcing market stability.

Consumer preferences in Europe favor advanced features such as electronic program guides, multi-language options, and interactive services, which enhance viewer engagement. The regional market also benefits from ongoing upgrades to next-generation technologies, including DVB-T2 enhancements and hybrid broadcasting solutions, enabling broadcasters to optimize bandwidth and offer additional services.

Combined with high urban penetration, steady household purchasing power, and a focus on sustainable broadcasting practices, Europe maintains a stable yet innovative market environment, sustaining opportunities for both consumer and broadcaster growth.

Asia Pacific Digital Terrestrial Television (DTT) Market Trends

Asia Pacific is anticipated to register the fastest growth in the digital terrestrial television market, driven by the convergence of digital policy reforms and rising local content production. Governments in countries such as India, Malaysia, and Vietnam are implementing spectrum reallocation strategies to accommodate multiple digital channels, enabling broadcasters to expand offerings efficiently.

This regulatory support is complemented by a surge in regional content tailored to local languages and cultural preferences, driving viewer engagement.

Infrastructure modernization, including the deployment of low-cost terrestrial transmitters in rural and semi-urban areas, is creating unprecedented market accessibility. Coupled with a tech-savvy younger population adopting smart TVs and hybrid devices, these factors accelerate penetration.

The rise of interactive services, such as real-time voting, e-commerce integration, and educational programming, differentiates the region from mature markets, positioning Asia Pacific as a high-potential growth hub for both broadcasters and advertisers seeking scalable, targeted reach.

Competitive Landscape

The global digital terrestrial television market is moderately consolidated, with major players such as Samsung Electronics, Huawei Technologies, Humax, and ARRIS holding significant market shares.

These companies leverage strong brand recognition, established distribution networks, and technological expertise to maintain leadership. Their focus on research and development ensures continuous innovation in set-top boxes, integrated TVs, and advanced broadcasting solutions, meeting evolving consumer demands and enhancing service quality.

Market concentration is expected to increase as leading companies pursue geographic expansion and strategic investments. Collaborations, partnerships, and acquisitions enable players to strengthen their product portfolios, enter new regions, and achieve economies of scale. Such strategies intensify competitive dynamics, fostering innovation while reinforcing the dominance of established players in both mature and emerging markets.

Key Industry Developments

- In September 2025, Arcom, France's communications regulator, delayed reallocation of four Canal+ pay-TV channels on digital terrestrial television for two years due to unfavorable economic conditions amid declining TV consumption and weak advertising. Canal+ exited DTT in June after license rejection for C8 news channel.

- In September 2025, Radiocuba’s Las Tunas division launched an investment initiative to expand DTT services, introducing advanced equipment through collaboration with China. The upgrade significantly enhances the quality and coverage of television signals, improving access to high-quality broadcasts for residents across the Las Tunas region.

- In April 2025, UHD Spain endorsed the new National Technical Plan for Digital Terrestrial Television, enabling DVB-T2 transmission across national, regional, and local areas. The framework paves the way for widespread UHD broadcasts, following the transition from standard definition to high definition in February 2024.

Companies Covered in Digital Terrestrial Television (DTT) Market

- Samsung Electronics

- Huawei Technologies

- Humax

- ARRIS

- Kaonmedia

- Technicolor

- Sagemcom

- EchoStar

- Intelsat

- Sentech

Frequently Asked Questions

The global digital terrestrial television (DTT) market is projected to reach US$ 38.74 billion in 2026.

Rising consumer demand for high-quality broadcasts, government digital migration initiatives, and growing adoption of advanced transmission technologies are driving the market.

The market is poised to witness a CAGR of 4.1% from 2026 to 2033.

Rural penetration of DTT services and considerable growth in integrated digital TVs are key market opportunities.

Some of the key market players include Samsung Electronics, Huawei Technologies, Humax, ARRIS, Kaonmedia, Technicolor, Sagemcom, EchoStar, Intelsat, and Sentech.