- Specialty & Fine Chemicals

- Battery Materials Market

Battery Materials Market Size, Share, and Growth Forecast 2026 - 2033

Battery Materials Market by Battery Type (Lead Acid, Li-ion, Nickel-Cadmium, Nickel-metal hydride, Other), Material (Cathode, Anode, Electrolytes, Separator, Other), Application (Automotive, Consumer Electronics, Industrial, Other), and Regional Analysis for 2026 - 2033

Battery Materials Market Size and Trend Analysis

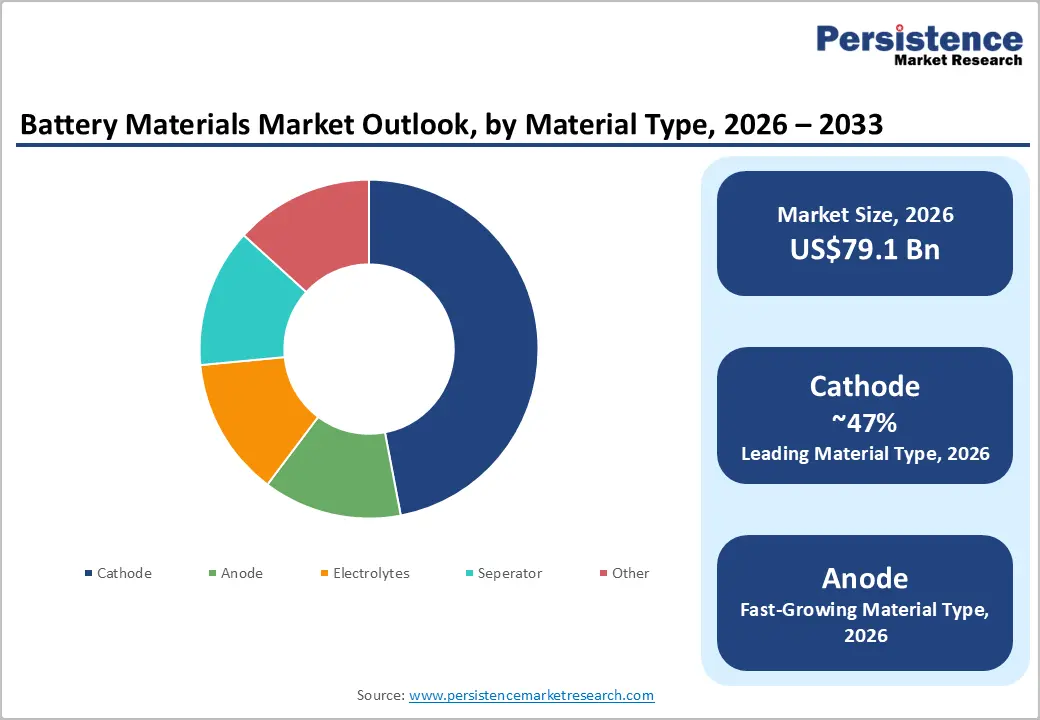

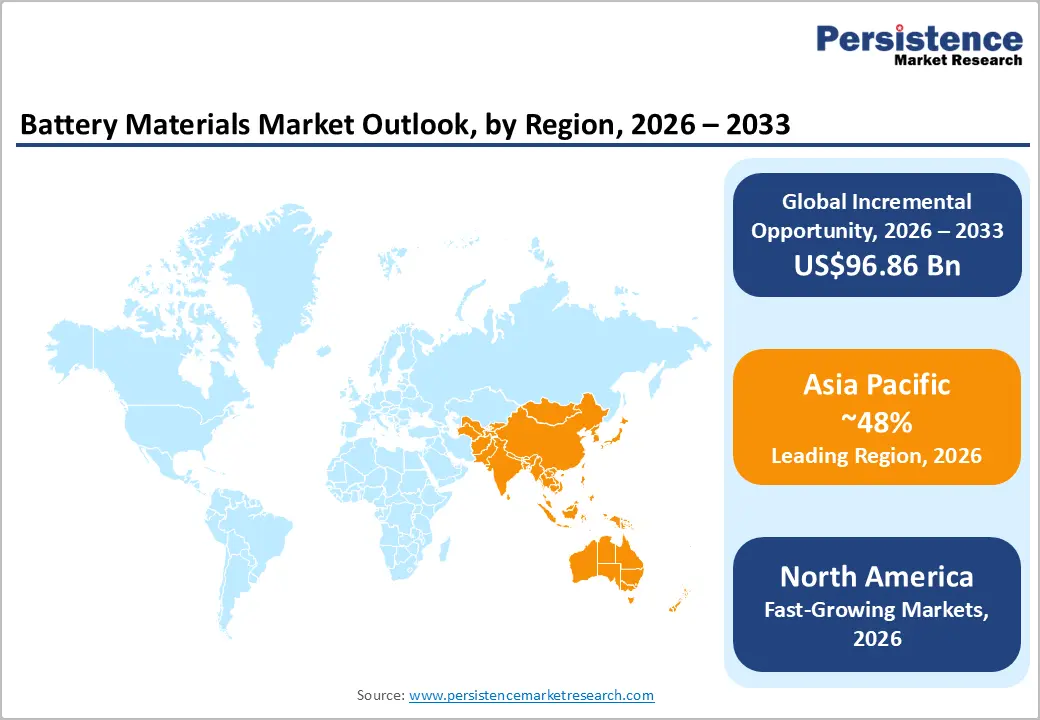

The global Battery Materials Market size is supposed to be valued at US$ 79.1 billion in 2026 and is projected to reach US$ 176.0 billion by 2033, growing at a CAGR of 12.1% between 2026 and 2033. The market is primarily driven by the rapid global transition toward electric vehicles, with the International Energy Agency (IEA) projecting battery capacity requirements to increase tenfold from current levels of 340 GWh per year to over 3,500 GWh per year to meet 2030 electrification targets, necessitating output from approximately 100 gigafactories worldwide.

Additionally, declining battery pack prices, which fell to $132 per kWh in 2021 according to the IEA, coupled with continuous innovation in cathode and anode chemistries, including lithium iron phosphate and high-nickel formulations, enhance market accessibility and application versatility across automotive, consumer electronics, and industrial energy storage sectors.

Key Industry Highlights:

- Regional Leader: Asia Pacific dominates the global Battery Materials Market, with over 48% market share, driven by China's comprehensive manufacturing capabilities, with total cathode material shipments reaching 4.987 million tonnes in 2025, up 51.5% year-over-year, and supported by established supply chain infrastructure across the battery materials value chain.

- Fastest Growing Region: North America represents the fastest-growing regional market, driven by the U.S. Department of Energy's $3 billion grant program supporting battery materials capacity development across 14 states.

- Leading Segment: Cathode materials command approximately 47% market share as the dominant component segment, driven by critical roles in determining battery energy density and cost structures, with LFP materials accounting for 79.1% of China's total cathode shipments in 2025.

- Fastest Growing Segment: Anode materials constitute the fastest-growing material segment at an estimated 14% CAGR, propelled by innovation in silicon-dominant and lithium-metal anode architectures promising substantial energy density improvements for next-generation battery chemistries entering commercialization phases.

- Key Opportunities: The expansion of stationary energy storage systems for renewable energy integration and grid modernization creates substantial market opportunities, with leading battery manufacturers collectively procuring cathode materials totaling approximately 6 million tonnes, valued at over RMB 24 million, in 2025 across diversified automotive and energy storage applications.

| Key Insights | Details |

|---|---|

|

Battery Materials Market Size (2026E) |

US$ 79.1 Bn |

|

Market Value Forecast (2033F) |

US$ 176.0 Bn |

|

Projected Growth CAGR (2026-2033) |

12.1% |

|

Historical Market Growth (2020-2025) |

10.2% |

Market Dynamics

Drivers - Exponential Growth in Electric Vehicle Adoption and Battery Demand

The global automotive sector’s rapid shift toward electrification remains the principal driver of rising demand for battery materials. Electric vehicle sales exceeded 17 million units in 2024, marking a 25% annual increase and reinforcing long-term growth momentum. Meeting international climate objectives will require lithium demand to rise sixfold to 500 kilotons by 2030, equivalent to developing approximately 50 additional mid-sized mines.

Major automakers have outlined extensive electrification strategies, supported by substantial investments in battery-electric vehicle manufacturing. China’s cathode material shipments reached 4.987 million tonnes in 2025, a 51.5% year onyear increase, underscoring its significant scale-up capacity. Concurrently, policy measures, such as the U.S. Inflation Reduction Act’s Section 45X incentives, are accelerating localized production of battery materials across North America and Europe.

Technological Advancements in Battery Chemistry and Energy Density Enhancement

Continuous innovation in battery materials is driving significant improvements in performance and cost efficiency, expanding opportunities across multiple applications. Advances in high-nickel cathode chemistries, such as NMC and NCA, now enable energy densities above 1000 Wh/l and 400 Wh/kg. At the same time, lithium iron phosphate (LFP) continues to gain momentum in cost-sensitive segments. China shipped 3.944 million tonnes of LFP cathode materials in 2025, representing 79.1% of total cathode shipments and a 62.5% annual growth rate, highlighting strong demand for safety, longevity, and affordability.

Silicon-enhanced anode materials with 10–50% silicon provide substantial capacity gains over graphite and are increasingly used in wearables, smartphones, drones, and light electric vehicles. According to the IEA, global demand for LFP and LMFP chemistries may reach 2,683 GWh by 2036, while high nickel formulations could reach 2,207 GWh, underscoring continued diversification in battery chemistry.

Restraints - Critical Raw Material Supply Chain Vulnerabilities and Price Volatility

The battery materials sector faces significant structural challenges stemming from concentrated critical mineral supplies and persistent price volatility. Cobalt prices, for example, have historically tripled to nearly $81,000 per metric ton over short periods, creating substantial cost uncertainty for cathode manufacturers. Supply chain risks are further heightened by the geographic concentration of mineral extraction in politically unstable regions.

According to the IEA, continued market constraints and elevated commodity prices could increase battery pack costs by up to 15% year over year, potentially slowing electric vehicle adoption. China’s lithium-ion battery production capacity exceeded 2 TWh in 2024, around 60% above global demand, resulting in overcapacity, intensified price competition, and sustained supply chain dependencies. Growth is also limited by nickel purity constraints, as battery-grade material requires specialized refining infrastructure with multi-year development timelines.

Environmental and Regulatory Compliance Complexities

Escalating environmental regulations across major markets are imposing stringent requirements on battery material manufacturing, raw material sourcing, and end-of-life recycling processes. The European Union’s battery framework mandates supply chain transparency, carbon footprint reporting, and minimum recycled-content thresholds, thereby increasing operational complexity and compliance costs for manufacturers.

In the United States, Treasury Department rules requiring that at least 50% of battery components be manufactured in North America and that 40% of critical minerals be sourced domestically or from free-trade partners to qualify for consumer tax credits are driving extensive supply-chain restructuring. Additionally, rising expectations for ethical sourcing and responsible mineral extraction demand rigorous auditing systems, thereby increasing procurement costs and administrative burdens, particularly for cobalt sourced from regions with known governance and labor-practice challenges.

Opportunity - Expansion of Energy Storage Systems Beyond Automotive Applications

The rapid expansion of stationary energy storage systems for grid stabilization, renewable energy integration, and commercial and industrial backup power is generating substantial additional demand for battery materials beyond the automotive sector. Leading manufacturers such as CATL, BYD, EVE Energy, Sunwoda, and CALB collectively procured nearly 6 million tonnes of cathode materials in 2025, reflecting an increasingly diversified range of applications across transportation and energy storage.

Global renewable energy goals and grid modernization initiatives are accelerating utility-scale storage deployments, with many projects favoring cost-optimized LFP chemistries that emphasize safety, long cycle life, and overall cost efficiency. China’s demand for LFP materials alone is expected to reach 6 million tonnes in 2026, with industry growth projected at 40–50%, driven largely by the expansion of energy storage. Manufacturers developing materials tailored to storage-specific requirements are well-positioned to capture growth while reducing reliance on automotive markets.

Solid-State Battery Development and Next-Generation Chemistry Commercialization

Investment in next-generation battery technologies, particularly solid-state batteries that use solid electrolytes instead of liquid formulations, offers substantial opportunities for material suppliers developing components for emerging chemistries. Energy density improvements of up to 50% through advanced composite cathodes incorporating sodium ion and lithium sulfur materials. Solid-state architectures remove the need for flammable liquid electrolytes and enable lithium-metal anodes, significantly improving energy density, driving range, and charging performance.

Automotive manufacturers and battery producers have announced major R&D commitments, with pilot-scale solid-state production expected in the latter half of the forecast period. Companies investing in solid-electrolyte technologies, such as sulfide-, oxide-, and polymer-based systems, along with compatible electrode materials, are positioned as key partners in next-generation cell manufacturing. Emerging chemistries, including lithium-sulfur, sodium-ion, and lithium metal batteries, further expand commercial opportunities for suppliers with adaptable manufacturing capabilities and strong R&D platforms.

Category-wise Analysis

Battery Type Insights

Lithiumion batteries hold approximately 82% of the battery materials market, supported by their superior energy density, declining production costs, and widespread use across electric vehicles, consumer electronics, and industrial energy storage. According to the IEA, meeting future demand will require expanding global lithium-ion manufacturing capacity from 340 GWh per year to more than 3,400 GWh by 2030, a tenfold increase requiring substantial materials infrastructure.

Within this segment, diversification in chemistry continues to accelerate. LFP batteries accounted for 79.1% of China’s cathode material shipments in 2025 due to their strong safety profile, long cycle life, and cost advantages. High-nickel chemistries such as NMC and NCA remain dominant in premium EV segments requiring higher energy density. Traditional technologies such as lead-acid, nickel-cadmium, and nickel-metal hydride batteries retain niche roles in automotive, industrial, and specialized applications.

Material Insights

Cathode materials account for a leading 47% share of the battery materials market, reflecting their critical influence on energy density, power performance, and overall cost, owing to the use of high-value metals such as lithium, nickel, cobalt, and manganese. China’s cathode material shipments reached 4.987 million tonnes in 2025, with LFP accounting for 3.944 million tonnes, demonstrating substantial production capacity and chemistry-specific specialization. Major suppliers, Hunan Yuneng, Wanrun Energy, and Defang Nano, each exceeded 1 million tonnes in shipments, indicating strong market concentration among established manufacturers.

Anode materials, primarily graphite-based with increasing incorporation of low-percentage silicon to boost capacity, continue to maintain a significant market presence. Electrolytes and separators, essential for ionic conductivity and cell safety, are also experiencing strong demand aligned with global battery output growth. The anode segment shows the fastest expansion, with an estimated 14% CAGR driven by innovations in silicon-dominant and lithium-metal designs that support next-generation chemistries.

Application Insights

Automotive applications remain the largest segment, accounting for approximately 61% of the market, driven by the global shift toward battery-electric and plug-in hybrid vehicles. This transition is supported by stricter emissions regulations and substantial government incentives across major regions. Battery demand continues to rise sharply, with electric vehicle sales surpassing 17 million units in 2024 and expected to maintain strong growth. In the United States, the Department of Energy has emphasized the need for domestic manufacturing capabilities, allocating $3 billion in 2024 grants across 14 states to strengthen battery materials and production capacity.

Consumer electronics account for approximately 24% of the market, supported by ongoing innovation cycles and increasing device adoption in emerging economies. Industrial applications, such as material handling, backup power, telecommunications, and grid-scale energy storage, are the fastest-growing segment, expanding at an estimated 15% CAGR as renewable integration and grid modernization accelerate demand for large-scale stationary storage systems.

Regional Insights

North America Battery Materials Market Trends

The North American battery materials market is undergoing significant expansion. U.S. Treasury tax credit rules requiring that at least 50% of battery components be manufactured in North America and 40% of critical minerals be sourced domestically or from free-trade partners are accelerating supply chain localization and increasing demand for regional materials capacity. Additionally, the U.S. Department of Energy’s $3 billion grant initiative launched in September 2024 is expediting manufacturing development across 14 states.

The United States also supports a robust innovation ecosystem, with technology firms, national laboratories, and academic institutions collaborating on advanced materials such as solid-state electrolytes and silicon-dominant anodes. Major automakers with regional production footprints continue to expand electric-vehicle manufacturing and establish joint ventures with Asian battery producers to secure compliant supply. The regulatory landscape emphasizes transparency, ethical sourcing, and environmental compliance, guided by the Department of Energy’s National Blueprint for Lithium Batteries, which outlines a decade-long plan to strengthen domestic capabilities from mineral extraction to recycling.

Europe Battery Materials Market Trends

Europe’s battery materials market continues to expand, supported by stringent regulatory frameworks, such as the EU Battery Regulation, which requires supply chain transparency, carbon footprint reporting, and minimum recycled-content levels. Public initiatives, including the European Battery Alliance and IPCEI programs, are accelerating gigafactory development and strengthening regional localization of the supply chain across Germany, France, Sweden, Poland, and Hungary. Leading manufacturers such as CATL and LG Energy Solution are also increasing their regional footprint, with CATL beginning construction of a 50 GWh LFP plant in Aragon, Spain, in 2025.

Germany remains a central hub for battery innovation, with BASF expanding cathode capacity and renewing long-term supply agreements. Collaborative efforts, such as the BASF–Umicore cross-license for advanced chemistries, reinforce technological progress. The growing emphasis on sustainability and circular-economy goals is accelerating battery recycling infrastructure, which the IEA estimates could meet up to 25% of lithium and nickel demand and 40% of cobalt demand by 2050.

Asia Pacific Battery Materials Market Trends

Asia-Pacific dominates the global battery materials market, with a market share exceeding 48%, driven largely by China’s extensive control across the value chain, from raw material processing to cell manufacturing. China produced 819,300 tonnes of ternary cathode materials in 2025 and shipped 4.987 million tonnes of total cathode materials, including 3.944 million tonnes of LFP, underscoring its leadership in cost-competitive chemistries for EVs and energy storage. However, China’s lithium-ion battery capacity exceeded 2 TWh in 2024, nearly 60% above demand, creating overcapacity and intensifying price competition.

Japan maintains strong technological leadership through companies such as Asahi Kasei, Toray, Mitsubishi Chemical, and Nichia, while South Korea specializes in high-nickel cathode precursors through firms such as Posco Future M and L&F. India is emerging as a high-growth market, supported by production-linked incentives for domestic battery manufacturing.

Competitive Landscape

The global battery materials market is moderately consolidated, with major multinational companies holding significant shares alongside specialized regional players. Cathode materials show the highest concentration, led by Umicore, BASF, and leading Chinese producers, while the separator and electrolyte segments remain more competitive. Companies are expanding production capacity through multi-billion-dollar investments in gigafactory-scale facilities across North America, Europe, and Asia to meet rising EV demand. Competitive differentiation focuses on advanced chemistries, vertical integration, geographic diversification, and long-term partnerships with automotive OEMs and battery manufacturers. R&D efforts increasingly target next-generation materials such as solid-state electrolytes, silicon-dominant anodes, and high-manganese cathodes.

Key Developments:

- February 2026: GFCL EV launches $216 million advanced battery materials project in Oman. Through its subsidiary GFCL EV (SFZ) LLC, registered in the Salalah Free Zone, Oman, the company announced plans to set up a state-of-the-art greenfield facility to manufacture advanced battery materials for electric vehicles and energy storage applications.

- February 2026: Arkema and Senior have signed a Memorandum of Understanding to deepen their long-term strategic partnership and accelerate innovation across the global battery value chain. The two companies will expand cooperation around Arkema’s current and future battery materials portfolio and Senior’s advanced separator technologies and industrialization capabilities.

- December 2025: POSCO Future M and Factorial signed a Memorandum of Understanding (MoU) for the development of all-solid-state battery technology. Under the MoU, the two companies plan to explore cooperation in developing materials for all-solid-state batteries, which are powering progress in next-generation industries such as electric vehicles, robotics, energy storage systems, and more.

Top Companies in Battery Materials Market

Umicore (Belgium) maintains global leadership in cathode materials for lithium-ion batteries, with a comprehensive product portfolio spanning nickel-manganese-cobalt and nickel-cobalt-aluminum chemistries, serving premium automotive and consumer electronics applications. The company operates manufacturing facilities across Europe, Asia, and North America, delivering cathode materials and precursors to leading battery cell manufacturers worldwide.

BASF SE (Germany) operates as a leading global cathode active materials supplier with manufacturing facilities in Germany, Japan, and strategic partnerships across Asia and North America, serving automotive and industrial battery applications. The company leverages its extensive chemical manufacturing expertise and global supply chain capabilities to deliver cathode materials and precursors including NMC, NCA, and emerging high-manganese chemistries optimized for cost and performance balance.

Asahi Kasei Corporation (Japan) dominates the lithium-ion battery separator market through its Hipore™ wet-process separator product line serving automotive battery applications globally. Asahi Kasei differentiates through advanced wet-process separator technologies delivering superior safety and performance characteristics for automotive lithium-ion batteries, established manufacturing presence across key geographic markets supporting customer proximity and supply chain resilience, and ongoing evaluation of additional greenfield facility investments in North America and Japan, addressing anticipated regional demand growth.

Companies Covered in Battery Materials Market

- Umicore

- Asahi Kasei Corporation

- BASF SE

- Nichia Corporation

- Mitsubishi Chemical Corporation

- Posco Future M

- Toray Industries Inc.

- Ube Corporation

- Resonac Holdings Corporation

- Kureha Corporation

- L&F Co., Ltd.

- Hitachi Energy Ltd.

- CATL

- LG Energy Solution

- Hunan Yuneng

- Wanrun Energy

- Defang Nano

- BYD Company Limited

Frequently Asked Questions

The global Battery Materials Market is valued at US$ 79.1 billion in 2026 and is projected to reach US$ 176.0 billion by 2033, expanding at a robust compound annual growth rate (CAGR) of 12.1% during the forecast period.

The market is primarily driven by exponential electric vehicle adoption with global sales surpassing 17 million units in 2024, representing 25% annual growth, and the International Energy Agency projecting lithium demand to increase sixfold to 500 kilotons by 2030.

Cathode materials dominate the market with approximately 47% market share, driven by their critical role in determining battery energy density, power characteristics, and cost structures due to incorporation of high-value metals including lithium, nickel, cobalt, and manganese.

Asia Pacific dominates the global market with over 48% market share, largely due to China's control of the battery materials value chain. In 2025, China's production of ternary cathode materials reached 819,300 tonnes, a 19.36% year-over-year increase, while total cathode shipments rose to 4.987 million tonnes, up 51.5% annually, driven by strong manufacturing infrastructure, cost advantages, and proximity to key manufacturers.

Significant opportunities include expansion of stationary energy storage systems for grid stabilization and renewable energy integration, with leading battery manufacturers collectively procuring cathode materials approaching 6 million tonnes valued at over RMB 24 million in 2025 across diversified applications.