- Automotive Components & Materials

- Electric Vehicle Battery Market

Electric Vehicle Battery Market Share, and Growth Forecast, 2025 - 2032

Electric Vehicle Battery Market By Battery Type (Lithium-ion Battery, Others), Propulsion Type (Battery Electric Vehicle (BEV, Others), Vehicle Type (2Ws, 3Ws, Others), and Regional Analysis for 2025 - 2032

Electric Vehicle Battery Market Share and Trends Analysis

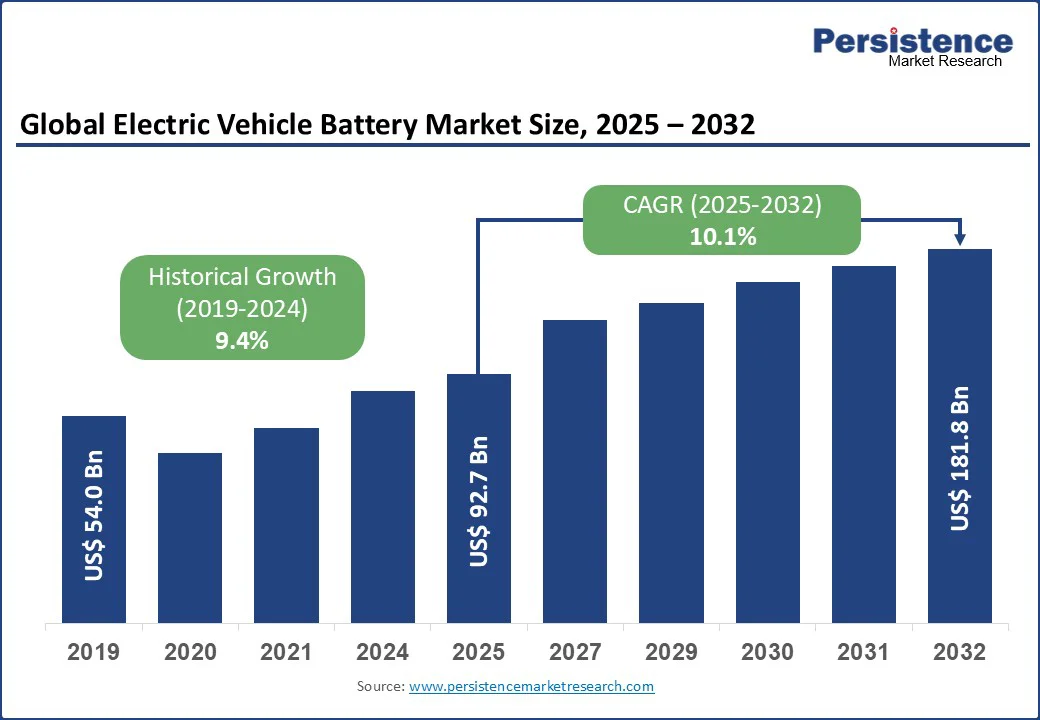

The global electric vehicle battery market size is likely to be valued at US$92.7 Bn in 2025 and is expected to reach US$181.8 Bn by 2032, growing at a CAGR of 10.1% during the forecast period from 2025 to 2032. Surging electric vehicle (EV) sales, which reached 17 million units in 2024, coupled with government subsidies and clean energy policies, are fueling rapid growth.

Technological advancements in lithium-ion and solid-state batteries, which offer higher energy density, longer driving ranges, and faster charging, are boosting adoption worldwide. With increasing investments in EV battery manufacturing and recycling, the EV battery market outlook remains highly positive, positioning it as a critical driver in the global shift toward sustainable mobility and clean transportation solutions.

Key Industry Highlights

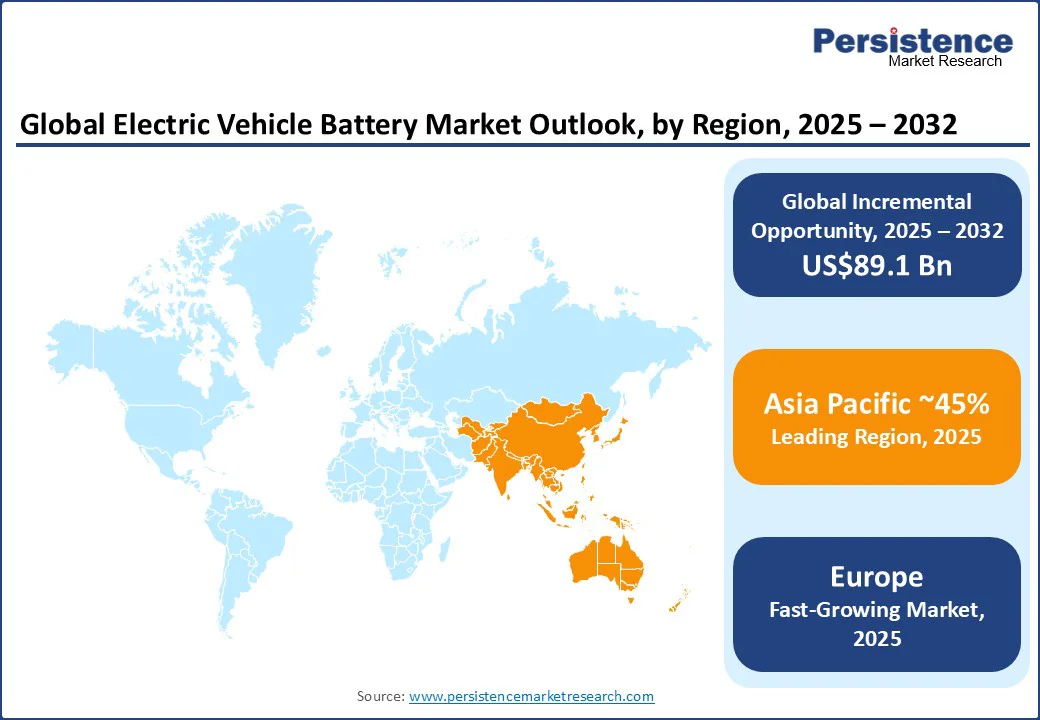

- Leading Region: Asia Pacific is anticipated to lead with 45% market share, supported by strong EV production in China, Japan, and South Korea.

- Fastest-growing Region: Europe is projected to be the fastest-growing region, accounting for 25% of the market share, driven by strict emission norms, rising EV adoption, and strong investments in gigafactories.

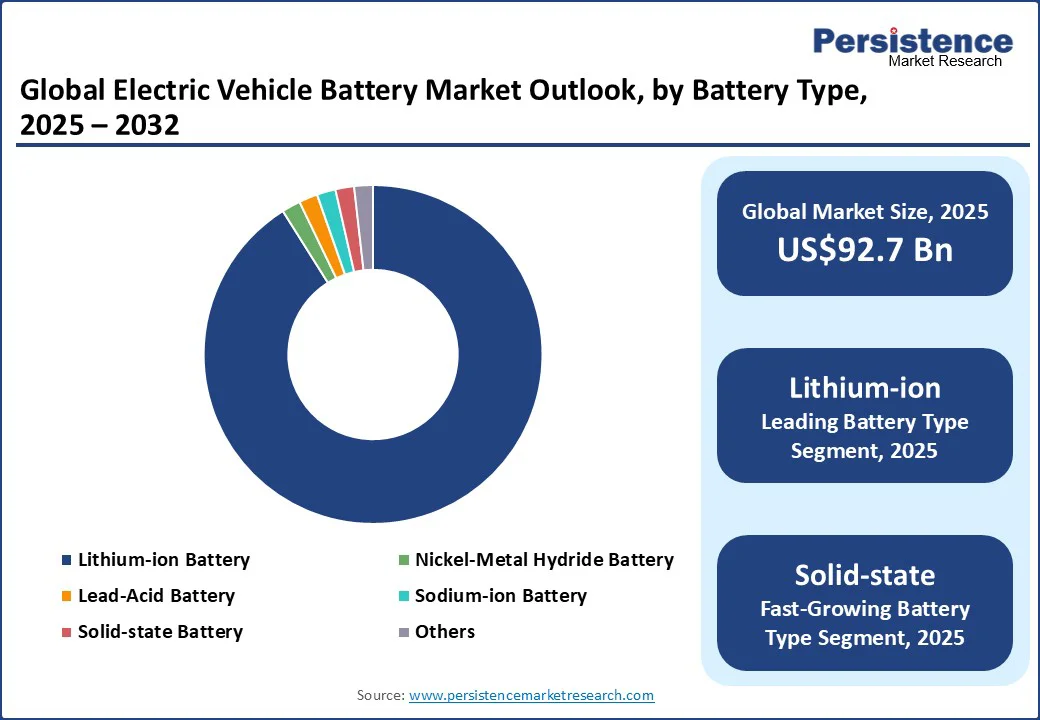

- Dominant Batter Type: Lithium-ion batteries are anticipated to dominate with over 85% share, while solid-state batteries emerge as the fastest-growing technology offering higher energy density and safety.

- Leading Propulsion Type: Battery Electric Vehicles (BEVs) are anticipated to remain the largest demand segment, while passenger EVs lead adoption across major markets.

|

Global Market Attribute |

Key Insights |

|

Large Language Model Size (2025E) |

US$92.7 Bn |

|

Market Value Forecast (2032F) |

US$181.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

10.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.4% |

Market Dynamics

Driver - Increasing Electric Vehicle Sales Boost Battery Demand Across the Globe

The global EV battery market is expanding rapidly, fueled by the surge in EV adoption worldwide. In 2024, electric car sales surpassed 17 million units, reflecting a 25% annual increase, with China contributing nearly 60% of the total volume. The trend continued in 2025, as over 4 million EVs were sold in the first quarter alone, highlighting strong global momentum. This surge in EV penetration has directly elevated battery demand, which exceeded 950 GWh in 2024 and pushed total global demand beyond 1 TWh.

The declining cost of lithium-ion batteries, falling below US$100/kWh, is making EVs more affordable and driving consumer preference over internal combustion vehicles. Supported by government incentives, stricter emission regulations, and sustainability goals such as the EU’s zero-emission bus target by 2035, rising EV adoption remains the most critical growth driver in the global EV battery market.

Restraint - Supply Chain Vulnerabilities Pose Significant Challenges

The global EV battery market faces a major restraint in the form of supply chain vulnerabilities, primarily due to heavy reliance on a few countries for critical raw materials. China currently dominates the mining, refining, and processing of essential inputs such as lithium, graphite, cobalt, and rare earth metals, which are vital for large-scale battery manufacturing. Recent Chinese export restrictions on graphite have intensified concerns about potential supply disruptions, price volatility, and long-term availability of resources.

Although governments, particularly in the U.S. and Europe, are investing in domestic supply chains to reduce dependency, significant gaps remain in mining, refining, and processing capacities. This overdependence on China creates risks of material shortages, unstable costs, and bottlenecks that could hinder EV battery market growth. While companies are actively exploring alternative sourcing and investing in local production, building these capabilities requires considerable time and capital, leaving supply chain risks a persistent challenge.

Opportunity - Innovations in Battery Technologies Present Significant Growth Opportunities

The global EV battery market is witnessing significant opportunities driven by rapid innovations in battery technologies, which are addressing key challenges such as long charging times, limited driving ranges, and high production costs. In 2025, Nyobolt secured US$30 Mn to scale ultra-fast-charging batteries capable of reaching 80% charge in under five minutes, compared to the 30–45 minutes required by conventional lithium-ion batteries.

Leading automakers are also accelerating research in solid-state batteries, with Toyota planning to launch EVs powered by this technology by 2027, promising up to 1,200 kilometers (750 miles) per charge and complete charging in just 10 minutes. Solid-state batteries offer greater energy density, improved safety, and reduced fire risks compared to traditional chemistries.

Companies such as QuantumScape, CATL, and LG Energy Solution are actively investing in next-generation battery chemistries, while strategic collaborations with global automakers are paving the way for advanced, high-performance EV battery solutions worldwide.

Category-wise Analysis

Battery Type Insights

Lithium-ion batteries are projected to dominate the global EV battery market in 2025, accounting for more than 85% of total installations. These batteries remain the preferred technology due to their high energy density, long lifecycle, lightweight design, and fast-charging capability, making them ideal for both passenger EVs and commercial electric fleets. Within this segment, LFP (Lithium Iron Phosphate) batteries are gaining remarkable traction, particularly in cost-sensitive regions such as China and India. Their affordability, safety features, and superior thermal stability make them highly suitable for budget EVs, mid-range cars, and electric two-wheelers, ensuring strong demand in emerging markets.

Solid-state batteries represent the fastest-growing segment of the EV battery industry, supported by advancements in battery chemistry and rising investments from global automakers. Offering longer driving ranges, improved safety, higher energy density, and ultra-fast charging, solid-state batteries eliminate the use of flammable liquid electrolytes, reducing fire risks and enabling compact, high-performance battery packs. With companies such as Toyota, QuantumScape, CATL, and LG Energy Solution investing heavily in commercialization, solid-state batteries are expected to play a crucial role in the long-term growth of the electric vehicle battery market.

Propulsion Type Insights

Battery Electric Vehicles (BEVs) are expected to lead the global EV battery market, accounting for more than 70% of total demand in 2025. Powered exclusively by large-capacity lithium-ion battery packs, BEVs offer zero tailpipe emissions, lower operating costs, and improved driving ranges, making them the top choice for environmentally conscious consumers. Global automakers, including Tesla, BYD, Volkswagen, Hyundai, and BMW, are expanding their BEV portfolios across various price points, further accelerating the demand for advanced EV batteries.

Other propulsion categories, such as Plug-in Hybrid Electric Vehicles (PHEVs) and Fuel Cell Electric Vehicles (FCEVs), are also gaining momentum. PHEVs bridge the transition toward full electrification by combining a battery with an internal combustion engine. At the same time, FCEVs powered by hydrogen fuel cells deliver ultra-long range and rapid refueling, making them highly suitable for long-haul trucks and heavy-duty applications. Countries including Japan, South Korea, and Germany are investing in hydrogen refueling infrastructure, which will expand the role of fuel cell technology in the EV battery ecosystem between 2025 and 2032.

Vehicle Type Insights

Passenger EVs are expected to remain the largest contributor to the EV battery market size, driven by robust adoption in China, Europe, and North America. According to the International Energy Agency (IEA), global electric car sales crossed 17 million units in 2024, marking a 25% increase from the previous year. This surge is supported by stricter emission regulations, government subsidies, and aggressive net-zero targets, with leading automakers such as Tesla, Volkswagen, and BMW transitioning toward EV-only product lines. Passenger EVs dominate demand for high-capacity lithium-ion batteries, ensuring their position as the primary revenue-generating segment.

At the same time, electric two-wheelers (2Ws) are witnessing explosive growth, particularly in India, China, Vietnam, and Indonesia. Rising urbanization, last-mile connectivity needs, and government-backed incentives are driving consumers toward affordable electric scooters and motorcycles. While individual 2W batteries are relatively small (1–3 kWh), the massive sales volume across emerging economies significantly boosts demand for EV batteries. The rapid adoption of electric two-wheelers, alongside growth in passenger cars and commercial EVs, underscores the expanding opportunities within the global electric vehicle battery industry.

Regional Insights

North America Electric Vehicle Battery Market Trends

North America is projected to hold around one-fifth of the global EV battery market in 2025, driven by strong EV adoption trends, lithium-ion battery demand, and government incentives for sustainable mobility. The U.S. dominates the region, contributing over 80% of the market share due to the Inflation Reduction Act (IRA), which offers tax credits for both EV purchases and domestic battery manufacturing. Falling battery pack costs, rising consumer preference for zero-emission vehicles, and robust investments in EV infrastructure and gigafactories further strengthen market growth.

Canada is emerging as a key country, focusing on EV battery production, assembly, and recycling to achieve its clean energy targets. North America’s growth is also fueled by collaborations between automakers and battery producers to scale advanced lithium-ion and next-generation solid-state battery technologies, ensuring long-term market expansion.

Europe Electric Vehicle Battery Market Trends

Europe is expected to capture approximately one-fourth of the global EV battery market in 2025, led by aggressive emission reduction policies, BEV adoption, and localized battery production. Germany remains the regional leader with strong investments in gigafactories, solid-state battery R&D, and advanced energy storage systems. Norway continues to set the benchmark with nearly 90% of new car sales being electric in 2023. France is rapidly scaling domestic battery production and assembly facilities to support the increasing EV demand.

Europe is also advancing battery recycling programs, circular economy initiatives, and next-generation chemistries to enhance sustainability. The dominance of the passenger car EV segment, coupled with growing interest in electric commercial vehicles, ensures Europe remains a critical hub for lithium-ion and solid-state battery technologies.

Asia Pacific Electric Vehicle Battery Market Trends

Asia Pacific leads the global EV battery market, accounting for 45% of the total share in 2025, driven by China, Japan, and India. The region benefits from rapid urbanization, economies of scale in battery manufacturing, and abundant raw materials such as lithium, cobalt, and graphite, reducing production costs. China alone produces over 70% of the world’s lithium-ion batteries and accounted for 12.87 million EV Car sales in 2024, creating enormous domestic battery demand. Market leaders such as CATL, BYD, and CALB are driving innovation in high-capacity EV batteries, solid-state chemistries, and fast-charging solutions.

India’s EV battery market is expanding rapidly, driven by the electrification of two-wheeler and three-wheeler vehicles, as well as government initiatives like FAME II and PLI incentives that promote local battery production. The region’s growth is further supported by battery recycling initiatives, sustainable production practices, and electric bus adoption, solidifying Asia Pacific’s position as the largest EV battery hub globally.

Competitive Landscape

The global electric vehicle battery market is highly competitive, dominated by leading manufacturers such as CATL, LG Energy Solution, Panasonic, BYD, and Samsung SDI. These top EV battery companies are driving growth through large-scale production, cutting-edge lithium-ion and solid-state battery technologies, and optimized supply chains to meet the rising global EV demand.

Strategic partnerships and technological innovations are accelerating EV battery market expansion. CATL’s high-energy density LFP batteries, LG Energy Solution’s collaboration with GM, and Panasonic’s advanced solid-state batteries enhance driving range, safety, and fast charging. Rising EV adoption, government incentives, and continuous R&D position the global EV battery market for rapid growth, making it a dynamic, innovation-driven sector with immense long-term opportunities.

Key Industry Developments

- In March 2025, Contemporary Amperex Technology Co. Ltd. (CATL), the world’s largest EV battery manufacturer, unveiled its next-generation high-energy density lithium iron phosphate (LFP) battery. The new battery featured a 20% increase in energy density compared to its previous models, significantly improving the driving range of EVs.

- In February 2025, LG Energy Solution and General Motors (GM) announced an expanded partnership to supply Ultium battery cells for GM's next-generation electric vehicles. This deal focused on manufacturing high-performance batteries with improved energy density and cost efficiency at GM’s upcoming battery production facilities in the U.S.

- In January 2025, Panasonic announced significant advancements in its solid-state battery technology for electric vehicles. The new solid-state batteries provided twice the energy density of conventional lithium-ion batteries, which could lead to longer ranges and faster charging times for EVs.

Companies Covered in Electric Vehicle Battery Market

- Contemporary Amperex Technology Co., Ltd. (CATL)

- LG Energy Solution

- BYD Company Ltd.

- Panasonic Corp.

- Samsung SDI Co., Ltd.

- SK Innovation Co., Ltd.

- Toshiba Corporation

- EnerSys, Inc.

- Hitachi, Ltd.

- Mitsubishi Corp.

- Gotion

- Northvolt

- Farasis Energy

Frequently Asked Questions

The global electric vehicle battery market size is projected to exceed US$92.7 Bn in 2025, driven by rapid lithium-ion battery adoption, solid-state battery innovations, and rising electric vehicle sales worldwide.

Asia Pacific dominates the electric vehicle battery market, holding nearly 45% of global market share in 2025, led by China, Japan, and India due to high EV production, battery manufacturing capacity, and abundant raw materials.

North America’s growth is fueled by declining battery costs, EV adoption, the U.S. Inflation Reduction Act (IRA), gigafactory expansions, and solid-state battery development.

Europe is advancing localized battery production, solid-state R&D, battery recycling initiatives, and BEV adoption, with Germany, Norway, and France leading the market.

High-volume EV sales, economies of scale in battery manufacturing, government incentives, raw material availability, and innovations by CATL, BYD, and CALB drive the Asia Pacific market.