- Energy Storage Solutions

- Marine Lithium-ion Battery Market

Marine Lithium-ion Battery Market Size, Share, and Growth Forecast 2026 - 2033

Marine Lithium-ion Battery Market by Battery Type (12 V, 24 V, 36 V, 48 V, 60 V, 72 V, Others), Application (Propulsion Systems, Auxiliary Power, Emergency Power Systems, Lighting and Electronics), Ship Type (Fishing Boats, Luxury Yachts, Cargo Ships, Military Ships, Others), and Regional Analysis, 2026 - 2033

Marine Lithium-ion Battery Market Size and Trend Analysis

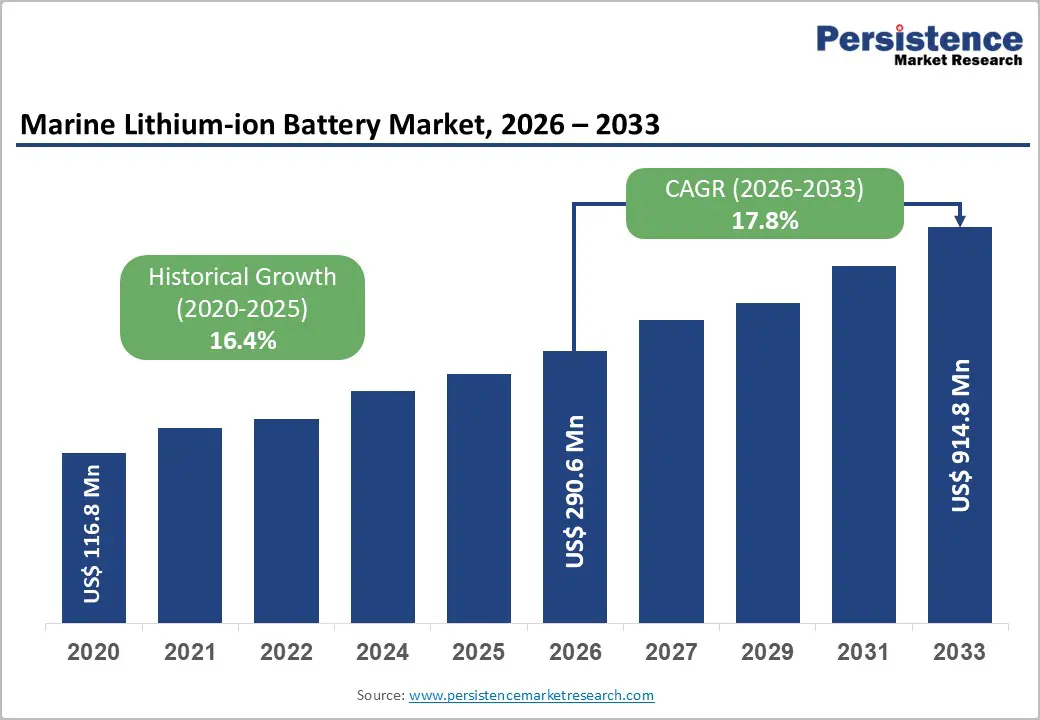

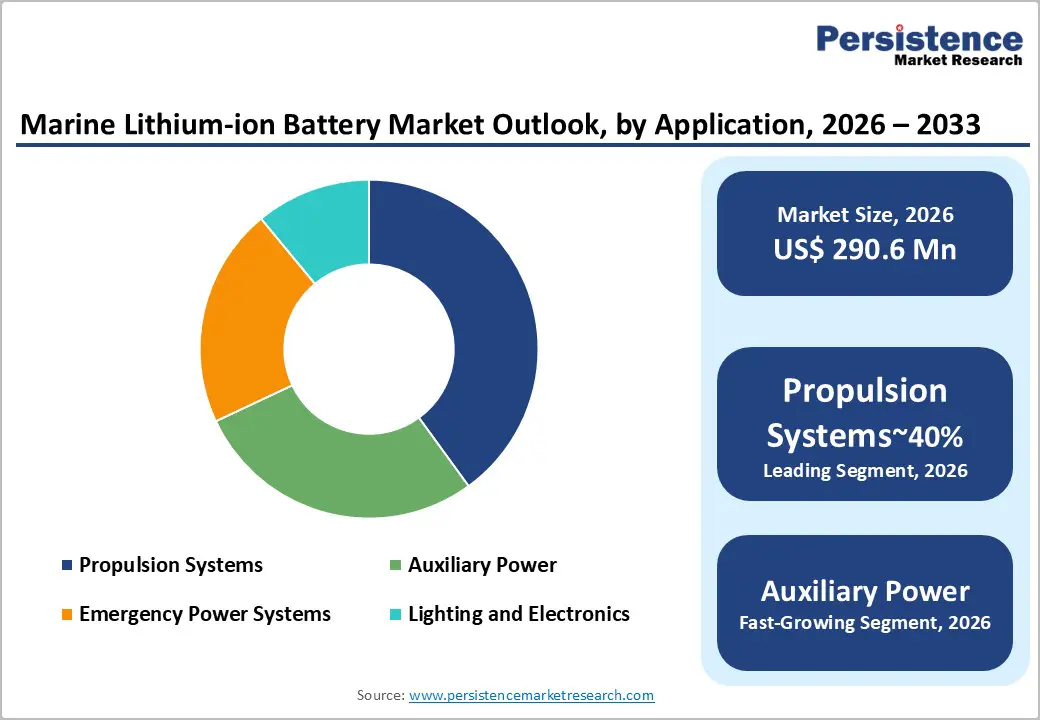

The global Marine Lithium-ion Battery Market size is likely to be valued at US$ 290.6 Million in 2026 and is expected to reach US$ 914.8 Million by 2033, growing at a CAGR of 17.8% during the forecast period from 2026 to 2033. Stringent decarbonization mandates and electrification of fleets propel this surge, prioritizing lithium-ion over lead-acid for efficiency.

Key Industry Highlights:

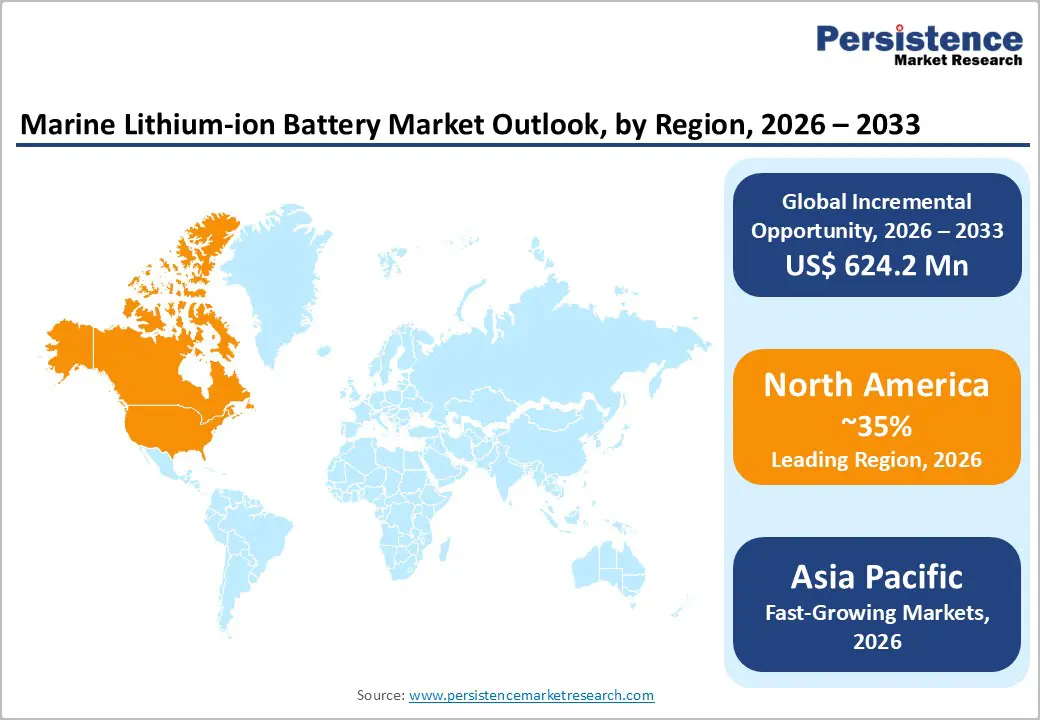

- Leading Region: North America leads as the dominant region, accounting for 35% share, remains a strong innovation hub for marine lithium-ion battery development.

- Fastest Growing Region: Asia Pacific fastest-growing region with a rising CAGR of 19.7%, powered by China's manufacturing and India's shipbuilding subsidies.

- Leading Segment: Propulsion Systems dominate applications with 40% share, enabling fuel savings in cargo vessels.

- Fastest Growing Segment: 48 V batteries grow fastest, suiting mid-power hybrid needs per IEC standards.

- Key opportunity in cargo ship retrofits, aligning with IMO net-zero goals for emission reductions.

| Key Insights | Details |

|---|---|

|

Marine Lithium-ion Battery Market Size (2026E) |

US$ 290.6 Million |

|

Market Value Forecast (2033F) |

US$ 914.8 Million |

|

Projected Growth CAGR(2026-2033) |

17.8% |

|

Historical Market Growth (2020-2025) |

16.4% |

Market Dynamics

Drivers - Global emission regulations and hybrid propulsion mandates accelerate marine lithium-ion battery adoption across commercial shipping fleets

Growing global regulatory pressure to reduce emissions in the shipping industry is strongly driving the adoption of marine lithium-ion batteries, particularly for hybrid propulsion systems that significantly lower fuel consumption and carbon output. The International Maritime Organization (IMO) 2023 strategy targets net-zero emissions by 2050, encouraging shipowners to adopt cleaner technologies.

The European Union’s MRV framework has already reported nearly 15% improvement in fleet efficiency through battery-supported systems. According to DNV, around 40% of newbuild vessels are expected to integrate lithium-ion batteries by 2025, with trials by the American Bureau of Shipping showing up to 25% reduction in diesel usage. With higher energy density ranging between 150–250 Wh/kg compared to 50 Wh/kg for lead-acid batteries, lithium-ion solutions enable longer operational ranges. This makes them attractive for operators navigating a shipping sector responsible for nearly $3 trillion in annual trade-related emissions.

Expansion of offshore wind and marine renewables increases demand for reliable lithium-ion battery energy storage systems

The rapid expansion of offshore wind farms and aquaculture projects is creating strong demand for reliable marine energy storage solutions. Offshore platforms require a stable and continuous power supply, and lithium-ion batteries help balance load fluctuations while reducing reliance on diesel generators. The Global Wind Energy Council forecasts offshore wind capacity to reach 234 GW by 2030, significantly increasing the need for integrated storage systems.

According to IRENA, marine battery costs have declined by nearly 30% since 2020, improving commercial viability. Projects in Norway, including installations led by Equinor, have successfully used lithium-ion systems to enhance platform stability and reduce generator fuel consumption by around 20%. Compliance with IEC 62619 safety standards further strengthens market confidence. As renewable energy infrastructure expands into remote marine environments, batteries play a critical role in ensuring reliability, efficiency, and smoother integration of clean power sources.

Restraints - Elevated battery costs and limited port charging infrastructure restrict widespread marine lithium-ion adoption

Despite strong demand, high upfront costs remain a major barrier to large-scale adoption of marine lithium-ion batteries. Lithium-ion systems are typically two to three times more expensive than traditional lead-acid alternatives, making retrofitting projects financially challenging for many operators. BloombergNEF data shows lithium prices peaked at nearly $80,000 per ton in 2022, pushing battery pack prices close to $500 per kWh. Although prices are gradually stabilizing, capital expenditure remains significant.

In addition, charging infrastructure at ports is still underdeveloped. Surveys by the U.S. Coast Guard indicate that only about 25% of ports are expected to have adequate charging facilities by 2025. This infrastructure gap slows commercialization and increases uncertainty for shipowners considering battery integration. Without stronger policy incentives and port electrification investments, cost concerns may continue to limit adoption across smaller fleets and developing maritime regions.

Thermal runaway, vibration stress, and saltwater exposure raise safety concerns for marine lithium-ion batteries

Safety concerns remain another key restraint, particularly given the harsh conditions in marine environments. Lithium-ion batteries face risks such as thermal runaway, fire hazards, and corrosion due to saltwater exposure. The U.S. Coast Guard reported 12 lithium-ion–related incidents in 2024, compared to a much lower incident rate for lead-acid systems. Vibration and mechanical stress at sea can further increase failure risks, with Lloyd’s Register noting an 18% rise in vibration-induced issues.

Inconsistent compliance with marine safety standards also adds to operational uncertainty. While manufacturers are investing in improved battery management systems and enhanced containment technologies, concerns over fire suppression, crew safety, and insurance costs continue to affect purchasing decisions. Strengthening adherence to international safety standards and improving onboard monitoring systems will be critical to building greater industry confidence in lithium-ion battery deployment.

Opportunities - High-voltage lithium-ion systems unlock efficiency and range improvements for large commercial and defense vessels

Significant growth opportunities exist in the development of high-voltage lithium-ion battery systems, particularly in the 48V to 72V range for larger cargo and military vessels. These systems support higher propulsion loads while maintaining improved safety and efficiency standards. Ongoing hybrid trials by the U.S. Navy are expected to demonstrate up to 40% range extension, highlighting the operational advantages of advanced battery systems.

Industry bodies in Europe estimate a potential 25% CAGR for high-voltage marine battery applications as shipowners seek greater fuel savings and compliance with emission regulations. The EU Battery Regulation introduced in 2023 also provides incentives for research and development, accelerating innovation in marine-grade storage systems. Demonstration projects by major engineering firms have achieved uptime levels close to 95%, proving reliability. As demand grows for cleaner propulsion in large commercial fleets, high-voltage lithium-ion solutions present strong long-term revenue potential.

Government-backed retrofit programs in Asia Pacific drive lithium-ion adoption across fishing and ferry fleets

Retrofitting existing fishing boats and ferry fleets presents a strong volume opportunity, particularly across Asia Pacific where governments are gradually reducing fuel subsidies and promoting greener maritime practices. According to FAO estimates, around 4.6 million small and mid-sized vessels globally require modernization, creating substantial retrofit demand. ASEAN countries have introduced green shipping agreements targeting 20% electrification by 2030, encouraging battery adoption in short-distance operations.

In India, recent initiatives by the Ministry of Ports, Shipping and Waterways aim to support up to 15% fleet conversion through financial assistance programs. Modular lithium-ion battery packs are particularly suitable for ferries and coastal vessels due to their compact design and scalability. As operators seek lower operating costs and improved compliance with environmental policies, retrofitting programs across Asia Pacific are expected to generate steady and scalable demand growth.

Category-wise Analysis

Battery Type Insights

48V batteries currently lead the battery type segment with approximately 35% market share, as they offer an optimal balance between power output, safety, and operational efficiency. These systems are widely used in mid-range propulsion and auxiliary applications across yachts, ferries, and cargo vessels. Certification under IEC 62620 standards confirms durability beyond 200 charge cycles in marine conditions. Testing by U.S. energy authorities indicates that 48V systems can effectively support nearly 70% of auxiliary onboard loads, making them highly practical for hybrid configurations.

Compared to lower voltage alternatives, 48V batteries deliver improved efficiency without the complexity of very high-voltage installations. Their strong performance record, combined with regulatory support for hybrid propulsion, positions them as a preferred solution for shipowners seeking reliable and scalable marine battery systems.

Application Insights

Propulsion systems account for nearly 40% of total application share, making them the dominant use case for marine lithium-ion batteries. The increasing enforcement of emission efficiency measures under IMO’s Energy Efficiency Existing Ship Index (EEXI) is accelerating the shift toward hybrid and fully electric propulsion solutions. Trials conducted by leading marine engine manufacturers demonstrate fuel savings of up to 35% when batteries are integrated into propulsion systems.

Lithium-ion batteries provide high discharge rates, often up to 5C, enabling rapid acceleration and smooth maneuverability, which is particularly valuable in port operations and short-sea routes. Their ability to store excess energy and support peak shaving further enhances fuel efficiency and engine lifespan. As shipowners prioritize operational savings and regulatory compliance, battery-supported propulsion systems are expected to remain the largest and fastest-growing application segment in the marine lithium-ion battery market.

Ship Type Insights

Cargo ships represent around 40% of total demand by ship type, driven by their scale, high fuel consumption, and growing retrofitting initiatives. According to global maritime trade reviews, more than 90,000 vessels above 1,000 gross tonnage operate worldwide, creating a large addressable market. Major shipping companies have already introduced hybrid systems capable of reducing carbon emissions by approximately 20%.

Regulatory pressure on large fleets to comply with international emission standards further accelerates adoption. Classification approvals for marine lithium-ion battery packs have simplified integration into newbuild and retrofit projects. Cargo vessels benefit significantly from fuel savings during port operations and slow steaming, where battery support improves efficiency. Given their large operational footprint and regulatory exposure, cargo ships will continue to lead demand for advanced marine battery technologies in the coming years.

Regional Insights

North America Marine Lithium-ion Battery Trends

North America, led by the United States, remains a strong innovation hub for marine lithium-ion battery development. Regulatory frameworks from agencies such as the U.S. Coast Guard and maritime authorities emphasize safety compliance and battery certification standards. Government-backed research programs, including advanced energy funding initiatives, have enabled the development of battery systems reaching energy densities up to 250 Wh/kg.

Adoption of electric propulsion in recreational yachts and ferries is steadily increasing, supported by port electrification programs and environmental compliance measures. Domestic manufacturers are expanding production capacity to meet rising demand, particularly in coastal states with strict emission regulations. Incentives such as R&D tax credits and clean energy grants further encourage investment in industry. With a strong regulatory foundation and growing hybrid vessel adoption, North America continues to position itself as a technology-driven market for marine battery innovation.

Europe Marine Lithium-ion Battery Trends

Europe is advancing rapidly in marine electrification, supported by unified environmental regulations under the EU Green Deal and strict maritime emission policies. Countries such as Germany and Norway are leading the transition, with a significant share of hybrid vessels already operating in coastal routes. European ferry operators have successfully deployed battery-powered systems capable of reducing emissions by nearly 50%.

Regional classification societies actively certify advanced 72V and higher voltage systems for offshore and commercial use. Public funding programs and green financing initiatives further accelerate adoption across shipyards and fleet operators. The region’s strong focus on sustainability, combined with collaboration between engineering companies and maritime yards, creates a mature ecosystem for innovation. As regulatory pressure intensifies, Europe is expected to remain at the forefront of marine lithium-ion battery deployment and hybrid vessel development.

Asia Pacific Marine Lithium-ion Battery Trends

Asia Pacific represents the fastest-growing regional market, supported by large-scale battery manufacturing and expanding shipbuilding capacity. China accounts for a substantial share of global lithium processing and battery exports, supplying key markets such as Japan and India. Major shipping companies in the region have initiated retrofit programs targeting dozens of cargo vessels as part of emission reduction strategies.

ASEAN nations are promoting cost-effective electrification solutions, particularly for ferries and short-distance coastal routes. India’s maritime development initiatives also encourage electrification of small fishing boats under modernization programs. Competitive manufacturing costs and government-backed industrial policies strengthen regional supply chains. With rising domestic demand and strong export capabilities, the Asia Pacific is well-positioned to lead production and adoption of marine lithium-ion batteries over the next decade.

Competitive Landscape

The marine lithium-ion battery market remains moderately consolidated, with major technology companies holding a combined share of nearly 40% through vertical integration strategies. Leading players focus heavily on research and development, particularly in solid-state battery technology and enhanced safety systems. Strategic partnerships between battery manufacturers, shipyards, and engineering firms are becoming increasingly common to accelerate commercialization. Product differentiation centers on safety certifications, energy density improvements, and lifecycle performance.

Companies are also expanding direct-to-customer models in the recreational yacht segment, where customization and compact designs offer competitive advantages. Continuous investment in innovation, combined with compliance with international marine safety standards, defines the competitive landscape. As demand grows for cleaner propulsion solutions, established players with strong technical expertise and global supply networks are expected to maintain market leadership while new entrants target niche retrofit opportunities.

Key Developments:

- In June, 2025: Samsung SDI entered a strategic collaboration with Hyundai’s maritime division to develop lithium-ion propulsion batteries tailored for cargo ships, aiming to meet future IMO emission compliance standards and improve energy efficiency in heavy marine applications.

- In October, 2024: Mastervolt expand its marine portfolio with IP67-rated lithium-ion batteries tailored for luxury yacht use, providing superior water resistance, enhanced offshore range, and integrated battery management to deliver reliable high-performance power for leisure vessel operations.

Companies Covered in Marine Lithium-ion Battery Market

- Arkema Group

- BASF Petronas Chemicals Sdn. Bhd.

- Bax Chemicals

- DowDuPont, Inc.

- Eastman Chemical Company

- Evonik Industries AG

- ExxonMobil Chemical Company

- INEOS Group

- LG Chem Ltd.

- Oxea Corporation

- Siemens

- MG Energy Systems

- Mastervolt

- Samsung SDI

- Trojan Battery Company

- Corvus Energy

- Kokam

- Saft Batteries

Frequently Asked Questions

Valued at US$ 290.6 Million in 2026, reaching US$ 914.8 Million by 2033 at 17.8% CAGR, driven by electrification.

IMO decarbonization and hybrid propulsion needs, cutting fuel 30-50% per DNV data.

Propulsion Systems at 40% share, powering emission reductions in cargo ships.

Europe dominates via EU Green Deal and Norway's advanced hybrid fleets.

High-voltage systems for cargo retrofits, supported by IMO incentives and naval trials.