- Bulk Chemicals

- Battery Chemicals Market

Battery Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Battery Chemicals Market by Chemical Type (Lithium Chemicals, LiPF6, LiFSI, LiOH, Li2CO3, Li2SO4, Others; Carbonates, EC, DMC, VC, FEC; Sulfates, NiSO4, CoSO4, MnSO4; Others, H2SO4, KOH, NaPF6, Others), Application (Cathode, Anode, Electrolyte, Binders & Conductive Additives, Others), Battery Type (Lithium-ion, Lead-acid, Nickel-based, Sodium-ion, Others), and Regional Analysis, 2026 - 2033

Battery Chemicals Market Size and Trend Analysis

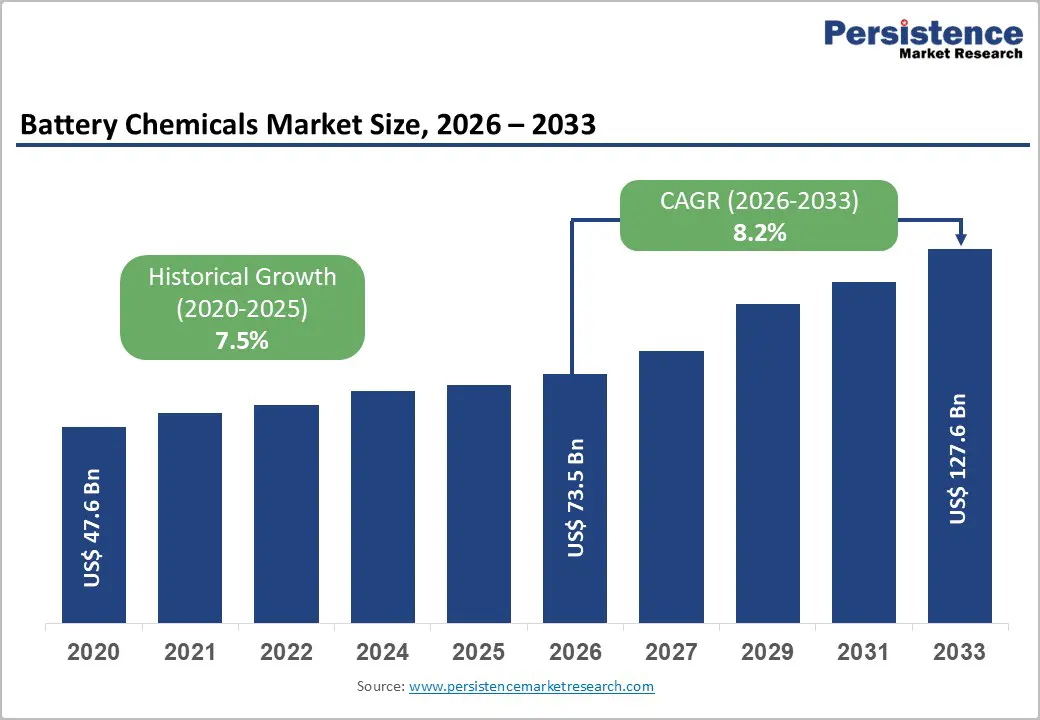

The global battery chemicals market size is expected to be valued at US$ 73.5 billion in 2026 and projected to reach US$ 127.6 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033.

This robust and sustained growth is primarily driven by the global electric vehicle (EV) revolution and the accelerating deployment of grid-scale energy storage systems, both of which are generating unprecedented demand for lithium-ion battery production and, by direct extension, for the full spectrum of battery chemicals, including lithium salts, transition metal sulfates, carbonate solvents, and electrolyte additives, that constitute the fundamental building blocks of advanced battery cell chemistries. Sweeping government mandates targeting internal combustion engine phase-outs across the European Union, United States, China, and India, combined with aggressive renewable energy integration targets that require large-scale stationary energy storage, are creating a structurally durable, policy-reinforced demand environment for battery chemicals manufacturers and their upstream raw material suppliers through the forecast period and well into the 2030s.

Key Industry Highlights:

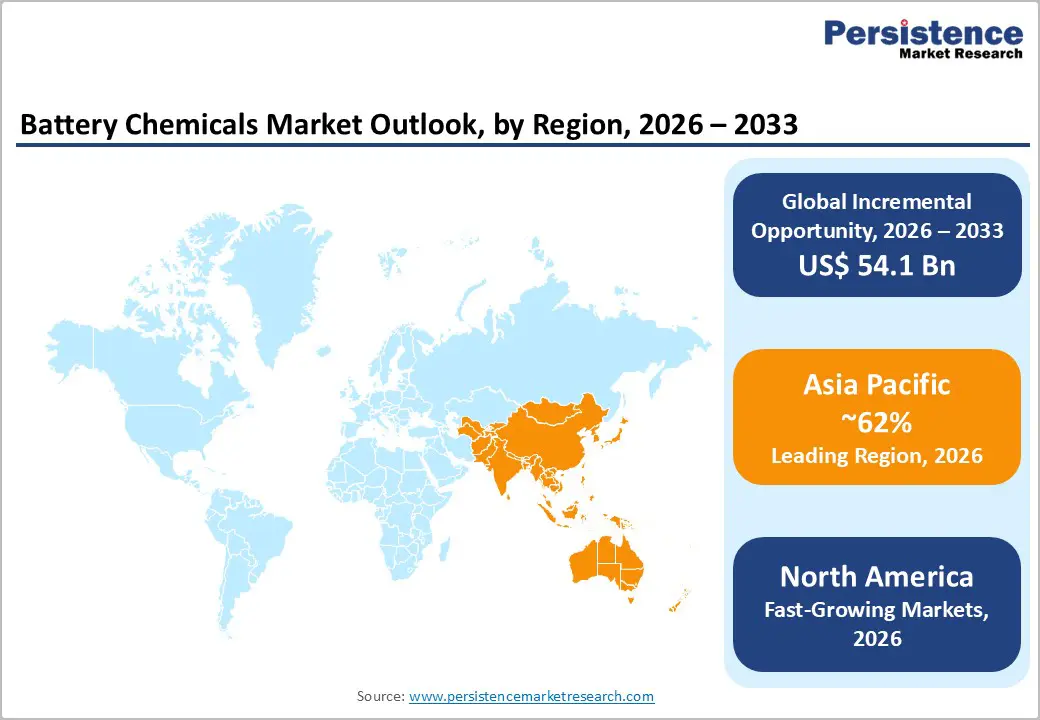

- Leading Region: Asia Pacific leads the global Battery Chemicals Market with about 62% share in 2025, driven by China’s dominant lithium refining capacity and large-scale regional battery manufacturing.

- Fastest Growing Region: North America is the fastest-growing market outside Asia, supported by Inflation Reduction Act incentives and accelerating domestic gigafactory investments.

- Dominant Chemicals: Lithium chemicals account for roughly 44% of market share in 2025, reflecting their central role in cathode production and electrolyte systems.

- Fastest Growing Chemical Segment: Sodium-ion batteries are the fastest-growing segment, creating rising demand for sodium-based salts and alternative anode and cathode chemistries.

- Key Opportunity: LiFSI adoption represents a high-margin opportunity as advanced battery cells increasingly shift from LiPF6 to improve thermal stability and performance.

| Key Insights | Details |

|---|---|

| Battery Chemicals Market Size (2026E) | US$ 73.5 Billion |

| Market Value Forecast (2033F) | US$ 127.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.2% |

| Historical Market Growth (2020 - 2025) | 7.5% |

Market Dynamics

Drivers - Explosive Electric Vehicle Adoption Generating Structural, Multi-Decade Battery Chemical Demand

The global electrification of transportation is the dominant structural driver underpinning battery chemicals demand growth. The International Energy Agency (IEA) reported that global electric vehicle sales reached 14 million units in 2023, representing approximately 18% of total global car sales, a share the agency projects will rise to 60% by 2030 under its Stated Policies Scenario and even higher under accelerated transition pathways. Each battery electric vehicle (BEV) manufactured requires a lithium-ion battery pack containing substantial quantities of battery-grade chemicals, including lithium hydroxide (LiOH) or lithium carbonate (Li2CO3) for cathode active material synthesis, nickel sulfate (NiSO4) and cobalt sulfate (CoSO4) for high-nickel NMC cathode formulations, and lithium hexafluorophosphate (LiPF6) for electrolyte salt systems. The U.S. Inflation Reduction Act (IRA), the EU Battery Regulation (2023/1542), and China’s New Energy Vehicle (NEV) industrial policy are collectively ensuring that EV production scales rapidly across all major markets, creating a demand pull of extraordinary magnitude for battery chemical suppliers across the entire value chain.

Accelerating Grid-Scale Energy Storage Deployment Diversifying and Expanding the Battery Chemical Demand Base

Beyond transportation, the accelerating global deployment of utility-scale battery energy storage systems (BESS) is emerging as an increasingly significant and diversified demand driver for battery chemicals. The IEA projects that global energy storage capacity additions must reach approximately 1,500 GW by 2030 under net-zero emissions pathways, a more than sixfold increase from current installed capacity, driven by the need to balance intermittent solar and wind generation in decarbonizing electricity grids. Grid-scale storage applications, predominantly utilizing lithium iron phosphate (LFP) battery chemistry, drive significant consumption of lithium chemicals (particularly Li2CO3), iron phosphate, and carbonate electrolyte solvents. The U.S. Department of Energy (DOE) has committed substantial funding under the Grid Deployment Office to accelerate domestic BESS manufacturing and battery chemical supply chain development, while the EU’s Net-Zero Industry Act establishes strategic battery manufacturing capacity targets that will drive European battery chemical demand across the forecast period. This grid storage megatrend is progressively broadening the battery chemicals demand base beyond automotive, providing market participants with a more diversified and resilient revenue foundation.

Restraints - Critical Raw Material Supply Concentration and Geopolitical Risk Threatening Supply Chain Stability

The battery chemicals market is acutely exposed to supply chain concentration risk arising from the geographic concentration of critical raw material production. The U.S. Geological Survey (USGS) reports that Chile and Australia collectively account for approximately 75% of global lithium production, while the Democratic Republic of Congo (DRC) supplies over 70% of the world’s cobalt. China’s dominant role in battery chemical processing, controlling an estimated 60-80% of global lithium chemical refining capacity according to the IEA, introduces significant geopolitical supply chain risk for Western battery manufacturers and OEMs. Disruptions to these concentrated supply nodes, from regulatory actions, export restrictions, or political instability, can cause severe raw material shortages and price volatility that compress battery chemical producer margins and disrupt downstream cell manufacturing schedules globally.

Volatility in Lithium and Transition Metal Prices Creating Significant Margin Uncertainty

The battery chemicals market has experienced dramatic raw material price cycles that significantly complicate investment planning and margin management for producers. Benchmark lithium carbonate prices surged to approximately US$ 80,000 per metric ton in late 2022 before collapsing by over 80% through 2023 and into 2024, driven by the interplay of surging EV demand, speculative inventory build-up, and a subsequent demand correction. Cobalt prices have similarly exhibited high volatility, fluctuating between US$ 30,000 and US$ 80,000 per metric ton in recent years. This pricing instability creates significant challenges for battery chemical producers in contracting, inventory management, and long-term capacity investment decisions, while incentivizing battery manufacturers to accelerate cathode chemistry transitions toward lower-cobalt and cobalt-free formulations that can periodically disrupt demand structures for specific battery chemicals.

Opportunity - Next-Generation Sodium-Ion Battery Commercialization Opening a High-Growth Adjacent Chemical Market

The emerging commercial deployment of sodium-ion (Na-ion) battery technology represents one of the most strategically significant growth opportunities for battery chemical suppliers, creating an entirely new adjacent market for sodium-based electrolyte salts, cathode precursor materials, and compatible carbonate solvent systems. CATL (Contemporary Amperex Technology Co., Limited), the world’s largest battery manufacturer, commenced mass production of sodium-ion batteries in 2023 and has integrated them into commercial EV platforms, while BYD, HiNa Battery Technology, and Faradion (a Reliance Industries subsidiary) are advancing Na-ion commercialization across energy storage and mobility applications. Sodium-ion batteries utilize sodium hexafluorophosphate (NaPF6) or emerging sodium bis(fluorosulfonyl)imide (NaFSI) as electrolyte salts, alongside hard carbon anode materials and layered oxide or Prussian blue analog cathodes, creating new demand streams for battery chemical producers who can develop and supply these sodium-specific material platforms at commercial scale. The IEA identifies sodium-ion batteries as a promising technology for grid-scale storage due to their use of earth-abundant sodium rather than scarce lithium, potentially unlocking very large-volume applications that would generate substantial battery chemical demand through the forecast period.

Rising Adoption of Lithium bis(fluorosulfonyl)imide (LiFSI) as a Next-Generation Electrolyte Salt Creating a Premium Revenue Opportunity

The industry adoption of Lithium bis(fluorosulfonyl)imide (LiFSI) as a high-performance electrolyte salt, either replacing or supplementing the incumbent LiPF6, represents a compelling high-margin growth opportunity for battery chemical producers with LiFSI manufacturing capability. LiFSI offers superior thermal stability, improved ionic conductivity, better low-temperature performance, and significantly enhanced compatibility with silicon-containing anodes and solid-state electrolyte systems compared to conventional LiPF6. As battery cell manufacturers race to achieve higher energy density, wider operating temperature ranges, and longer cycle life to meet next-generation EV performance targets, LiFSI is increasingly specified in premium NMC 811 and NMC 9xx cell formulations by leading cell makers including Panasonic Energy, Samsung SDI, SK On, and LG Energy Solution. Nippon Shokubai, Shenzhen Capchem Technology, and Jiangsu Guotai Super Power are among the leading LiFSI producers scaling capacity. Given LiFSI’s approximately 3-5× higher price premium over LiPF6 per kilogram, expansion into LiFSI production represents a significant revenue quality improvement opportunity for battery chemical manufacturers through 2033.

Category-wise Analysis

Chemical Type Insights

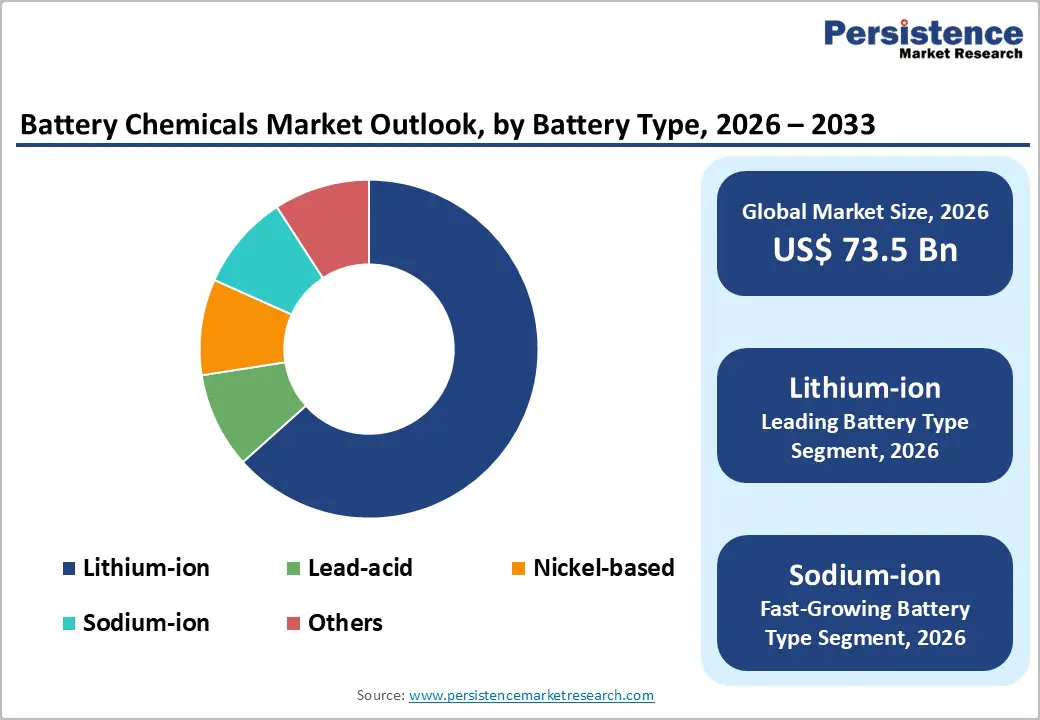

Lithium Chemicals dominated the global Battery Chemicals Market by chemical type, commanding approximately 44% of total market share in 2025. This commanding leadership position reflects lithium’s irreplaceable centrality in lithium-ion battery electrochemistry, serving as the active charge-carrying ion and as the fundamental input for cathode active materials, electrolyte salts, and certain anode coating applications. Lithium hydroxide (LiOH), used in the synthesis of high-nickel NMC and NCA cathode materials preferred in long-range EVs, and lithium hexafluorophosphate (LiPF6), the standard electrolyte salt in commercial lithium-ion batteries, are the highest-volume and highest-value lithium chemical products globally. Albemarle Corporation, the world’s largest lithium producer, and SQM (Sociedad Química y Minera de Chile) are globally significant producers of battery-grade lithium compounds. The accelerating shift toward higher-nickel cathode formulations is structurally increasing lithium hydroxide consumption per unit of cathode material, reinforcing lithium chemicals’ dominant market position. Carbonates represent the fastest-growing chemical type sub-segment, driven by booming electrolyte solvent demand as lithium-ion battery production scales globally.

Application Insights

The Cathode application segment dominated the global Battery Chemicals Market, representing approximately 46% of total market share in 2025. Cathode active materials are the most chemically complex and highest-cost component of a lithium-ion battery cell, accounting for approximately 30-40% of total cell manufacturing cost, and their production consumes the largest share of battery-grade lithium chemicals, transition metal sulfates (nickel sulfate, cobalt sulfate, manganese sulfate), and precursor processing materials. The progressive industry transition toward higher-nickel cathode chemistries, particularly NMC 811 (80% nickel, 10% manganese, 10% cobalt) and emerging NMC 9xx (90%+ nickel) formulations, is simultaneously increasing the per-kWh nickel sulfate consumption intensity while reducing cobalt sulfate requirements per cell. Leading cathode material producers including Umicore SA, Sumitomo Metal Mining Co., Ltd., Johnson Matthey PLC, and BASF SE are investing heavily in next-generation cathode precursor manufacturing capacity. Electrolyte represents the fastest-growing application segment, driven by scaling lithium-ion production volumes and the accelerating adoption of next-generation LiFSI electrolyte salt systems.

Battery Type Analysis

Lithium-ion batteries dominated the global Battery Chemicals Market by battery type, accounting for approximately 68% of total market share in 2025. Lithium-ion’s commanding leadership reflects its status as the overwhelmingly dominant battery technology across the entire spectrum of high-growth applications, electric vehicles, portable consumer electronics, grid-scale energy storage, and industrial equipment. The technology’s unmatched combination of high energy density, long cycle life, declining cost curve, and established global supply chain infrastructure makes it the de facto standard for virtually all new battery deployments of commercial significance. Leading global lithium-ion cell manufacturers, including CATL, BYD, LG Energy Solution, Panasonic Energy, Samsung SDI, and SK On, collectively operate gigawatt-scale manufacturing facilities that consume enormous annual volumes of battery-grade lithium chemicals, sulfate precursors, carbonate solvents, and conductive additives. Sodium-ion batteries represent the fastest-growing battery type segment, albeit from a nascent base, driven by the commercial scale-up efforts of CATL, HiNa Battery Technology, and multiple international new entrants entering the sodium-ion cell manufacturing space.

Regional Insights

North America Battery Chemicals Market Trends and Insights

North America is a rapidly growing battery chemicals market, leveraging the transformative policy momentum of the U.S. Inflation Reduction Act (IRA) to build a domestically integrated battery supply chain spanning raw material extraction, chemical processing, cell manufacturing, and EV assembly. The IRA’s battery manufacturing production credits, including US$ 35 per kWh for battery cell production and incentives for North American critical mineral sourcing, are catalyzing an unprecedented wave of gigafactory investment in the United States, with announced commitments from Ford (BlueOval SK), GM (Ultium Cells), Stellantis, Toyota, and Volkswagen collectively representing hundreds of billions of dollars in planned North American battery manufacturing capacity additions through 2030, directly stimulating demand for domestically sourced and processed battery chemicals.

On the supply side, Albemarle Corporation, headquartered in Charlotte, North Carolina, is expanding its Kings Mountain, North Carolina lithium hydroxide processing facility, targeting increased domestic battery-grade LiOH supply to serve North American cell manufacturers seeking IRA-compliant domestic content sourcing. The U.S. DOE’s Office of Manufacturing and Energy Supply Chains has allocated substantial funding through the Bipartisan Infrastructure Law for battery chemical processing facility construction, including grants supporting domestic electrolyte salt, cathode precursor, and separator manufacturing. Canada, with significant lithium, nickel, and cobalt mineral reserves, is increasingly positioned as a strategic upstream supplier to the North American battery chemical supply chain, aligned with the bilateral Critical Minerals Agreement between the U.S. and Canadian governments.

Europe Battery Chemicals Market Trends and Insights

Europe’s Battery Chemicals Market is experiencing significant structural growth, driven by the continent’s ambitious EV transition mandates, including the EU’s effective ban on new internal combustion engine vehicle sales from 2035, and the progressive build-out of a European domestic battery manufacturing ecosystem anchored by multiple gigafactories across Germany, Sweden, Poland, France, and Spain. The EU Battery Regulation (2023/1542), which came into force in August 2023, establishes mandatory recycled content requirements for battery chemicals, carbon footprint thresholds, and supply chain due diligence obligations that are reshaping sourcing strategies and stimulating investment in domestic battery chemical production. Germany hosts Volkswagen Group’s battery venture activities and BASF SE’s battery materials operations, cementing its role as Europe’s primary hub for battery chemical value addition.

Umicore SA (headquartered in Brussels, Belgium) is a leading European producer of cathode active materials and battery chemical precursors, with ongoing capacity expansion programs targeting growing NMC cathode demand from European gigafactories. Johnson Matthey PLC (United Kingdom) has advanced development of next-generation eLNO (enhanced lithium nickel oxide) cathode materials for European battery cell customers. France’s strategic investment in battery manufacturing, anchored by the Gigafactory ACC (Automotive Cells Company) joint venture between Stellantis, TotalEnergies, and Mercedes-Benz, is expanding French battery chemical consumption. The EU Critical Raw Materials Act (CRMA), adopted in 2024, establishes domestic processing capacity targets for battery-critical minerals including lithium, nickel, cobalt, and manganese, directly stimulating European battery chemical industry investment and reducing geopolitical import dependence.

Asia Pacific Battery Chemicals Market Trends and Insights

Asia Pacific leads the global battery chemicals market with approximately 62% of total market share in 2025 and is simultaneously the fastest-growing region, underpinned by China’s unrivaled dominance in lithium-ion battery manufacturing, cathode and anode material production, and electrolyte chemical supply, complemented by Japan’s and South Korea’s sophisticated battery technology ecosystems and India’s rapidly emerging battery industry. China processes an estimated 60-80% of global lithium chemicals, produces the majority of global cathode active materials and electrolyte solvents, and is home to CATL and BYD, whose combined annual production capacity exceeds 500 GWh. Shanshan Technology is China’s leading anode material and electrolyte producer, supplying major domestic and international cell manufacturers. The Chinese government’s continued policy support for the NEV industry under its 14th Five-Year Plan is ensuring sustained domestic battery chemical demand growth.

Japan maintains a technologically sophisticated battery chemicals ecosystem, with Mitsubishi Chemical Holdings Corporation producing high-performance electrolyte solvents and additives, Asahi Kasei Corporation manufacturing advanced separator films critical to battery safety, and Sumitomo Metal Mining Co., Ltd. operating leading nickel and cobalt refining operations that supply battery-grade sulfates globally. South Korea’s battery industry, anchored by LG Energy Solution, Samsung SDI, and SK On, generates substantial battery chemical demand served by a combination of domestic and imported supply. India is the most dynamic emerging market, with the Production Linked Incentive (PLI) Scheme for Advanced Chemistry Cells committing US$ 2.4 billion in government incentives for domestic battery cell and chemical manufacturing investment, attracting international battery chemical producers seeking early-mover positions in one of the world’s fastest-growing EV markets.

Competitive Landscape

The global battery chemicals market features moderate top-tier consolidation, where large vertically integrated chemical groups operate alongside specialized battery chemical producers and a fragmented base of regional suppliers, particularly in Asia. High entry barriers stem from stringent battery-grade purity requirements, capital-intensive refining infrastructure, and long qualification cycles with cell manufacturers. Market concentration is strongest in lithium processing and high-performance electrolyte salts, while precursor and additive segments remain more competitive.

Competitive strategy increasingly centers on securing long-term offtake agreements with battery cell manufacturers to ensure supply stability and predictable revenue streams. Producers are prioritizing expansion of battery-grade refining capacity, strengthening ESG compliance and traceability systems aligned with emerging global battery regulations, and investing in next-generation cathode chemistries and advanced electrolyte formulations. Vertical integration across mining, chemical conversion, and cathode material production is emerging as a key strategic lever to control costs, manage raw material volatility, and enhance bargaining power within the rapidly expanding EV and energy storage value chain.

Key Developments:

- January, 2026: Himadri Speciality Chemical initiated discussions with prospective global buyers, including in the US and South Korea, to supply lithium-ion battery components ahead of its INR 1,130-crore Odisha LFP production plant coming online.

- January, 2026: Acutaas Chemicals inaugurated Phase 1 of a new state-of-the-art manufacturing block for electrolyte additives and other battery chemicals at its Jhagadia, Gujarat facility to boost production capacity.

- November, 2025: Sumitomo Chemical announced it will restructure its lithium-ion secondary battery separator business by consolidating production in South Korea and focusing Japan operations on next-generation materials to enhance competitiveness.

Companies Covered in Battery Chemicals Market

- Albemarle Corporation

- Umicore SA

- Sumitomo Metal Mining Co., Ltd.

- Mitsubishi Chemical Holdings Corporation

- Johnson Matthey PLC

- BASF SE

- 3M Company

- American Elements

- Nynas AB

- Asahi Kasei Corporation

- Eastman Chemical Company

- Shanshan Technology Co., Ltd.

- Rio Tinto

- Shenzhen Capchem Technology Co., Ltd.

- Solvay SA

- Stella Chemifa Corporation

- Acutaas Chemicals

- Himadri Speciality Chemical

Frequently Asked Questions

The battery chemicals market is projected to reach US$ 73.5 billion in 2026, driven by expanding lithium-ion battery production for EVs and energy storage.

Demand is fueled by rapid EV adoption and large-scale grid energy storage deployment, increasing consumption of lithium salts, metal sulfates, and electrolyte chemicals.

Asia Pacific leads with around 62% share, supported by China’s processing dominance and large-scale regional battery manufacturing capacity.

Major opportunities include sodium-ion battery commercialization and rising adoption of premium electrolyte salts such as LiFSI.

Key players include Albemarle, Umicore, BASF, Sumitomo Metal Mining, Mitsubishi Chemical, Johnson Matthey, Solvay, and others.