- Electric Mobility

- Electric Vehicle Battery Cooling Plate Market

Electric Vehicle Battery Cooling Plate Market Size, Share, and Growth Forecast 2026 - 2033

Electric Vehicle Battery Cooling Plate Market by Vehicle Type (Passenger Car, Commercial Vehicle), Propulsion Type (BEV, HV), Technology (Liquid Cooling, Air Cooling, PCM), Battery Type (Lithium-ion, Nickel-Metal Hydride), and Regional Analysis for 2026 - 2033

Electric Vehicle Battery Cooling Plate Market Size and Trend Analysis

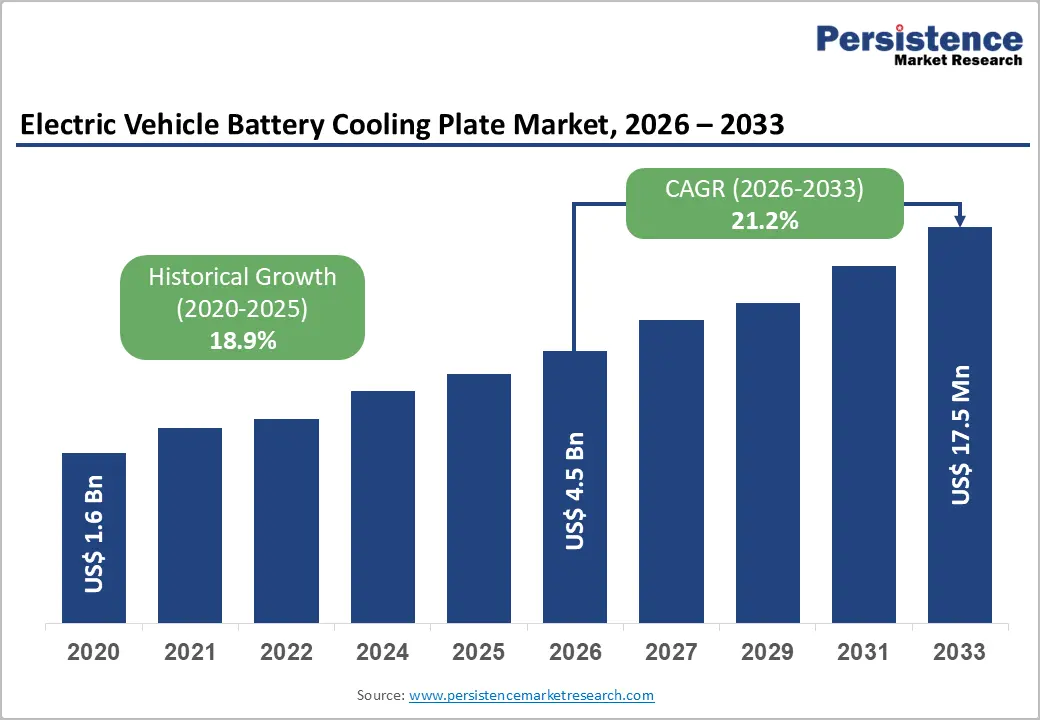

The global electric vehicle battery cooling plate market size is likely to be valued at US$ 4.6 billion in 2026 and is projected to reach US$ 17.5 billion by 2033, growing at a CAGR of 21.2% between 2026 and 2033.

This exceptional growth trajectory is anchored in the global acceleration of electric-vehicle adoption, increasingly stringent battery thermal-management requirements, and regulatory mandates targeting reductions in vehicle emissions. The International Energy Agency (IEA) confirmed that global EV sales exceeded 14 million units in 2023, representing approximately 18% of all new car sales worldwide fundamental demand signal for battery thermal management components, including cooling plates.

Key Industry Highlights:

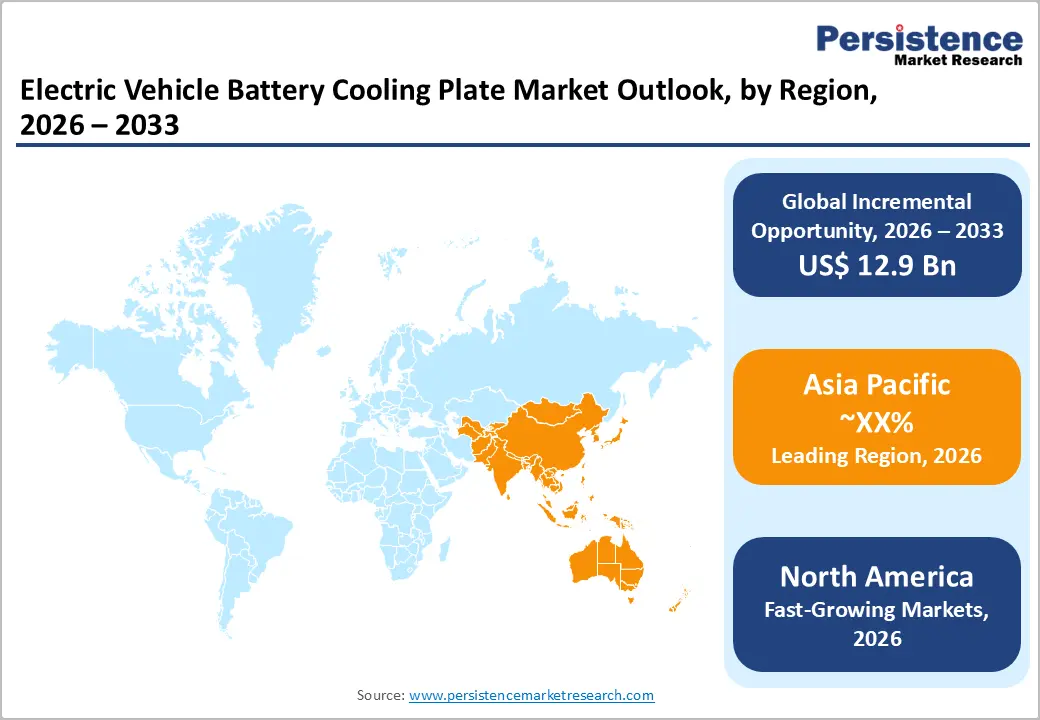

- Leading Region: Asia Pacific leads the global Electric Vehicle Battery Cooling Plate Market, driven by China's 9.4 million NEV units sold in 2023 per MIIT, world-leading battery manufacturing by CATL and BYD, and active government EV adoption incentives across India, Japan, and ASEAN.

- Fastest Growing Region: North America markets represent the fastest-growing regional markets, propelled by substantial federal investment in EV infrastructure, domestic battery manufacturing incentives, and an active OEM innovation ecosystem.

- Leading Propulsion Type: Battery Electric Vehicles (BEVs) dominate the Propulsion Type segment with approximately 72% market share, driven by the full battery-traction architecture's demands for sophisticated liquid-cooled plate systems that manage sustained thermal loads across high-energy-density packs exceeding 70 kWh per vehicle.

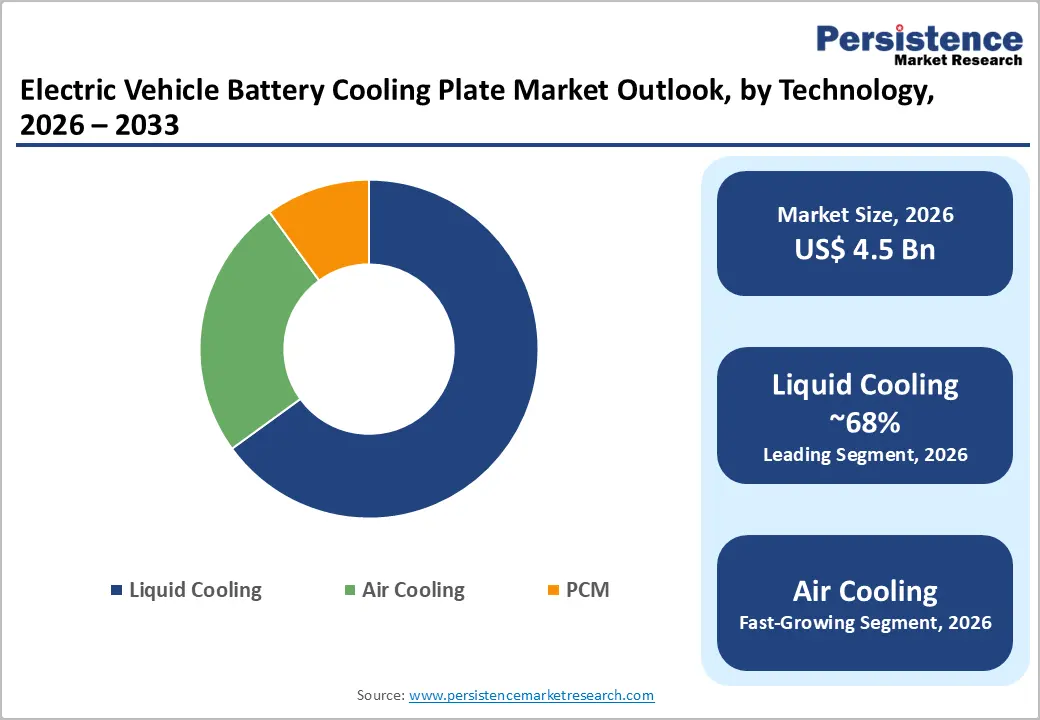

- Fastest Growing Technology: Liquid Cooling technology is the fastest-growing and dominant Technology segment, with OEMs including Tesla, BMW, and GM standardizing on liquid-cooled plate designs across flagship BEV platforms to maintain precise cell temperature differentials below 5°C under fast-charging operational conditions.

- Opportunities: The integration of solid-state battery platforms targeted for commercialization by Toyota by 2027 - 2028 and supported by U.S. Department of Energy R&D funding represents the most transformative market opportunity, requiring entirely redesigned thermal interface architectures and creating first-mover design-win advantages for cooling plate manufacturers who invest in co-development partnerships now.

| Key Insights | Details |

|---|---|

| Electric Vehicle Battery Cooling Plate Market Size (2026E) | US$ 4.6 Bn |

| Market Value Forecast (2033F) | US$ 17.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 21.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 18.9% |

Market Dynamics

Drivers - Surging Global EV Adoption Fueling Structural Demand for Battery Thermal Management Systems

The exponential adoption of electric vehicles across passenger and commercial segments worldwide is the single most powerful demand catalyst for the electric vehicle battery cooling plate market. According to the International Energy Agency (IEA), global EV sales reached 14 million units in 2023, and the agency projects that EVs could account for over 60% of new car sales globally by 2030 under its Net Zero Emissions scenario. Each battery-electric vehicle requires one or more precision-machined cooling plates to regulate cell temperatures within the optimal operating range, typically 15°C to 35°Cto prevent thermal runaway and extend battery cycle life. With average battery pack sizes in passenger EVs now exceeding 70 kWh, thermal loads are intensifying with each successive platform generation.

Fast-Charging Infrastructure Expansion Intensifying Battery Thermal Load Requirements

The rapid global rollout of high-power DC fast-charging infrastructure is creating a direct and growing demand driver for advanced battery cooling plate solutions. Fast-charging systems operating at 150 kW to 350 kW generate elevated heat within battery cells, demanding cooling plates with superior thermal conductivity, tighter dimensional tolerances, and more efficient coolant channel geometries. The U.S. Department of Transportation announced a federal commitment of US$7.5 billion for EV charging infrastructure under the Bipartisan Infrastructure Law, targeting the installation of 500,000 public charging stations by 2030. In parallel, China's National Development and Reform Commission (NDRC) reported that over 2.7 million public charging points had been installed domestically as of 2023, making it the world's largest charging network. The convergence of higher charging power and greater charging frequency places unprecedented thermal stress on battery packs, compelling OEMs and Tier-1 suppliers to source higher-specification cooling plates with enhanced flow path engineering and multi-layer material constructions.

Restraints - High Precision Manufacturing Costs Constraining Supplier Margins and Scalability

Battery cooling plates require highly precise fabrication processes, including vacuum brazing, friction stir welding, and computer-controlled channel machining that demand sophisticated capital equipment and strict quality control protocols. Manufacturing defects such as micro-porosity, uneven channel distribution, or inadequate seal integrity can compromise battery safety and lead to costly recalls. Battery thermal incidents remain a documented risk across multiple OEM platforms, with the National Highway Traffic Safety Administration (NHTSA) maintaining active investigation records on EV thermal events. For mid-tier and emerging suppliers, the capital investment required to establish and certify precision cooling plate production lines creates a significant barrier, limiting supply chain diversification and constraining competitive pricing pressure.

Supply Chain Concentration Risk in Critical Raw Materials

Battery cooling plates are manufactured from aluminum alloys, a material whose upstream supply chain carries its own strategic risk profile. According to the U.S. Geological Survey (USGS), China controls approximately 56% of global primary aluminum smelting capacity, creating geopolitical concentration risk for OEMs reliant on cost-competitive aluminum plate stock. While aluminum itself is abundant, high-purity, alloy-specific grades required for automotive thermal management applications are subject to pricing volatility and export policy uncertainty. Tariff actions, energy cost shocks affecting smelter operations, and logistics disruptions can collectively elevate input costs by 15-25% within a single procurement cycle, directly compressing supplier margins and forcing OEMs to absorb cost increases or delay platform launches.

Opportunity - Solid-State Battery Platforms Creating Next-Generation Thermal Management Design Opportunities

Solid-state batteries represent the most consequential emerging technology opportunity for participants in the Electric Vehicle Battery Cooling Plate Market, as their commercial introduction will require entirely redesigned thermal management architectures distinct from current liquid-cooled lithium-ion configurations. Solid-state cells operate at different thermal profiles and require intimate, uniform contact between the cooling interface and cell surfaces, creating demand for next-generation cooling plate geometries with higher surface-area precision and new material compositions.

Toyota Motor Corporation has publicly committed to commercializing solid-state EV batteries by 2027-2028, while QuantumScape, backed by Volkswagen AG, continues to advance lithium-metal solid-state cell development, with pilot production underway. The U.S. Department of Energy's Vehicle Technologies Office has allocated funding specifically for solid-state battery thermal management research under its battery programs. Cooling plate manufacturers who invest in R&D partnerships with solid-state battery developers today will secure first-mover design-win advantages that translate into multi-platform, multi-decade supply exclusivity once solid-state EVs enter mass production.

Commercial EV Segment Electrification Unlocking High-Value, High-Volume Demand Streams

The accelerating electrification of commercial vehicles, including electric buses, heavy-duty trucks, last-mile delivery vans, and construction equipment represents a structurally distinct and high-growth demand segment for the Electric Vehicle Battery Cooling Plate Market, given that commercial EV battery packs are significantly larger than passenger car equivalents and generate substantially greater thermal loads under operational duty cycles.

Amazon has committed to deploying 100,000 electric delivery vehicles by 2030 through its partnership with Rivian, while the European Commission's revised CO2 standards for heavy-duty vehiclesmandating a 90% CO2 reduction for new trucks by 2040are compelling fleet operators to accelerate electrification timelines. Commercial EVs typically carry battery packs ranging from 100 kWh to over 600 kWh, requiring multiple cooling plate assemblies per vehicle and significantly increasing per-unit content value for suppliers. Battery cooling plate manufacturers who develop commercial-vehicle-specific thermal management platforms with modular, scalable designs will capture premium revenue per vehicle relative to passenger car programs throughout the forecast period.

Category-wise Analysis

Vehicle Type Insights

Passenger cars dominate the vehicle type category of the electric vehicle battery cooling plate market, accounting for approximately 78% share. This position reflects the sheer volume scale of passenger EV production globally relative to commercial vehicle electrification, which remains at an earlier adoption stage. According to the IEA, passenger EVs represented the overwhelming majority of the 14 million global EV units sold in 2023, with markets such as China, Germany, and the United States each recording passenger EV penetration rates well above the global average. The shift toward larger battery architectures in premium passenger platforms such as the Tesla Model S and Mercedes EQS, both carrying packs exceeding 100 kWh amplifies per-vehicle cooling plate content value, further consolidating the segment's revenue dominance well into the forecast period.

Propulsion Type Insights

Battery Electric Vehicles (BEVs) hold the lead in the Propulsion Type category, accounting for approximately 72% of the Electric Vehicle Battery Cooling Plate Market. Unlike hybrid vehicles (HVs), where battery packs are smaller and thermal demands are moderated by internal combustion engine assistance, BEVs rely entirely on their battery systems for traction power, creating greater and more sustained thermal loads requiring dedicated, high-performance cooling plate systems. The IEA reported that pure BEVs accounted for approximately 70% of all new electric vehicle registrations globally in 2023, directly corroborating the segment's market share dominance. Government policies across the European Union, United States, and China are progressively favoring pure BEV adoption through purchase incentives and internal combustion engine phase-out timelines, reinforcing BEV's structural market share leadership through 2033.

Technology Insights

Liquid Cooling is the dominant technology segment in the Electric Vehicle Battery Cooling Plate Market, representing approximately 68% of total market share. Liquid cooling plates circulate coolant, typically a water-glycol mixture, through precision-machined channels embedded within aluminum plate structures, delivering far superior heat dissipation per unit area compared to air cooling or Phase Change Material (PCM) systems. The thermal conductivity advantage of liquid cooling is critical for high-energy-density lithium-ion battery packs operating under fast-charging conditions, where temperature differentials across cells must be maintained below 5°C to ensure longevity and safety. Major OEMs including Tesla, BMW, and General Motors have standardized liquid-cooled battery thermal management systems across their flagship platforms, validating this technology's technical supremacy. PCM-based solutions, while growing in research interest, remain commercially nascent for automotive applications.

Battery Type Insights

Lithium-ion batteries represent the dominant segment in the battery Type category, accounting for approximately 88% of the Electric Vehicle Battery Cooling Plate Market. Lithium-ion chemistry underpins the entire global EV production fleet from NMC (Nickel Manganese Cobalt) and NCA (Nickel Cobalt Aluminum) configurations in premium vehicles to LFP (Lithium Iron Phosphate) variants increasingly adopted in mass-market and commercial EVs. The operating temperature sensitivity of lithium-ion cells where performance degrades sharply outside the 15°C to 45°C window and thermal runaway risk escalates above 60°Cmakes precisely engineered cooling plates an absolute functional requirement rather than an optional enhancement. Nickel-Metal Hydride (NiMH) batteries, while retaining relevance in certain hybrid platforms such as the Toyota Prius, require less intensive cooling management and represent a structurally declining share as full BEV adoption accelerates across all vehicle categories.

Regional Insights

North America Electric Vehicle Battery Cooling Plate Trends

The United States leads the North American Electric Vehicle Battery Cooling Plate Market, supported by substantial federal investment in EV infrastructure, domestic battery manufacturing incentives, and an active OEM innovation ecosystem. The Inflation Reduction Act (IRA) of 2022 established a US$ 7,500 per-vehicle consumer EV tax credit conditional on domestic battery component sourcing, directly incentivizing North American battery and thermal management component manufacturing.

The U.S. regulatory environment is further shaping thermal management specifications, as the National Highway Traffic Safety Administration (NHTSA) and Society of Automotive Engineers (SAE) continue developing standards for battery safety and thermal event prevention. Canada is emerging as a complementary manufacturing hub, supported by federal EV supply chain investment programs under its Strategic Innovation Fund. The combination of policy-driven EV adoption reshored battery manufacturing, and fast-charging network expansion positions North America as a high-growth, premium-margin market for battery cooling plate suppliers through the forecast horizon.

Europe Electric Vehicle Battery Cooling Plate Trends

Europe's Electric Vehicle Battery Cooling Plate Market is driven by the European Union's landmark regulatory mandate to ban the sale of new internal combustion engine passenger cars by 2035, creating a non-negotiable timeline for OEM electrification across Germany, France, U.K., and Spain. Germany leads European EV production, anchored by Volkswagen AG's multi-platform MEB and PPE electric architectures, BMW's iX platform, and Mercedes-Benz EQ series, each relying on liquid-cooled battery thermal management.

France and Spain are expanding EV manufacturing capacity as part of broader industrial policy realignments, while the U.K. post-Brexit has maintained its 2035 ICE ban commitment, sustaining EV procurement growth. EASA and UNECE harmonized safety regulations for EV battery systems particularly UNECE Regulation 100are driving OEMs to adopt certified thermal management solutions meeting defined temperature control performance thresholds. European Tier-1 thermal management suppliers, including Valeo SA and Hanon Systems, are scaling cooling plate capacity in alignment with OEM platform launches scheduled through 2028.

Asia Pacific Electric Vehicle Battery Cooling Plate Trends

Asia Pacific is both the largest and fastest-growing regional market for the Electric Vehicle Battery Cooling Plate Market, anchored by China's dominant position as the world's largest EV producer and consumer. China's Ministry of Industry and Information Technology (MIIT) reported that NEV sales in China reached 9.4 million units in 2023, representing approximately 31% of all new vehicle sales domestically market scale that dwarfs all other geographies. Chinese battery manufacturers led by CATL and BYD produce many the world's lithium-ion EV battery packs, each requiring thermally managed cooling plate assemblies, creating an enormous co-located component procurement ecosystem.

Japan sustains a significant market presence through Toyota's hybrid and BEV platforms, with the company investing heavily in next-generation solid-state battery development that will redefine thermal management requirements. India is an accelerating growth market, supported by the government's FAME-II and PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-DRIVE) scheme, which allocated INR 10,900 crore to EV adoption incentives, and a domestic EV manufacturing base expanding rapidly across two-wheeler, three-wheeler, and passenger car segments.

Competitive Landscape

The global electric vehicle battery cooling plate market is characterized by a moderately fragmented to consolidating competitive structure, with global automotive Tier-1 thermal management specialists competing alongside specialized aluminum component manufacturers and vertically integrated EV system suppliers. Market leaders differentiate through proprietary coolant channel geometry optimization, multi-material brazing expertise, and platform-specific design-win integration with major OEM engineering teams. Leading companies are investing heavily in friction stir welding and vacuum brazing process automation to achieve both precision and scale. Strategic themes include co-development partnerships with battery manufacturers, geographic manufacturing expansion near OEM assembly clusters, and integration of digital simulation tools for thermal performance validation.

Key Developments:

- In March 2024, Valeo announced the launch of its next-gen liquid-cooled battery plate system tailored for high-performance BEVs and PHEVs. The system incorporates multi-channel aluminum flow paths and an adaptive coolant distribution network, enhancing thermal efficiency by up to 30% and extending battery life under extreme fast-charging scenarios.

- In February 2024, Sanhua Automotive revealed a strategic collaboration with a leading Chinese EV manufacturer to co-develop integrated cooling solutions that merge battery, inverter, and e-motor cooling through a single thermal loop. The solution is aimed at lowering vehicle system complexity and cost while maintaining optimal thermal management.

Companies Covered in Electric Vehicle Battery Cooling Plate Market

- ZIEHL-ABEGG

- Schaeffler Technologies AG & Co., KG

- Protean Electric

- Bonfiglioli Riduttori S.p.A.

- ZF Friedrichshafen AG

- Elaphe AG

- Evans Electric

- TM4

- Siemens AG

- Kolektor

- Printed Motor Works

- NSK Ltd.

- NTN Corporation

- Other Key Players

Frequently Asked Questions

The global Electric Vehicle Battery Cooling Plate Market is valued at US$ 4.6 Bn in 2026 and is projected to reach US$ 17.5 Bn by 2033, expanding at a forecast CAGR of 21.2% during 2026 - 2033.

The market is primarily driven by exponential global EV adoption, with IEA reporting 14 million EV units sold globally in 2023 and the expansion of high-power fast-charging infrastructure requiring advanced battery thermal management. Government mandates, including the EU's 2035 ICE ban, the U.S.

Passenger Cars lead the Vehicle Type segment with approximately 78% market share. This dominance reflects the scale of global passenger EV production, which accounts for the overwhelming majority of the 14 million EV units sold in 2023 per IEA.

Asia Pacific is the dominant regional market, driven by China's exceptional NEV scale9.4 million units sold in 2023 per MIIT, representing 31% of all new domestic vehicle sales. China's globally dominant lithium-ion battery manufacturing ecosystem, led by CATL and BYD, creates co-located procurement demand for cooling plate assemblies at unmatched volume.

Key companies in the Electric Vehicle Battery Cooling Plate Market include Valeo SA, Dana Incorporated, Hanon Systems, Mahle GmbH, Modine Manufacturing Company, Denso Corporation, ZF Friedrichshafen AG, and Schaeffler Technologies AG & Co. KG, among others.