- Energy Storage Solutions

- Energy Storage Market

Energy Storage Market Size, Share, Trends, Growth, Regional Forecasts 2025 - 2032

Energy Storage Market by Energy Type (Electrical Energy Storage, Thermal Energy Storage), Application (Residential, Commercial & Industrial, Grid/Utility Services), and Regional Analysis 2025 - 2032

Energy Storage Market Share and Trends Analysis

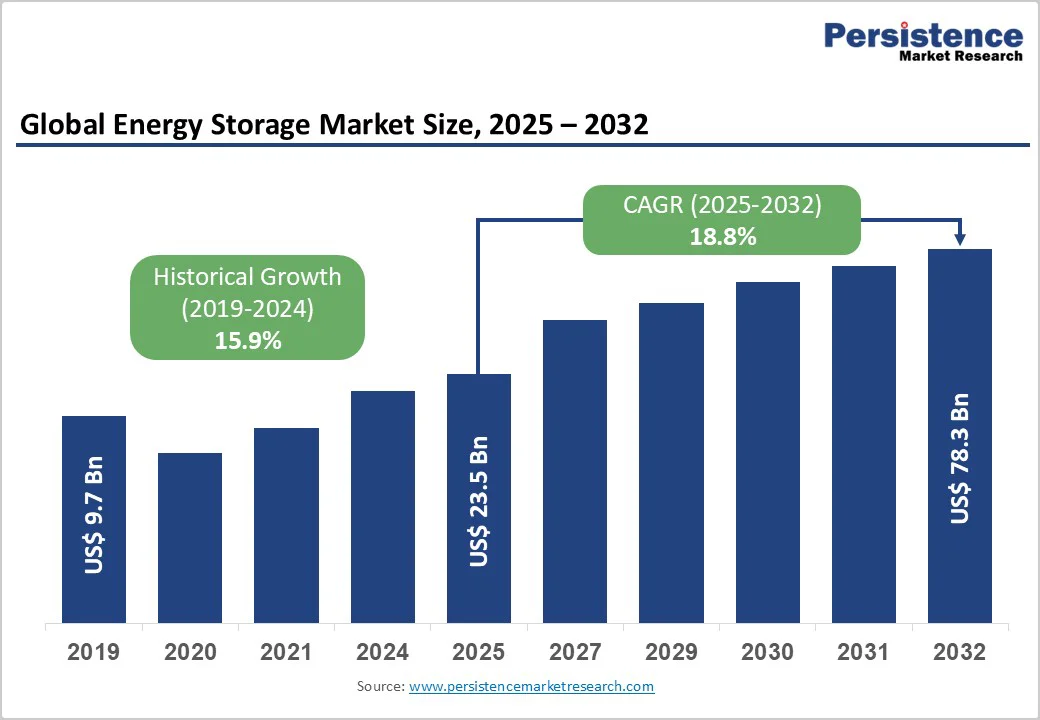

The global energy storage market size was valued at US$ 23.5 billion in 2025 and is projected to reach US$ 78.3 billion by 2032, growing at a CAGR of 18.76% between 2025 and 2032. This remarkable expansion reflects the accelerating global transition toward renewable energy integration, grid modernization initiatives, and the critical need for reliable power infrastructure to support intermittent clean energy sources.

The market is experiencing strong growth due to falling battery costs, with lithium-ion pack prices decreasing 20% to $115 per kilowatt-hour in 2024. Global installed capacity is expected to exceed 175.4 GWh. This expansion is fueled by government incentives, advancements in battery energy storage, and the need for improved grid stability driven by increased electricity demand from data centers, electric vehicles, and renewable energy projects.

Key Industry Highlights:

- Electrical Energy Storage dominates the energy type segment led by lithium-ion batteries and pumped hydropower, while thermal energy storage emerges as the fastest-growing segment with 17.1% CAGR, addressing industrial process heat and concentrated solar power applications.

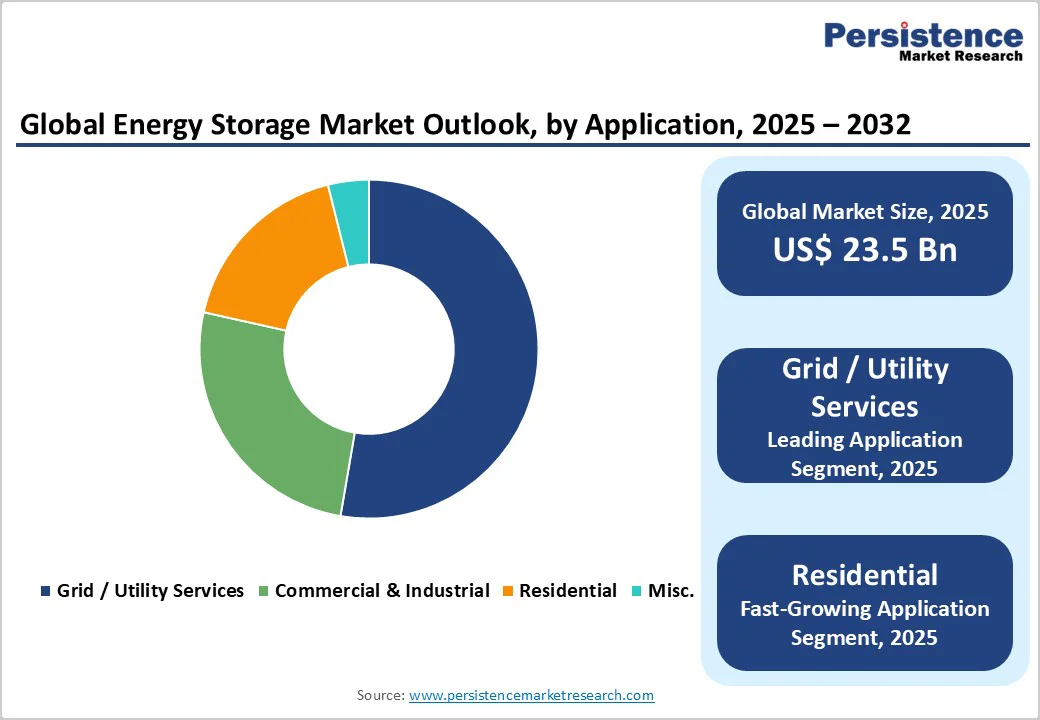

- Grid/Utility Services commands 53% application market share, providing bulk power management and renewable integration services, while Residential applications demonstrate the highest growth at 20.1% CAGR, driven by solar integration, backup power requirements, and energy independence demands.

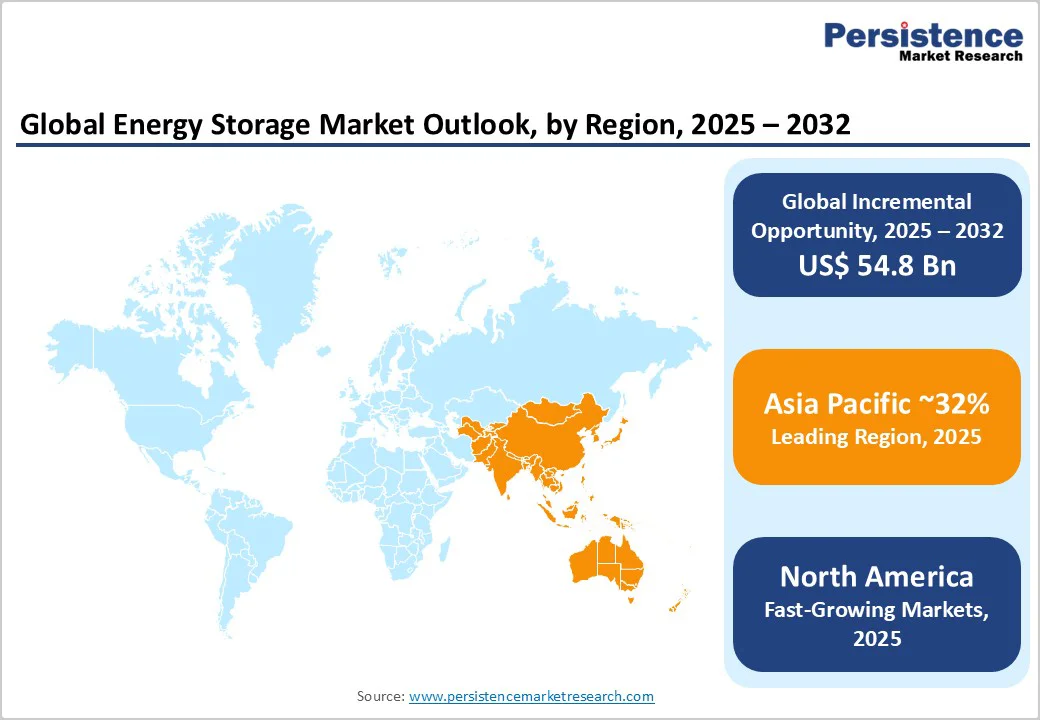

- Asia Pacific leads with 32% market share, supported by China's manufacturing dominance and India's renewable targets, while North America exhibits the fastest regional growth at 18.7% CAGR propelled by IRA incentives and utility-scale deployment acceleration, and Europe maintains 27% market share backed by decarbonization commitments.

- Lithium-ion battery pack prices dropped 20% to a record low of $115/kWh in 2024, with global battery energy storage deployments reaching 86.7 GWh in H1 2025, representing 54% year-over-year growth, and the United States installing 12.3 GW across all segments in 2024, marking 33% annual increase.

- Strategic developments include CATL's 587 Ah cell launch with 434 Wh/L energy density, Samsung SDI's $800 million NextEra Energy contract, Rio Tinto's $6.7 billion Arcadium Lithium acquisition, and Constellation Energy's $16.4 billion Calpine purchase, demonstrating industry consolidation and technology advancement.

- Major market opportunities encompass emerging markets projected for 40% annual storage growth over the next decade, long-duration storage technologies including pumped hydro's 600+ GW pipeline, and vehicle-to-grid integration enabling electric vehicles as distributed energy resources supporting grid flexibility and renewable integration.

| Key Insights | Details |

|---|---|

|

Energy Storage Market Size (2025E) |

US$ 23.5 billion |

|

Market Value Forecast (2032F) |

US$ 78.3 billion |

|

Projected Growth CAGR (2025-2032) |

18.8% |

|

Historical Market Growth (2019-2024) |

15.9% |

Market Dynamics Analysis

Driver - Accelerating Renewable Energy Integration and Grid Stability Requirements

The exponential growth of intermittent renewable energy sources represents the primary catalyst propelling energy storage market expansion. Global renewable capacity additions reached approximately 295 GW in 2023, demonstrating a 35% increase from the previous year, with projections indicating continued robust growth through 2030. Solar capacity installations increased by 29% in 2024, while wind and solar generation are forecast to nearly double by 2030, adding approximately 935 GW annually. This massive influx of variable renewable energy creates fundamental challenges for grid operators who must maintain supply-demand balance despite the intermittent nature of solar and wind power. Energy storage systems bridge renewable intermittency by storing surplus power during peak generation and supplying it during demand surges. India’s Central Electricity Authority forecasts 411.4 GWh capacity by 2032, including 236.22 GWh from batteries and 175.18 GWh from pumped storage. Grid scale deployments grew 63 percent year over year in Q2 2025, reaching 4.9 GW or 15 GWh, underscoring their vital role in grid stability and renewable integration.

Supportive Government Policies and Declining Technology Costs

Comprehensive policy frameworks and financial incentives across major economies are fundamentally reshaping energy storage economics and deployment trajectories. The United States Inflation Reduction Act provides substantial tax credits for energy storage installations, including Investment Tax Credit benefits and domestic content bonus adders, catalyzing record deployment levels with 12.3 GW installed across all segments in 2024, representing a 33% year-over-year increase. European markets are advancing under the European Green Deal and REPowerEU, recognizing energy storage as essential for carbon neutrality by 2050, with 21.9 GWh installed in 2024. India’s Energy Storage Obligations mandate storage procurement growth from one to four percent by 2030, prioritizing renewable energy. Meanwhile, global system costs fell sharply, with battery prices dropping 40 percent to 165 dollars per kWh in 2024 due to economies of scale and wider lithium iron phosphate adoption.

Restraint - High Initial Capital Investment and Financing Challenges

Despite declining technology costs, energy storage projects continue to face substantial upfront capital requirements that present barriers to widespread adoption, particularly in emerging markets and for commercial-industrial segments. The installation of thermal energy storage devices involves significant initial investment encompassing infrastructure components including storage tanks, heat exchangers, control systems, and insulation materials. Battery energy storage deployment demands extensive investment across battery racks, power conversion systems, energy management, transformers, and switchgear, with turnkey costs averaging 165 dollars per kWh globally. In India, tariffs range between 0.22 and 0.28 million rupees per MW monthly for two-hour storage, while high financing costs hinder viability. Global corporate funding fell 41 percent to 9.1 billion dollars in early 2025 as market overcapacity and falling cell prices near 40 dollars per kWh prompted cautious investment sentiment.

Supply Chain Constraints and Raw Material Dependencies

Energy storage industry growth confronts structural vulnerabilities stemming from concentrated supply chains and limited availability of critical battery materials. The battery energy storage supply chain heavily relies on raw materials, including lithium, cobalt, nickel, manganese, and graphite, with supply geographically concentrated among a few key players globally. China dominates global lithium processing, handling nearly 70 to 80 percent of the world’s supply, and its potential restrictions on refining technologies could significantly disrupt global supply chains. Lithium demand for batteries is forecasted to expand five times by 2030 and fourteen times by 2040, straining raw material availability amid rapid demand growth and slower nickel supply development. Short-term lithium shortages are anticipated through 2029, alongside tight supply for graphite and manganese. Limited U.S. manufacturing capacity and delayed component deliveries further constrain large-scale battery storage project execution.

Opportunity - Expansion in Emerging Markets with Renewable Energy Targets

Emerging economies present transformative growth opportunities as nations pursue ambitious renewable energy integration and grid modernization objectives. Energy storage deployments in emerging markets are projected to grow 40% annually over the coming decade, resulting in approximately 80 gigawatts of new storage capacity, a substantial increase from less than 2 GW currently in place. The largest energy storage markets through the next decade are expected to be China and India, supported by aggressive renewable energy targets, with Latin America representing another attractive development region given renewable roll-out plans, particularly in Mexico, Chile, and Brazil. India’s energy storage capacity reached 490 megawatt-hours by June 2025, supported by government mandates requiring solar projects to include co-located storage with at least two-hour duration or 10 percent of project capacity.

The Middle East and Africa are emerging as fast-growing energy storage markets, with the Middle East projected to rank third globally by 2026 due to large-scale renewable deployment and fuel export optimization. The United Arab Emirates plans over 70 gigawatts of renewable power by 2050 with $700 billion investment, while Saudi Arabia’s NEOM project features a 536 MW/600 MWh system, and South Africa advances with Eskom’s 8 MW/32 MWh project.

Integration with Electric Vehicle Infrastructure and Vehicle-to-Grid Services

The convergence of electric vehicle proliferation and bidirectional charging technologies presents unprecedented opportunities for distributed energy storage deployment and grid services revenue generation. Residential energy storage markets are experiencing robust expansion, with the global market growing from USD 1.96 billion in 2024 to a projected USD 5.60 billion by 2032 at a 14.08% CAGR, driven by energy independence demands, rising rooftop solar installations, and integration with electric vehicle charging infrastructure.

The United States residential energy storage market recorded record installations of 346 megawatts in Q3 2024, marking a 63 percent quarter-over-quarter rise driven by heightened consumer focus on reliability and energy independence. Vehicle-to-grid technology allows electric vehicles to store renewable energy and return it to the grid during peak demand, generating additional income through frequency regulation and demand response programs. Bidirectional charging enhances renewable integration, supports grid stability, and enables time-of-use optimization, while energy storage-backed EV charging stations alleviate grid strain and promote widespread fast-charging expansion.

Segmentation Analysis

Energy Type Analysis

Electrical Energy Storage maintains its position as the leading segment in the energy storage market, encompassing battery energy storage systems, pumped-storage hydroelectricity, and advanced electrochemical solutions that collectively dominate global installed capacity. Lithium-ion batteries represent the fastest-growing technology within electrical storage, with global deployments reaching 86.7 GWh in the first half of 2025, marking a 54% year-over-year increase, while the full-year pipeline projects just over 412 GWh. Battery energy storage systems play a crucial role in grid stability, holding 36% market share in 2024, driven by utility-scale projects delivering frequency regulation, load balancing, and renewable integration. Pumped-storage hydroelectricity dominates global capacity at 189 GW, offering reliable, long-duration energy shifting backed by mature technology, cost efficiency, and proven performance versatility.

Thermal Energy Storage represents the fastest-growing segment with prominent growth rate of 17.1% CAGR, driven by increasing adoption in concentrated solar power plants, district energy systems, and industrial process applications. Thermal energy storage is gaining momentum due to its efficiency, eliminating electricity-to-heat conversion losses and offering cost-effective, long-duration solutions for industries like power, chemical, and food processing. Rapid adoption in district heating and smart city projects, especially in India, underscores its pivotal role in decarbonizing heat-intensive global energy consumption.

Application Analysis

Grid/Utility services represents the leading application segment with a dominating share of 53%, reflecting the critical role energy storage plays in bulk power system operations, transmission and distribution infrastructure support, and wholesale electricity market participation. Utility-scale battery energy storage deployments reached 4.9 GW/15 GWh during Q2 2025, rising 63% year-over-year, with Texas and California continuing to lead the market, accounting for combined 61% of total installed capacity in Q4 2024. The grid-scale stationary battery storage market is expanding at a 17.6% CAGR, fueled by adoption for grid balancing, frequency regulation, and decentralized energy integration. Including pumped storage hydropower, capacity reached 189 GW in 2024 with over 1,075 GW in development, as operators leverage storage to enhance reliability, defer infrastructure costs, and support renewable integration.

Residential emerges as the fastest-growing application segment with a 20.1% CAGR, propelled by declining system costs, supportive net metering policies, increasing frequency of grid outages, and consumer desire for energy independence and resilience. The U.S. residential storage market surpassed 1,250 MW in 2024, up 57% from 2023, with record 380 MW added in Q4 driven by rooftop solar pairing, time-of-use pricing, and bidirectional EV charging. Asia Pacific, led by India at 27.7% CAGR, benefits from subsidies, urbanization, and reliability needs, while incentives and smart-home integration further accelerate adoption.

Regional Market Insights

North America Energy Storage Market Trends

North America demonstrates the most prominent growth trajectory with an 18.7% CAGR, positioning the region as the fastest-growing market globally through the forecast period. The United States energy storage market set a record in 2024 with 12.3 gigawatts of installations across all segments, representing 12,314 megawatts and 37,143 megawatt hours deployed, increases of 33% and 34% respectively over 2023 figures. Global grid scale storage installations are expected to reach 13.3 GW in 2025, with total deployments across all segments projected at 15 GW, reflecting a 25 percent increase over 2024. Growth momentum remains strong with capacity on track to surpass 100 GW by 2030 as Texas and California lead with 61 percent share, while new projects in New Mexico, Oregon, and Arizona expand regional presence supported by Inflation Reduction Act incentives, rising manufacturing investments, and Canada’s 250 MW Oneida project advancing grid reliability and renewable integration.

Market dynamics in North America remain robust, supported by strong renewable energy mandates and portfolio standards driving sustained demand for advanced storage solutions. The US residential segment surpassed 1,250 MW in 2024 amid rising outages and reliability concerns, while commercial and industrial deployments grew 22 percent to 145 MW. Innovation strength, research excellence, and venture funding sustain leadership, though policy and tariff uncertainties may temper near-term growth by nearly 19 percent over the next five years.

Europe Energy Storage Market Trends

Europe maintains a significant global market position with a 27% market share, supported by aggressive decarbonization targets, regulatory harmonization efforts under European Union frameworks, and mature renewable energy markets requiring grid flexibility solutions. European battery energy storage capacity reached 61 GWh of installed capacity at the end of 2024 after adding 21 GWh during the year, with Germany and Italy each contributing approximately 6 GWh to annual growth. The European energy storage market added 19.1 GWh in 2024, representing 12.4% year-over-year growth, with projections indicating nearly 27 GWh of new installed capacity in 2025 at 41% annual growth as the market transitions from behind-the-meter residential dominance to front-of-meter utility-scale expansion. Italy has emerged as Europe's largest energy storage market through utility-scale installations, surpassing Germany and the United Kingdom, while for the first time installation capacities of front-of-meter and behind-the-meter markets reached parity with the growth engine shifting from residential to utility applications.

Renewable energy accounts for around 24.1% of the European Union’s final energy use in 2023, driven by the region’s 2050 carbon neutrality goal and rapid residential solar growth in Germany, Italy, and Spain. Energy storage is recognized as essential infrastructure under the European Green Deal and REPowerEU, ensuring energy security and reducing import dependency. Rising electricity costs and government incentives accelerate household storage adoption, while a 52.9 GW pumped hydro pipeline and the Battery 2030+ initiative strengthen long-duration and advanced battery development. Germany and Italy lead with 9.4 GW and 7.2 GW capacity, respectively, as focus increasingly shifts toward next-generation battery technologies.

Asia Pacific Energy Storage Market Trends

Asia Pacific commands the largest regional market share at 32%, driven by China's manufacturing dominance, India's ambitious renewable targets, and widespread energy access expansion across Southeast Asian markets. China remained the leading developer globally, adding 14.4 GW of new hydropower capacity in 2024, more than half comprising pumped storage, positioning the country on track to exceed its 120 GW pumped storage target by 2030. China leads global installed capacity with over 50.9 gigawatts of pumped hydropower, followed by Japan with 21.8 GW, while Chinese battery energy storage systems provide the largest share of global manufacturing with over 3.1 terawatt-hours of fully commissioned battery-cell capacity, more than 2.5 times annual global demand.

June 2025 saw 7.96 GW/22.17 GWh of grid-scale battery energy storage enter commercial operations globally across 109 projects, with over half deployed in China, including three projects exceeding 1 GWh. India represents the second-largest growth market, with energy storage capacity projected to reach 411.4 GWh by 2031-32 to support the 500 GW non-fossil capacity target by 2030, driven by government policy support, including Energy Storage Obligations and standalone battery tender programs.

Asia Pacific has emerged as the global energy storage manufacturing hub, led by Chinese giants such as CATL and BYD dominating lithium-ion cell production, battery assembly, and system integration. India’s battery storage capacity reached around 490 MWh by mid-2025, with solar plus storage accounting for most deployments. Japan’s renewable expansion exceeding 30 percent in five years spurred 1.37 GW of BESS approvals in 2024, while Southeast Asian countries and Australia advance large-scale projects supporting grid stability. However, financing constraints in emerging economies highlight the need for stronger policy alignment and international development support.

Competitive Landscape

The global energy storage market shows moderate consolidation, with 6–8 major players holding over 45% share. Tesla leads with 14.7 GWh deployed in 2023 and $6.04 billion in revenue, followed by CATL’s 256 GWh global capacity and advanced 587 Ah cells. BYD, LG Energy Solution, Samsung SDI, and Fluence strengthen competition through large-scale deployments, AI-driven systems, and long-duration technologies, while emerging flow, thermal, and solid-state innovators intensify market dynamism.

Strategic Developments

Major Technology Launches and System Introductions

- In June 2025, CATL unveiled its next-generation 587 Ah energy storage cell featuring 434 Wh/L energy density, marking a 10% improvement over the previous generation, with the capability to boost system density by up to 25% while reducing component count from 30,000 to 18,000 pieces.

- In May 2025, CATL introduced the TENER Stack, the world’s first 9 MWh ultra-large-capacity energy storage system, delivering a 45% improvement in volume utilization and a 50% increase in energy density compared to standard 20-foot container systems, while reducing deployment costs by up to 20% and logistics costs by 35%.

Acquisitions, Strategic Partnerships and Market Activity

- In March 2025, Rio Tinto finalized its $6.7 billion all-cash acquisition of Arcadium Lithium plc, strengthening its position as a leading global lithium producer with a production target exceeding 200,000 tonnes of lithium carbonate equivalent annually by 2028.

- In 2025, Samsung SDI partnered with Stellantis to establish a North American joint venture for lithium-ion battery production, targeting 23 GWh initial annual capacity with expansion potential to 40 GWh, scheduled to commence operations within the year.

- In H1 2025, energy storage project-level M&A surged by 138%, reaching 31 transactions compared to 13 in H1 2024, while corporate M&A slowed to three deals from fourteen in the same period last year, reflecting a market shift toward project-based investments.

Business Strategies

Innovation-led strategies define market leadership, with top players advancing solid-state, silicon-anode, and alternative chemistries to enhance energy density, safety, and lifecycle performance. Tesla and BYD pursue vertical integration for cost control and margin capture, while Asian giants expand in North America and Europe to leverage IRA incentives. Fluence’s AI-driven software platforms boost asset value, as cost optimization through LFP adoption and standardized designs drives competitiveness across the evolving energy storage landscape.

Companies Covered in Energy Storage Market

- Tesla, Inc.

- Contemporary Amperex Technology Co., Limited (CATL)

- BYD Company Limited

- LG Energy Solution

- Samsung SDI Co., Ltd.

- Fluence Energy, LLC

- Panasonic Corporation

- Siemens Energy

- NextEra Energy Resources

- AES Corporation

- Hitachi Energy Ltd.

- ABB Ltd.

- Sungrow Power Supply Co., Ltd.

- Eaton Corporation plc.

Frequently Asked Questions

The global energy storage market was valued at US$ 23.5 billion in 2025 and is projected to reach US$ 78.3 billion by 2032.

The market is propelled by accelerating renewable energy deployment, supportive government policies, and dramatic cost reductions with lithium-ion battery prices declining 20% to $115/kWh in 2024, alongside surging electricity demand from data centers, electric vehicle infrastructure, and residential backup power requirements.

The energy storage market is forecast to grow at a CAGR of 18.76% in the forecast period.

Significant opportunities include emerging markets projected to grow storage deployments; long-duration storage technologies (pumped hydro's 600+ GW development pipeline and thermal storage systems for industrial applications); and vehicle-to-grid integration enabling electric vehicles to function as distributed energy resources.

Leading companies include Tesla, Inc., Contemporary Amperex Technology Co., Limited (CATL), BYD Company Limited, LG Energy Solution, Samsung SDI, Fluence Energy (a Siemens and AES joint venture), Panasonic Corporation, and Siemens Energy.