- Energy Storage Solutions

- Lead Acid Battery Market

Lead Acid Battery Market Size, Share, and Growth Forecast, 2025 - 2032

Lead Acid Battery Market by Product Type (SLI Batteries, Stationary Batteries, Others), Construction (Flooded Lead Acid Batteries, Others), Application (Automotive, Uninterrupted Power Supply (UPS), Telecom, Data Centers, Others), and Regional Analysis for 2025 - 2032

Lead Acid Battery Market Share and Trends Analysis

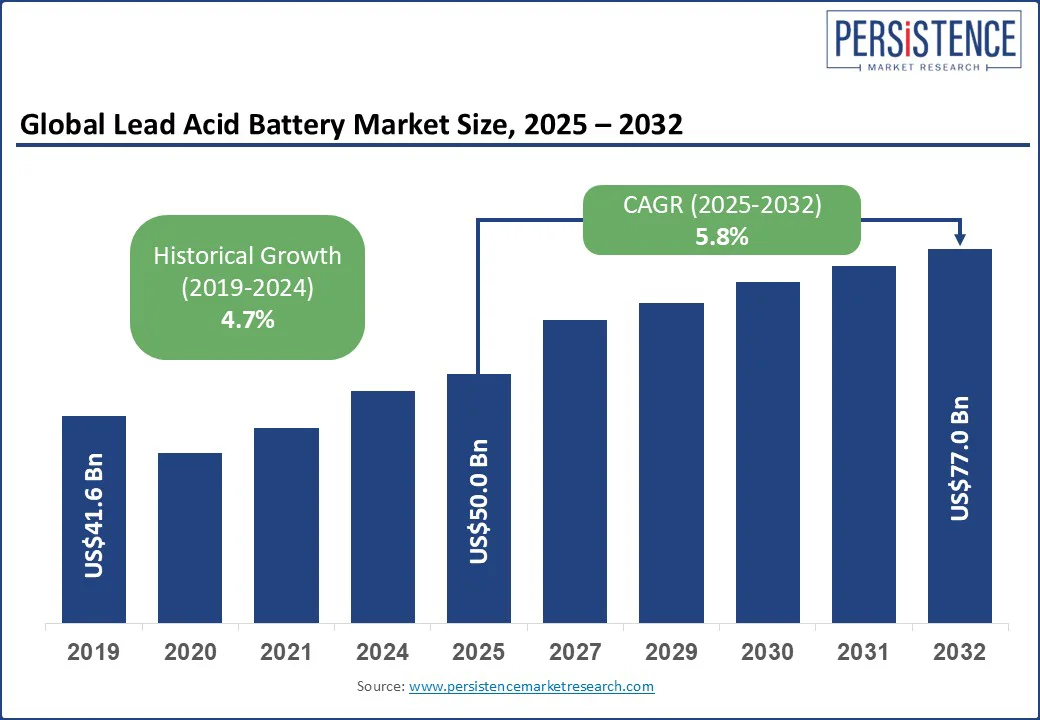

The global lead acid battery market size is likely to be valued at US$50.0 Bn in 2025, and is estimated to reach US$77.0 Bn by 2032, growing at a CAGR of 5.8% during the forecast period 2025-2032.

Key Industry Highlights:

- Prominent Development: In July 2025, GS Yuasa launched its advanced SWL+ series, a new generation of VRLA batteries designed for high-rate discharge and standby power applications in critical environments such as data centers, infrastructure, and manufacturing.

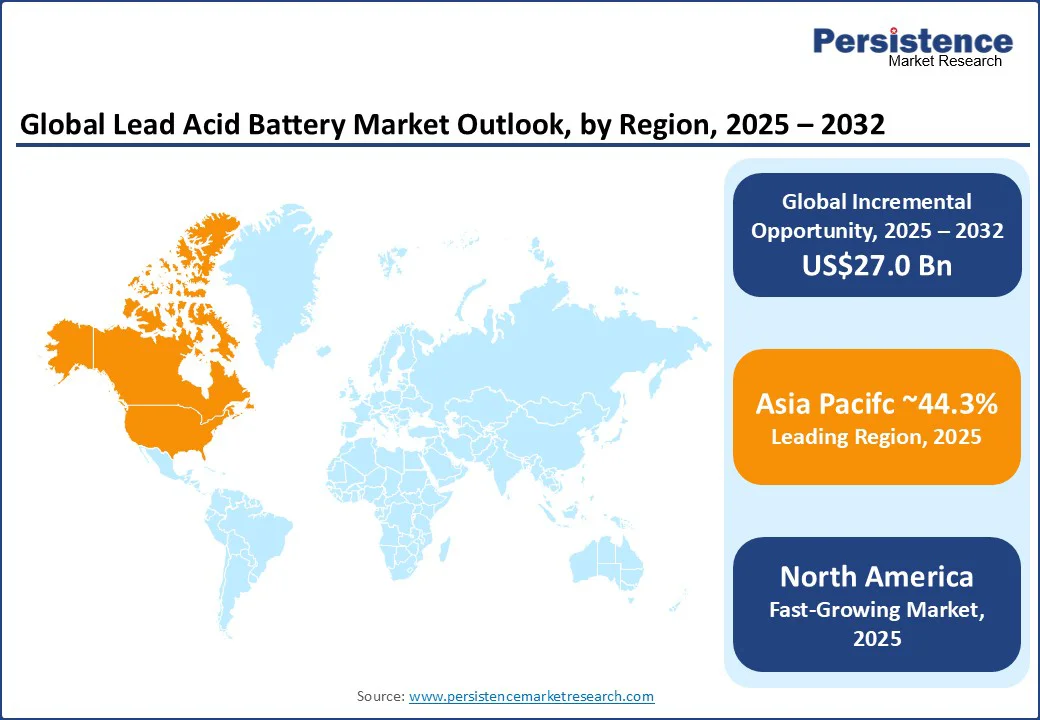

- Dominant Region: Asia Pacific is expected to dominate the market with an estimated 44.3% share in 2025, driven by rapid industrialization and growing automotive ownership across China and India.

- Fastest-growing Regional Market: The North America market is forecasted to grow the fastest over the forecast period, bolstered by strong vehicle electrification initiatives and investments in grid resilience.

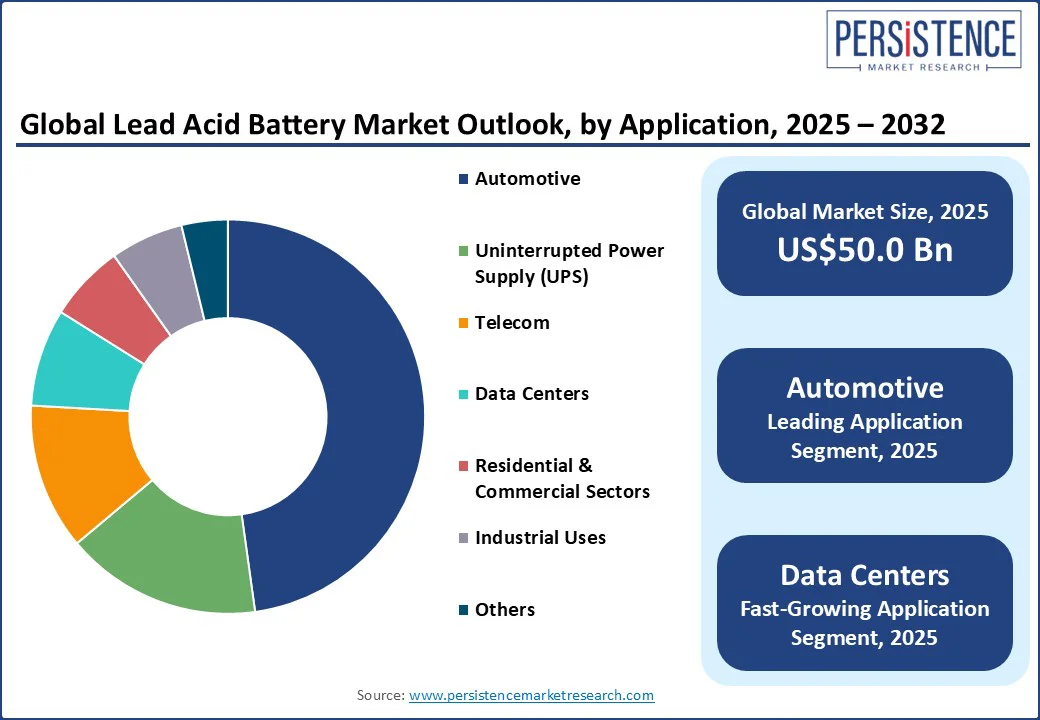

- Leading Application: The automotive segment is slated to lead among applications with nearly 47.8% of the revenue share in 2025, owing to the extensive use of lead acid batteries for starting, lighting, and ignition (SLI) purposes in conventional internal combustion engine (ICE) vehicles.

- Fastest-growing Application Area: The data centers segment is projected to post the highest CAGR through 2032, backed by a surging demand for UPS systems amid IT infrastructure modernization across major economies.

|

Global Market Attribute |

Key Insights |

|

Lead Acid Battery Market Size (2025E) |

US$50.0 Bn |

|

Market Value Forecast (2032F) |

US$77.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.6% |

Rising investments in data centers and telecom infrastructure, which require uninterruptible power systems, are becoming instrumental in fueling the market's growth.

Lead-acid batteries, comprising lead dioxide and sulfuric acid electrodes, are one of the oldest yet most reliable rechargeable energy storage technologies. Known for their robustness, cost-effectiveness, and high surge current delivery, these batteries remain crucial in automotive starting systems, uninterruptible power supply (UPS) solutions, and renewable energy storage. Their renowned recyclability and established global infrastructure have ensured their industrial relevance in an era increasingly dominated by advanced battery chemistries.

The market growth is likely to be steady in the forthcoming years due to multifaceted demand for these batteries across automotive, industrial, and utility sectors. The widening deployment of electric vehicles (EVs) in several large economies, supported by affordable and reliable lead-acid battery solutions, is playing a central role in pushing the boundaries of this market. Furthermore, advancements in valve-regulated lead-acid (VRLA) technology have ensured longer life cycles and lower battery maintenance costs, propelling the adoption of these batteries in commercial and residential structures. Other favorable factors for lead acid batteries include substantial government incentives and corporate funding for sustainable battery recycling and grid stabilization initiatives, highlighting emerging market opportunities.

Market Dynamics

Driver - Expanding Adoption of Electric and Hybrid Vehicles to Catalyze Market Growth

Over the last few years, the demand and adoption of EVs and hybrid electric vehicles (HEVs) have been exponential due to fluctuations in petrol and diesel prices and concerted efforts to reduce air pollution. In 2024, more than 17 million electric cars were sold globally, reflecting a 25% increase from 2023, as per data provided by the International Energy Agency (IEA).

Despite the surge of lithium-ion batteries, lead-acid batteries maintain a unique competitive edge, even in the EV industry, on account of their proven track record in terms of cost-efficiency, reliability, and superior performance in start-stop automotive systems, which represent a sizable section of the automotive industry.

Moreover, global vehicle production rose from approximately 85 million units in 2022 to over 93.5 million units in 2023, as reported by the Organisation Internationale des Constructeurs d'Automobiles (OICA). Innovations such as graphene-enhanced and carbon additive lead acid batteries have vastly improved charge acceptance and cycle life, making these batteries increasingly viable for partial state of charge operations common in hybrid vehicles and renewable energy setups.

Furthermore, governmental incentives and funding, such as the U.S. Department of Energy's multi-hundred-million-dollar investments in lead battery recycling technologies, have spotlighted the strategic importance of lead-acid batteries in energy storage and grid stabilization efforts.

Restraint - Increasing Raw Material Costs and Stricter Environmental Regulations to Curtail Market Momentum

Stringent environmental regulations and volatile lead supply are driving up costs and posing major challenges for the lead-acid battery market. Since early 2024, lead prices have been oscillating between US$2,000 and US$2,400 per ton, a range that triggered unprecedented supply shortages in the secondary lead market, imposing a considerable cost burden on manufacturers.

Simultaneously, the increasing stringency of environmental policies, especially in Europe and North America, has put in place rigorous standards for lead emission controls and disposal, which have escalated compliance costs while limiting battery life cycle flexibility. The other constraint thwarting the market is the intensifying competition from lithium-ion and emerging battery chemistries, favored for higher energy density and lighter weight, enticing key consumers toward alternatives with enhanced performance and higher sustainability profiles.

Opportunity - Booming Demand for Renewable Energy Storage to Stimulate Novel Market Opportunities

For a large number of stakeholders in the lead-acid battery market, the intersection point between the soaring demand for renewable energy storage and the movement toward electric mobility contains a variety of business opportunities. Renewable power installations have surged in recent years, escalating the demand for cost-effective, reliable energy storage solutions to stabilize intermittent supply. Projections by the IEA suggest that global annual renewable energy capacity additions will increase from 666 GW in 2024 to 935 GW in 2030, with solar PV and wind accounting for 95% of all these additions. To power these installations, VRLA batteries, enhanced with advanced carbon additives and graphene, are the perfect candidates based on their affordability and robust lifecycle.

Similarly, the rapid electrification of commercial and passenger vehicles in countries such as India and Southeast Asia will also open unprecedented avenues for lead-acid batteries. A noteworthy example is the 2024 launch of the e-Alfa Plus electric rickshaw by Mahindra Last Mile Mobility, incorporating high-capacity lead acid batteries with warranties emphasizing durability, resonating with cost-conscious fleet operators.

Category-wise Analysis

Application Insights

By application, the automotive segment is expected to lead with an approximate 47.8% market revenue share in 2025, primarily driven by the widespread use of lead acid batteries for starting, lighting, and ignition purposes in conventional internal combustion engine vehicles and now in hybrid electric vehicles as well. The expanding automotive industry, with global vehicle production hitting over 93.5 million units in 2023, creates a robust demand for reliable, cost-effective battery systems.

The growing adoption of start-stop technology in passenger cars to improve fuel efficiency will further fuel the segment expansion in the foreseeable future. Battery innovations such as absorbent glass mat (AGM) and enhanced flooded batteries with improved lifecycle also help automotive original equipment manufacturers (OEMs) to meet their sustainability goals, thereby broadening the market scope.

The fastest-growing application segment is anticipated to be data centers, propelled by rapid digital transformation and expanding cloud infrastructure worldwide. Data centers require UPS systems, where VRLA batteries provide key backup power due to their reliability and cost advantages over other technologies.

The global increase in internet penetration and cloud services, coupled with rising investments in data infrastructure, is likely to catalyze the future growth of the data centers segment. Emerging developments, including modular battery systems and smart diagnostic tools, are improving operational efficiency and disaster resilience in critical infrastructure, driving segment growth.

Construction Insights

The flooded lead-acid batteries segment is estimated to hold around 58.32% of the market revenue share in 2025, largely on account of their cost-effectiveness and robustness, which make them ideal for powering heavy-duty construction equipment, electric shovels, power hand tools, and other portable electric devices. Flooded lead-acid batteries are preferred in demanding work environments where durability and ease of maintenance remain critical. In addition to the above, these batteries have established manufacturing processes and enjoy widespread availability, giving this segment an extra advantage over the others.

At the same time, valve-regulated lead-acid batteries are projected to grow the fastest at an estimated CAGR of nearly 5.0% through 2032. VRLA batteries are gaining traction owing to their maintenance-free nature, enhanced safety profile, and improved cycle life, making them increasingly suitable for stationary power backup, emergency lighting, and clean energy storage applications in both commercial and residential construction projects in rapidly urbanizing regions. This segment also benefits from the proliferation of off-grid renewable energy systems and growing regulatory emphasis on safety and environmental compliance.

Regional Insights

Asia Pacific Lead Acid Battery Market Trends

Asia Pacific is anticipated to hold the largest lead acid battery market share at approximately 44.3% in 2025, backed by rapid industrialization, escalating automobile ownership, and expanding infrastructure development across China and India. The widespread availability of low-cost labor and abundance of raw materials support high-volume manufacturing and export leadership in the region, driving its dominance.

A salient trend is the surge in off-grid renewable energy installations. For example, China boosted its off-grid renewable capacity by nearly 5% in 2021 alone, augmenting the demand for lead acid batteries in rural electrification, telecom, and storage applications. Apart from this, the expansive adoption of electric two-wheelers and commercial vehicles is also likely to contribute to keeping Asia Pacific as a growth epicenter of this market for the foreseeable future.

North America Lead Acid Battery Market Trends

In North America, which is projected to register the highest CAGR through 2032 and secure nearly 26% of the market in 2025, a strong and mature automotive sector, boosted by an increasing demand for start-stop and hybrid vehicle technologies using lead acid batteries, will help the market.

Moreover, rising investments in next-gen grid infrastructure and UPS systems due to the growing frequency and intensity of extreme weather events, such as prolonged hurricanes and wildfires, will also heighten the demand for reliable stationary lead acid battery solutions in the region. The integration of smart battery management and advanced recycling technologies backed by federal initiatives further reinforces the position of North America as the fastest-growing regional market.

Europe Lead Acid Battery Market Trends

The prospects of Europe lead acid battery market are bolstered by stringent environmental regulations and aggressive clean energy transitions under frameworks such as the European Green Deal of the European Union (EU). These ambitions and mandates are expected to enforce a progressive adoption of advanced lead acid batteries, particularly VRLA types, for renewable energy storage and clean mobility applications.

The EU is also undertaking massive IT infrastructure modernization projects, such as the EuroQCI (Quantum Communication Infrastructure), which are also set to fuel the demand for reliable UPS battery systems.

Competitive Landscape

The global lead acid battery market landscape is characterized by technological innovation, sustainability, and strategic partnerships amid growing competition from lithium-ion alternatives. Advancements in VRLA technologies, such as AGM designs and carbon additives, are boosting battery lifecycles and charge efficiency for automotive start-stop systems, renewable energy storage, and telecom backup.

Manufacturers are increasingly aligning their products with circular economy practices, recycling the majority of materials to meet regulations and offset volatile lead prices. Industry consolidation through mergers, acquisitions, and joint ventures is steadily expanding players’ technological and geographic reach, with companies such as Clarios investing heavily in advanced recycling and energy storage solutions. Digital tools, including IoT-enabled diagnostics, are also being leveraged by the top guns to further differentiate their offerings.

Key Industry Developments

- In August 2025, Clarios agreed to acquire Ecobat’s recycling operations in Germany and Austria, strengthening its EU footprint amid the EV shift to lithium-ion and circular models. The deal is expected to close in early 2026, pending approval.

- In July 2025, Exide Industries advanced its lithium-ion push via its subsidiary, Exide Energy Solutions Ltd. (EESL), with cell production expected this fiscal year. It invested INR 1,000 crore (US$120 Mn) in FY25 and plans INR 400 crore (US$48 Mn) in FY26, while adopting a “One-Exide” model and reporting strong growth in most segments.

- In July 2025, Varroc entered India’s two-wheeler aftermarket with new VRLA batteries, offering over four years of service life. Built with AGM tech and calcium alloy, they will be distributed via Varroc’s 730 distributors and 50,000 retailers nationwide.

Companies Covered in Lead Acid Battery Market

- Clarios LLC

- East Penn Manufacturing Company, Inc.

- GS Yuasa International Ltd.

- Exide Technologies

- EnerSys

- Yuasa Battery, Inc.

- Panasonic Corporation

- Amara Raja Batteries Ltd.

- Trojan Battery Company

- C&D Technologies, Inc.

Frequently Asked Questions

The lead acid battery market is projected to reach US$50.0 Bn in 2025.

The increasing demand for and adoption of EVs and hybrid electric vehicles (HEVs) are driving the market.

The lead acid battery market is poised to witness a CAGR of 5.8% from 2025 to 2032.

The global surge in renewable power installations and the transition to clean mobility systems are key market opportunities.

Clarios LLC, East Penn Manufacturing Company, Inc., and GS Yuasa International Ltd. are some leading players.