- Metals & Minerals

- Graphite Market

Graphite Market Size, Share, and Growth Forecast 2026 - 2033

Graphite Market by Graphite Type (Natural Graphite, Synthetic Graphite), Form (Powder, Block, Granule, Others), Purity Level (High Purity ≥99.9%, Medium Purity 95%-99.9%, Low Purity <95%), Application (Refractories, Batteries, Foundries, Lubricants, Friction Products, Electrodes, Conductive Materials, Nuclear Reactors, Other Industrial Applications), by Regional Analysis, 2026 - 2033

Graphite Market Size and Trend Analysis

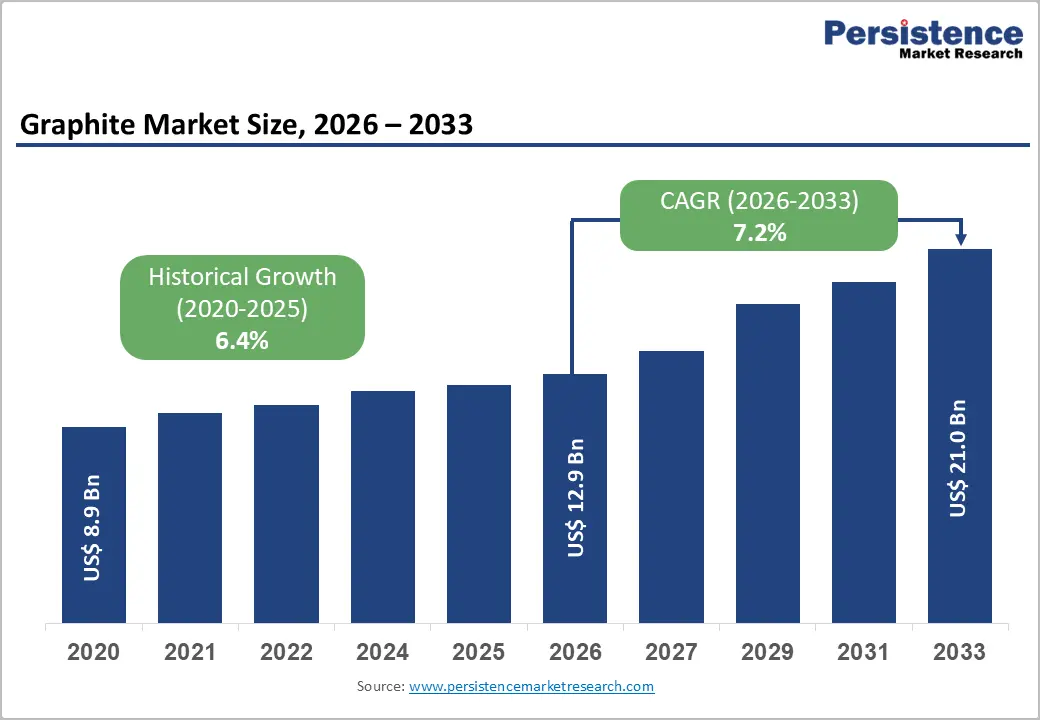

The global graphite market size is expected to be valued at US$ 12.9 billion in 2026 and projected to reach US$ 21.0 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033. The market’s growth trajectory is principally driven by the accelerating global transition to electric mobility and clean energy infrastructure, both of which depend on graphite as a critical anode material in lithium-ion batteries.

According to the International Energy Agency (IEA), global electric car sales surged by 35% year-on-year in 2024, reaching nearly 14 million units, directly amplifying demand for battery-grade graphite. Simultaneously, expanding electric arc furnace (EAF) steelmaking, increasing refractory applications in metallurgy, and rising investments in domestic graphite supply chains across North America and Europe are reinforcing the long-term commercial outlook for the market.

Key Industry Highlights

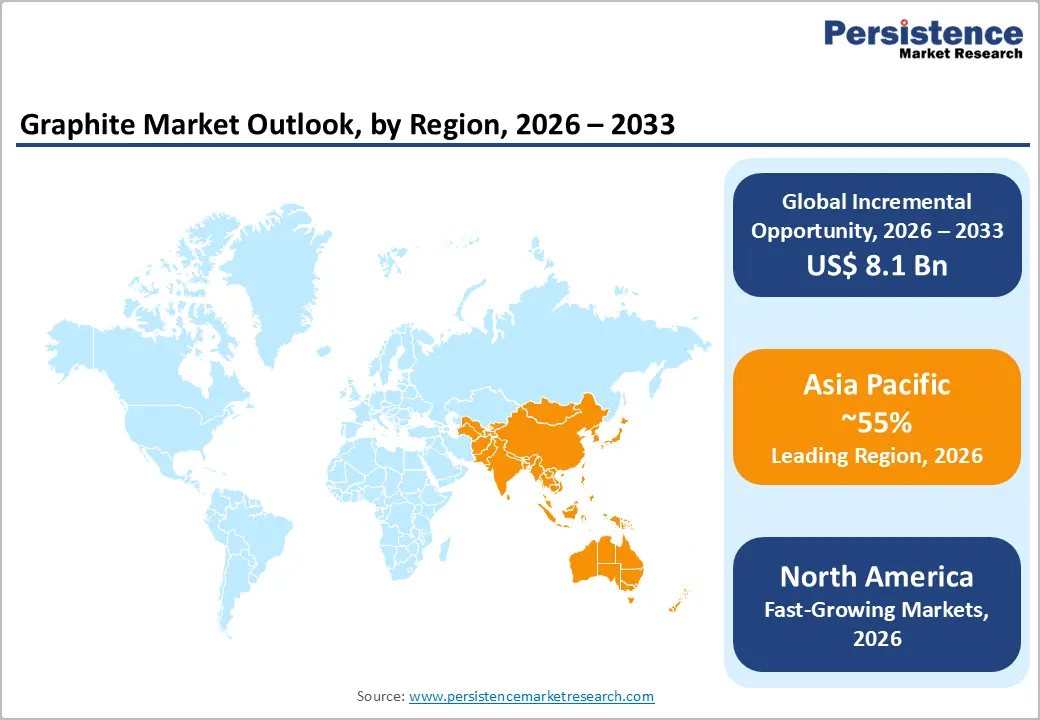

- Leading Region: Asia Pacific leads the global graphite market with approximately 55% revenue share in 2025, underpinned by China’s commanding position as the world’s largest graphite producer and consumer, supported by deep integration across the EV battery and steelmaking supply chains.

- Fastest Growing Region: North America is the fastest-growing regional market, driven by the U.S. Inflation Reduction Act, Department of Energy loan programs, and strategic investments aimed at reducing dependence on Chinese graphite, with industry-scale facilities such as NOVONIX’s Chattanooga plant advancing toward commercial production.

- Dominant Graphite Type Synthetic Graphite dominates the market with a 68% revenue share in 2025, driven by its superior performance in lithium-ion battery anodes and EAF electrodes, with the 10:90 natural-to-synthetic ratio in EV batteries confirming sustained structural demand from the automotive sector.

- Fastest growing Application: The Batteries application segment is the fastest-growing category, poised to record the highest CAGR through 2033, with global battery-grade graphite demand expected to triple from 900,000 tonnes in 2024 to 2.7 million tonnes by 2030 as gigafactory capacity scales globally.

- Key Opportunity: The most compelling market opportunity lies in developing domestic graphite supply chains outside China, with government-backed incentives under the U.S. Inflation Reduction Act, the EU Critical Raw Materials Act, and India’s PLI scheme mobilizing billions in investment for processing, purification, and recycling infrastructure.

Market Dynamics

Drivers - Surge in Demand from Electric Vehicle Battery Manufacturing

The rapid global proliferation of electric vehicles (EVs) represents the most significant structural demand driver for the graphite market. Each battery-electric vehicle requires an average of 136 pounds (approximately 62 kg) of graphite, primarily as anode material in lithium-ion cells, according to analysis published by the Center for Strategic and International Studies (CSIS). With the IEA reporting that global EV sales reached nearly 14 million units in 2024, a 35% year-on-year increase, the consequent spike in battery manufacturing capacity has directly translated into sustained demand for both natural and synthetic graphite.

Industry analysis further indicates that global battery-grade graphite demand is projected to triple from approximately 900,000 tonnes in 2024 to 2.7 million tonnes by 2030, as new gigafactories add roughly 150 GWh of additional cell manufacturing capacity annually. This structural demand pipeline positions graphite as an irreplaceable input within global clean energy supply chains, compelling both automakers and battery producers to secure long-term graphite procurement contracts and accelerating upstream investment.

Expanding Electric Arc Furnace Steelmaking and Industrial Applications

Beyond battery applications, graphite’s critical role in electric arc furnace (EAF) steelmaking and high-temperature metallurgical processes constitutes a robust and enduring demand pillar. Graphite electrodes are indispensable in EAF operations, where they enable the melting of scrap steel at temperatures exceeding 3,000°C, offering superior electrical conductivity and thermal shock resistance. Industry data indicate that approximately 93% of new steelmaking capacity under development as of 2024 is EAF-based, as steelmakers in North America and Europe align their operations with net-zero-emission mandates.

Concurrently, refractories, the second-largest application segment, continue to record stable demand from cement, non-ferrous metal, and glass manufacturing industries. According to industry reports, the refractory segment accounted for over 29% of the graphite market's revenue in 2024, and moderating yet persistent industrial growth in Asia and Latin America is expected to sustain this demand base throughout the forecast period.

Restraints - China’s Export Control Policies and Supply Chain Concentration Risk

The global graphite market faces a pronounced supply vulnerability stemming from overwhelming geographic concentration. China accounts for approximately 77% of the world’s natural graphite production and more than 95% of synthetic graphite production, while refining nearly 100% of global graphite supply, according to analysis by the Center for Strategic and International Studies (CSIS). In October 2023, China’s Ministry of Commerce (MOFCOM) imposed end-user licensing requirements on high-purity and high-quality graphite exports, which took effect in December 2023, introducing compliance costs, procurement delays, and pricing volatility.

Further tightening measures were announced in December 2024 in response to U.S. semiconductor export restrictions. These controls have heightened concerns for downstream industries, particularly EV battery manufacturers in Japan, South Korea, Europe, and North America, constraining supply certainty and elevating the strategic risk premium associated with graphite procurement.

High Energy Intensity and Environmental Costs of Synthetic Graphite Production

The production of synthetic graphite is a highly energy-intensive process that requires heating petroleum coke or coal tar pitch to temperatures exceeding 2,800°C during graphitization, resulting in substantial greenhouse gas emissions and elevated production costs. These energy demands represent a meaningful structural cost barrier, particularly as carbon pricing mechanisms are tightened in key producing regions.

Natural graphite extraction similarly carries significant environmental liabilities, including ecosystem disruption, water contamination, and chemical processing waste from acid purification. Increasingly stringent environmental, social, and governance (ESG) standards imposed by institutional investors and regulatory bodies in Europe and North America are constraining new capacity development timelines, escalating capital expenditure requirements, and pressuring margins across the graphite value chain.

Opportunities - Domestic Graphite Supply Chain Development Backed by Government Policy

Growing geopolitical concerns over China’s dominance of critical mineral supply chains have catalyzed aggressive government-backed investments in domestic graphite production across North America and Europe, creating significant commercial opportunities for market participants. In the United States, the U.S. Department of Energy (DOE) offered NOVONIX Limited a conditional loan commitment of up to US$754 million in December 2024 to co-finance a new synthetic graphite manufacturing plant in Chattanooga, Tennessee, one of the largest public investments in critical mineral processing infrastructure in the country’s history.

Additionally, the U.S. International Development Finance Corporation issued a US$150 million loan to a graphite mining project in Mozambique in 2024, underlining the push to diversify supply. In Europe, Norway’s Vianode secured EUR 150 million in funding in early 2025 to scale output from 10,000 tonnes per annum to 50,000 tonnes per annum by 2030. These policy-backed investments represent material revenue and partnership opportunities for companies positioned along the graphite processing and purification value chain.

Rising Demand from Energy Storage Systems and Renewable Energy Integration

The accelerating build-out of utility-scale and residential energy storage systems (ESS) presents a rapidly expanding demand opportunity for high-purity graphite producers. As governments globally commit to decarbonizing electricity grids, the deployment of lithium-ion-based stationary storage, which relies on graphite anodes identical in specification to those used in EV batteries, is expected to grow substantially through 2033. This demand layer is structurally distinct from the automotive segment and provides diversified demand exposure for graphite suppliers.

Furthermore, nuclear energy’s resurgence as part of low-carbon energy strategies, including investments in Generation IV reactor technologies, is driving renewed demand for nuclear-grade graphite for moderator and reflector applications. The International Atomic Energy Agency (IAEA) has documented growing member state interest in expanding nuclear capacity, creating niche but high-value demand for ultra-high-purity graphite, adding another dimension of commercial opportunity for specialized producers.

Category-wise Analysis

Graphite Type Insights

Synthetic graphite commands an estimated 68% share of the global graphite market in 2025, establishing it as the unambiguous market leader by revenue. The segment’s dominance is attributable to its superior structural uniformity, higher purity consistency, and tailored electrochemical performance compared to natural alternatives, attributes that are essential for battery anode applications in lithium-ion EVs and energy storage systems. According to available industry data, the ratio of natural to synthetic graphite in EV batteries is approximately 10% to 90%, reflecting battery manufacturers’ strong preference for synthetic material in performance-sensitive applications.

In EAF steelmaking, synthetic graphite electrodes are similarly dominant due to their thermal shock resistance and electrical conductivity. Furthermore, advances in graphitization technology, including improvements in the design of continuous graphitization furnaces pioneered by companies such as NOVONIX, are gradually reducing energy costs, incrementally improving the economic profile of synthetic graphite production, and reinforcing segment leadership through the forecast period.

Form Insights

The powder form of graphite holds the leading position in the global market, accounting for approximately 45% of the total market share in 2025. Powdered graphite is the dominant commercial form for battery anode material manufacturing, where it is coated, spheronized, and purified before integration into lithium-ion cells, the fastest-growing application for graphite globally.

In addition, graphite powder is widely used in refractories as a blending additive, in lubricant formulations as a dry-film lubricant, and in conductive coatings and gaskets. The versatility and process compatibility of graphite powder across both high-growth and mature application segments ensure its continued commercial primacy. Companies including Asbury Carbons, Imerys S.A., and Superior Graphite have built specialized powder processing capabilities to cater to the evolving specifications of battery and advanced industrial customers, further consolidating the powder form’s market leadership.

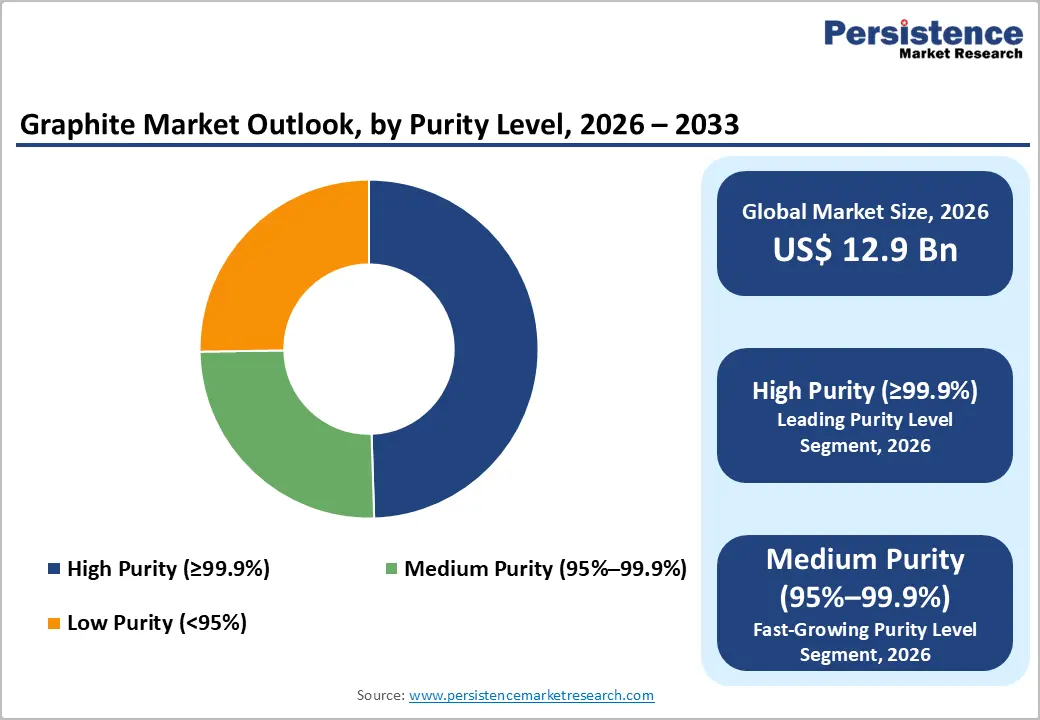

Purity Level Insights

High-purity graphite (≥99.9%) accounts for approximately 49% of the global graphite market by revenue in 2025, reflecting the critical importance of material purity for leading end-use applications. Battery-grade graphite for EV anodes mandates carbon content of 99.95% or higher, as impurities directly compromise electrochemical efficiency, cycle life, and thermal stability. Similarly, nuclear-grade graphite used in reactor moderators and reflectors, as well as in semiconductor processing equipment, demands ultra-high-purity specifications.

As EV production scales globally and battery chemistries become increasingly demanding in terms of material quality, the share of high-purity graphite in total consumption is rising. The purification process, typically involving hydrofluoric acid or high-temperature thermal purification, adds significant value and serves as a key competitive differentiator for producers capable of consistently supplying battery- or nuclear-grade material at commercial scale.

Application Insights

Electrodes represent the leading application segment of the graphite market, accounting for approximately 36% of total market revenue in 2025. Graphite electrodes are indispensable to EAF steelmaking, the process responsible for producing steel through the melting of scrap metal, and their demand is structurally tied to the global steel industry’s transition away from blast furnace operations.

According to industry data, approximately 93% of new steelmaking capacity being commissioned globally as of 2024 is EAF-based, driven by decarbonization mandates in Europe and North America. Leading producers such as GrafTech International and Graphite India Limited supply ultra-high-power (UHP) graphite electrodes specifically engineered for high-current EAF operations. Concurrently, the batteries segment is rapidly gaining share as the fastest-growing application category, with battery anode material demand doubling between 2020 and 2025 and expected to reach 2.7 million tonnes by 2030, positioning batteries as the key growth frontier within the broader application landscape.

Regional Insights

North America Graphite Market Trends and Insights

The North America Graphite Market has emerged as one of the most strategically significant regions in the global graphite landscape, primarily driven by the accelerating domestic transition to electric vehicles and mounting geopolitical pressure to reduce dependency on Chinese graphite imports. U.S. Graphite market size accounting for 88% of the regional market share, has been gaining investor attention, with the U.S. Department of Energy and Department of Defense directing substantial capital toward domestic graphite processing capacity. Initiatives under the Inflation Reduction Act (IRA), including the 48X manufacturing tax credit, have provided material incentives for synthetic graphite producers and processors operating within domestic supply chains.

The U.S. Graphite Market Size context is further reinforced by landmark investments such as NOVONIX’s Chattanooga Riverside facility, slated for commercial-scale industrial graphite production from 2026, alongside a US$754 million conditional DOE loan commitment for an expanded plant. Canada’s Bissett Creek natural graphite mine also restarted operations in 2024, targeting 25,000 tonnes per annum of concentrate. North America is projected to register the fastest growth rate among global regions during the 2026 - 2033 forecast period, driven by policy support, strategic investment, and expanding end-use demand from the EV and energy storage sectors.

Europe Graphite Market Trends and Insights

Europe maintains a significant position in the global graphite value chain, supported by a robust industrial base in steelmaking, automotive manufacturing, and advanced materials processing. Germany's graphite market size reflects the country’s dual role as both a leading consumer of graphite electrodes for EAF steelmaking and a major automotive market undergoing electrification, trends that are deepening domestic graphite demand across both industrial and battery applications.

U.K. graphite market size is anchored in the country’s growing battery gigafactory pipeline and investments by companies such as Talga Group, which secured a EUR 150 million loan from the European Investment Bank to expand its Vittangi natural graphite project in Sweden to 19,500 tonnes per annum by 2027.

France's graphite market size is growing alongside the country’s commitment to EV manufacturing expansion and nuclear energy, both of which demand high-purity graphite. At the regional policy level, the European Union’s Critical Raw Materials Act (CRMA), enacted to reduce strategic material dependencies on third countries, explicitly identifies graphite as a critical raw material and mandates that 10% of EU annual consumption be sourced domestically by 2030. This framework is stimulating investments in regional exploration, processing, and recycling. Vianode’s plant in Herøya, Norway, which raised EUR 150 million in early 2025, exemplifies the scale of capital mobilizing across European jurisdictions to build a resilient, low-carbon graphite supply chain.

Asia Pacific Graphite Market Trends and Insights

Asia Pacific is the dominant graphite-consuming region, accounting for approximately 55% of global market revenue in 2025. China Graphite Market Size is foundational to this regional supremacy; the country not only controls 77% of natural graphite production globally but also processes nearly all of the world’s spherical graphite for battery applications. China’s vertically integrated graphite value chain, combined with sustained government support for the EV and battery industries through the 14th Five-Year Plan, has resulted in both high output volumes and cost-competitive pricing that shape global market benchmarks.

Japan's graphite market remains significant due to the country’s advanced battery-material processing sector, with companies such as Tokai Carbon and major electronics producers maintaining strong demand for high-performance graphite. India Graphite Market Size is emerging as a key growth frontier, as the government’s Production-Linked Incentive (PLI) scheme for advanced chemistry cells (ACC) batteries catalyzes domestic EV battery manufacturing investment. In February 2025, Epsilon Advanced Materials announced plans to invest INR 15,350 crore in EV battery materials infrastructure in Karnataka, including a INR 9,000 crore graphite anode manufacturing facility, underscoring the magnitude of industrial investment beginning to reshape India’s graphite processing landscape.

Competitive Landscape

The global graphite market exhibits a moderately consolidated competitive structure, with a combination of large diversified material science corporations and specialized graphite producers vying for market share across distinct value chain positions. Leading players, including SGL Carbon, GrafTech International, Imerys S.A., and BTR New Material Group, differentiate through proprietary graphitization technology, advanced purification capabilities, and long-term offtake agreements with EV battery manufacturers.

Strategic priorities across the competitive landscape include geographic expansion into supply-chain-diversification markets, vertical integration from mining through processing, and R&D investment in low-carbon production methods. Emerging business models center on circular economy approaches, particularly battery graphite recycling, which are gaining commercial traction in Europe and North America, reshaping traditional supply dynamics and offering new revenue streams for established players and new entrants alike.

Key Developments

- February 2026: Northern Graphite launched a €1.7 million German-funded three-year R&D program with partners to develop cleaner, low-energy graphite processing technologies using recycled battery materials, aiming to build a Europe-based, China-independent supply chain.

- April 2025: Vianode launched a recycled graphite-based anode material for EV batteries, enabling lower carbon emissions, improved battery performance, and reduced reliance on imported raw materials while supporting circular supply chains in North America and Europe.

- February 2025: Sovereign Metals announced that coarse flake graphite from its Kasiya project in Malawi met stringent specifications for refractory-grade graphite, enhancing the project’s potential to serve as a secure, high-quality raw material source for refractory applications across global markets.

Graphite Market - Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 8.9 billion |

| Current Market Value (2026) | US$ 12.9 billion |

| Projected Market Value (2033) | US$ 21.0 billion |

| CAGR (2026 - 2033) | 7.2% |

| Leading Region | Asia Pacific, 55% market share |

| Dominant Category (Graphite Type) | Synthetic Graphite, 68% market share |

| Top-ranking Category (Purity Level) | High Purity (≥99.9%), 49% market share |

| Incremental Opportunity | US$ 8.1 billion |

Companies Covered in Graphite Market

- Imerys S.A.

- Grafitbergbau Kaisersberg GmbH

- GrafTech International

- BTR New Material Group Co., Ltd.

- Northern Graphite

- Mineral Commodities Ltd.

- Asbury Carbons

- Graphit Kropfmühl GmbH

- SGL Carbon

- Mason Resources Inc.

- NOVONIX Limited

- Nacional de Grafite

- Tirupati Carbons & Chemicals Pvt Ltd

- Graphite India Limited

- Superior Graphite

- Syrah Resources Limited

- Talga Group

- Vianode AS

- Epsilon Advanced Materials

- Tokai Carbon Co., Ltd.

Frequently Asked Questions

The global Graphite market is estimated at US$ 12.9 billion in 2026 and is projected to reach US$ 21.0 billion by 2033 at a CAGR of 7.2%.

Growth is driven by rising EV production, increasing lithium-ion battery demand and expanding EAF steelmaking, boosting graphite electrode consumption.

Asia Pacific leads the market due to China’s dominant production, strong value chain integration, and high regional demand.

The biggest opportunity lies in developing non-China graphite supply chains supported by government policies and investments in processing and recycling.

Key players include Imerys S.A., GrafTech International, SGL Carbon, BTR New Material Group, Asbury Carbons, Superior Graphite, and Graphite India Limited.