- Automotive Components & Materials

- Automotive Semiconductor Market

Automotive Semiconductor Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Semiconductor Market Size, Share, and Growth Forecast 2026 – 2033 by Component Location (Processor, Analog IC, Sensor, Memory), Vehicle Type (Passenger Car, LCV, HCV), Application (Powertrain, Safety, Body Electronics, Chassis, Telematics and Infotainment), and Regional Analysis, 2026 - 2033

Automotive Semiconductor Market Size and Trend Analysis

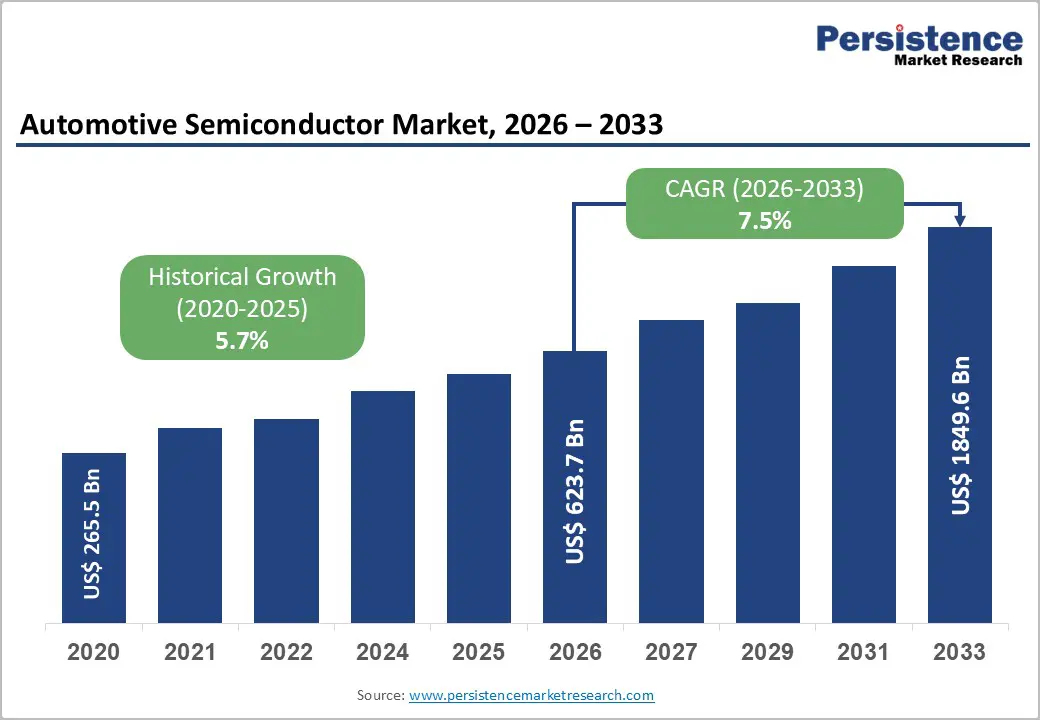

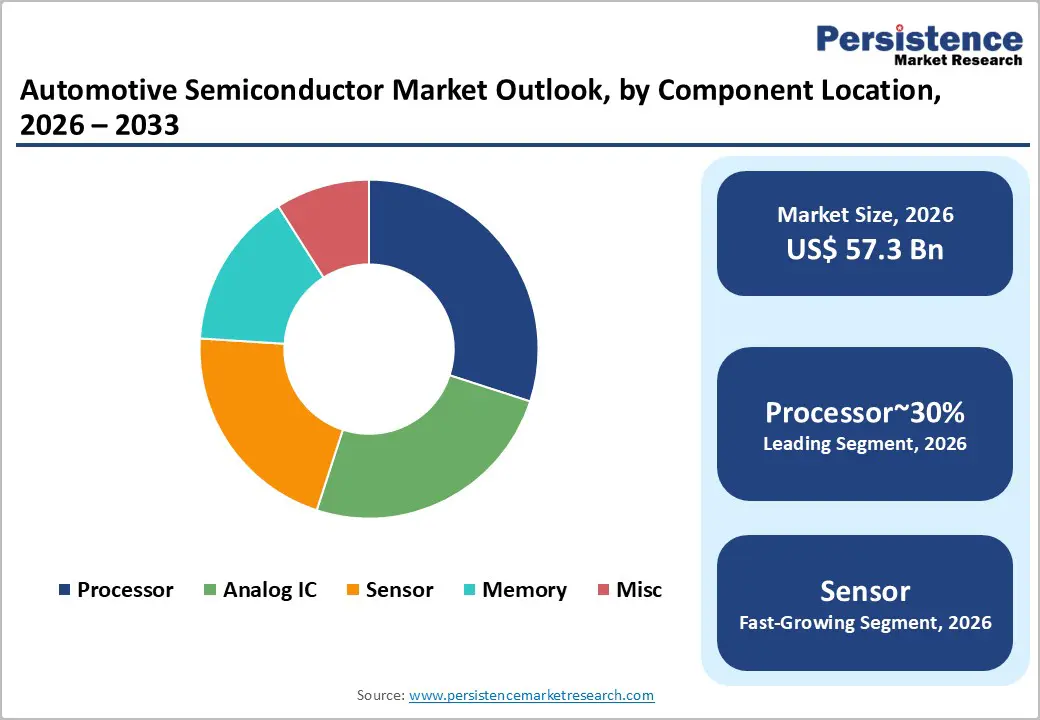

The global automotive semiconductor market size is likely to be valued at US$ 57.3 billion in 2026 and is expected to reach US$ 95.1 billion by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 to 2033. This robust expansion is being driven by the rapid electrification of vehicles, rising demand for advanced driver-assistance systems (ADAS), and the proliferation of connected and autonomous features that require sophisticated processors, sensors, and analog ICs.

Key Industry Highlights:

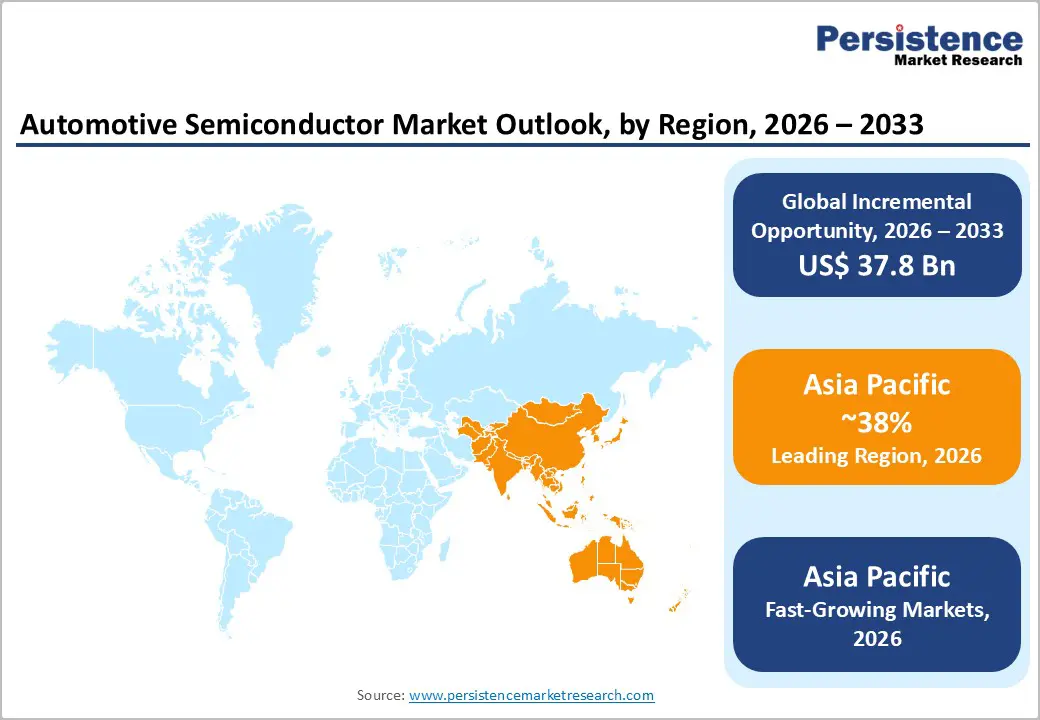

- Leading Region: Asia Pacific leads the automotive semiconductor market with 38% share, due to large-scale EV production, strong automotive manufacturing, and supportive government incentives in China, Japan, and India.

- Fastest-growing region: Asia Pacific is also the fastest-growing region with rising CAGR of 8.9%, driven by rising EV adoption, urbanization, and government-led electrification initiatives in China, India, and ASEAN economies.

- Dominant Component Location: The Analog IC component segment is the dominant category, capturing about 35% share by 2025, thanks to its widespread use in power management, signal conditioning, and sensor interfacing across powertrain, safety, and body-electronics applications.

- Fastest-growing segment: The Sensor component segment is one of the fastest-growing, supported by ADAS, autonomous-driving, and safety-regulation requirements that increase sensor content per vehicle in passenger cars and LCVs.

- Key market opportunity: Expansion into powertrain and electrified systems offers a major opportunity to position power semiconductors, MCUs, and sensors as core enablers of EVs, hybrids, and fuel-cell vehicles across North America, Europe, and Asia Pacific.

| Key Insights | Details |

|---|---|

|

Automotive Semiconductor Market Size (2026E) |

US$ 57.3 Billion |

|

Market Value Forecast (2033F) |

US$ 95.1 Billion |

|

Projected Growth CAGR (2026–2033) |

7.5% |

|

Historical Market Growth (2020–2025) |

5.7% |

Market Dynamics

Drivers - EV Adoption and ADAS Integration Driving Rapid Growth in Automotive Semiconductor Demand Across Global Markets

The rapid shift toward electric vehicles (EVs) and plug-in hybrid electric vehicles (PHEVs) is one of the strongest growth drivers for the automotive semiconductor market. Compared to traditional internal-combustion vehicles, EVs require a significantly higher number of semiconductors, particularly power devices, sensors, and microcontrollers used in battery-management systems, onboard charging units, and motor-control systems.

Across Europe, countries such as Germany, the United Kingdom, France, and Spain have introduced aggressive emission reduction targets and EV adoption mandates, accelerating demand for advanced power technologies such as silicon carbide (SiC) and insulated-gate bipolar transistor (IGBT) components supplied by companies such as Infineon Technologies AG, STMicroelectronics, and ROHM CO., LTD. In North America, investments by U.S. automakers and Tesla in next-generation EV platforms are further strengthening semiconductor demand.

Connected Mobility and Autonomous Driving Technologies Accelerating Semiconductor Content Per Vehicle Worldwide

The increasing adoption of connected and autonomous vehicles represents another powerful growth engine for the automotive semiconductor market. These vehicles depend heavily on advanced processors, memory chips, sensors, and communication integrated circuits to enable real-time data processing, environmental sensing, and over-the-air software updates. In the Asia Pacific region, countries such as China, Japan, and India are making large investments in smart mobility infrastructure, 5G connectivity, and intelligent transportation systems, which are driving strong demand for semiconductors used in ADAS, infotainment, and vehicle-to-everything communication platforms.

North America, collaborations between technology companies and automakers are accelerating the development of autonomous driving systems that require high-performance computing chips and sensor fusion technologies. As vehicles become increasingly software-driven and data-centric, semiconductors are evolving into core enablers of mobility innovation, ensuring long-term growth across the automotive semiconductor market.

Restraints - Ongoing Supply Chain Disruptions and Semiconductor Shortages Limiting Production Stability and Market Expansion

Despite strong long-term demand, the automotive semiconductor market continues to face challenges from supply-chain instability and periodic chip shortages. The global semiconductor disruption that began in 2020 revealed significant weaknesses in foundry capacity planning, raw material availability, and logistics networks, particularly for legacy manufacturing nodes widely used in automotive microcontrollers and power devices. Across Europe and North America, automakers were forced to halt or slow vehicle production, prioritize premium vehicle models, and delay product launches due to limited chip availability.

These disruptions directly impacted semiconductor order volumes in price-sensitive vehicle segments. In addition, heavy dependence on a limited number of global fabrication plants continues to expose the industry to geopolitical risks and operational bottlenecks. Until manufacturing capacity expands and supply chains become more diversified and resilient, supply-side volatility will remain a structural constraint that can temporarily slow revenue growth within the automotive semiconductor market.

High Development Costs and Capital-Heavy Manufacturing Creating Strong Barriers to Entry for New Players

The development of automotive-grade semiconductors requires exceptionally high investments in research, long product qualification timelines, and capital-intensive manufacturing infrastructure, which limits market participation to a small group of major players. Automotive chips must comply with strict reliability standards such as AEC-Q100 and functional safety certifications like ISO 26262, often requiring years of testing before commercial deployment. These rigorous requirements significantly increase development costs and slow time-to-market compared to consumer electronics semiconductors.

Across Asia Pacific, particularly in China and Japan, governments and private firms are investing heavily in domestic fabrication facilities, yet building advanced power semiconductor capacity remains extremely expensive. High fixed costs and long payback periods discourage smaller entrants and startups from competing at scale. As a result, industry concentration remains high, innovation cycles are lengthy, and expansion in niche semiconductor segments progresses at a measured pace across the automotive sector.

Opportunity - Rising Electrification of Powertrains Unlocking Strong Growth Opportunities for Power Semiconductors and Control ICs

Powertrain and electrified vehicle systems are likely to create more opportunities. Electric and hybrid vehicles rely heavily on power semiconductors, microcontrollers, and sensors to manage battery performance, regulate motor speed, and optimize energy efficiency. In Europe, countries such as Germany and France have introduced strict carbon emission reduction policies and zero-emission urban zones, significantly accelerating EV adoption.

This trend is driving strong demand for advanced SiC and gallium nitride (GaN) power devices that improve charging speed and reduce energy loss. In North America, U.S. automakers are rapidly expanding their EV portfolios, increasing the need for sophisticated battery-management ICs, thermal sensors, and motor-control processors. As global EV penetration continues to rise across passenger and commercial vehicles, the powertrain semiconductor segment is expected to deliver some of the fastest revenue growth in the automotive semiconductor market.

Expanding ADAS Adoption and Safety Regulations Fueling Demand for Sensors and High-Performance Processing Chips

Advanced driver-assistance systems and safety-critical electronics present another high-growth opportunity for semiconductor suppliers. Technologies such as radar modules, LiDAR systems, camera sensors, and AI-based processing chips are increasingly becoming standard features not only in luxury vehicles but also in mid-range models. Across Europe, regulatory bodies and consumer safety organizations are promoting higher safety benchmarks, encouraging widespread adoption of features such as automatic emergency braking, adaptive cruise control, and lane-keeping assistance.

In the Asia Pacific region, countries including China and Japan are supporting autonomous vehicle pilot programs and smart transportation projects that depend on high-performance computing platforms and sensor networks. Semiconductor manufacturers such as NXP Semiconductors, Renesas Electronics Corporation, and Analog Devices, Inc. are expanding portfolios to address this growing demand. Rising safety expectations and regulatory mandates will continue to fuel strong growth.

Category-wise Analysis

Component Location Insights

Within the component location category, the processor segment represents the leading revenue contributor, accounting for an estimated 30% share of the automotive semiconductor market by 2025. This segment includes microcontrollers, microprocessors, and application-specific integrated circuits that power critical vehicle functions such as engine control units, advanced safety systems, infotainment platforms, and telematics solutions. In North America, automakers increasingly rely on high-performance processors for managing electrified powertrains and complex ADAS features.

In Europe, particularly in Germany and France, demand remains strong for functional-safety-compliant processors that meet strict automotive reliability standards. As vehicles continue evolving into software-defined platforms with higher computing requirements, the role of processors is expanding rapidly. Growing integration of artificial intelligence, connectivity, and real-time control systems is expected to further strengthen processor demand, making this segment a core growth pillar within the automotive semiconductor market.

Vehicle Type Insights

The passenger car segment dominates the automotive semiconductor market, representing approximately 60% of total revenue by 2025. Passenger vehicles require extensive semiconductor integration across powertrain systems, safety features, body electronics, and infotainment platforms, particularly in electric and premium models. In North America, automakers are continuously increasing semiconductor content per vehicle to enable EV functionality, connected services, and advanced driver assistance technologies.

Across Europe, countries such as Germany, the United Kingdom, and France are witnessing strong consumer demand for enhanced safety, comfort, and digital features, which further boosts chip usage. In Asia Pacific, rapid EV adoption in China and India is significantly raising semiconductor demand across passenger vehicle platforms. High production volumes combined with growing technological complexity ensure that passenger cars remain the primary revenue engine driving long-term expansion of the automotive semiconductor market.

Application Insights

The powertrain segment stands as the largest application area within the automotive semiconductor market, capturing approximately 25% of total revenue by 2025. This segment includes semiconductor solutions for engine control, transmission systems, battery management, and electric motor control. Electrification trends are dramatically increasing the need for advanced power devices, microcontrollers, and precision sensors.

In Europe, carbon emission reduction policies in countries such as Germany and France are pushing automakers toward greater EV and hybrid adoption, boosting demand for SiC and IGBT technologies. In North America, expanding EV production is driving strong growth in battery monitoring ICs and motor-control processors. Meanwhile, Asia Pacific markets such as China and Japan are scaling domestic EV manufacturing, further accelerating powertrain semiconductor consumption. As global electrification continues to intensify, the powertrain segment will remain a fundamental growth pillar for semiconductor suppliers.

Regional Insights

North America Automotive Semiconductor Market Trends

North America represents a highly mature and technology-driven automotive semiconductor market, led by the United States. The region benefits from a strong automotive ecosystem that includes established automakers, EV manufacturers, and advanced technology companies. High adoption of EVs, ADAS, and connected-vehicle features is driving strong demand for processors, sensors, and power semiconductors.

Major suppliers such as Texas Instruments Incorporated, Analog Devices, Inc., and NXP Semiconductors play a central role in supplying automotive-grade components to OEMs and Tier-1 suppliers. Government incentives supporting EV infrastructure and smart-mobility programs are further reinforcing semiconductor investment. With continuous innovation in vehicle automation and electrification, North America remains a high-value market characterized by strong margins, advanced technology adoption, and consistent long-term growth opportunities.

Europe Automotive Semiconductor Market Trends

Europe is a regulation-driven and safety-focused automotive semiconductor market, with Germany, the U.K., France, and Spain leading regional demand. Strict emission standards and vehicle safety regulations are pushing automakers to rapidly adopt EVs, hybrid technologies, and ADAS features. European manufacturers are increasingly investing in SiC and GaN power devices, advanced sensors, and functional-safety-certified processors to meet regulatory requirements.

Consumer demand for premium safety and comfort technologies is also rising, particularly in Western Europe. These trends are increasing semiconductor content per vehicle across both luxury and mid-range models. With strong policy support for electrification and sustainability, Europe continues to represent a high-compliance, high-technology market that drives innovation within the global automotive semiconductor industry.

Asia Pacific Automotive Semiconductor Market Trends

Asia Pacific is the fastest-growing region in the automotive semiconductor market, driven by China, Japan, India, and Southeast Asian economies. China and Japan possess highly developed automotive and semiconductor ecosystems, with strong EV production and rapid adoption of ADAS technologies. India is witnessing rising urbanization, increasing disposable income, and government incentives for electric mobility, which are boosting semiconductor demand in passenger vehicles.

ASEAN countries such as Thailand, Vietnam, and Indonesia are expanding automotive manufacturing bases, creating new consumption centers for power devices, sensors, and processors. Additionally, large investments in domestic semiconductor fabrication across China and India are strengthening regional supply chains. This combination of manufacturing expansion, electrification, and rising vehicle electronics content positions Asia Pacific as the primary growth engine of the global automotive semiconductor market.

Competitive Landscape

The automotive semiconductor market is moderately consolidated, dominated by a group of global technology leaders alongside several specialized regional players. Companies such as Infineon Technologies AG, NXP Semiconductors, Renesas Electronics Corporation, STMicroelectronics, Texas Instruments Incorporated, and Analog Devices, Inc. hold strong market positions through advanced manufacturing capabilities, functional-safety certifications, and long-term relationships with automakers and Tier-1 suppliers.

These firms differentiate through proprietary process technologies, high-reliability product portfolios, and extended product lifecycles tailored for automotive applications. Heavy investment in R&D is driving innovation in silicon carbide and gallium nitride power devices, AI-enabled processors, and next-generation sensors. Strategic partnerships, long-term supply agreements, and custom chip co-development are becoming common, strengthening customer loyalty and raising barriers to entry. This structure supports stable growth while limiting intense price competition across the market.

Key Market Developments

- In October, 2024: Infineon Technologies AG unveiled the HybridPACK™ Drive G2 Fusion, an innovative power module that blends silicon and silicon-carbide (SiC) technology to boost efficiency and reduce inverter system costs for electric vehicles in Europe and North America, helping OEMs optimize EV traction performance without compromising range or reliability.

- In March, 2025: NXP Semiconductors launched a next-generation applications processor with AI-enabled sensor fusion designed for advanced driver-assistance systems in premium passenger cars across North America and Europe, delivering improved real-time sensing, in-cabin monitoring, and safety processing capabilities.

- In July, 2025: STMicroelectronics expanded its automotive sensor portfolio by acquiring part of NXP’s MEMS sensors business, strengthening its high-precision temperature, pressure, and electromechanical sensor offerings for electric and hybrid vehicles in Asia Pacific and Europe to support safety, powertrain, and comfort functions.

Companies Covered in Automotive Semiconductor Market

- Analog Devices, Inc.

- Infineon Technologies AG

- NXP Semiconductors

- Renesas Electronics Corporation

- Robert Bosch GmbH

- ROHM CO., LTD.

- Semiconductor Components Industries, LLC

- STMicroelectronics

- Texas Instruments Incorporated

- TOSHIBA CORPORATION

- ON Semiconductor Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Micron Technology, Inc.

Frequently Asked Questions

The global automotive semiconductor market is valued at US$ 57.3 Billion in 2026 and is projected to reach US$ 95.1 Billion by 2033, growing at a CAGR of 7.5% during the forecast period.

Key drivers include vehicle electrification, advanced driver‑assistance systems (ADAS), and connected‑car features, which require processors, sensors, analog ICs, and memory for EVs, hybrids, and autonomous‑driving platforms across North America, Europe, and Asia Pacific.

The Analog IC segment dominates, capturing about 35% share by 2025, because analog ICs are essential for power management, signal conditioning, and sensor interfacing in powertrain, safety, and body‑electronics applications.

Asia Pacific leads the automotive semiconductor market, supported by large‑scale EV production, strong automotive manufacturing, and government‑led electrification initiatives in China, Japan, and India.

A key opportunity lies in expanding into powertrain and electrified systems, where power semiconductors, MCUs, and sensors are essential for EVs, hybrids, and fuel‑cell vehicles, enabling growth in high‑value, safety‑critical applications.