- Electric Mobility

- Electric Powertrain Market

Electric Powertrain Market Size, Share, and Growth Forecast, 2025 - 2032

Electric Powertrain Market by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Two and Three-Wheeler, Off-Highway Vehicles), Propulsion Type (Battery Electric Vehicle, Plug-in Hybrid Electric Vehicle, Fuel-Cell Electric Vehicle), Component, and Regional Analysis for 2025 - 2032

Electric Powertrain Market Size and Trend Analysis

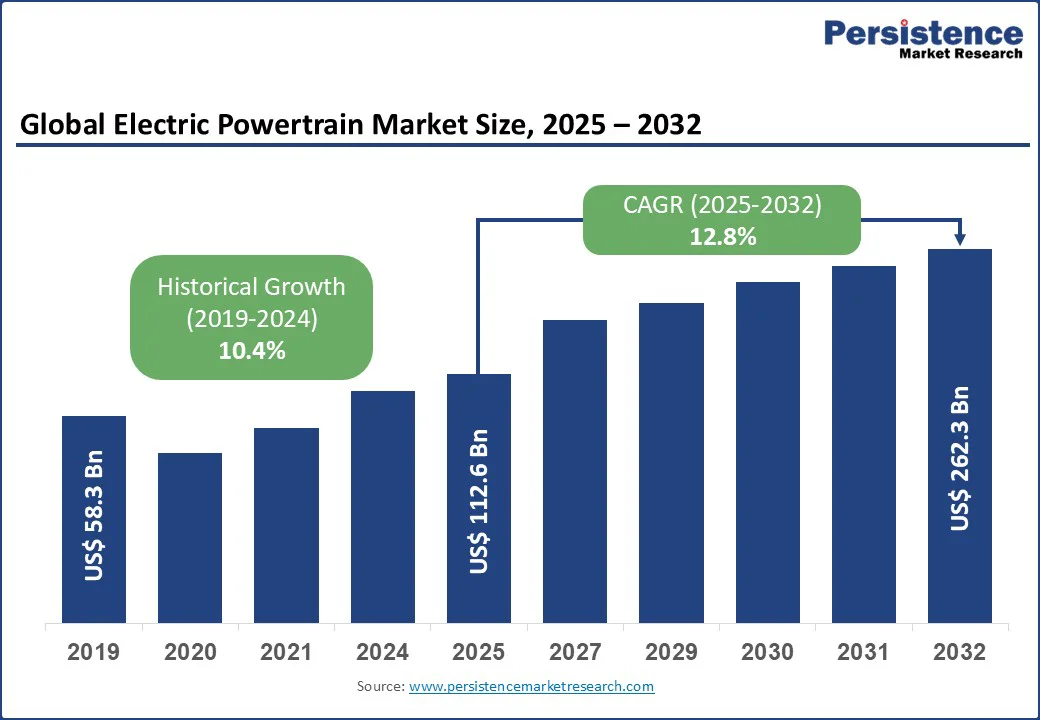

The global electric powertrain market size is likely to value at US$ 112.6 Bn in 2025 and reach US$ 262.3 Bn by 2032, growing at a CAGR of 12.8% during the forecast period from 2025 to 2032.

The electric powertrain market is experiencing robust growth, driven by the global shift toward sustainable transportation, stringent emission regulations, and advancements in battery technology. Electric powertrains, comprising critical components such as motors, batteries, and power electronics, are pivotal in enabling efficient and eco-friendly mobility across various vehicle types.

Key Industry Highlights:

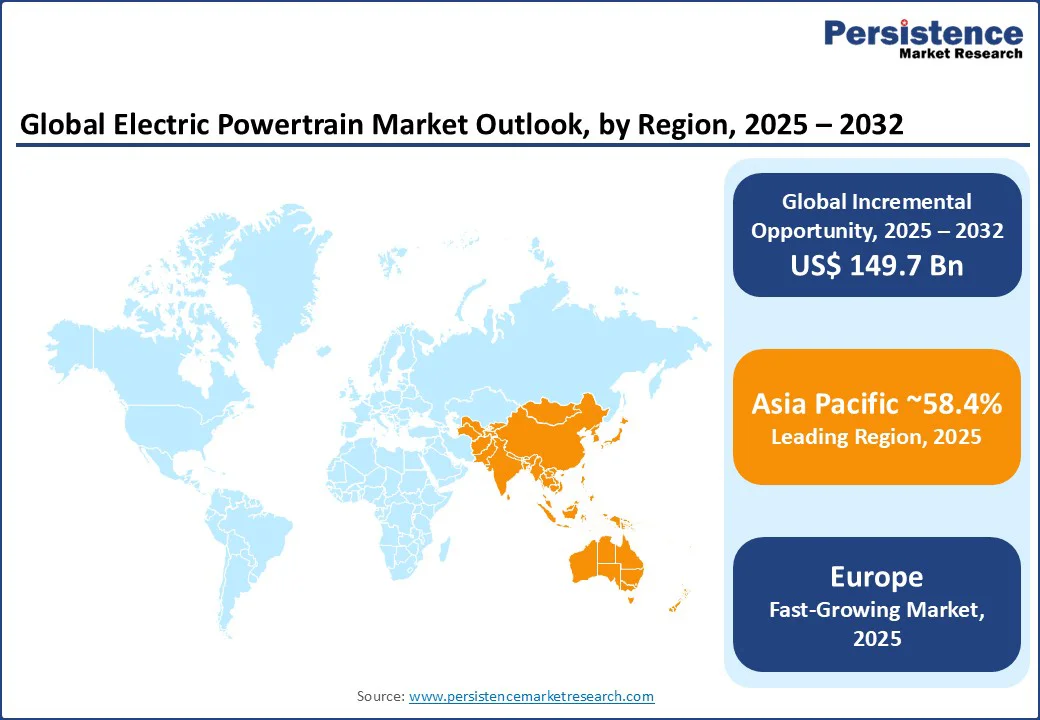

- Leading Region: Asia Pacific holds a 58.4% share in 2025, driven by high EV adoption rates, robust manufacturing capabilities, and supportive policies in countries such as China and Japan.

- Fastest-Growing Region: Europe emerges as the fastest-growing region, fueled by stringent EU emission standards and significant investments in EV infrastructure across Germany, France, and Norway.

- Investment Plans: China’s 2023 New Energy Vehicle (NEV) Industry Development Plan targets 25% of vehicle sales to be electric by 2025, boosting demand for electric powertrains in passenger cars and commercial vehicles.

- Dominant Vehicle Type: Passenger cars account for 62.5% of market revenue, driven by rising consumer demand for electric sedans and SUVs, particularly in urban areas.

- Leading Propulsion Type: Battery Electric Vehicles (BEVs) contribute 69.8% of market share, supported by advancements in battery range and charging infrastructure.

| Key Insights | Details |

|---|---|

| Electric Powertrain Market Size (2025E) | US$112.6 Bn |

| Market Value Forecast (2032F) | US$262.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 12.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.4% |

Market Dynamics

Driver: Stringent Emission Regulations and Government Incentives

The electric powertrain market is witnessing significant growth due to stringent emission regulations and supportive government policies worldwide. Governments are implementing rigorous standards to curb carbon emissions, driving the adoption of electric vehicles equipped with advanced powertrains.

The European Union’s CO2 emission targets aim for a 55% reduction by 2030, compelling automakers to prioritize electric powertrains. In China, the New Energy Vehicle (NEV) policy offers subsidies and tax exemptions, with the China Association of Automobile Manufacturers reporting a 35% increase in EV sales in 2024.

In the U.S., the Inflation Reduction Act provides tax credits of up to $7,500 for EV buyers, boosting demand for powertrain components. Companies such as Tesla and BYD have reported increased production to meet this demand, with Tesla’s Gigafactory in Shanghai scaling output by 20% in 2024. Rising consumer awareness of environmental concerns and government-led initiatives ensure sustained market growth through 2032.

Restraint: High Initial Costs and Battery Supply Chain Challenges

The electric powertrain market faces challenges due to high initial costs and supply chain constraints for critical components, such as batteries. The production of electric powertrains, particularly batteries, involves expensive raw materials such as lithium and cobalt, subject to price volatility. In 2024, lithium prices surged, impacting production costs, per the International Energy Agency. This cost burden affects affordability, particularly in price-sensitive markets, limiting EV adoption.

Additionally, supply chain disruptions, including shortages of semiconductors and rare earth materials, hinder scalability. Synthetic alternatives, such as solid-state batteries, are still in early development, delaying cost reductions. These challenges create pricing pressures for manufacturers such as Bosch and Magna, constraining market growth in regions with lower purchasing power, despite growing demand for sustainable mobility solutions.

Opportunity: Advancements in Battery Technology and Charging Infrastructure

Advancements in battery technology and expanding charging infrastructure are transforming the electric powertrain market, driving rapid growth and innovation. Breakthroughs in solid-state batteries and ongoing improvements in lithium-ion technology are significantly increasing energy density while reducing charging times, as projected by the International Energy Agency’s forecast of a 40% rise in battery energy density by 2030.

This enables electric vehicles (EVs) to achieve longer driving ranges, making them more attractive to consumers and boosting demand for advanced powertrain components. Leading companies such as Mitsubishi Electric and Nidec are developing highly efficient motors and electronic controllers, enhancing overall powertrain performance and reliability.

Simultaneously, investments in charging infrastructure are critical for widespread EV adoption. For example, Electrify America expanded its fast-charging network by 25% in 2024, enhancing support for both passenger and commercial electric vehicles.

Coupled with robust government incentives, such as the European Union’s Green Deal, these technological and infrastructural developments create compelling opportunities for manufacturers to innovate, scale production, and capture increasing market share through 2032 and beyond.

Category-wise Analysis

By Vehicle Type

- Passenger cars are dominant, and account for a 62.5% share in 2025. The segment’s growth is driven by rising consumer demand for electric sedans, SUVs, and hatchbacks, particularly in urban areas with stringent emission regulations. Companies such as Tesla and BYD lead with extensive portfolios, offering models such as the Tesla Model Y and BYD Han, which integrate advanced powertrains for enhanced range and performance. Government incentives, such as China’s NEV subsidies and Europe’s EV purchase grants, further boost demand, making passenger cars the cornerstone of the electric powertrain market.

- The two and three-wheeler segment is the fastest-growing, driven by increasing adoption in the Asia Pacific and urban mobility trends. Electric scooters and motorcycles, such as those from Super Soco and Ola Electric, rely on compact, efficient powertrains for cost-effective urban transport. Rapid urbanization and last-mile delivery needs in countries such as India and Indonesia fuel this segment’s growth, supported by affordable models and government-backed electrification initiatives.

By Propulsion Type

- BEVs account for the largest share at 69.8% in 2025, driven by advancements in battery technology and widespread charging infrastructure. Models such as the Tesla Model 3 and Nissan Leaf utilize high-efficiency powertrains, offering superior range and zero-emission performance. Government policies, such as China’s NEV mandates and Europe’s CO2 targets, prioritize BEVs, making them the preferred choice for manufacturers and consumers seeking sustainable mobility solutions.

- FCEVs are the fastest-growing propulsion type, propelled by investments in hydrogen infrastructure and their suitability for heavy-duty applications. Companies such as Toyota and Hyundai are advancing FCEV powertrains, with models such as the Toyota Mirai leveraging fuel cells for long-range capabilities. Growing government support, such as Japan’s hydrogen strategy and Germany’s H2 funding, drives adoption in commercial and off-highway vehicles, positioning FCEVs for rapid expansion.

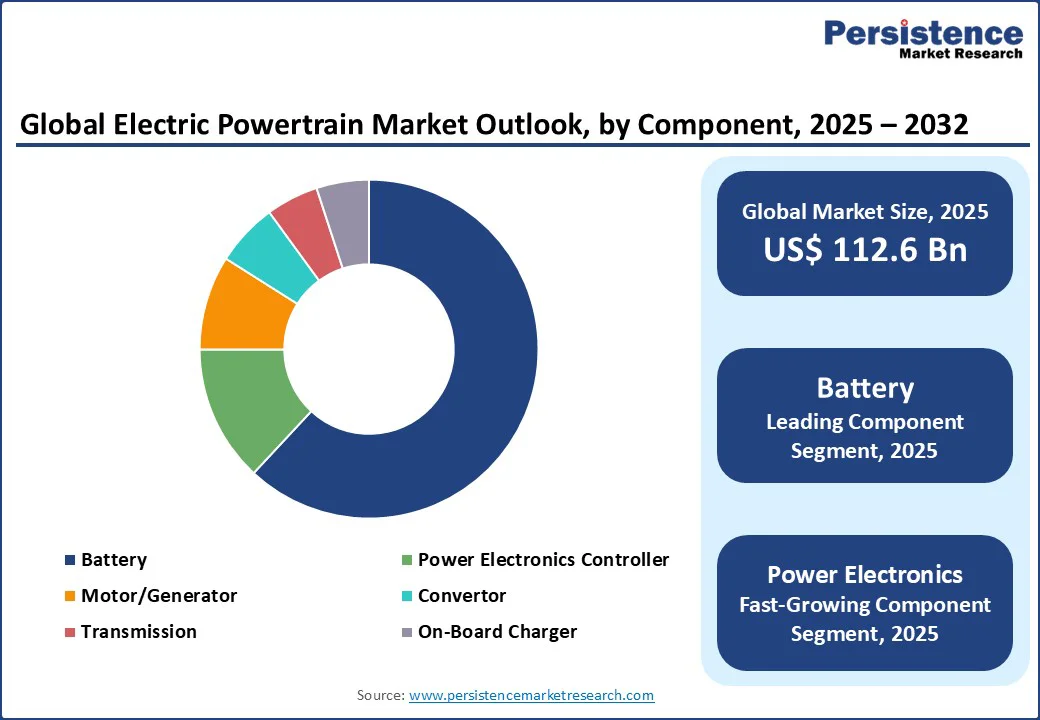

By Component

- Batteries account for the largest share, approximately 61.8% share, driven by their critical role in EV performance and range. Lithium-ion batteries dominate, with companies such as CATL and LG Chem supplying high-capacity units for passenger cars and commercial vehicles. Innovations in energy density and cost reductions, supported by economies of scale, ensure batteries remain the most significant component in powertrain systems through 2032.

- Power electronics controllers are the fastest-growing component, driven by their role in optimizing powertrain efficiency and vehicle performance. These controllers manage energy flow between batteries and motors, with companies such as Bosch and Hitachi Astemo innovating for higher efficiency. The increasing complexity of EV systems and demand for fast-charging capabilities in regions such as Europe and North America fuel rapid growth in this segment.

Regional Insights

Asia Pacific Electric Powertrain Market Trends

Asia Pacific emerges as a dominant region in 2025, commanding 58.4% share. This leadership is primarily fueled by robust electric vehicle (EV) adoption and advanced manufacturing capabilities in China, Japan, and South Korea.

China, as the world’s largest EV market, produced around 12 million EVs out of 17 million global units in 2024, accounting for over 70% of global production. With approximately 11 million EVs sold domestically, China’s NEV policies and subsidies play a crucial role in sustaining this momentum.

Meanwhile, Japan is accelerating fuel cell electric vehicle (FCEV) powertrain demand through its strong emphasis on hydrogen technology, complementing the battery-driven growth led by South Korean giants such as LG Chem. Additionally, rapid urbanization, government incentives, and expanding charging infrastructure, exemplified by India’s FAME II program, further solidify the region’s dominance.

Europe Electric Powertrain Market Trends

Europe is emerging as the fastest-growing market for electric powertrains, driven by stringent CO2 emission regulations and substantial investments in EV infrastructure. Countries such as Germany, France, and Norway are at the forefront of this transition, with Germany’s automotive sector playing a crucial role in powering demand for advanced electric powertrains in passenger vehicles.

The European Union’s ambitious Green Deal, coupled with a dedicated €7 billion investment to deploy one million charging stations by 2025, is accelerating EV adoption across the continent. This infrastructure build-out addresses range anxiety and supports widespread use of electric vehicles.

Leading companies such as ZF Friedrichshafen and Siemens AG are innovating by developing high-efficiency electric motors and sophisticated controllers, aligning their technologies with Europe’s strong emphasis on sustainability and regulatory compliance. These combined efforts position Europe as a global leader in clean mobility, with continued growth expected well into the next decade.

North America Electric Powertrain Market Trends

North America stands as the second fastest-growing region, propelled by strong demand across the U.S. and Canada. The U.S. market heavily relies on advanced powertrain technologies for passenger cars and light commercial vehicles. Robust federal policies, including tax incentives and stringent emissions standards, are accelerating EV adoption. Similarly, Canada’s zero-emission vehicle mandates are driving a rapid transition toward electrification.

Leading companies such as Tesla and BorgWarner dominate with their cutting-edge powertrain solutions and extensive distribution networks, ensuring wide availability and reliability.

Infrastructure investments are equally critical; Electrify America’s significant expansion of its fast-charging network by 25% in 2024 is a prime example, addressing range anxiety and enabling greater EV accessibility. Combined with continued innovation in battery and motor technology, these factors position North America for sustained growth and leadership in the electric powertrain market through 2032.

Competitive Landscape

The global electric powertrain market is highly competitive, characterized by a mix of global giants and specialized players. Companies such as Tesla, BYD, and Bosch Mobility lead through innovation and extensive supply chains, while Magna International and ZF Friedrichshafen focus on integrated powertrain solutions.

The market is moderately fragmented, with regional players such as Nidec Corporation excelling in the Asia Pacific. Investments in R&D for battery efficiency and power electronics are key strategies, driven by demand for high-performance, sustainable powertrains.

Key Industry Developments

- March 2025: Mitsubishi Motors and Foxtron (a Foxconn subsidiary) signed a Memorandum of Understanding (MOU) to supply Mitsubishi with an EV model developed by Foxtron, to be manufactured in Taiwan by Yulon Motor Co., with launch planned for Australia and New Zealand in the second half of 2026. This move is part of Mitsubishi's strategy to reduce costs and accelerate its EV development, while also allowing Foxconn to enter the EV manufacturing market.

- July 2024: QuantumScape and Volkswagen's battery subsidiary, PowerCo, formalized a partnership to industrialize solid-state lithium-metal batteries for mass production, building on PowerCo's existing investment and technology platform. The agreement includes licensing payments for PowerCo to mass produce QuantumScape's QSE-5 cell, a 12.2-minute fast-charging solid-state cell, with a commercial launch potentially by 2028 to outfit vehicles with higher energy density, faster charging, and improved safety.

Companies Covered in Electric Powertrain Market

- Tesla, Inc.

- BYD Co. Ltd.

- Bosch Mobility

- Magna International Inc.

- BorgWarner Inc.

- ZF Friedrichshafen AG

- Dana Incorporated

- GKN Automotive

- Hitachi Astemo, Ltd.

- Mitsubishi Electric Corporation

- AVL List GmbH

- Cummins Inc.

- Siemens AG

- Nidec Corporation

- Others

Frequently Asked Questions

The Electric Powertrain market is projected to reach US$112.6 Bn in 2025.

Stringent emission regulations, government incentives, and advancements in battery technology are key market driver.

The electric powertrain market is poised to witness a CAGR of 12.8% from 2025 to 2032.

Advancements in battery technology and the expansion of charging infrastructure are key market opportunities.

Tesla, BYD, Bosch Mobility, and Magna International are key market players.