- Automotive Components & Materials

- Automotive Exhaust Systems Market

Automotive Exhaust Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Exhaust Systems Market by Product type (Exhaust Manifold, Muffler, Catalytic Converter, Oxygen Sensor and Exhaust Pipes), by Fuel Type (Gasoline and Diesel), by Vehicle Type (Passenger Car, LCV and HCV), and Regional Analysis for 2026 - 2033

Automotive Exhaust Systems Market Size and Trends Analysis

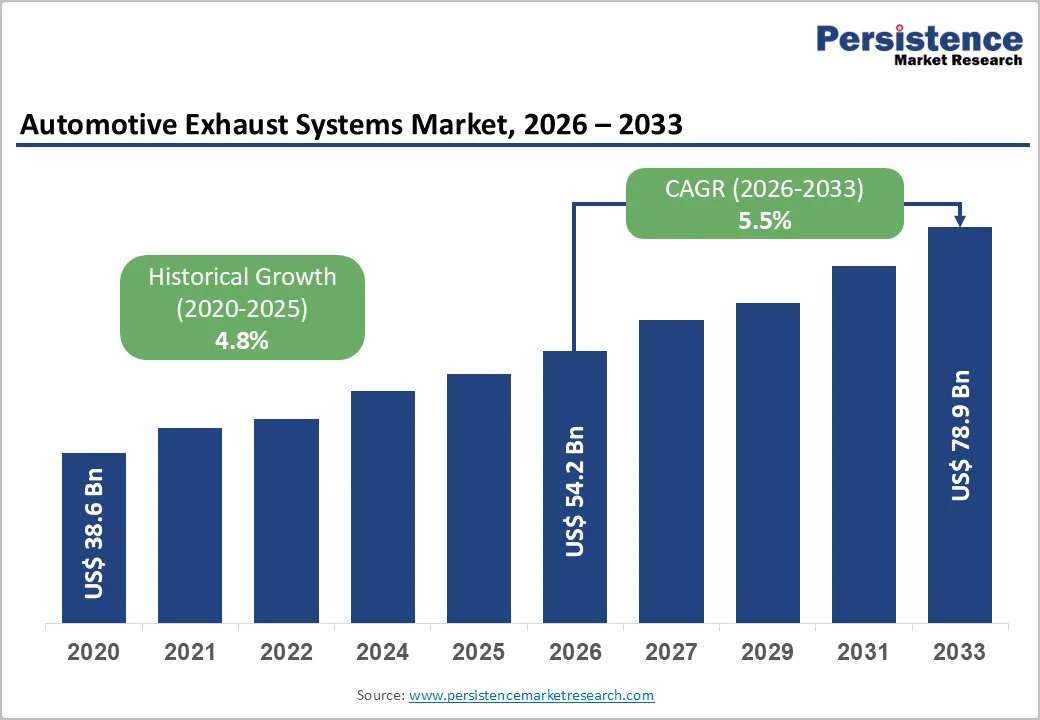

The global automotive exhaust systems market size is likely to value at US$ 54.2 billion in 2026 and is projected to reach US$ 78.9 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Growth is underpinned by stringent tailpipe emission regulations, continued production of gasoline and diesel vehicles in emerging markets, and ongoing demand for cost-effective aftertreatment in light commercial and heavy vehicles. Within the component mix, exhaust manifolds account for about 38.8% of revenues, while mufflers are the fastest-growing subsegment, reflecting both regulatory and NVH (noise, vibration, harshness) requirements.

Key Industry Highlights:

- Component Leadership: Exhaust manifolds dominate the market with a 38.8% share, driven by their critical role in engine performance, thermal management, and emission control. Mufflers represent the fastest-growing component segment, projected to grow at approximately 8.6% CAGR.

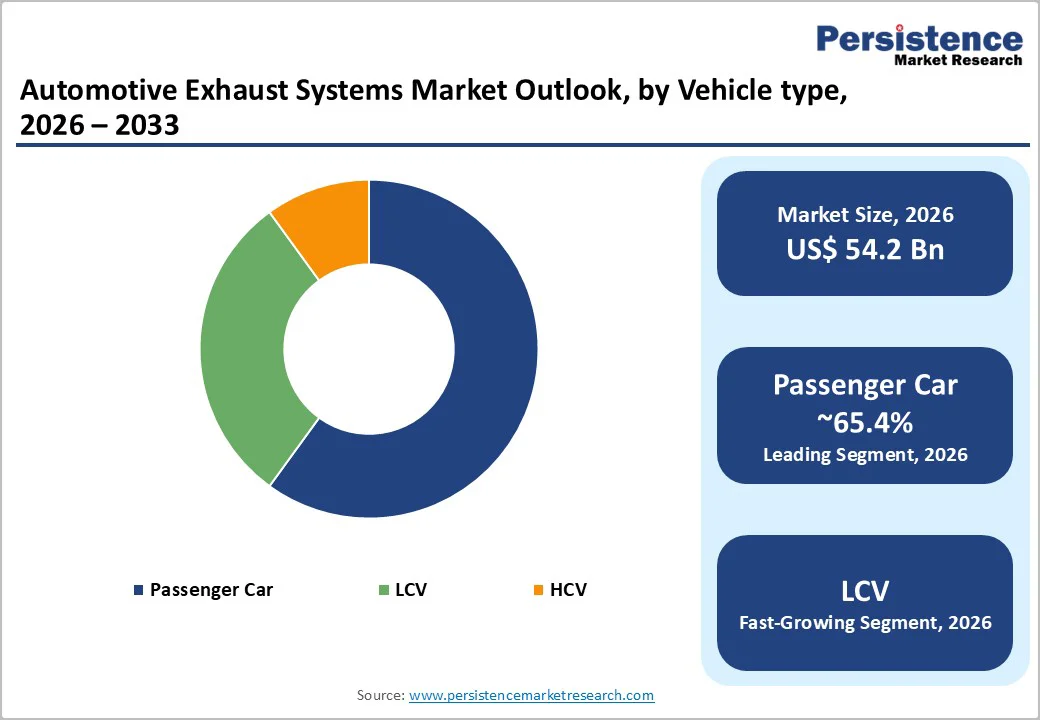

- Fuel & Vehicle Mix Dynamics: Gasoline vehicles command about 83.2% market share, supported by large global passenger car fleets and lower emission control complexity compared to diesel engines. Passenger cars remain the leading vehicle category with ~65.4% share. Light commercial vehicles (LCVs) are the fastest-growing segment, propelled by expanding e-commerce logistics, last-mile delivery demand, and urban mobility requirements.

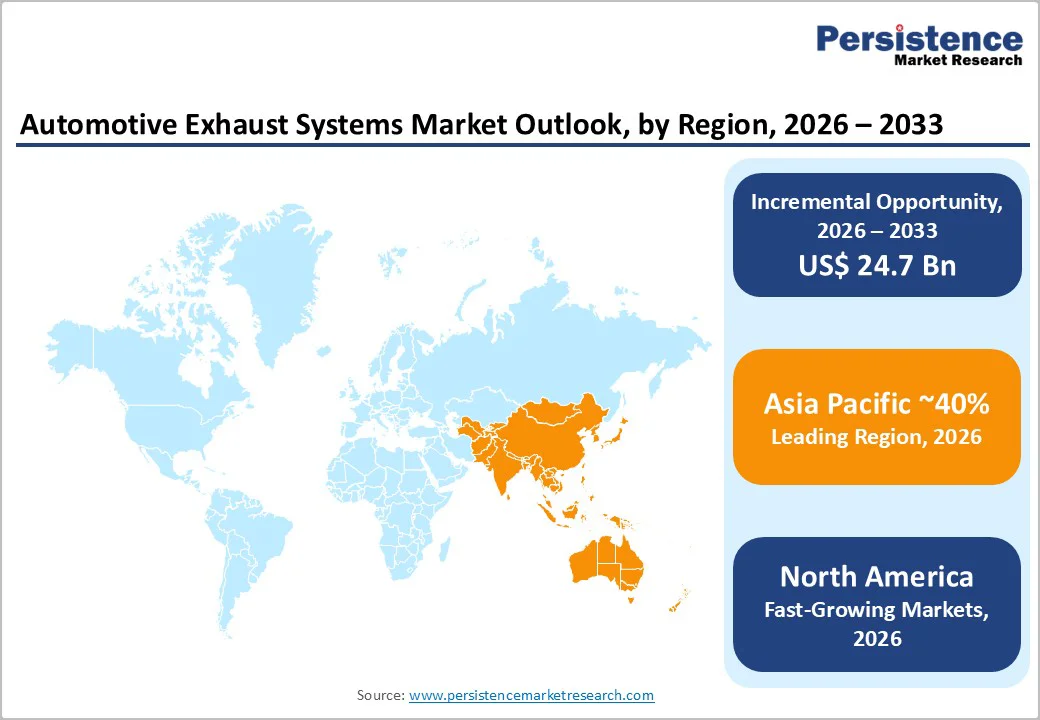

- Regional Growth Patterns: Asia Pacific leads the global market with approximately 40% revenue share, driven by large-scale vehicle production across China, India, and Japan. North America and Europe continue functioning as regulatory and technology innovation hubs, shaping global exhaust system design, materials, and performance standards.

- Regulatory Catalysts: Emission norms such as Euro 7, U.S. EPA updates, and upcoming China VII / BS VII standards are tightening NOx and particulate matter limits by 50–60% compared to previous norms. These regulations significantly increase exhaust system content, complexity, and the need for advanced thermal, filtration, and aftertreatment solutions.

- Strategic Developments: Recent advancements, including Tenneco’s 2024 thermal management system launch, Faurecia’s lightweight aluminum manifold innovations, and Euro 7 implementation, are accelerating the shift toward high-value exhaust solutions.

| Key Insights | Details |

|---|---|

|

Automotive Exhaust Systems Market Size (2026E) |

US$ 54.2 Bn |

|

Market Value Forecast (2033F) |

US$ 78.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.5% |

|

Historical Market Growth (CAGR 2020 to 2024) |

4.8% |

Market Dynamics

Drivers - Tightening Global Emission Standards

Regulators are tightening limits on NOx, particulate matter (PM), hydrocarbons, and CO, directly increasing the complexity and value of exhaust and aftertreatment systems. The European Union’s Euro 7 standard, agreed in 2024, cuts NOx limits for heavy-duty engines by around 50–56% versus Euro VI and reduces PM limits by approximately 20%, while also introducing durability and on-board monitoring requirements. In June 2024 the U.S. EPA announced new light-duty standards that target a 50% reduction in NOx and 40% reduction in PM emissions from 2025. China’s move from China VI to planned China VII and India’s prospective BS VII will further tighten requirements. These policies force OEMs to adopt more advanced exhaust manifolds, catalysts, particulate filters, and sensors, sustaining demand for integrated exhaust systems despite long-term electrification trends.

Technological Advancements in Aftertreatment and Lightweight Materials

The push to meet stricter limits at lower back-pressure and cost is driving innovation across catalysts, filters, manifolds, and thermal management. Industry analyses highlight selective catalytic reduction (SCR), gasoline particulate filters (GPF), lean NOx traps (LNT), and advanced exhaust gas recirculation (EGR) as key growth technologies. In January 2024, Tenneco announced an integrated thermal management system designed to maintain optimal exhaust temperatures in hybrid and conventional vehicles, improving catalyst light-off and emission control under low-load conditions. In February 2024, Faurecia (FORVIA) unveiled a lightweight exhaust manifold using high-strength aluminum alloy to reduce system mass while preserving durability. These innovations support OEM targets for fuel economy and CO2 reduction and enable compliance with durability and real-driving emissions (RDE) provisions in Euro 7 and comparable standards.

Restraints - Electrification and Declining ICE Share in Light-Duty Passenger Cars

Growing BEV and plug-in hybrid penetration, especially in Europe, China, and parts of North America, structurally reduces the addressable market for conventional exhaust systems in light-duty passenger cars. Several long-range forecasts project BEVs to account for a substantial share of new car sales by 2030–2035, which will gradually erode exhaust volumes in those segments. While commercial and emerging markets mitigate this impact in the medium term, suppliers must manage overcapacity risk and rationalize ICE-focused production footprints.

Rising Catalyst Material Costs and Supply Chain Volatility

Exhaust aftertreatment systems rely on precious metals such as platinum, palladium, and rhodium, whose prices are volatile and sensitive to geopolitical and mining supply dynamics. Elevated or unstable prices increase system cost and pressure margins for both OEMs and tier-1 suppliers. At the same time, the broader automotive supply chain faces semiconductor constraints and fluctuating steel and alloy prices, which can disrupt production and raise working capital needs. These structural cost and supply risks constrain the ability of some OEMs and suppliers to invest aggressively in next-generation exhaust technologies, particularly in lower-margin vehicle segments and price-sensitive emerging markets.

Opportunities - Aftermarket and Replacement Demand in Legacy ICE Fleets

Despite electrification, the global vehicle parc will retain hundreds of millions of ICE vehicles for decades, particularly in developing regions and in heavy-duty fleets. This creates a durable opportunity in replacement exhaust components, catalysts, mufflers, and pipes for maintenance, emissions compliance, and performance upgrades. Market studies suggest that the overall exhaust system sector could reach US$ 60–80 Bn by 2030, with a significant share linked to aftermarket and service parts. Suppliers with strong distribution networks, flexible manufacturing, and region-specific portfolios can capture recurring revenue, especially as emissions testing and inspection regimes tighten and aging fleets require more frequent exhaust system replacement.

Advanced Systems for Hybrid Powertrains and Low-Emission Diesel

Hybrid powertrains and next-generation diesel engines require more sophisticated thermal management and aftertreatment architectures to remain compliant under RDE and on-board monitoring (OBM) requirements. Tenneco’s 2024 integrated thermal management solution is an example of emerging systems designed to maintain catalyst activity during low-load hybrid operation. There is also continued demand for SCR-DPF combinations, advanced DOCs, and low-temperature NOx control in long-haul trucks and off-highway applications, where diesel remains hard to replace. This niche potentially representing billions of dollars annually in high-value exhaust content offers margin-accretive growth for suppliers that can provide integrated, modular systems optimized for lifecycle CO2 and pollutant emissions.

Category-wise Analysis

Fuel Type Insights

Gasoline engines dominate the exhaust systems market with roughly 83.2% share, reflecting their prevalence in global passenger car production. Gasoline exhaust systems rely heavily on three-way catalysts and increasingly on gasoline particulate filters (GPFs) to meet strict Euro 6/7 and China VI/VII particulate and cold-start emission limits. Although gasoline engines naturally produce lower NOx, tightening regulations have increased system complexity and value.

Diesel holds a smaller share but remains a higher-value, technology-intensive segment, especially in commercial and heavy-duty vehicles. Growth is supported by diesel’s efficiency and torque advantages in long-haul applications. Diesel exhaust systems incorporating DOC, DPF, SCR, and ammonia slip catalysts carry significantly higher content, making the segment resilient even as light-duty diesel volumes stabilize or decline.

Product Type Insights

The exhaust manifold is the largest component category, accounting for about 38.8% of market revenues in 2026. Manifolds channel exhaust gases from engine cylinders, manage high thermal loads, and support rapid catalyst light-off. With OEMs adopting engine downsizing, turbocharging, and close-coupled catalysts, manifold design has grown more complex, driving greater use of stainless steel and high-temperature alloys. This keeps manifold value closely tied to ICE production while allowing material upgrades to boost unit pricing.

Mufflers are the fastest-growing segment, expected to record about 8.6% CAGR. Increasing noise regulations, rising SUV and pickup demand, and consumer expectations for quieter cabins are driving more advanced muffler designs, including active valves and tuned resonators, supporting sustained growth.

Vehicle Type Insights

Passenger cars hold the largest share of the exhaust systems market at around 65.4%, driven by high global production volumes and stringent emission standards in regions such as Europe, China, and North America. Their exhaust systems including manifolds, pipes, mufflers, and catalytic converters constitute a significant portion of overall market revenue. Despite growing BEV adoption, the large global ICE passenger car fleet continues to sustain strong demand.

Light commercial vehicles (LCVs) represent the fastest-growing segment, supported by expanding e-commerce, last-mile delivery, and urban logistics. Most LCVs still rely on gasoline and diesel engines, often requiring advanced aftertreatment systems like SCR and DPF. This increases exhaust system value per vehicle, enabling LCVs to outpace passenger cars in value growth.

Regional Market Insights

North America Automotive Exhaust Systems Market Share and Trends

North America represents a significant share of global exhaust system revenues, with U.S. sales of about US$ 5.63 Bn in 2026 and a projected US$ 8.51 Bn by 2033, equating to ~11.6% of global market value. The region’s market is driven by high per-capita vehicle ownership, strong pickup and SUV demand, and robust LCV and HCV fleets. New EPA emission standards for light-duty vehicles from 2025 will cut NOx by 50% and PM by 40%, requiring more advanced catalysts, GPF/DPF, and tighter thermal and sensor control.

The U.S. regulatory framework combines federal EPA rules with California Air Resources Board (CARB) and other state programs, creating a demanding environment for exhaust and aftertreatment design. Heavy-duty rulemakings and greenhouse gas (GHG) standards for trucks further reinforce the need for high-performance diesel exhaust solutions.

Europe Automotive Exhaust Systems Market Share and Trends

Europe is both a major production hub and a regulatory bellwether for automotive exhaust systems. European emission standards (Euro 6 and now Euro 7) set stringent type-approval, durability, and RDE requirements that strongly influence global exhaust designs. Euro 7 introduces lower NOx and PM limits, extends durability requirements, and mandates more robust on-board monitoring, with heavy-duty NOx limits reduced by over 50% versus Euro VI and CO limits by around 62% on the WHTC test cycle.

Germany, the U.K., France, and Spain are key markets. Germany hosts major OEMs (Volkswagen Group, BMW, Mercedes-Benz, Stellantis operations) and several leading exhaust suppliers (Eberspächer, Friedrich Boysen, Continental, Benteler), creating a dense innovation ecosystem. The U.K. is implementing its own post-Brexit regulations and preparing for Euro 7-aligned rules, influencing local exhaust system requirements.

Asia Pacific Automotive Exhaust Systems Market Share and Trends

Asia-Pacific is the largest and one of the fastest-growing regional markets, accounting for about 40% of global automotive exhaust system revenues in 2022. High vehicle production in China, Japan, India, South Korea, and ASEAN underpins this dominance. Emission regulations such as China VI (and planned China VII) and India’s BS-VI (moving toward BS VII) are closely aligned with Euro 6/7, requiring complex aftertreatment systems including GPF, DPF, SCR, and advanced EGR.

China is central, with large passenger and commercial vehicle volumes and an ongoing transition from older China III/IV vehicles to China VI/VII-compliant fleets, creating both OEM and retrofit opportunities. Japan and South Korea maintain high technical standards and focus on efficiency and durability, favoring advanced exhaust designs for gasoline and diesel powertrains.

Competitive Landscape

The automotive exhaust systems market is moderately concentrated. Valuate data indicates the top five players hold around 35% of global revenues, while Tenneco and Friedrich Boysen together account for roughly 14% share. Major OEM-focused suppliers span Europe, North America, and Asia, with Faurecia/Forvia, Tenneco, Eberspächer, Boysen, Benteler, Futaba, Sejong, Bosal, Sango, Yutaka Giken, Katcon, Dinex, Wanxiang, and others identified as key players. Competition centers on technology, global manufacturing footprint, cost efficiency, and program wins with major automakers, rather than on price alone.

Key Industry Developments:

- In January 2024, Continental AG revealed plans for a new hydraulic hose production plant in Mexico. The proposed investment is approximately USD 90 million, marking one of the company’s significant investments in 2024. This upcoming facility will serve industrial purposes and is poised to enhance Continental’s regional manufacturing capabilities.

- In November 2023, Eberspächer’s facility, spanning over 7,000 square meters, will manufacture exhaust gas after-treatment systems for passenger cars and commercial vehicles intended for Chinese automotive brands. This encompasses hot-end systems comprising catalytic converters, particulate filters, and cold-end components.

Companies Covered in Automotive Exhaust Systems Market

- Faurecia

- Tenneco Inc.

- Eberspächer Group

- Friedrich Boysen GmbH & Co. KG

- Yutaka Giken Co., Ltd.

- Benteler Automotive

- Sejong Industrial Co., Ltd.

- Futaba Industrial Co., Ltd.

- SANGO Co., Ltd.

- Bosal International N.V.

- Others Key Players

Frequently Asked Questions

The Automotive Exhaust Systems market is estimated to be valued at US$ 54.2 Bn in 2026.

The key demand driver for the Automotive Exhaust Systems market is the tightening of global emission and noise regulations.

In 2026, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Automotive Exhaust Systems market.

Among the Vehicle type, Passenger Car holds the highest preference, capturing beyond 65.3% of the market revenue share in 2026, surpassing other Vehicle type.

The key players in Automotive Exhaust Systems are Faurecia, Tenneco Inc., Eberspächer Group and Friedrich Boysen GmbH & Co. KG.