- Automotive Components & Materials

- Lightweight Automotive Materials Market

Lightweight Automotive Materials Market Size, Share, and Growth Forecast 2026 – 2033

Lightweight Automotive Materials Market by Material Type (Metals, Composites, Plastics and Elastomers), Application (Body in White, Chassis and Suspension, Powertrain, Closures, Interiors and Others), End- user (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV)) and Regional Analysis for 2026 – 2033

Lightweight Automotive Materials Market Share and Trends Analysis

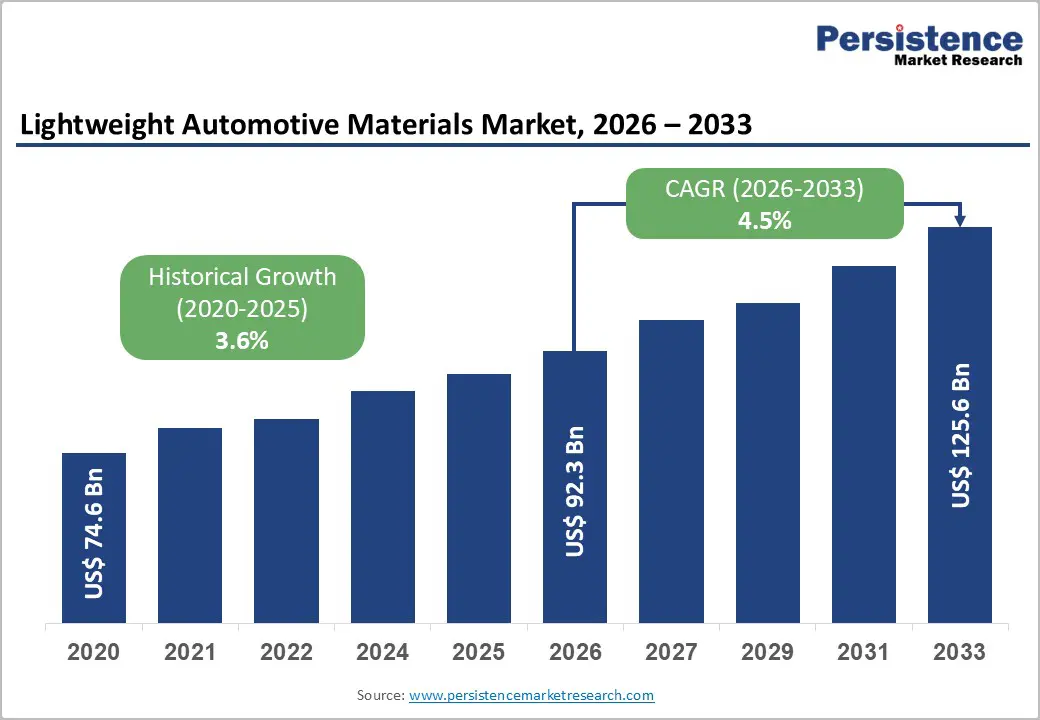

The global lightweight automotive materials market size is likely to be valued at US$ 92.3 billion in 2026 and is projected to reach US$ 125.6 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

The market expansion is driven by three fundamental factors: stringent corporate average fuel economy (CAFE) standards requiring a 50.4 miles per gallon fleet average by 2031, escalating demand for electric vehicle range extension through weight reduction, and widespread adoption of advanced materials, including composites, aluminum alloys, and engineering polymers across body-in-white, chassis, and powertrain systems.

Key Industry Highlights:

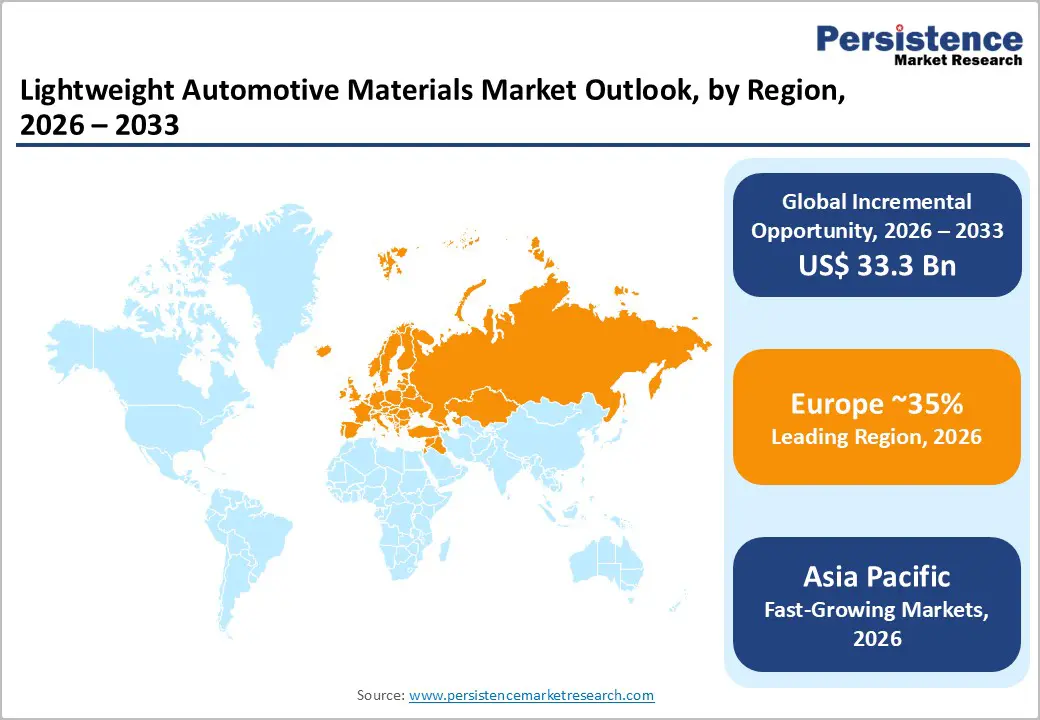

- Leading Region: Europe dominates with 36.52% global market share, driven by stringent EU Energy Efficiency Directive mandating 11.7% consumption reduction by 2030, sophisticated composite manufacturing ecosystems, particularly in Germany, advanced regulatory frameworks establishing 95 grams per kilometer CO2 emissions standards, and comprehensive circular economy initiatives promoting recycled content integration.

- Fastest Growing Region: Asia Pacific represents the fastest-growing region with 4.5% CAGR, driven by accelerating electric vehicle production across China, Japan, South Korea, and India, government electrification mandates, rising vehicle demand from the emerging middle class, and cost-effective lightweight material adoption strategies, including natural fiber composites for mass-market platforms.

- Dominant Segment: Composites dominate with 66% market share, reflecting exceptional stiffness-to-weight ratios, design flexibility, crash energy absorption capabilities, and increasingly favorable economics as manufacturing automation expands, with glass fiber composites representing 92% of automotive composite utilization.

- Fastest Growing Segment: Carbon fiber composites represent the fastest-growing material category, driven by premium vehicle segment expansion, cost reduction through manufacturing automation, expanding EV platform adoption requiring specialized thermal management, and increasing application penetration into mass-market vehicles as production scaling reduces unit costs.

- Key Market Opportunity: Lightweight automotive body panels expansion through advanced manufacturing technologies, including automated fiber placement (AFP) and thermoplastic composite integration, offering substantial weight reduction applicability across vehicle categories, enabling up to 50% weight savings versus steel while supporting right material in right place design optimization strategies.

| Key Insights | Details |

|---|---|

| Lightweight Automotive Materials Market Size (2026E) | US$ 92.3 Bn |

| Market Value Forecast (2033F) | US$ 125.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Dynamics

Drivers

Stringent Regulatory Requirements for Fuel Efficiency and Emissions Reduction

Global regulatory frameworks including Corporate Average Fuel Economy (CAFE) standards, European Union emissions regulations, and China's New Energy Vehicle mandates are compelling automakers to adopt lightweight materials as a primary strategy for meeting increasingly stringent efficiency and emissions targets. The United States National Highway Traffic Safety Administration (NHTSA) finalized new CAFE standards requiring 50.4 miles per gallon fleet average by model year 2031 for passenger cars and 45 miles per gallon for SUVs and pickups, creating powerful economic incentives for material lightweighting. European Union regulations mandate 95 grams per kilometer of carbon dioxide emissions, driving equivalent material specification strategies across European automotive manufacturers. The European Union's Energy Efficiency Directive revision mandates 11.7% energy consumption reduction by 2030, further accelerating lightweight material adoption.

Accelerating Electric Vehicle Production and Battery Weight Mitigation Strategies

Electric vehicle proliferation fundamentally reshapes lightweight material demand as automotive manufacturers recognize that reducing curb weight directly extends driving range and improves overall vehicle efficiency without requiring larger battery packs. Battery pack weight ranging from 450 to 1,000 pounds (approximately 200 to 450 kilograms) represents a substantial portion of total vehicle weight, creating powerful incentives for material substitution throughout remaining vehicle structures. EV-specific composite applications including battery enclosures, thermal management systems, and structural frames are expanding rapidly as manufacturers develop specialized solutions addressing unique electrified powertrain requirements. China, Japan, South Korea, and India have announced ambitious transformation initiatives for public transportation and private vehicle fleets toward electrification, accelerating regional lightweight material adoption.

Restraints

High Production Costs and Scalability Challenges for Advanced Composites

Carbon fiber and advanced composite materials command substantially higher material costs compared to conventional steel and aluminum, with carbon fiber price premiums limiting adoption to premium vehicle segments and specialized applications. Manufacturing complexity associated with composite part production, including automated fiber placement (AFP), resin transfer molding (RTM), and compression molding processes, requires substantial capital equipment investments and specialized workforce development. Mass production scalability remains challenging for advanced composite manufacturing, as current production technologies struggle to match the throughput rates achieved by conventional stamping and forming operations for steel and aluminum. Production cycle times for carbon fiber composite parts frequently exceed those for alternative materials, creating manufacturing scheduling constraints and inventory management complexity.

Uncertainty Regarding Recycling Technologies and Circular Economy Implementation

Advanced composite materials, particularly carbon fiber reinforced plastics (CFRP), present significant recycling challenges compared to conventional metallic materials, with established recycling infrastructure remaining underdeveloped across many regions. End-of-life vehicle (ELV) processing for composite-intensive vehicles requires specialized equipment and technical expertise currently available in limited locations, creating geographic constraints on sustainable material recovery. Regulatory uncertainty regarding composite waste classification, hazardous material restrictions, and landfill disposal regulations creates compliance complexity for automotive manufacturers and material suppliers. Consumer and regulatory skepticism regarding composite recycling effectiveness and environmental benefits creates hesitancy regarding large-scale adoption commitments. Supply chain fragmentation for recycled composite materials prevents establishment of economically viable closed-loop recycling systems comparable to those available for aluminum and steel.

Opportunities

Lightweight Automotive Body Panels Market Expansion Through Advanced Manufacturing

Lightweight automotive body panels represent an exceptional growth opportunity as automakers seek cost-effective weight reduction solutions applicable across broad vehicle categories without requiring fundamental architecture redesign. Advanced manufacturing technologies including automated fiber placement (AFP), injection molding for plastic components, and hybrid molding processes combining fiber reinforcement with injection molding enable production cost reduction while maintaining superior mechanical properties. Thermoplastic composites (TPC) demonstrate promise, enabling rapid manufacturing cycles and enabling integration of complex geometries that would be impractical using traditional thermoset composite processes. Glass fiber composites, representing 92% of automotive composite utilization, provide cost-effective lightweighting suitable for mass-market vehicle segments where carbon fiber economics remain prohibitive.

Specialized Applications in Electric Powertrain Thermal Management and Battery Enclosures

Electric vehicle proliferation creates entirely novel composite material application categories requiring specialized thermal management, electrical insulation, and mechanical protection capabilities unavailable from conventional materials. Battery thermal management systems incorporating advanced polymers and composite materials address critical heat dissipation requirements, as battery thermal conductivity optimization directly impacts driving range and overall vehicle efficiency. Autoneum's advanced thermal management materials demonstrate thermal conductivity around 0.3 watts per meter-kelvin, substantially lower than aluminum's 200 watts per meter-kelvin, enabling superior thermal insulation properties critical for cold-weather performance and efficiency optimization. Electric motor housing protection and power electronics enclosure applications require combinations of thermal conductivity, electrical insulation, and mechanical robustness achievable through specialized composite architectures. High-voltage cable routing and battery pack integration demand materials offering superior electrical insulation properties unavailable from traditional metallic alternatives.

Category-wise Analysis

Materials Deployment Insights

Composites dominate the lightweight automotive materials market with approximately 66% market share in 2026, reflecting overwhelming preference for composite materials across structural, semi-structural, and non-structural applications. Composite materials offer exceptional stiffness-to-weight ratios, design flexibility enabling complex geometry integration, superior crash energy absorption, and increasingly favorable cost positioning as manufacturing technology matures. Thermoplastic composites (TPC) demonstrate particularly strong growth momentum due to exceptional manufacturing cycle time advantages enabling rapid production rates compatible with high-volume automotive production. Natural fiber composites incorporating agricultural waste products exhibit emerging market presence particularly in Asia Pacific regions, where sustainability benefits and cost advantages align with regional priorities.

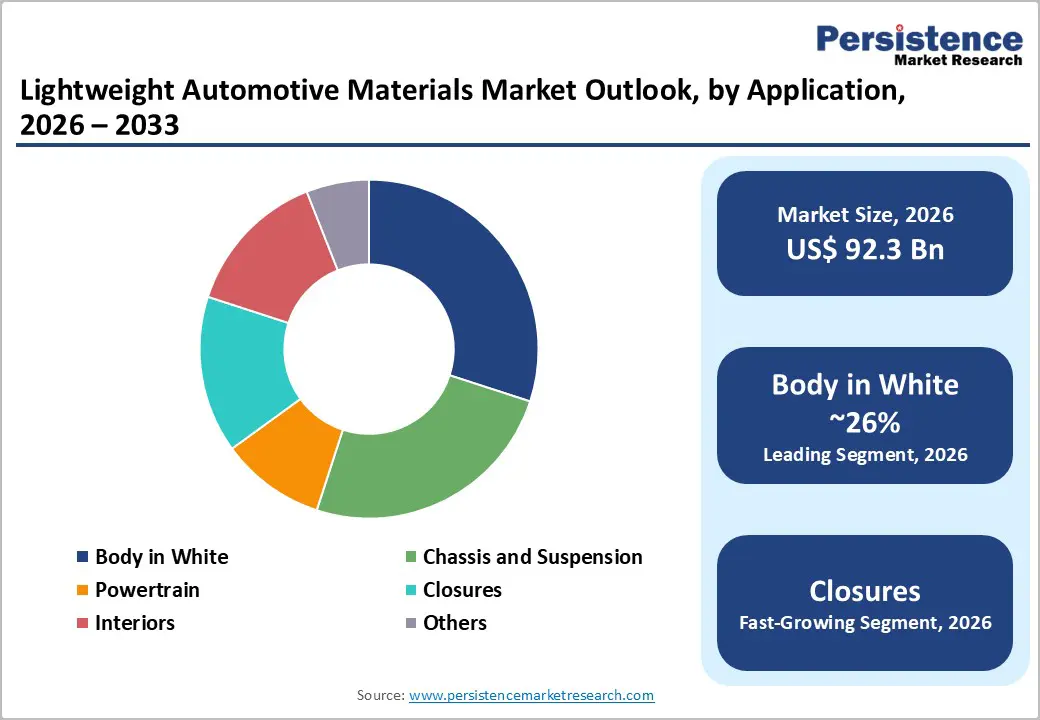

Application Insights

Body-in-White (BiW) represents the largest application segment with approximately 26% market share in 2026, as automotive manufacturers prioritize structural weight reduction through material substitution within vehicle primary load-bearing structures. BiW applications including side rails, roof panels, floor structures, and pillar reinforcements offer substantial weight reduction opportunities while maintaining structural integrity and crash performance requirements. Composites and advanced high-strength steels (AHSS) enable designers to implement "right material in right place" strategies, optimizing material specifications for specific structural requirements including stiffness, crash performance, and thermal characteristics. Chassis and suspension components including control arms, cross members, and suspension brackets represent secondary growth segments, with composite adoption enabling 10% weight reduction relative to conventional aluminum or cast-iron components. Powertrain applications including engine covers, transmission housings, and thermal management systems demonstrate emerging composite integration, driven by EV-specific thermal management requirements and electrification-induced architecture changes.

End-user Insights

Passenger cars represent the largest end-user segment with approximately 83% market share in 2026, reflecting universal automotive application of lightweight materials across consumer vehicle categories. Passenger vehicle platforms ranging from economy through luxury segments increasingly incorporate lightweight materials, driven by regulatory compliance requirements, consumer demand for fuel efficiency and performance, and manufacturer emphasis on vehicle dynamics optimization. Light commercial vehicles (LCV) including pickup trucks and vans represent the fastest-growing segment with 3.3% CAGR, driven by expanding electric vehicle platform development and corresponding weight management requirements for range optimization.

Regional Insights

North America Lightweight Automotive Materials Trends

North America maintains market leadership with approximately 25-28% global market share, supported by advanced regulatory frameworks including CAFE standards requiring 50.4 miles per gallon by model year 2031, sophisticated supplier ecosystems, and substantial R&D investments. The United States dominates regional markets through technology innovation leadership across carbon fiber manufacturing, advanced high-strength steel development, and composite processing automation. New CAFE standards finalized in June 2024 establish powerful economic incentives for lightweight material adoption, with regulatory penalties making material substitution economically optimal relative to alternative compliance strategies.

Premium automotive brands including BMW, Mercedes-Benz, and Porsche continue pioneering advanced material applications across luxury vehicle segments, with carbon fiber integration demonstrating 200+ kilogram weight reduction through structural redesign. Research and development investment concentration in Silicon Valley, Detroit, and Ohio continues advancing manufacturing technology including automated fiber placement enabling production cost reduction and cycle time optimization.

Europe Lightweight Automotive Materials Trends

Europe dominated the global lightweight automotive materials market with 36.52% market share in 2024, driven by the European Union's stringent energy policy directives, aggressive renewable energy integration targets, and aggressive carbon emission reduction mandates. German automotive manufacturers including BMW, Mercedes-Benz, Audi, and Porsche lead composite material integration globally, with carbon fiber adoption rates substantially exceeding global averages. The European Union's Energy Efficiency Directive mandates 11.7% energy consumption reduction by 2030, compelling comprehensive vehicle redesign around lightweight material platforms.

Sustainability and circular economic emphasis drive regional composite recycling technology development, with Novelis' breakthrough 100% recycled automotive aluminum coil and emerging carbon fiber recycling technologies demonstrating technology pathway maturity. Manufacturing innovation concentration in Germany continues advancing production technologies including automated fiber placement (AFP) and resin transfer molding (RTM), with Röchling Automotive and Envalior demonstrating thermoplastic composite integration for complex structural applications. European automotive supplier ecosystem remains globally competitive through sustained material science innovation and manufacturing technology leadership.

Asia Pacific Lightweight Automotive Materials Trends

Asia Pacific represents the fastest-growing region with projected 4.5-6% regional CAGR through 2033, driven by rapid electric vehicle production acceleration, government electrification mandates, and rising middle-class vehicle demand. China dominates regional markets through massive electric vehicle manufacturing investment, with companies including BYD, NIO, and Li Auto implementing aggressive lightweight material strategies for range optimization. China's first mass-produced carbon fiber vehicle, Yangwang U9 supercar, incorporates 110+ kilograms of aerospace-grade T700 12K carbon fiber, achieving 30% weight reduction versus traditional steel-aluminum structures.

India's automotive manufacturing expansion and rising commercial vehicle demand create opportunities for cost-effective lightweight material integration, particularly through natural fiber composites offering superior price-performance positioning. Japan and South Korea continue leading advanced composite development, with manufacturers integrating composites across structural frames, dashboards, and safety reinforcements for next-generation hybrid and compact electric vehicles. ASEAN emerging economies demonstrate rapid automotive production growth and increasing lightweight material adoption as manufacturers pursue global export competitiveness.

Competitive Landscape

The global lightweight automotive materials market exhibits moderate consolidation with dominant positions held by major chemical companies and specialized material suppliers. BASF, Toray Industries, LyondellBasell, and Solvay control substantial market shares through comprehensive material portfolios spanning composites, advanced polymers, and specialty chemicals. Novelis Inc. and Alcoa Corporation command substantial aluminum market share through vertically integrated production and recycling capabilities, while ArcelorMittal and POSCO dominate advanced high-strength steel segments.

Stratasys Ltd. and Owens Corning focus on specialized composite materials and manufacturing technologies respectively. Company strategies emphasize circular economy integration through recycling technology development, AI-driven material design optimization, and strategic partnerships with automotive OEMs for co-development of lightweight material solutions.

Key Market Developments

- In November 2025, Owens Corning Advanced Composites Launch - Owens Corning launched new glass fiber composite materials specifically engineered for automotive applications, delivering improved durability, enhanced lightweighting capabilities, and superior sustainability characteristics, reinforcing the company's market leadership in advanced composites for mobility solutions.

- In September 2025, Solvay Thermoplastic Composites Showcase - Solvay S.A. unveiled innovative thermoplastic composites engineered for EV battery enclosures and structural components, emphasizing lightweight performance, durability optimization, and sustainability integration, thereby reinforcing Solvay's technological leadership in advanced automotive composites.

Companies Covered in Lightweight Automotive Materials Market

- BASF

- Toray Industries, Inc.

- LyondellBasell

- Novelis Inc

- ArcelorMittal

- Alcoa Corporation

- Owens Corning

- Stratasys Ltd.

- Tata Steel

- POSCO

- Other Key Players

Frequently Asked Questions

The global Lightweight Automotive Materials Market is projected to reach US$ 125.6 Bn by 2033 from US$ 92.3 Bn in 2026, representing a CAGR of 4.5% during the forecast period.

Primary demand drivers include regulatory compliance requirements including CAFE standards and EU emissions mandates, electric vehicle proliferation creating battery weight management requirements, oil price volatility incentivizing fuel efficiency improvements, advanced manufacturing technology development, reducing composite production costs, and circular economy integration.

Composites dominate with 66% market share in 2026, with glass fiber reinforced plastics representing 92% of automotive composite utilization, while carbon fiber composites represent the fastest-growing category, achieving 30% weight savings versus aluminum and 70% reduction versus traditional steel while offering exceptional design flexibility and impact resistance.

Europe leads with 36.52% global market share driven by stringent EU Energy Efficiency Directive mandating 11.7% consumption reduction by 2030, advanced 95 grams per kilometer CO₂ emissions standards, sophisticated German manufacturing ecosystems, and comprehensive circular economy initiatives promoting recycled content integration.

Market leaders include BASF, Toray Industries, LyondellBasell, Novelis Inc., ArcelorMittal, Alcoa Corporation, Solvay S.A. and POSCO.