- Automotive Components & Materials

- Automotive Energy Recovery Systems Market

Automotive Energy Recovery Systems Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Automotive Energy Recovery Systems Market by Subsystem Type (Regenerative Braking System, Turbocharger, and Exhaust Gas Recirculation), Vehicle Type (Passenger Cars, Commercial Vehicles, and Electric Vehicles), and Regional Analysis for 2026 - 2033

Automotive Energy Recovery Systems Market Size and Trends Analysis

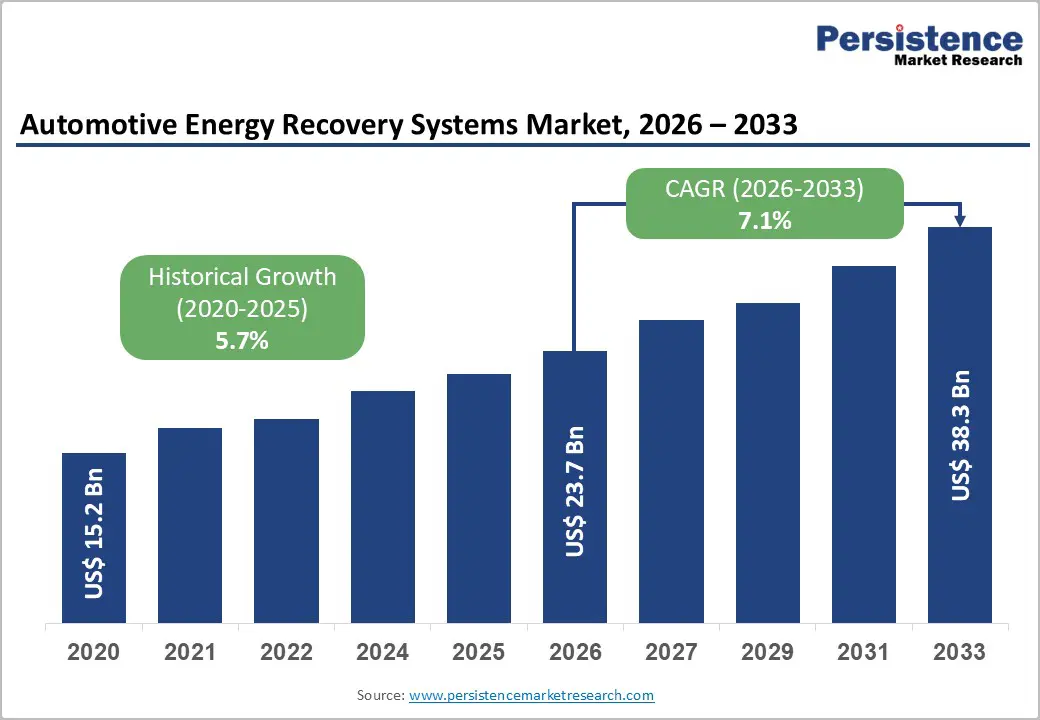

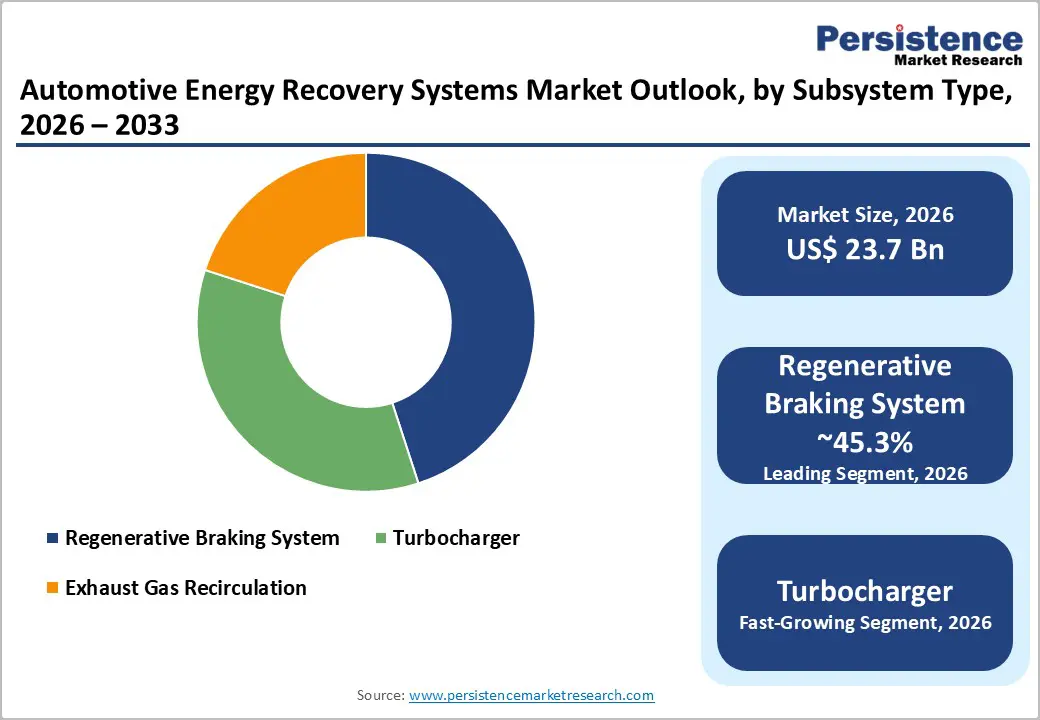

The global Automotive Energy Recovery Systems Market size is likely to be valued at US$ 23.7 billion in 2026 and is projected to reach US$ 38.3 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033. The market is driven by stringent fuel economy standards across developed economies, increasing consumer demand for fuel-efficient vehicles, and the paradigm shift toward hybrid and electric vehicle platforms requiring advanced energy recovery capabilities.

Key Industry Highlights:

- Leading Subsystem Type: Regenerative Braking Systems dominate with 45.3% market share through electric and hybrid vehicle proliferation and proven fuel economy benefits, while Turbocharger-based energy recovery represents the fastest-growing segment at 8.4% CAGR, driven by conventional powerplant efficiency mandates through 2030-2035 transition periods.

- Leading Vehicle Application: Passenger cars establish 61.4% market share through OEM adoption acceleration and consumer demand for fuel efficiency; Electric Vehicles represent the fastest-growing segment at 15% CAGR, driven by 15-20% annual EV production growth and 500+ km range requirements necessitating regenerative braking integration.

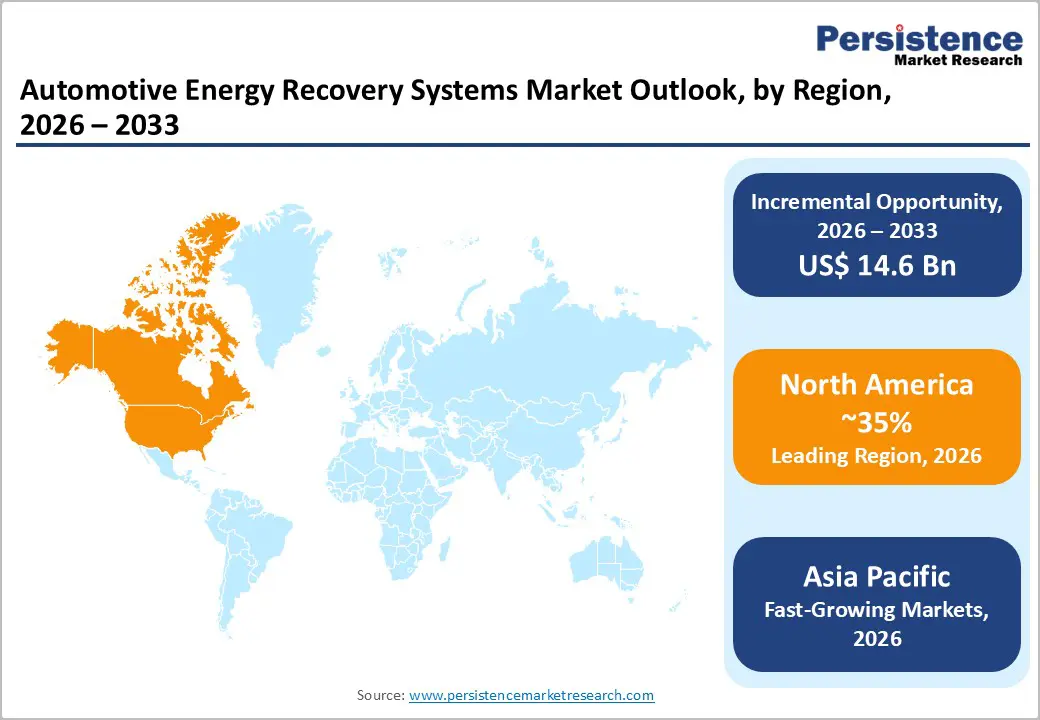

- Regional Market Leadership: North America maintains 35% global market share driven by CAFE standards escalation and federal electrification investment; Europe commands 25% share with EU CO2 emission reduction mandates; Asia Pacific demonstrates fastest regional growth at 11% CAGR, expanding from 28% current share to 35% by 2033.

- Emerging Technology Opportunity: Vehicle-to-grid integration establishing US$ 2-3 billion market opportunity by 2033 through bidirectional energy flow, enabling energy trading and demand response participation; V2G-capable vehicles are projected to reach 5.8% of the total EV fleet, creating new revenue models for vehicle owners and grid operators.

- Supplier Consolidation: Top 8 suppliers control 58% global share, with Bosch, ZF Friedrichshafen, Continental, and Valeo maintaining technology and relationship dominance; emerging competitors and Chinese manufacturers establishing competitive positioning through vertical integration and cost structure advantages.

- Technology Convergence: Electrically assisted turbochargers achieving 28% energy recovery efficiency, addressing conventional powertrain fuel economy requirements; artificial intelligence-driven energy management systems enabling predictive optimization; battery chemistry advancement supporting 50%+ regenerative efficiency improvements.

| Key Insights | Details |

|---|---|

|

Automotive Energy Recovery Systems Market Size (2026E) |

US$ 23.7 Bn |

|

Market Value Forecast (2033F) |

US$ 38.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.1% |

|

Historical Market Growth (CAGR 2020 to 2024) |

5.7% |

Market Dynamics

Drivers - Advancements in Energy Storage Technologies

The automotive energy recovery systems market is experiencing accelerated growth due to continuous advancements in energy storage technologies. As battery technologies evolve, the ability to efficiently capture, store, and release energy in vehicles improves, enhancing the overall effectiveness of ERS.

Advanced energy storage systems, such as high-capacity batteries and supercapacitors, enable more efficient energy recuperation during braking and acceleration. This progress not only extends the range of electric and hybrid vehicles but also fosters the widespread adoption of energy recovery systems across various automotive segments. The symbiotic relationship between energy storage advancements and the ERS market drives innovation, making these systems more robust, cost-effective, and appealing to both manufacturers and consumers.

In addition, the global automotive industry's heightened focus on sustainability, coupled with stringent environmental regulations, acts as a powerful driver for the Automotive Energy Recovery Systems market. Governments worldwide are implementing policies to reduce carbon emissions and promote eco-friendly transportation. ERS plays a pivotal role in achieving these goals by minimizing energy waste and enhancing fuel efficiency.

Automakers are compelled to incorporate energy recovery systems into their vehicles to comply with regulations, foster a greener image, and meet the growing consumer demand for environmentally conscious transportation. As sustainability becomes a key differentiator, the integration of ERS aligns with industry trends, creating a synergistic relationship between regulatory compliance, consumer preferences, and the accelerated growth of the Automotive Energy Recovery Systems market.

Restraints - Prevalent Supply Chain Disruptions

The automotive energy recovery systems (ERS) market may face challenges due to supply chain disruptions, impacting the availability and production of essential components. The global supply chain for automotive technologies is intricate, involving numerous suppliers for key elements like batteries, capacitors, and electronic components. Any disruptions, whether caused by geopolitical tensions, natural disasters, or unforeseen events, can lead to shortages and increased costs.

Such disruptions can hinder the seamless production of ERS-equipped vehicles, affecting market performance. To mitigate these risks, industry stakeholders need robust contingency plans, diversified sourcing strategies, and collaborative efforts to enhance the resilience of the supply chain, ensuring a more stable and reliable market performance for Automotive Energy Recovery Systems.

Integration Complexity and Standardization Challenges

The significant challenge facing the automotive energy recovery systems (ERS) market is the complexity of integrating these systems seamlessly into diverse vehicle architectures. Standardization across the industry is essential for widespread adoption, yet the lack of uniformity in ERS technologies and specifications poses integration challenges for automotive manufacturers. Varied vehicle designs, powertrain configurations, and the absence of standardized interfaces can impede interoperability.

Achieving consensus on common standards is crucial to overcoming integration complexities, ensuring compatibility, and facilitating the widespread adoption of ERS across different vehicle models. Industry collaboration and regulatory initiatives are pivotal in addressing this challenge and promoting a more streamlined and interoperable ERS landscape.

Opportunity - Growing Integration of ERS in Autonomous Vehicles

The evolving landscape of autonomous vehicles presents a significant revenue opportunity for the automotive ERS market. As the automotive industry moves towards autonomy, vehicles equipped with advanced driver assistance systems (ADAS) and full autonomy can benefit from ERS to optimize energy usage. The constant acceleration and deceleration patterns in autonomous driving scenarios provide ample opportunities for energy recovery during braking and acceleration.

Integrating ERS into autonomous vehicle designs not only enhances overall energy efficiency but also aligns with the sustainability goals of future transportation. This symbiotic relationship between autonomous technology and ERS presents a strategic avenue for market players to capitalize on the growing demand for energy-efficient solutions in the evolving automotive landscape.

Moreover, collaborations between the automotive sector and other industries present another lucrative opportunity for revenue growth in the automotive energy recovery systems market. Partnering with energy storage companies, technology firms, and infrastructure developers can lead to innovative solutions and expanded applications for ERS. For example, collaborations with smart grid initiatives can enable the bidirectional flow of energy between vehicles and the power grid, creating new revenue streams through vehicle-to-grid (V2G) systems.

Similarly, partnerships with renewable energy providers can explore synergies between ERS and sustainable energy sources, further enhancing the market's appeal. These cross-industry collaborations foster innovation, diversify revenue streams, and position ERS as a key player in the broader ecosystem of sustainable and intelligent transportation solutions.

Category-wise Analysis

Subsystem Type Insights

Within the AERS market, the regenerative braking system (RBS) emerges as the dominant category, particularly owing to its widespread adoption in electric vehicles (EVs). The RBS efficiently captures and stores energy during deceleration, aligning seamlessly with the growing emphasis on electrification. Its integral role in enhancing EV range and efficiency solidifies its dominance.

Simultaneously, the fastest-growing category is the turbocharger subsystem, driven by the surge in hybrid powertrains. Turbochargers play a pivotal role in optimizing internal combustion engine efficiency, meeting the demands of hybrid powertrains for higher power outputs without compromising fuel economy.

Vehicle Type Insights

Electric vehicles (EVs) emerge as the dominant category. The inherent integration of energy recovery systems is a defining attribute, positioning EVs at the forefront of energy efficiency in automotive transportation. As the automotive industry undergoes a paradigm shift towards electrification, EVs seamlessly incorporate advanced energy recovery technologies, such as regenerative braking systems, contributing significantly to their overall efficiency and sustainability.

The fastest-growing category encompasses commercial vehicles, driven by increasing efforts to enhance fuel efficiency and reduce emissions in the commercial transportation sector, fostering a demand surge for energy recovery systems in this vehicle segment.

Regional Analysis

North America Automotive Energy Recovery Systems Market Analysis

North America commands approximately 35% of the global automotive energy recovery systems market share, valued at approximately US$ 7.6 billion in 2026 with projections approaching US$ 12 billion by 2033. The United States represents the dominant regional market contributor, accounting for 85% of the North American market value, driven by CAFE standards, state-level EV mandates, and federal electrification investment.

The North American market reflects technology leadership dominance by established powertrain suppliers, including Bosch, ZF Friedrichshafen, and Continental. Traditional OEM suppliers, including Dana Incorporated and Linamar Corporation, demonstrate variable transition velocity toward energy recovery system integration.

Europe Automotive Energy Recovery Systems Market Analysis

Europe represents approximately 25% of the global automotive energy recovery systems market share, valued at approximately US$ 6.6 billion in 2026. Germany, United Kingdom, France, and Spain collectively represent 78% of European market value, reflecting manufacturing concentration and regulatory framework implementation.

European Union CO2 emission reduction mandates, targeting 55.4 grams CO2/km fleet average by 2025, represent the primary market driver establishing binding energy recovery system integration requirements. Hybrid vehicle adoption in Europe, with HEV and PHEV sales reaching 2.5+ million units annually, creates substantial regenerative braking system demand. Third, government infrastructure investment, including EU Connecting Europe Facility allocating €100+ billion for transportation electrification through 2030, establishes sustained technology development support.

Asia Pacific Automotive Energy Recovery Systems Market Analysis

Asia Pacific dominates the global automotive energy recovery systems market expansion, commanding approximately 22% market share with projections increasing to 30% by 2033. The region valued at approximately US$ 6.6 billion in 2026 is anticipated to reach US$ 14 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 11% during the forecast period.

Chinese government new-energy vehicle targets establish binding vehicle transition timelines. Indian government EV promotion initiatives provide production-linked incentives supporting domestic supply chain development. Japanese regulatory framework emphasizes hybrid vehicle advancement and hydrogen fuel cell integration.

Regional investment concentrates on EV and hybrid platform scaling, with Chinese manufacturers allocating US$ 100-150 billion through 2030 for electrification. Manufacturing capacity expansion in India, Vietnam, and Indonesia reduces system costs, supporting emerging market penetration and TAM expansion.

Competitive Landscape

Competitive intelligence in the automotive energy recovery systems market involves systematic gathering and analysis of information about key market players, their strategies, strengths, weaknesses, and market dynamics. Prominent organizations, including BorgWarner Inc, Robert Bosch GmbH, Hyundai Motors Group, Mitsubishi Electric Corporation, Cummins Inc, are at the vanguard of this sector. Understanding competitors' product offerings, market share, technological advancements, and customer preferences is crucial for staying ahead.

Continuous monitoring of industry trends, regulatory changes, and emerging technologies provides valuable insights for strategic decision-making. By comprehensively assessing the competitive landscape, companies in the automotive ERS market can identify opportunities, anticipate challenges, and position themselves strategically for sustainable growth.

Key Industry Developments:

- In September 2024, BorgWarner launched its largest passenger car twin turbochargers for the General Motors Corvette ZR1, designed to power its 5.5-liter V8 engine, delivering 1,064 horsepower and 828 lb-ft of torque. The turbochargers feature a patented decoupled ball bearing system, offering faster response time, improved durability, and reduced noise. BorgWarner’s reputation with the NTT INDYCAR SERIES contributed to its selection for this project.

- In January 2024, Cummins Turbo Technologies (CTT) launched the 8th generation Holset Series 400 Variable Geometry Turbocharger (HE400VGT), following the success of the 7th generation. This new turbocharger is engineered for the 10-15L heavy-duty truck market, offering a 5% efficiency improvement over its predecessor. It features advancements such as a new bearing system, tighter clearances, and enhanced transient response.

Companies Covered in Automotive Energy Recovery Systems Market

- BorgWarner Inc.

- Continental AG

- Robert Bosch GmbH

- Tenneco Inc.

- Rheinmetall Automotive AG

- Hyundai Motor Group

- Cummins Inc.

- Mitsubishi Electric Corporation

- GARRETT MOTION INC.

- Enersgy Recovery

- Others Key Players

Frequently Asked Questions

The Automotive Energy Recovery Systems market is estimated to be valued at US$ 23.7 billion in 2026.

The key demand driver for the Automotive Energy Recovery Systems market is the global push for improved fuel efficiency and reduced vehicle emissions.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Automotive Energy Recovery Systems market.

Among the Regenerative Braking System, Healthcare holds the highest preference, capturing beyond 45.3% of the market revenue share in 2026, surpassing other Subsystem Type.

The key players in Automotive Energy Recovery Systems are BorgWarner Inc., Continental AG, Robert Bosch GmbH, and Tenneco Inc.