- Electric Mobility

- Europe Vehicle Electrification Market

Europe Vehicle Electrification Market Size, Share, and Growth Forecast 2026 - 2033

Europe Vehicle Electrification Market by Product Type (Start/Stop System, Battery Packs, Traction Inverters, Integrated Starter Generator, Onboard Chargers, Other), Propulsion Type (Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Full Hybrid Electric Vehicle (HEV), Fuel Cell Electric Vehicle (FCEV), Other), and Regional Analysis for 2026 - 2033

Europe Vehicle Electrification Market Size and Trend Analysis

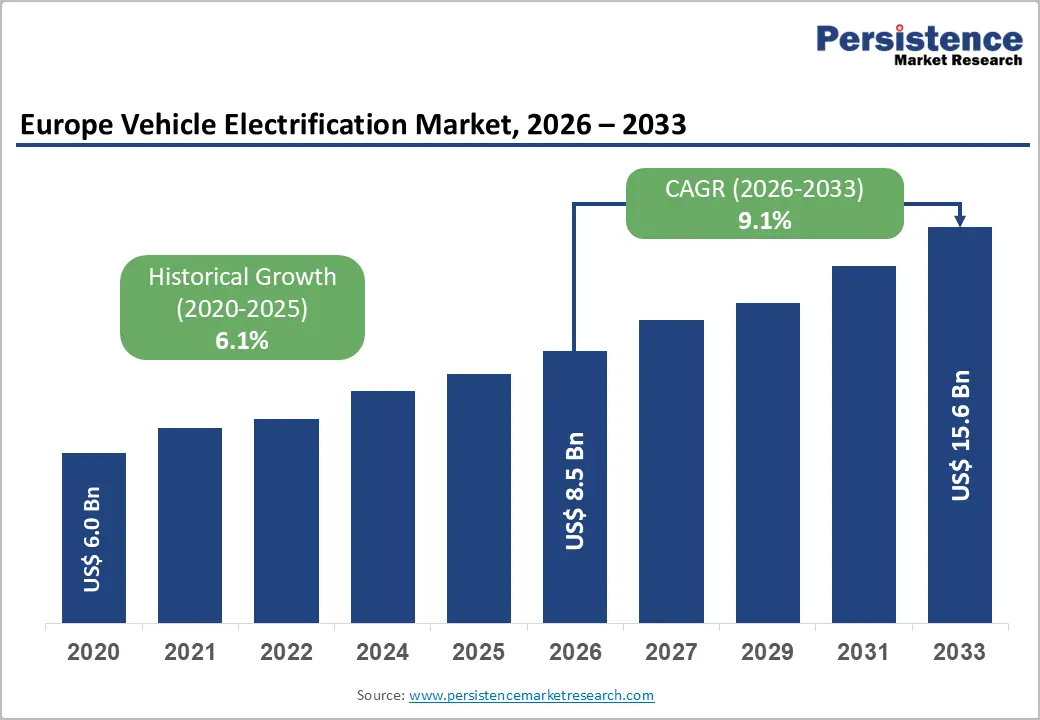

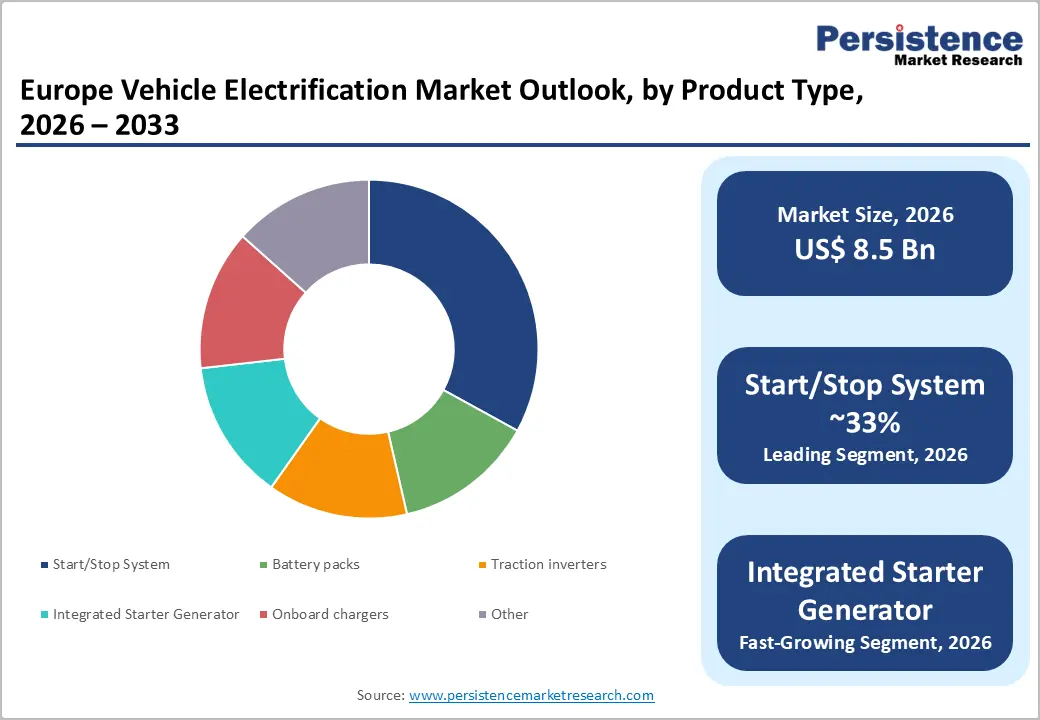

The European Vehicle Electrification Market is valued at US$ 8.5 billion in 2026 and is projected to reach US$15.6 billion by 2033, growing at a CAGR of 9.1% between 2026 and 2033.

This robust growth trajectory is underpinned by the European Union’s binding regulatory architecture, notably Regulation (EU) 2019/631, which mandates a 55% fleet-wide CO2 reduction from new passenger cars by 2030 and a 100% reduction by 2035, compelling every major original equipment manufacturer (OEM) to accelerate electrification investment. Complementing regulation, rapid advances in battery technology, and proliferating charging infrastructure, Europe recorded nearly 1.14 million public charging points by the end of 2025, more than four times the 241,000 available in 2020, and is substantially reducing the total cost of EV ownership and broadening consumer adoption.

Key Highlights:

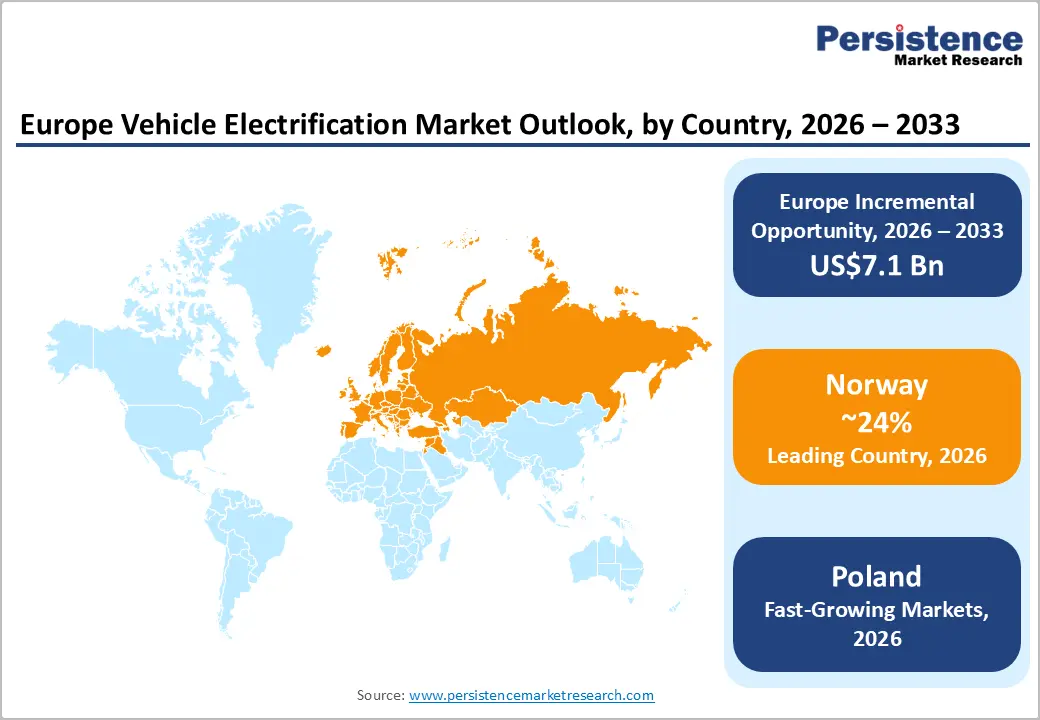

- Leading Country: Norway leads the Europe Vehicle Electrification Market with 24% market share, underpinned by multi-decade policy incentives including VAT exemption, toll waivers, and Europe’s densest public charging infrastructure at 46 charging points per 1,000 vehicles.

- Fastest Growing Country: Poland is the fastest-growing electrification market in Europe, recording +125% BEV registration growth year-to-date through October 2025 (ICCT), driven by EU CO2 compliance requirements, expanding OEM manufacturing investment, and AFIR-funded charging infrastructure deployment.

- Dominant Segment: Start/Stop Systems lead the Product Type category with approximately 33% market share, driven by mandatory integration in new ICE and mild hybrid vehicles under EU Regulation (EU) 2019/631 CO standards, offering the lowest-cost compliance mechanism for mass-market OEMs.

- Fastest Growing Segment: The Integrated Starter Generator (ISG) segment is projected to grow at a CAGR of 18.3% through 2033, driven by widespread OEM adoption of 48V mild hybrid architectures as a cost-effective CO2 compliance strategy across mass-market passenger car and light commercial vehicle platforms.

- Key Market Opportunity: Vehicle-to-Grid (V2G) integration and urban commercial fleet electrification offer significant revenue expansion potential, supported by the EU Battery Regulation mandating standardized BMS communication protocols and by growing city-level low-emission zone policies that drive demand for bidirectional charging systems and advanced battery management technologies.

| Key Insights | Details |

|---|---|

|

Europe Vehicle Electrification Market Size (2026E) |

US$ 8.5 Bn |

|

Market Value Forecast (2033F) |

US$ 15.6 Bn |

|

Projected Growth CAGR (2026–2033) |

9.1% |

|

Historical Market Growth (2020–2025) |

6.1% |

Market Dynamics

Drivers - EU Regulatory Mandates Compelling Industry-wide Electrification

The primary structural driver of market expansion is the European Union’s increasingly stringent CO regulatory framework. Under Regulation (EU) 2019/631, original equipment manufacturers are required to achieve a 15% fleet-wide CO reduction between 2025 and 2027, a 55% reduction by 2030, and complete transition to zero-emission fleets by 2035. This regulatory pressure has already produced measurable market effects.

The International Council on Clean Transportation (ICCT) reported that battery electric vehicle registrations rose by approximately 31% in 2025 compared with 2024, raising the BEV share to a record 19%. Concurrently, the European Automobile Manufacturers’ Association (ACEA) observed a 20.6% decline in petrol and a 27.1% decline in diesel registrations in Q1 2025, underscoring a decisive industry shift toward electrification.

Rapid Decline in Battery Costs and Expanding Charging Infrastructure

The sustained decline in battery prices and the rapid expansion of Europe’s public charging network are significantly enhancing the economic viability of vehicle electrification for mainstream consumers. According to Transport & Environment, battery costs are expected to decrease by approximately 27% between 2022 and 2025, with an additional 28% reduction projected by 2027. This downward trajectory enables OEMs to introduce battery-electric vehicles priced below €25,000, supported by the launch of at least 9 affordable models in 2025 and an anticipated 19 models by 2027.

Concurrently, Europe’s public charging infrastructure has grown to roughly 1.14 million charging points by the end of 2025, covering 77% of the EU core highway network. Together, these developments are substantially expanding market opportunities for key electrification components.

Restraints - Uneven EV Adoption Across Member States Creating Market Fragmentation

A major constraint on market consolidation is the pronounced geographic disparity in EV adoption across European member states, which generates supply chain inefficiencies and uneven demand for electrification components. ICCT data for 2025 indicates that Norway reached a 95.9% BEV market share, while Denmark exceeded a 68% combined EV share.

In contrast, Italy achieved only 6% BEV penetration, and Poland remained below 5% in 2024. This fragmentation compels OEMs to maintain dual product strategies, simultaneously supporting ICE and EV platforms. Divergent national subsidy structures, such as France’s reduced incentives, which contributed to a 14% drop in BEV registrations in early 2025, further erode long-term production efficiency.

High Upfront Cost of EVs Relative to ICE Vehicles

Despite supportive policy measures, the elevated pricing of battery electric vehicles relative to conventional internal combustion models remains a significant impediment to mass-market adoption. ACEA data indicates that BEVs accounted for only 15.2% of new registrations in Q1 2025, substantially below the projected 30% for the year. T&E analysis suggests that OEMs leveraged the EU’s compliance flexibility to increase EV price premiums, potentially resulting in two million fewer BEVs sold than under stricter regulatory conditions.

Furthermore, ICCT findings show that public charging in the U.K. is approximately seven times more expensive than home charging, a trend consistent across Europe and a key factor diminishing total cost-of-ownership benefits, particularly in lower-income markets.

Opportunities - 48V Mild Hybrid and Integrated Starter Generator (ISG) Technology Expansion

The accelerating adoption of 48-volt mild hybrid architectures across Europe presents a significant near-term growth opportunity within the electrification components market. The Integrated Starter Generator (ISG) segment is projected to expand at a CAGR of 18.3% from 2025 to 2033, making it the fastest-growing product category due to its ability to deliver substantial CO2 reductions at considerably lower system costs than full electrification.

As OEMs work to meet the EU’s Fit for 55 objectives and achieve a 15% fleet-wide CO2 reduction, 48V systems provide a cost-effective compliance solution for B-and C-segment passenger and light commercial vehicles. Major suppliers, including Valeo S.A. and Continental AG, are scaling ISG production, supported by strong hybrid-electric vehicle adoption targets from OEMs such as Renault Group.

Electrification of Urban Commercial Fleets and Vehicle-to-Grid (V2G) Integration

The electrification of urban logistics, taxi services, and municipal fleets represents a substantial and rapidly expanding revenue opportunity for component manufacturers, supported by favourable operational economics and increasingly stringent city-level emission-zone policies. Light commercial vehicles, which contribute disproportionately to road transport CO2 emissions, have shorter payback periods for electrification due to high utilisation rates and predictable routing.

Furthermore, the EU Battery Regulation, requiring standardised battery communication protocols, is facilitating Vehicle-to-Grid (V2G) integration and enabling new value streams for both fleet and grid operators. According to the EAFO, pilot V2G initiatives are progressing across Germany, the Netherlands, and the U.K. The intersection of Europe’s renewable energy expansion and its growing electrified fleet is driving strong demand for advanced battery management systems, bidirectional onboard chargers, and DC-DC converters over 2026–2033.

Category-wise Analysis

Product Type Insights

The Start/Stop System segment remains the leading product category in the Europe Vehicle Electrification Market, accounting for roughly 33% of market share in 2025. Its continued dominance is driven by mandatory adoption across nearly all new internal combustion engine and mild hybrid vehicles to meet CO2 emission performance requirements under Regulation (EU) 2019/631. Owing to minimal engineering modifications to existing starter motor and battery management systems, Start/Stop solutions offer OEMs the most cost-efficient compliance pathway for high-volume non-electric vehicle production.

With BEVs and PHEVs accounting for only about 21% of new registrations in 2024, most vehicles still rely on start/stop and mild-hybrid technologies. As full electrification progresses, these systems will retain strategic relevance, especially for mass-market manufacturers such as Stellantis N.V. and Renault Group through 2033.

Propulsion Type Insights

Battery Electric Vehicles (BEVs) constitute the leading and fastest-growing propulsion segment in the European vehicle electrification market, accounting for nearly 19% of new passenger car registrations in 2025, up from 13.6% in 2024. BEV registrations expanded by approximately 31% year-on-year, adding more than two million electric cars to the regional fleet. This momentum is reinforced by the European Union’s 2035 zero-emission vehicle mandate, which continues to direct OEM investment toward dedicated BEV platforms.

Germany, the largest individual BEV market, recorded a 43% rise in BEV sales in 2025. The segment also generates the highest per-vehicle demand for electrification components, including large-format battery packs, traction inverters, onboard chargers, and thermal management systems, contributing significantly to overall market revenues.

Country-wise Insights

Norway Europe Vehicle Electrification Market Trends

Norway represents the most mature and advanced vehicle electrification market in Europe, serving as the region’s benchmark for policy-driven transformation. According to data from the Norwegian Road Federation (OFV) and the European Alternative Fuels Observatory (EAFO), battery-electric vehicles achieved a dominant 95.9% share of new passenger car registrations in 2025, relegating internal combustion engine vehicles to a marginal position. This exceptional transition is the outcome of long-standing, multi-instrument policies, including VAT exemptions, import duty waivers, toll reductions, bus-lane access, and Europe’s densest public charging network, offering approximately 46 chargers per 1,000 vehicles.

Commercial fleet electrification is also advancing rapidly, supported by Norway’s hydropower-based energy mix, which ensures near-zero lifecycle emissions. The government’s commitment to ending new sales of fossil-fuel cars further solidifies Norway’s leadership and its importance as a technology validation hub.

Poland Europe Vehicle Electrification Market Trends

Poland has emerged as Europe’s fastest-growing vehicle electrification market, recording an exceptional +125% increase in BEV registrations year-to-date through October 2025 compared with the same period in 2024. This rapid expansion reflects a delayed yet accelerating policy-driven transition, as Poland, one of Europe’s largest automotive markets, maintained EV penetration below 5% through 2024, creating substantial structural headroom for growth. The EU’s CO2 compliance framework serves as the primary catalyst, compelling OEMs with significant Polish fleet exposure to expedite zero-emission vehicle registrations.

Poland’s cost-competitive manufacturing base further strengthens momentum, supported by Stellantis N.V.’s establishment of EV assembly operations and EU AFIR-funded investments that expand charging infrastructure across motorways and urban centres. Collectively, these factors position Poland as a strategically important and rapidly expanding market for electrification components through 2026–2033.

Germany Europe Vehicle Electrification Market Trends

Germany is the second-largest market for vehicle electrification in Europe and the region’s leading country in absolute BEV registrations. According to the Kraftfahrt-Bundesamt (KBA), Germany, surpassed the two million BEV mark in its passenger car fleet in 2025, reflecting deep structural adoption of zero-emission mobility. BEV registrations increased by 43% in 2025, rebounding from the 27% decline in 2024 following the abrupt termination of the Umweltbonus programme, as noted by the European Environment Agency.

New subsidies planned for 2026 are expected to support continued growth. Beyond market demand, Germany serves as the industrial centre of European electrification, hosting major OEM and Tier-1 R&D hubs. The European Commission’s approval of a €1.6 billion state aid scheme in 2025 further strengthens its leadership in charging-infrastructure deployment.

Competitive Landscape

Europe Vehicle Electrification Market demonstrates a moderately consolidated structure at the OEM level, with the top five manufacturers, Volkswagen Group, Tesla, Inc., BMW Group, Mercedes-Benz Group, and Stellantis N.V., collectively accounting for a substantial share of BEV registrations. Key competitive strategies include shared EV platforms, vertical integration through initiatives like PowerCo’s gigafactory expansion, and continued R&D investment in advanced 800V power electronics. Emerging dynamics, including accelerated entry from Chinese OEMs, particularly BYD, which recorded approximately +240% YTD EU sales growth in 2025, and cross-border collaborations targeting solid-state batteries and next-generation inverters, further intensify competition.

Key Market Developments

- March 2026: BYD Auto announced the launch of its premium electric vehicle, the Denza Z9GT, in Europe, featuring advanced “flash-charging” technology that can charge the battery from 10% to 70% in approximately 5 minutes. The model also offers a driving range of up to 800 km, significantly higher than many current EV models in the region.

- January 2025: Volkswagen Group reported an 89% surge in BEV sales across Europe in H1 2025, driven by upgraded model launches and competitive pricing on the ID.3 and ID.4 platforms in direct response to tightening EU CO2 compliance targets for the 2025–2027 regulatory period.

- December 2025: Stellantis announced a strategic partnership with Bolt to accelerate the deployment of Level-4 autonomous (driverless) electric mobility services across Europe. The collaboration combines Stellantis’ AV-Ready autonomous vehicle platforms with Bolt’s large ride-hailing and mobility network to support commercial autonomous vehicle operations.

Top Companies in the European Vehicle Electrification Market

Volkswagen Group (Wolfsburg, Germany) is the dominant OEM in the European vehicle electrification market. The Group’s MEB and PPE electric platforms underpin BEV models across Volkswagen, Audi, Porsche, Škoda, and SEAT/CUPRA brands. With a remarkable 89% surge in BEV sales in H1 2025 across Europe, and the PowerCo subsidiary advancing gigafactory capacity in Valencia to secure battery supply chain sovereignty, the Group’s vertically integrated EV strategy and unrivalled manufacturing scale position it as the foremost electrification OEM across the continent.

Robert Bosch GmbH (Gerlingen, Germany) is the world’s largest automotive supplier and a pivotal enabler of Europe’s vehicle electrification transition. Bosch supplies the broadest portfolio of electrification components, including start/stop systems, 48V eDrive units, traction inverters, and battery management systems, to virtually every major European OEM. The company’s unparalleled scale, cross-platform technology breadth, and sustained R&D investment in next-generation power electronics make it an irreplaceable partner across the full vehicle electrification value chain.

Tesla, Inc. (Austin, U.S.) remains Europe’s leading BEV brand by share and a pivotal technology reference point for the industry. Gigafactory Berlin-Brandenburg provides localised production of the Model Y, ensuring competitive pricing and supply responsiveness for European consumers. While Tesla’s European market share faced competitive pressure in 2025 from intensifying OEM and Chinese challengers, its vertically integrated software-defined vehicle architecture, proprietary Supercharger network, and continuous OTA update capability continue to set industry benchmarks for charging technology and the connected vehicle customer experience.

Companies Covered in Europe Vehicle Electrification Market

- Volkswagen Group

- Tesla, Inc.

- BMW Group

- Mercedes-Benz Group

- Stellantis N.V.

- Renault Group

- Kia Group

- BYD Co., Ltd.

- DENSO CORPORATION

- Johnson Electric

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Valeo S.A.

- Daimler AG

Frequently Asked Questions

The Europe Vehicle Electrification Market is valued at US$ 8.5 Bn in 2026 and is projected to reach US$ 15.6 Bn by 2033, growing at a compound annual growth rate (CAGR) of 9.1% during the 2026–2033 forecast period. Historically, the market expanded at a CAGR of 6.1% between 2020 and 2025, with the market estimated at US$ 6.0 Bn in 2020.

The primary demand driver is the European Union’s stringent CO₂ regulatory framework under Regulation (EU) 2019/631, which mandates a 15% fleet-wide CO₂ reduction for 2025–2027, a 55% reduction by 2030, and zero-emission new car sales by 2035. This binding framework directly compels every OEM operating in Europe to accelerate investment in electrification technology, components, and platforms, creating sustained structural demand growth through the forecast period.

The Start/Stop System segment leads the Product Type category with approximately 33% market share. Its leadership is driven by mandatory integration requirements across ICE and mild hybrid vehicles under EU Regulation (EU) 2019/631 CO₂ standards, combined with the technology’s cost-effectiveness as the lowest-barrier compliance mechanism for mass-market OEMs producing high volumes of non-fully electric vehicles.

Norway leads the European Vehicle Electrification Market, achieving a landmark 95.9% BEV share of new passenger car registrations in 2025 according to the Norwegian Road Federation (OFV). Decades of consistent policy incentives, including VAT exemptions, toll waivers, and Europe’s most dense public charging network, have created an unparalleled EV adoption environment that serves as a benchmark for the rest of Europe.

The most significant opportunity lies in the convergence of urban commercial fleet electrification and Vehicle-to-Grid (V2G) technology integration. Enabled by the EU Battery Regulation’s standardised BMS communication protocols, V2G technology unlocks new revenue models for fleet operators and grid managers, driving disproportionate demand growth for bidirectional onboard chargers, advanced battery management systems, and DC-DC converters over the 2026–2033 horizon.