- Food Ingredients & Additives

- Wheat Protein Market

Wheat Protein Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Wheat Protein Market by Nature (Organic, Conventional), Form (Wheat Protein Isolates, Concentrate Wheat Protein, Hydrolyzed Wheat Protein), Application (Food, Animal Feed, Sports Nutrition & Weight management, Nutraceuticals, Cosmetics, Others), and Regional Analysis from 2026 - 2033

Wheat Protein Market Share and Trends Analysis

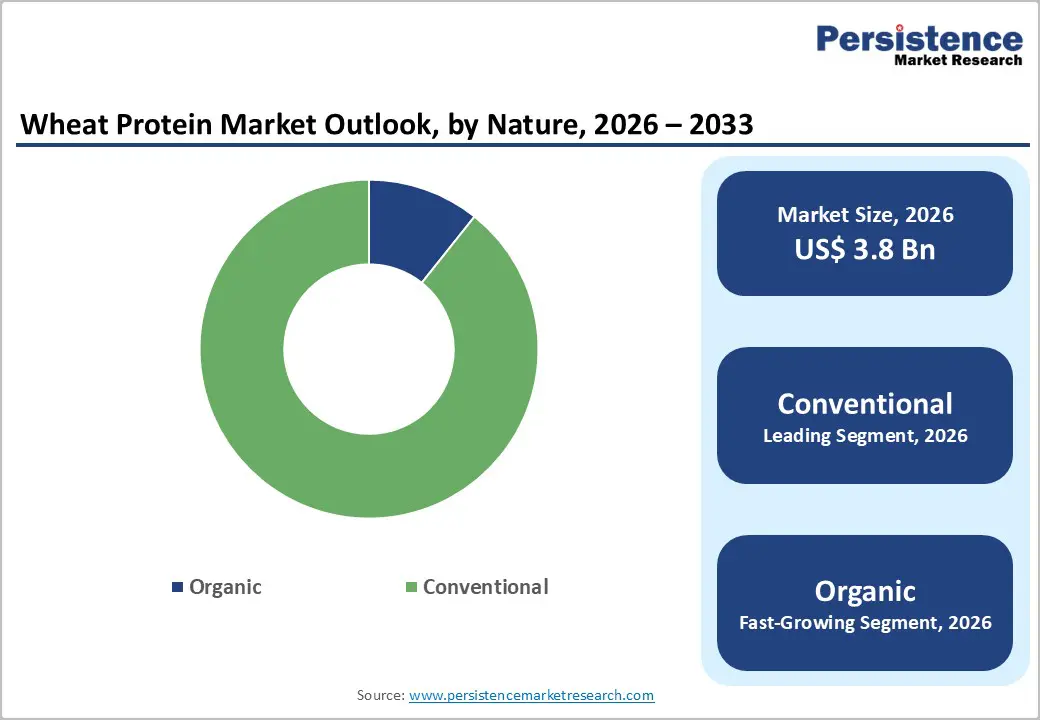

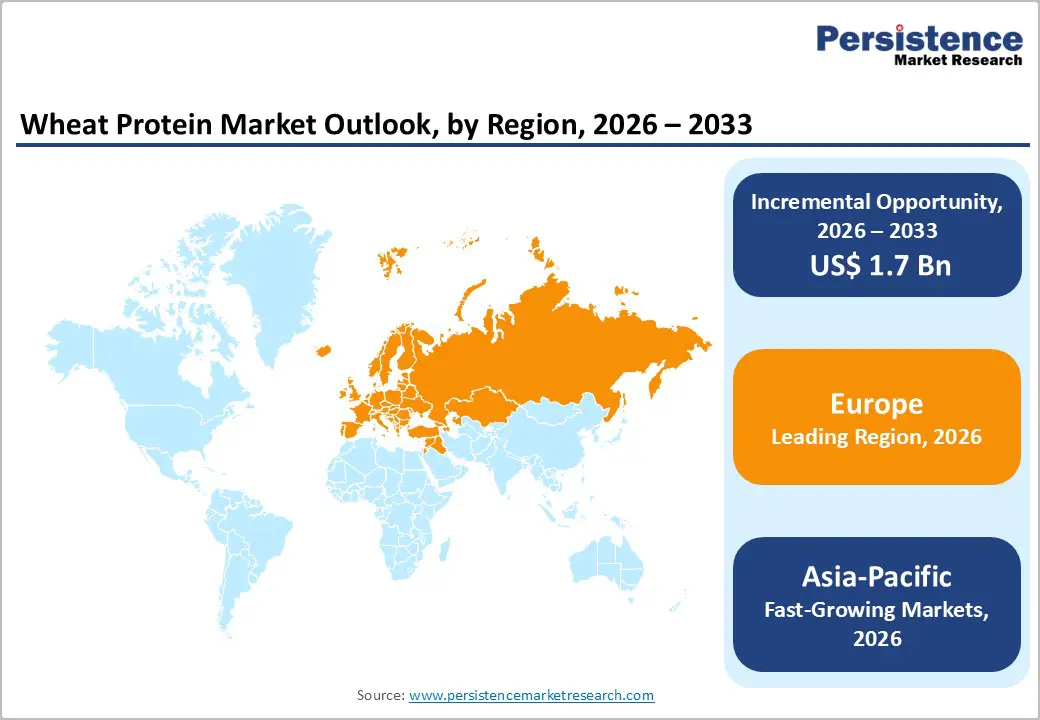

The global wheat protein market is estimated to grow from US$ 3.8 billion in 2026 to US$ 5.5 billion by 2033, projected to record a CAGR of 5.4% during the forecast period from 2026 to 2033. The global market is growing steadily, fueled by rising food consumption, urbanization, and changing dietary preferences. Europe leads in overall market share, while North America is the fastest-growing region due to health-conscious consumers, premium product demand, and expanding use in gourmet cooking and foodservice. Asia Pacific shows strong growth from large-scale production and high consumption.

Key Industry Highlights:

- Dominant Form Segment: Concentrate wheat protein (50–80% protein) is widely used in bakery, meat alternatives, snacks, and nutrition products, valued for functional, clean-label properties, driving global demand across household, foodservice, and industrial applications.

- Dominant Region: Europe held 37.6% share in 2025, supported by strong food processing infrastructure, high bakery and plant-based protein consumption, and growing demand for premium nutrition products in countries like Germany, France, Italy, and the UK.

- Growth Indicators: Growth is fueled by rising protein consumption, urbanization, expanding plant-based and health-focused food sectors, demand for functional and clean-label ingredients, and evolving dietary preferences toward high-protein and alternative foods.

- Market Opportunity: Opportunities exist in wheat protein isolates, hydrolyzed wheat protein, organic and clean-label products, innovative formulations, sports nutrition, and expanding penetration in Asia Pacific, Latin America, and Middle East & Africa.

| Key Insights | Details |

|---|---|

|

Global Wheat Protein Market Size (2026E) |

US$ 3.8 Bn |

|

Market Value Forecast (2033F) |

US$ 5.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

DRO Analysis

Driver: Rising Demand for High-Protein and Functional Foods

Global per-capita protein availability has increased substantially in recent decades, with cereal-derived proteins contributing a large share of plant protein in diets worldwide. FAO data show per-capita food and protein availability in Southeast Asia increased by 85.1 % from 1961 to 2018, reflecting broader global trends where protein availability has risen alongside economic and dietary changes. FAO data further indicate that cereals, including wheat, provide foundational protein for human diets and form a stable share of dietary energy.

Concurrently, consumer behavior in major economies highlights a marked shift toward high-protein foods. For example, 39 % of consumers are actively trying to increase plant-based protein intake, and high-protein claims in new product launches have grown by over 22 %, indicating rising demand for functional protein ingredients. Plant proteins, such as those derived from wheat, are increasingly incorporated into bakery, meat alternatives, and nutrition products to meet demand for protein-rich, convenient foods that align with health, environmental, and sustainability goals.

Restraint: High Cost of Protein Isolates and Specialty Ingredients

Production of highly processed protein ingredients, such as wheat protein isolates and hydrolyzed fractions, involves complex extraction and refinement steps that elevate costs relative to more basic ingredients. Research on protein hydrolysates highlights that enzymatic hydrolysis requires specialized protease enzymes priced around USD 15–25 per kilogram, along with controlled processing environments, making production 40–60% more expensive than non-hydrolyzed proteins.

These elevated production costs translate into higher input costs for manufacturers of specialty wheat protein products. In markets where price sensitivity is significant, such as in developing regions or low-margin food segments this can limit adoption rates. Additionally, regulatory and quality requirements for high-protein formulations further increase compliance costs for facilities that must maintain strict environmental, safety, and nutritional standards. As a result, companies may hesitate to expand production capacity or introduce premium isolates without clear demand justification, restraining broader market penetration in cost-constrained segments.

Opportunity: Innovations in Fnctional and Hydrolyzed Wheat Protein Products

Advances in processing technologies present significant opportunities for wheat protein market growth. Improved enzymatic hydrolysis, fractionation, and extraction methods enhance functionality, digestibility, and nutritional profiles of wheat protein derivatives. Innovations in hydrolyzed wheat protein, for example, have expanded its applicability beyond traditional baking into fortified beverages, nutrition bars, and personal care formulations due to enhanced emulsification and texture-improving properties.

Moreover, increasing consumer preference for natural, plant-based ingredients continues to support functional innovation. Hydrolyzed wheat protein demonstrates moisturizing and texturizing benefits, fueling its use in food applications and hair/skin care products. As plant-based diets and clean-label consumer priorities grow, ingredients that deliver multiple functional benefits, nutritional, sensory, and technical are increasingly attractive. This trend creates opportunities for wheat protein manufacturers to differentiate offerings via targeted product innovation, expanding into sports nutrition, fortified foods, and premium functional formulations that address emerging dietary and lifestyle demands.

Category-wise Analysis

By Nature Insights

Conventional wheat protein dominates the market because conventional wheat accounts for the vast majority of global wheat production and utilization. According to the UN Food and Agriculture Organization (FAO), global wheat production reached ~787 million tonnes in 2023, of which over 95 % is grown under conventional systems, with organic wheat constituting a small fraction (FAOSTAT). Conventional farming yields are generally higher and more consistent, helping keep raw material costs lower. In the US, the USDA reports that only ~1.5 % of total wheat acreage is certified organic, reflecting a limited organic supply. Since wheat protein is derived from flour and milling fractions of conventional wheat, the prevalence of conventional wheat in global supply chains directly leads to conventional wheat protein dominating the market, driven by availability, cost efficiency, and established processing infrastructure.

By Form Insights

Concentrate wheat protein dominates because it balances high protein content, functional performance, and cost efficiency compared to isolates and hydrolysates. USDA and agricultural extension data show that typical wheat flour contains about 10–15 % protein, whereas concentrate processes selectively remove non-protein components to yield 50–80 % protein, sufficient for many applications such as bakery, meat alternatives, and snacks. In contrast, isolates require additional processing to exceed ~90 % protein, increasing energy and enzyme use. Industry nutritional data also indicate concentrate’s superior water absorption and emulsification, improving texture in foods without the higher cost and technical complexity of isolates. Because concentrates offer functional versatility at moderate cost, they are preferred by food manufacturers seeking protein enrichment without premium pricing, driving their dominant share in the wheat protein market.

Regional Insights

Europe Wheat Protein Market Trends

Europe dominates the wheat protein market with 37.6% share in 2025, as the growth is high in terms of wheat producers and a major consumer of wheat-based foods, which underpins a strong raw material supply and downstream demand. According to FAOSTAT data, Europe is home to several of the world’s largest wheat producers and users, with countries like France and Germany among the top globally; wheat production in the EU exceeded 110 million tonnes in recent years. European consumers also show heightened interest in plant-based and flexitarian diets, reflected in dietary surveys indicating elevated meat reduction and plant food intake. This combination of production scale, entrenched wheat food culture, and rising plant-protein interest drives demand for wheat protein ingredients across bakery, meat alternatives, and functional food applications.

North America Wheat Protein Market Trends

North America is a critical wheat protein market due to its large wheat production and strong processing industry, particularly in the United States, where wheat output approaches 50 million-tonnes annually. This ample domestic supply supports extensive use of wheat protein in food manufacturing. North American consumers also exhibit strong interest in high-protein, plant-based products; surveys show a significant share of consumers reducing animal protein and experimenting with plant alternatives, reflecting broader demand for plant proteins. Combined with advanced food technology infrastructure and high food processing capacity, this makes North America a major market for wheat protein isolates, concentrates, and textured proteins, particularly in sports nutrition, bakery, and meat alternative segments.

Asia Pacific Wheat Protein Market Trends

Asia Pacific is the fastest-growing wheat protein market due to rapid population growth, urbanization, and rising incomes, which are expanding demand for protein-rich foods. FAO and USDA data confirm that China and India together contribute a significant portion of global wheat production, ensuring abundant raw material availability for protein extraction. As lifestyles shift toward processed and convenience foods, wheat protein is increasingly incorporated into bakery, snacks, and emerging plant-based products. Additionally, expanding middle classes in countries like China, India, and Southeast Asia are adopting health-oriented diets, seeking affordable, nutritious sources of protein, further accelerating wheat protein uptake. Regional food processing industries are also scaling up, enabling wider distribution and innovation in wheat protein applications, reinforcing the Asia Pacific’s rapid market expansion.

Competitive Landscape

The global wheat protein market is competitive, led by global players such as The Kraft Heinz Company, Mizkan Group, and Unilever. Companies focus on innovation, premium products, sustainable sourcing, and expanding distribution, catering to rising demand across retail, foodservice, and processed food sectors worldwide.

Key Industry Developments:

- In June 2025, Roquette Expanded Its NUTRALYS® Plant Protein Portfolio With New Textured Wheat and Pea Proteins. Roquette expanded its NUTRALYS® plant protein range by launching its first ever textured wheat protein, along with a new large chunk textured pea protein.

- In January 2025, Cargill announced it had aimed to establish new benchmarks in nutritional innovation, sustainability, and wellness across its food solutions business. The company integrated advanced technologies and strategic initiatives to align product development with growing consumer demand for healthier, more sustainable options.

Companies Covered in Wheat Protein Market

- Cargill, Incorporated

- Archer Daniels Midland

- MGP

- Roquette Frères

- Tereos

- Kröner-Stärke

- Manildra Group

- Royal Ingredients Group

- BENEO

- Bryan W Nash & Sons Ltd.

- Aminola

- Sacchetto SpA

- GC Ingredients Inc.

- Meelunie B.V

- AminoSib

- Glico Nutrition Co., Ltd.

- KELISEMA

- Blattmann Schweiz AG

- Others

Frequently Asked Questions

The global wheat protein market is projected to be valued at US$ 3.8 Bn in 2026.

Rising protein demand, plant-based diets, functional foods, urbanization, and expanding foodservice and processed food sectors.

The global wheat protein market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Organic and clean-label products, hydrolyzed proteins, functional formulations, meat alternatives, sports nutrition, emerging market expansion, and innovation.

Cargill, Incorporated, Archer Daniels Midland, MGP, Roquette Frères, Tereos, Kröner-Stärke.