- Beverages

- Wheat Beer Market

Wheat Beer Market Size, Share, and Growth Forecast, 2025 - 2032

Wheat Beer Market by Product Type (Traditional Wheat Beer, Craft Wheat Beer, Flavored Wheat Beer), Alcohol Content (Low Alcohol Wheat Beer, Medium Alcohol Wheat Beer, High Alcohol Wheat Beer), Distribution Channel, and Regional Analysis for 2025 - 2032

Wheat Beer Market Size and Trends Analysis

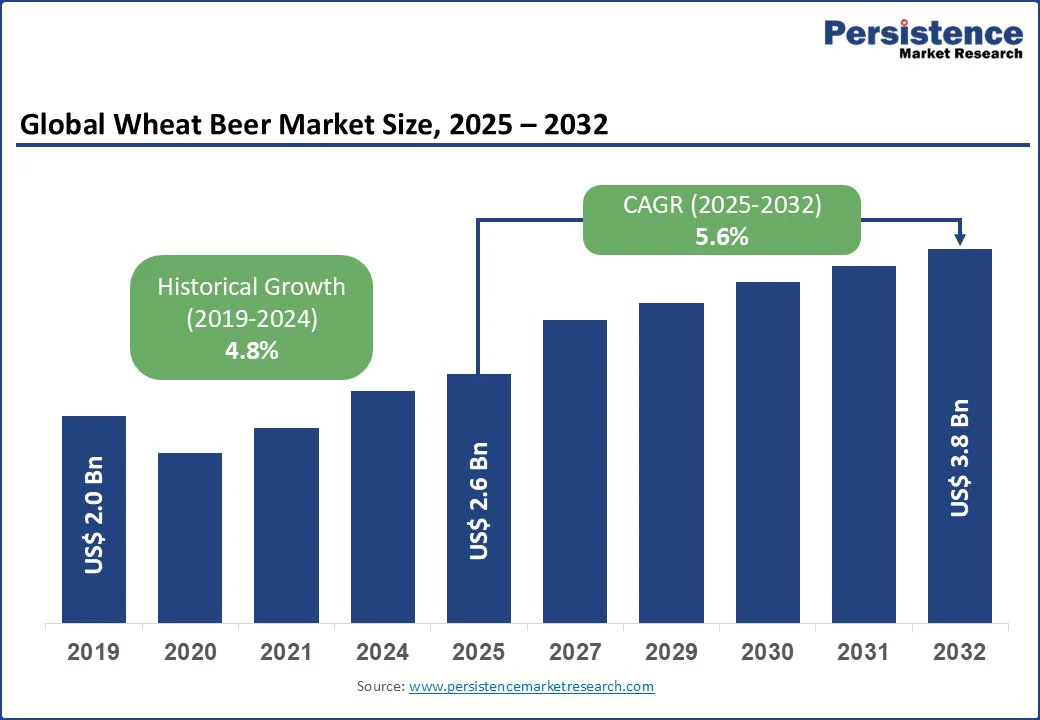

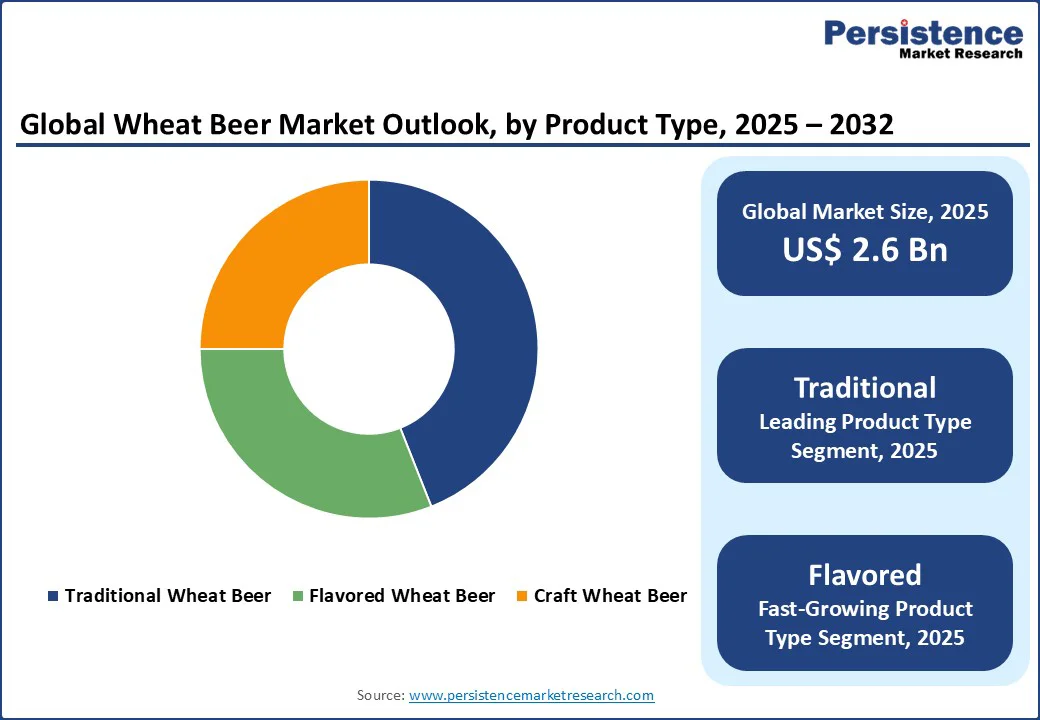

The global wheat beer market size is likely to be valued at US$ 2.6 Bn in 2025 and is expected to reach US$ 3.8 Bn by 2032, growing at a CAGR of 5.6% during the forecast period from 2025 to 2032.

The wheat beer market has experienced steady growth, driven by increasing consumer preference for craft and flavored beers, rising disposable incomes, and the expansion of distribution channels, particularly online retail.

Key Industry Highlights:

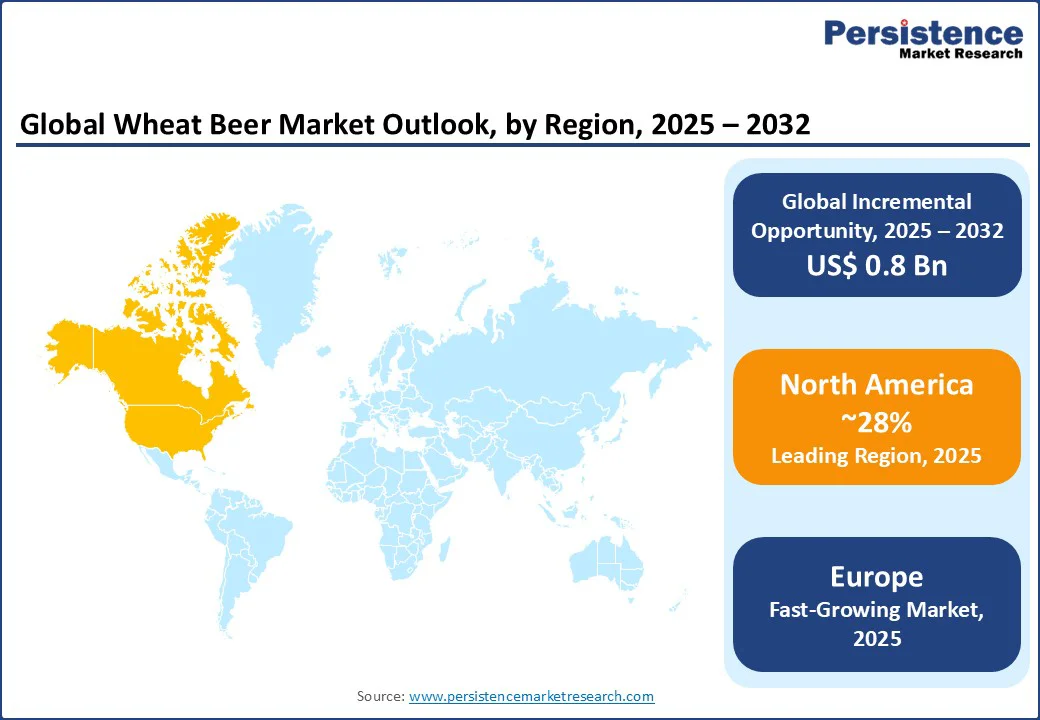

- Leading Region: North America dominates with a 28% share in 2025, driven by craft beer culture, artisanal demand, brewery expansion, innovation, and evolving consumer preferences.

- Fastest-growing Region: Europe is the fastest-growing, fueled by rich brewing traditions, premiumization trends, rising craft beer consumption, and increasing demand for innovative wheat beer styles.

- Dominant Product Type: Traditional wheat beer accounts for approximately 44%, driven by its appeal to younger demographics and innovative flavor profiles.

- Leading Alcohol Content: Medium alcohol wheat beer leads with a 48% share, reflecting its widespread acceptance in social settings.

- Leading Distribution Channel: Supermarkets/Hypermarkets lead with a 39% share in 2025, driven by their role as primary consumption venues for wheat beer.

| Key Insights | Details |

|---|---|

| Wheat Beer Market Size (2025E) | US$ 2.6 Bn |

| Market Value Forecast (2032F) | US$ 3.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market Dynamics

Driver - Rising Demand for Craft and Flavored Beers

The rising demand for craft and flavored beers, which cater to consumers seeking unique, premium, and experiential beverage options. Modern beer consumers, particularly Millennials and Gen Z, increasingly prefer products that offer distinct taste profiles, innovative ingredients, and artisanal production methods.

Flavored wheat beers, such as fruit-infused, spiced, or low-alcohol variants, are gaining popularity as they provide a refreshing alternative to traditional beer styles. For instance, Brewed by Bayerische Staatsbrauerei Weihenstephan, this traditional German wheat beer offers fruity nuances of banana and cloves, creating a balanced beer with a light, creamy character.

Craft breweries are also experimenting with seasonal offerings, small-batch productions, and local ingredients, reinforcing the perception of authenticity and exclusivity. This trend has encouraged established players to innovate and expand their portfolios, while smaller breweries leverage social media, taprooms, and e-commerce platforms to reach niche audiences.

Collectively, the rising preference for craft and flavored beers not only fuels wheat beer consumption but also accelerates market diversification and revenue growth globally.

Restraint - High Production Costs and Regulatory Challenges

The high production costs combined with complex regulatory challenges. Producing wheat beer often involves specialized ingredients, including high-quality wheat malt, specific yeast strains, and adjunct flavorings for fruit- or spice-infused variants, which increases raw material expenses.

Small and medium-sized breweries, particularly craft brewers, face higher per-unit production costs compared to large-scale commercial breweries due to limited economies of scale. Additionally, advanced brewing equipment, quality control, and storage facilities add further financial burden.

Regulatory challenges also constrain market growth. Alcoholic beverages, including wheat beer, are subject to strict licensing, labeling, and taxation policies that vary across countries and regions. Compliance with these regulations, such as government-mandated ingredient disclosures, health warnings, and environmental standards, can be both time-consuming and costly.

Exporting wheat beer to international markets introduces additional hurdles, including import duties, certification requirements, and adherence to varying safety standards. These factors collectively increase production costs and limit profitability, particularly for smaller breweries attempting to compete in premium or innovative segments.

For instance, craft breweries producing flavored or low-alcohol wheat beers may struggle to maintain competitive pricing while meeting regulatory standards, which can slow market expansion despite growing consumer demand.

Opportunity - Growth in Online Retail and Direct-to-Consumer Models

The growth of online retail and direct-to-consumer (DTC) models presents a significant opportunity for the wheat beer market. Increasing internet penetration, widespread smartphone adoption, and the convenience of e-commerce platforms have transformed consumer purchasing behavior, enabling beer enthusiasts to access a broader range of products without geographic constraints.

Online channels allow both established breweries and craft producers to reach niche and younger audiences, particularly Millennials and Gen Z, who value convenience, variety, and personalized experiences.

Direct-to-consumer sales, often facilitated through brewery websites, subscription services, and mobile apps, provide an avenue for higher margins by reducing reliance on traditional distribution channels such as supermarkets and bars.

Craft breweries can leverage DTC models to introduce limited-edition, seasonal, or experimental wheat beer variants, engaging consumers with exclusive offerings while building brand loyalty. For instance, Molson Coors launched an e-commerce platform for Blue Moon, partnering with Drizly and Minibar Delivery, offering exclusive, seasonal wheat beers, including Belgian White, to meet growing demand for limited-edition products.

Category-wise Analysis

Product Type Insights

Traditional wheat beer holds approximately 44%, driven by its appeal to younger consumers, classic styles such as Hefeweizen and Witbier, widespread availability, and premium offerings from breweries in Europe and North America.

Flavored wheat beer is the fastest-growing segment, fueled by rising consumer demand for innovative citrus, berry, and spice-infused varieties. Millennials and Gen Z particularly favor these unique, refreshing flavors, boosting market expansion across craft breweries and premium beverage channels.

Alcohol Content Insights

Medium alcohol wheat beer leads with a 48% share, driven by its balanced taste, versatility, and widespread popularity in social settings. Its approachable flavor and moderate strength make it a preferred choice for casual and group consumption.

Low alcohol wheat beer is the fastest-growing segment, driven by increasing health consciousness and a preference for lighter, refreshing beverages. Younger consumers, particularly Millennials and Gen Z, are adopting these options, boosting demand across craft breweries, retail, and on-trade channels.

Distribution Channel Insights

Supermarkets and hypermarkets lead the wheat beer market with a 39% share, driven by their convenience, wide product assortment, competitive pricing, and role as primary purchase and consumption venues for both mainstream and craft wheat beer consumers.

Online retailers are the fastest-growing distribution segment for wheat beer, driven by the expansion of e-commerce platforms, direct-to-consumer (DTC) models, and increasing urban consumer adoption, offering convenience, wider selection, and access to craft and premium wheat beer brands.

Regional Insights

Asia Pacific Wheat Beer Market Trends

The Asia-Pacific wheat beer market is experiencing steady growth, driven by rising disposable incomes, urbanization, and changing consumer preferences toward premium and flavored beers. Countries such as China, India, Japan, and Australia are witnessing increasing demand for both craft and mainstream wheat beer styles.

Young urban consumers are particularly attracted to innovative flavors, low- and medium-alcohol options, and imported premium brands. Expansion of modern retail channels, including supermarkets, hypermarkets, and e-commerce platforms, has enhanced product accessibility, while craft breweries and local brands are gaining visibility through taprooms, festivals, and social media marketing.

The growing awareness of beer culture, coupled with increasing interest in food pairing and dining experiences, supports consistent adoption of wheat beers. While the sector is still maturing compared to Europe and North America, the combination of favorable demographics, evolving tastes, and retail expansion ensures a steady growth trajectory for wheat beer in the Asia-Pacific region over the coming years.

North America Wheat Beer Market Trends

North America dominates the global wheat beer market, holding an estimated 28% share in 2025, largely due to the region’s robust craft beer culture, growing consumer preference for artisanal beverages, and the continuous expansion of brewery networks across the United States and Canada. The craft beer movement has redefined the industry, shifting consumer interest from mass-produced options to locally brewed, premium-quality beers with distinctive flavors.

Wheat beers, in particular, have benefited from this trend, as styles such as Hefeweizen, Witbier, and American Wheat Ale offer approachable, refreshing profiles that appeal to both casual and dedicated beer drinkers. Millennials and Gen Z consumers are increasingly seeking products that emphasize authenticity, innovation, and sustainability, favoring breweries that highlight small-batch production and locally sourced ingredients.

The growth of brewery taprooms, beer festivals, and beer tourism has strengthened engagement with wheat beer brands, while supermarkets, specialty stores, and online retail channels have improved accessibility and visibility.

Continuous innovation in flavor profiles, including fruit-infused, spiced, and experimental wheat beers, further fuels demand. These combined factors ensure that North America remains the leading regional market, driving both volume and revenue growth while setting trends that influence global wheat beer consumption patterns.

Europe Wheat Beer Market Trends

Europe is the fastest-growing wheat beer market, driven by a combination of rich brewing traditions, premiumization trends, rising craft beer consumption, and increasing demand for innovative wheat beer styles. Countries such as Germany, Belgium, and the Netherlands have long-standing wheat beer heritage, which contributes to strong consumer awareness and loyalty toward classic styles such as Hefeweizen, Witbier, and Weissbier.

At the same time, a growing number of craft breweries across the region are experimenting with unique flavor profiles, including fruit-infused, spiced, and low-alcohol variants, catering to younger demographics and health-conscious consumers.

The premiumization trend in Europe is encouraging consumers to trade up from mass-produced options to higher-quality, small-batch wheat beers that emphasize authenticity, artisanal production, and locally sourced ingredients. Retail expansion, including supermarkets, specialty stores, and online platforms, makes these products widely accessible, while beer festivals, taproom experiences, and brewery tours enhance consumer engagement and brand loyalty.

Furthermore, the increasing influence of social media and food-pairing culture has helped introduce innovative wheat beer styles to a broader audience, reinforcing Europe’s position as a dynamic and fast-growing regional market.

Competitive Landscape

The global wheat beer market is highly competitive, with a mix of multinational brewing giants and regional craft players. In Europe and North America, leading companies such as Anheuser-Busch InBev, Heineken, and Carlsberg dominate through extensive product portfolios, strong distribution networks, and innovations in flavored and low-alcohol wheat beers.

In the Asia Pacific, where demand for premium and craft-style beers is rising, players such as Tsingtao Brewery, CR Beer, and San Miguel are leveraging localized marketing strategies and expanding through partnerships and acquisitions.

Competition is driven by flavor innovation, craft positioning, and sustainability initiatives, including eco-friendly brewing practices, locally sourced ingredients, and waste reduction. Companies such as AB InBev are expanding flavored lineups such as Hoegaarden Rosée and Nectarine, while regional brewers such as Ironhill India are targeting mindful consumers with non-alcoholic wheat beer offerings

. Leading players are investing in R&D, online retail partnerships, and strategic acquisitions to capture evolving consumer preferences. While global brands dominate premium and large-scale distribution, niche craft breweries and regional brands continue to serve artisanal, specialty, and price-sensitive markets, creating a fragmented yet dynamic market landscape.

Key Developments

- In August 2025, AB InBev expanded the Hoegaarden lineup in India with Rosée and Nectarine, enhancing its flavoured wheat beer portfolio to attract younger, experimental, and premium-seeking consumers.

- In March 2025, Ironhill India launched Zero Gravity AF, its first non-alcoholic wheat beer, targeting mindful drinkers, health-conscious consumers, and younger audiences seeking refreshing yet guilt-free options.

Companies Covered in Wheat Beer Market

- Anheuser-Busch InBev

- Coors Brewing Company

- Staropramen

- Peroni Brewery

- Tsingtao Brewery

- Flensburger Brauerei

- CR Beer

- San Miguel

- Duvel

- Carlsberg

- Ambev

- Heineken N.V.

- Asahi

- Miller Brewing Factory

- Others

Frequently Asked Questions

The global wheat beer market is projected to reach US$2.6 billion in 2025.

Rising demand for craft and flavored beers, increasing disposable incomes, and expanding online retail channels are key drivers.

The wheat beer market is poised to witness a CAGR of 5.6% from 2025 to 2032.

Growth in online retail and DTC models, alongside sustainable brewing innovations, presents significant opportunities.

Anheuser-Busch InBev, Heineken N.V., and Carlsberg are among the leading players.