- Food Ingredients & Additives

- Wheat Starch Derivatives Market

Wheat Starch Derivatives Market Size, Share, and Growth Forecast 2026 - 2033

Wheat Starch Derivatives Market by Product Type (Maltodextrin, Glucose Syrups, Fructose, Isoglucose, Dextrose, others), by Form (Powder, Liquid), by End Use (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics, Animal Feed, others), by Regional Analysis, 2026-2033

Wheat Starch Derivatives Market Size and Trend Analysis

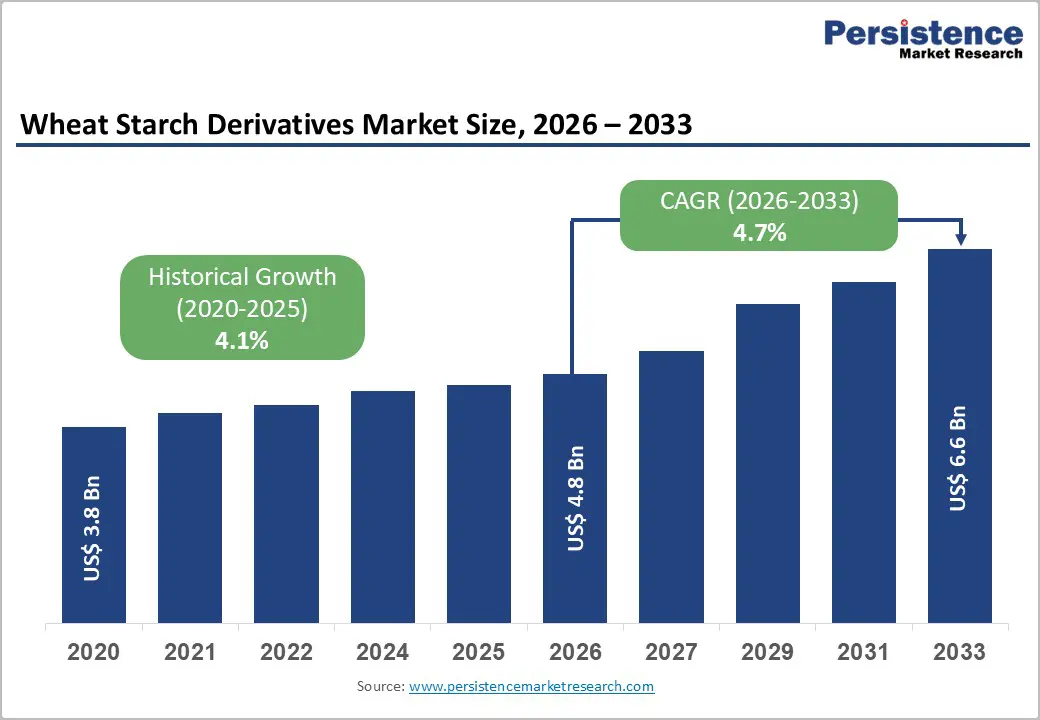

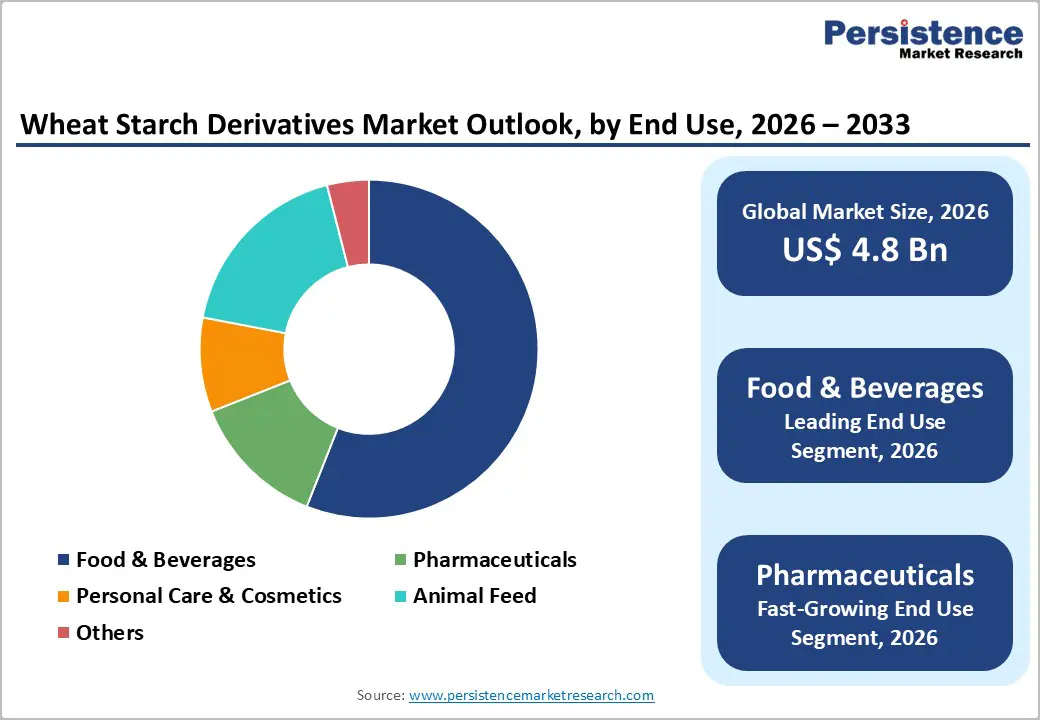

The global Wheat Starch Derivatives Market size is expected to be valued at US$ 4.8 billion in 2026 and projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033

The market expansion is primarily catalyzed by the accelerating shift toward clean-label and plant-based ingredients in the global processed food sector. As consumers increasingly demand transparency and natural alternatives to synthetic additives, wheat-derived sweeteners and texturizers like Maltodextrin and Glucose Syrups have become essential for manufacturers. Furthermore, the robust growth in pharmaceutical applications, where these derivatives serve as high-purity excipients, provides a stable secondary demand pillar, ensuring consistent market momentum across developed and emerging economies through 2033.

Key Industry Highlights

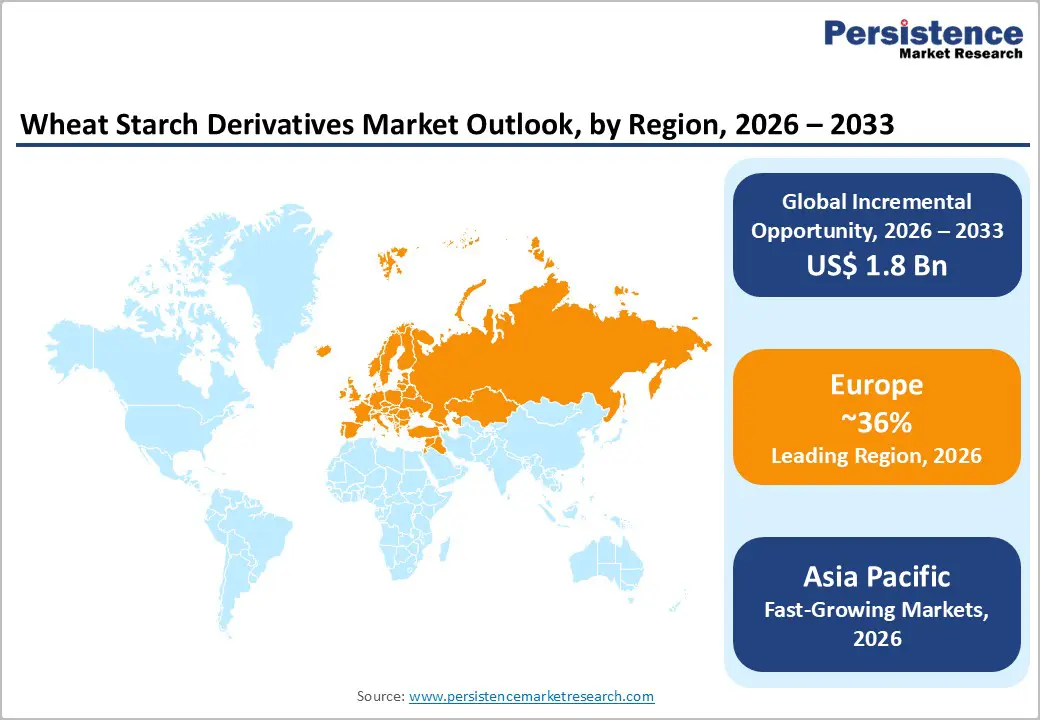

- Leading Region: Europe, accounting for around 36% market share, supported by deep-rooted wheat processing infrastructure, strong regulatory harmonization under EFSA, high non-GMO preference, and rapid adoption of wheat-based solutions in functional bakery and circular bio-economy applications.

- Fastest-Growing Region: Asia Pacific, driven by rapid urbanization, Westernization of diets, expanding food processing capacity, government-backed manufacturing initiatives, and rising pharmaceutical and nutraceutical production across China, India, Japan, and ASEAN markets.

- Fastest-Growing Form Segment: Powdered wheat starch derivatives, supported by superior shelf life, ease of transport, low contamination risk, and dominant usage in pharmaceuticals, infant nutrition, sports nutrition, and dry food premixes.

- Market Drivers: Rising demand for clean-label and functional food ingredients, as manufacturers replace synthetic stabilizers with wheat-derived carbohydrates that enhance texture, mouthfeel, and stability while meeting regulatory and consumer transparency expectations.

- Opportunities: Expansion into biodegradable packaging, starch-based biopolymers, and industrial biosolutions, enabling wheat starch producers to diversify beyond food and pharma into green materials aligned with global plastic reduction and carbon-neutral commitments.

- Key Developments: In June 2025, AGRANA and INGREDION secured full regulatory clearance from all relevant international authorities, including European antitrust approval, for their planned joint venture aimed at strengthening their position in specialty wheat starch derivatives and bio-based ingredient solutions.

| Key Insights | Details |

|---|---|

| Global Wheat Starch Derivatives Market Size (2026E) | US$ 4.8 Bn |

| Market Value Forecast (2033F) | US$ 6.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver – Growing Demand for Clean-Label and Functional Food Ingredients

The global transition toward "clean-label" products is a definitive driver for the Wheat Starch Derivatives Market. Modern consumers are scrutinizing ingredient lists more than ever, favoring natural carbohydrates over chemical stabilizers. Wheat starch derivatives, particularly Maltodextrin and Native Wheat Starch, are prized for their ability to provide fat-mimetic properties and enhance mouthfeel in low-calorie products without the need for synthetic modifiers. According to the Food and Agriculture Organization (FAO), global caloric intake from processed but natural-based sources has risen by 12% over the last decade. This trend is particularly visible in the bakery and confectionery sectors, where Südzucker AG and Roquette Frères have reported increased demand for non-GMO wheat derivatives that comply with stringent European Union (EU) food safety standards.

Restraints – Volatility in Raw Material Prices and Climate Impact on Wheat Yields

The primary barrier to consistent market growth is the extreme price volatility of raw wheat, which accounts for over 60% of the total production cost of derivatives. Global wheat prices are highly sensitive to geopolitical tensions and climate-related disruptions, such as the prolonged droughts in the U.S. Great Plains and shifting harvest cycles in the Black Sea region. Data from the International Grains Council (IGC) indicates that wheat price indices fluctuated by more than 25% between 2023 and 2025. Such instability forces manufacturers to frequently adjust their pricing strategies, which can deter long-term contracts with price-sensitive end-users in the animal feed and industrial sectors, ultimately squeezing profit margins for major players like Tereos Group.

Opportunity – Advancements in Biodegradable Packaging and Industrial Biosolutions

Environmental regulations targeting single-use plastics are creating a lucrative secondary market for starch-based biopolymers. Wheat starch derivatives are being increasingly researched and utilized as a base for biodegradable films and eco-friendly adhesives. The United Nations Environment Programme (UNEP) has emphasized the need for bio-based alternatives to reduce plastic waste, prompting governments in Europe and Asia Pacific to provide subsidies for bio-refineries. This shift offers a massive opportunity for wheat starch producers to diversify their portfolios beyond food and pharma. By refining wheat starch into specialized glucose polymers for bioplastic production, companies can tap into the Global Green Packaging Market, which is projected to grow significantly as major consumer goods companies commit to 100% recyclable or compostable packaging by 2030.

Category-wise Analysis

Form Analysis

The Powder segment represents the leading form in the market, commanding an estimated 78% market share in 2025. The overwhelming preference for the powder format is driven by its superior shelf-life, ease of transportation, and versatile application in dry-mix formulations. In the pharmaceutical sector, powdered Maltodextrin and Dextrose are vital for tablet compression and as carriers for active ingredients. Additionally, the Powder form is the standard for the sports nutrition and infant formula industries, which require high-purity, easily soluble carbohydrates. The logistical advantage of powder specifically the reduced risk of microbial contamination compared to liquid formats makes it the preferred choice for international trade. Manufacturers such as Ingredion Incorporated have focused their research and development on improving the flowability and dispersion rates of powdered wheat derivatives to maintain this market lead.

End Use Analysis

The Food & Beverages sector is the largest end-user segment, holding a significant 56% market share as of 2025. This segment's dominance is rooted in the ubiquitous use of wheat starch derivatives across nearly every sub-category of processed food, from ready-to-eat meals to artisanal breads. The "functional food" trend has further boosted this segment, as wheat derivatives are used to improve the nutritional profile of high-fiber and low-fat products. Conversely, the Pharmaceuticals segment is identified as the fastest-growing end-use category with a projected CAGR of approximately 5.4% through 2032. The surge in demand for sophisticated drug delivery systems and the globalization of the clinical nutrition market are the primary catalysts. As companies like Roquette Frères introduce highly specialized, low-endotoxin wheat derivatives for injectable formulations, the pharmaceutical segment is expected to capture an increasing share of total market value.

Region-wise Insights

North America Wheat Starch Derivatives Market Trends and Insights

North America remains a cornerstone of the global market, driven by a highly sophisticated food processing infrastructure and a massive pharmaceutical industry. The United States leads the region, characterized by high consumption of processed snacks, sports beverages, and convenience meals that heavily utilize Maltodextrin and Fructose. The market is bolstered by an innovation-centric ecosystem where companies like Ingredion Incorporated and ADM are pioneering the use of wheat derivatives in "Keto" and "Low-Glycemic" food formulations.

Regulatory frameworks, particularly those established by the U.S. Food and Drug Administration (FDA), have paved the way for the adoption of modified wheat starches in clean-label applications. Additionally, the region's focus on sustainable agricultural practices and the integration of AI in crop management are helping to stabilize the supply chain. The growing trend of "on-the-go" nutrition and the presence of major global beverage players ensure that North America remains a high-value market, with a strong emphasis on high-purity, high-functionality derivatives for both domestic consumption and export.

Europe Wheat Starch Derivatives Market Trends and Insights

Europe is the leading regional market, holding a 36% market share in 2025. This dominance is the result of a long-standing tradition of wheat cultivation and a highly integrated bio-economy. Countries like Germany, France, and the United Kingdom are hubs for starch processing, supported by the Common Agricultural Policy (CAP) which encourages value-added grain processing. The region is a global leader in regulatory harmonization, with the European Food Safety Authority (EFSA) providing clear guidelines that have fostered consumer trust in starch-based additives.

Innovation in Europe is currently focused on the "Green Deal" and circular economy initiatives. European manufacturers like Roquette Frères and Agrana Beteiligungs-AG are leading the transition toward carbon-neutral production and the development of wheat-based bioplastics. The demand for non-GMO wheat derivatives is exceptionally high in Europe, as consumers prioritize sustainability and ethical sourcing. This regional market is also characterized by a high penetration of functional bakery products, where wheat starch is essential for gluten-reduced and gluten-free formulations, maintaining its top-tier status globally.

Asia Pacific Wheat Starch Derivatives Market Trends and Insights

Asia Pacific is the fastest-growing region in the Wheat Starch Derivatives Market, fueled by rapid urbanization and the expansion of the middle class in China, India, and ASEAN countries. As dietary habits shift toward Westernized patterns, the consumption of baked goods, confectionery, and processed meats is skyrocketing. China, in particular, has emerged as a manufacturing powerhouse, leveraging domestic wheat production and advanced processing technologies to meet the growing internal and regional demand for Glucose Syrups and Dextrose.

The region's growth is further accelerated by the "Make in India" initiative and similar policies in Southeast Asia, which encourage the establishment of local food processing units. The cost-competitiveness of manufacturing in Asia Pacific makes it an attractive destination for global players seeking to optimize their supply chains. Furthermore, the rising awareness of health and wellness is driving a surge in the pharmaceutical and nutraceutical sectors in Japan and South Korea, where wheat starch derivatives are increasingly used in traditional and modern medicine formulations. This dynamic environment positions Asia Pacific as the primary engine of market volume growth through 2033.

Market Competitive Landscape

The Wheat Starch Derivatives Market is characterized by a consolidated structure, where the top five players control more than 50% of the total market share. This concentration is due to the high capital intensity required for industrial-scale wheat milling and starch modification. Leading companies like Cargill, Incorporated, ADM, and Ingredion Incorporated leverage their global reach and vertical integration from grain sourcing to specialized chemical modification to maintain dominance. Strategic growth is currently driven by Research and Development (R&D) focused on "specialty starches" that offer unique functional benefits, such as high-temperature stability or specific gelling textures. Emerging business models are increasingly focusing on sustainability, with companies investing in traceable supply chains and water-efficient processing technologies to differentiate themselves in a competitive landscape.

Key Developments:

In June 2025, AGRANA and INGREDION received full regulatory clearance for their planned joint venture from all relevant international authorities, including approval from the European antitrust regulator.

Companies Covered in Wheat Starch Derivatives Market

- Cargill, Incorporated

- ADM

- Ingredion Incorporated

- Roquette Frères

- Südzucker AG

- Agrana Beteiligungs-AG

- Tate & Lyle PLC

- Manildra Group

- Tereos Group

- Others

Frequently Asked Questions

The global market is expected to reach a valuation of US$ 4.8 billion by 2026, following a period of steady recovery and growth in the processed food and industrial sectors.

The leading driver is the global consumer shift toward Clean-Label and plant-based ingredients, which has prompted food manufacturers to replace synthetic additives with natural wheat-derived texturizers and stabilizers.

Europe leads the market with a 36% share in 2025, owing to its advanced agricultural infrastructure, high demand for non-GMO ingredients, and a strong presence of key industry players like Roquette and Tereos.

The expansion of the Plant-Based Meat sector and the rising demand for Biodegradable Packaging represent the most lucrative opportunities for market participants to diversify their revenue streams.

The market is dominated by global agribusiness and ingredient giants including Cargill, Incorporated, ADM, Ingredion Incorporated, Roquette Frères, and Tate & Lyle PLC.