- Animal Feed & Additives

- Wheat Middling Market

Wheat Middling Market Size, Share, and Growth Forecast, 2026 - 2033

Wheat Middling Market by Application (Animal Feed, Pet Food, Food & Beverages, Pharmaceutical, Cosmetics & Personal Care), Animal (Ruminants, Poultry, Swine, Cattle), Source (Conventional, Organic), and Regional Analysis for 2026 - 2033

Wheat Middling Market Share and Trends Analysis

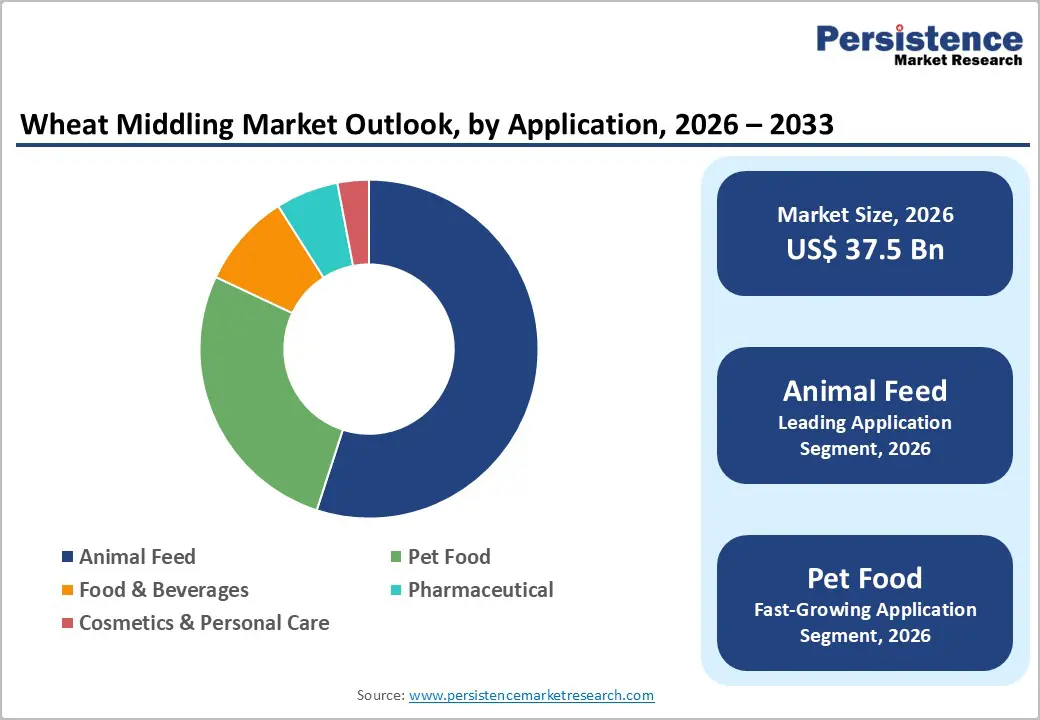

The global wheat middling market size is likely to be valued at US$ 37.5 billion in 2026, and is projected to reach US$ 51.0 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026 - 2033.

The livestock sector is driving this progression as producers scale up operations to meet surging protein demand from rising meat consumption worldwide. Feed formulators have increasingly incorporated this byproduct for its cost advantage, delivering essential protein and fiber without inflating formulation costs. Managers optimizing ingredient mixes have discovered reliable performance when blending wheat middlings with grains and pellets, sustaining animal growth while preserving profit margins.

Sustainable farming initiatives have amplified this ingredient's appeal by converting milling residues into valuable resources rather than waste streams. Processors have aligned with circular economy principles, reducing disposal expenses and enhancing environmental credentials for premium feed brands. Facilities evaluating supply strategies will have fortified resilience by securing consistent volumes from integrated millers who prioritize quality grading and traceability.

Key Industry Highlights

- Leading Application: Animal feed is slated to dominate with an estimated 2026 share of 55%, owing to the established role of wheat middling as a cost-effective source of energy and fiber in ruminant, swine, and poultry diets.

- Fastest-growing Source: Organic is anticipated to be the fastest-growing segment through 2033, driven by stringent retailer requirements for certified supply chains.

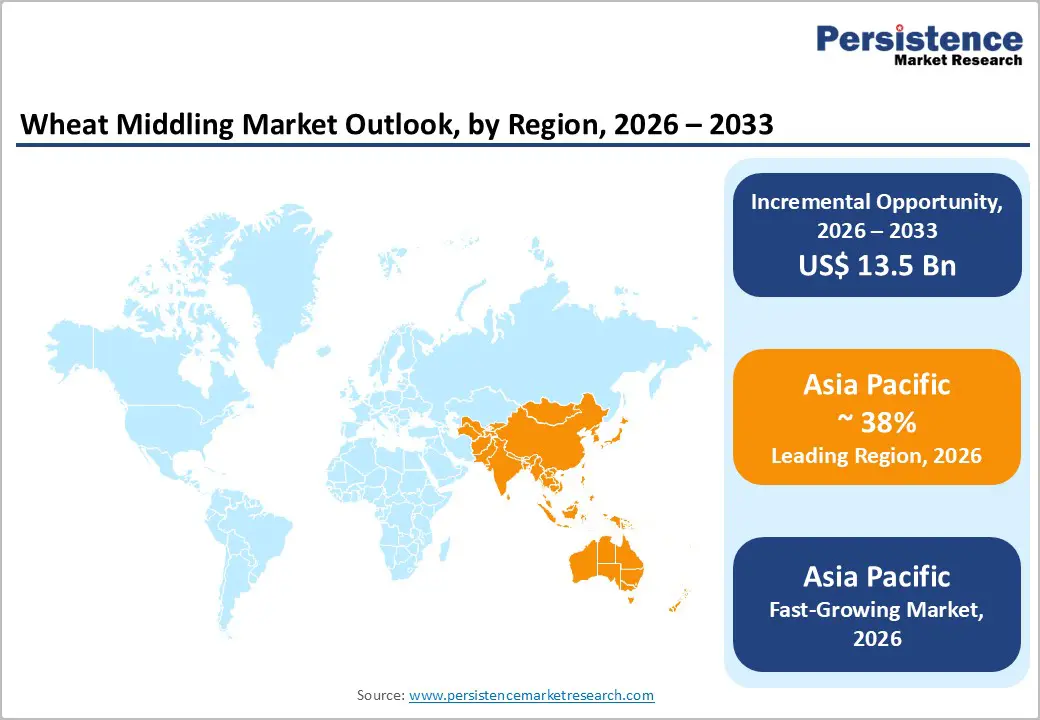

- Dominant Region: Asia Pacific market is expected to command about 38% market share in 2026, supported by rapid growth in livestock and feed production in major economies.

- Fastest-growing Regional Market: Asia Pacific is set to be the fastest-growing market through 2033 due to ongoing investment in milling and feed manufacturing infrastructure.

| Key Insights | Details |

|---|---|

| Wheat Middling Market Size (2026E) | US$ 37.5 Bn |

| Market Value Forecast (2033F) | US$ 51.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Global Livestock Production and Meat Consumption

Global meat production continues to expand, with the Food and Agriculture Organization (FAO) estimating output at about 371 million tons in 2023, reflecting a clear upward trend in animal protein demand. This growth directly increases the need for nutritionally efficient and affordable feed ingredients, particularly in cost-sensitive markets. Wheat middlings, with typical protein content in the 15-18% range and a useful mineral and vitamin profile, provide feed formulators with a practical way to partially replace more expensive grains or oilseed meals while maintaining ration quality. As producers in both intensive and semi-intensive systems reconsider diet structures, incorporating wheat middlings can support more resilient cost structures without compromising animal performance.

The United States Department of Agriculture (USDA) points to the continued expansion of livestock herds and flocks in developing regions, particularly in the Asia Pacific, where rising incomes and urbanization drive dietary shifts toward higher meat and dairy consumption. In this context, wheat middlings become strategically relevant for integrated feed companies and on-farm mixers seeking to optimize feed conversion ratios and stabilize margins. By aligning wheat middlings usage with precise formulation strategies, producers can improve gut health, support consistent growth, and reduce reliance on premium ingredients such as soybean meal. This positions wheat middlings not only as a low-cost filler but as part of a deliberate feed strategy that balances nutrition, economics, and long-term competitiveness in expanding protein markets.

Competition from Alternative Feed Ingredients and By-Products

The animal feed industry relies on a broad portfolio of ingredients, such as rice bran, corn gluten meal, soybean meal, and other cereal by-products, each offering distinct nutritional benefits and pricing implications. These options drive constant comparison with wheat middlings as nutritionists assess protein quality, fiber levels, palatability, and supply reliability before finalizing formulations. In higher-performance diets for poultry or young animals, many formulators prefer soybean meal because of its superior amino acid profile, even when it requires a higher investment. In regions where specific crops dominate, such as rice in many Asian markets, local by-products often gain an advantage because they reduce logistics costs and simplify sourcing.

Advances in feed formulation software enable nutritionists to model multiple-ingredient scenarios in real time and adjust recipes as market conditions change. This capability helps feed manufacturers design blends that balance nutritional objectives with margin targets, rather than depending heavily on any single raw material. Synthetic amino acids and specialized additives now complement or partially replace traditional protein sources in some rations, particularly where precision nutrition or tighter environmental controls are priorities. For stakeholders in the wheat middlings value chain, a strategic response involves positioning middlings as part of flexible, cost-effective formulations, supported by transparent data on digestibility, consistency, and compatibility with evolving ingredient strategies.

Expansion of Organic and Non-GMO Animal Product Markets

Consumer demand for organic and non-genetically modified organism (non-GMO) animal products continues to build across mature retail and food service channels, with industry bodies such as the Organic Trade Association consistently highlighting growth in organic meat and dairy categories. This trend creates clear opportunities for wheat middlings produced from certified organic and non-genetically modified (non-GM) wheat, particularly where retailers and processors want feed inputs to support on-pack sustainability and origin claims. Livestock producers targeting premium customer segments increasingly require documented compliance across their feed supply chains to justify higher product prices and strengthen brand positioning. For these buyers, the value proposition extends beyond cost per ton and includes certification integrity, traceability, and alignment with retailer procurement policies.

For wheat millers and feed manufacturers, this environment supports a strategic shift toward developing and promoting dedicated organic and non-GMO wheat middlings product lines. By segregating raw materials, tightening quality control, and obtaining recognized certifications, suppliers can access specialized channels where customers focus more on reliability, transparency, and partnership than on short-term price alone. As regulations for organic livestock production continue to mature in regions such as North America and Europe, demand for compliant feed inputs is likely to become more structured, with a greater share managed through long-term contracts rather than spot purchases. In this context, certified wheat middlings can become a core component of premium feed portfolios, supporting longer-term supply agreements, improving customer retention, and reinforcing the sustainability narratives of integrated meat and dairy value chains.

Category-wise Analysis

Application Insights

Animal feed is slated to maintain a dominant position in 2026, with an estimated revenue share of 55%. This leadership position reflects the well-known role of wheat middling as a cost-effective source of energy and fiber in ruminant, swine, and poultry diets. The segment continues to benefit from the ongoing expansion of the livestock sector and rising commercial feed production capacity across major producing regions. Feed manufacturers value wheat middlings for their digestibility, palatability, and contribution to pellet durability, while also using them to lower overall formulation costs compared with higher-priced protein ingredients.

Pet food is likely to be the fastest-growing segment during the 2026 - 2033 forecast period. Rising pet ownership rates globally, particularly in emerging Asian markets, and premiumization trends in pet nutrition drive this accelerated growth. Pet food manufacturers increasingly incorporate wheat middlings as a fiber source to support digestive health and satiety in weight management formulations. The humanization of pet care encourages natural ingredient preferences, positioning wheat middlings favorably as recognizable, whole-food components. Premium and super-premium pet food brands leverage the nutritional benefits of wheat middling to market clean-label products that appeal to health-conscious pet owners.

Animal Insights

Ruminants are slated to hold the highest revenue share, estimated to reach 45% in 2026. Ruminants can use the fiber in wheat middlings particularly efficiently, which helps support healthy rumen function and consistent animal performance. Dairy producers rely on wheat middlings as a cost-effective energy source in balanced rations, allowing them to manage feed costs while sustaining target productivity levels. Established feeding practices and a strong base of nutritional research reinforce this role and help maintain the ruminant segment’s leading position. Demand remains especially strong in dairy-intensive regions, and it generally follows broader livestock expansion, creating relatively stable volumes and supporting long-term supply relationships between millers and feed manufacturers.

Poultry is expected to be the fastest-growing segment over the 2026 - 2033 period. Rising global poultry meat consumption, driven by affordability, cultural acceptance, and short production cycles, underpins the growing role of wheat middlings in this segment. Modern broiler and layer feeding programs include wheat middlings at carefully controlled levels to balance cost management with growth, feed efficiency, and carcass quality objectives. Properly formulated diets use wheat middlings as one component within a broader ingredient mix, rather than relying on them as a single dominant input, which helps maintain nutritional consistency across flocks.

Source Insights

The conventional segment is foreseen to lead with an approximate 33.4% market revenue share in 2026. Conventional wheat middlings, produced from standard commercial wheat varieties using traditional milling processes, account for most of the available supply and form the core of the global market. Their predominance reflects how widely conventional wheat is grown, the breadth of existing milling capacity, and the strength of long-established supply links between millers and feed manufacturers. These provide predictable nutritional profiles, dependable availability, and competitive pricing that suit mainstream livestock and poultry operations, which tend to prioritize cost efficiency over premium positioning.

Organic is anticipated to be the fastest-growing segment between 2026 and 2033. Organic and wheat middlings occupy a relatively small but rapidly expanding niche within the market, driven by the growth of organic livestock systems, stronger retailer requirements for certified supply chains, and rising consumer interest in verified production claims. Limited organic wheat acreage and the need for dedicated, accredited milling infrastructure constrain supply, which supports significant price premiums over conventional products and encourages long-term contracting between buyers and qualified suppliers. For feed manufacturers and millers, this segment offers attractive margin potential but requires disciplined segregation, documentation, and compliance management across the value chain.

Regional Insights

Asia Pacific Wheat Middling Market Trends

Asia Pacific market is likely to be the fastest-growing and leading regional market with a projected 38% of the wheat middling market share in 2026. Rapid growth in livestock and increasing feed production in major economies such as China, India, and key ASEAN members are factors favoring the regional market. China’s transition from traditional smallholder farming to large, integrated commercial operations is increasing the need for standardized and nutritionally consistent feed ingredients, which strengthens demand for wheat middlings in industrial feed formulations. In India, the expansion of the dairy and poultry sectors, along with initiatives from institutions such as the National Dairy Development Board that promote scientifically formulated rations, reinforces the use of wheat middlings in compound feeds.

ASEAN countries, including Vietnam, Thailand, Indonesia, and the Philippines, are adding further momentum as rising incomes, urbanization, and evolving dietary patterns drive higher meat consumption and encourage investment in modern livestock production and feed milling capacity. The Asia Pacific market also benefits from several structural advantages. Large wheat-producing countries such as China, India and Australia provide a strong raw material base. At the same time, ongoing investment in milling and feed manufacturing infrastructure steadily improves the availability of wheat middlings for both domestic and export use. Lower labor costs and improving logistics contribute to competitive delivered costs into regional and selected export markets, which positions Asia Pacific suppliers as credible alternatives to more established origins.

Europe Wheat Middling Market Trends

Europe plays a central role in the market for wheat middlings, bolstered by a large milling base, high livestock density, and a mature regulatory environment that provides structure and predictability. Key producers such as Germany, France, Spain, and the United Kingdom anchor regional demand through extensive wheat cultivation, developed flour milling industries, and sizable dairy and swine sectors. Germany benefits from concentrated milling capacity in major wheat-growing regions and a substantial commercial livestock base. At the same time, France’s position as the European Union (EU) wheat leader supports reliable availability of middlings for domestic feed users and nearby export destinations. This combination of scale, infrastructure, and demand underpins steady, moderate growth that closely follows broader livestock and compound feed trends rather than rapid expansion.

Regulation and sustainability are defining features of the European market and shape both risks and opportunities for wheat middling suppliers. The European Food Safety Authority (EFSA) and EU feed legislation impose strict requirements on contaminants, traceability, and labelling, which increase compliance costs but also strengthen confidence among feed manufacturers, retailers, and end users. Harmonized rules support intra-EU trade and reduce non-tariff barriers, making cross-border sourcing of wheat middlings more predictable and easier to manage within integrated supply networks. Policy frameworks such as the Common Agricultural Policy (CAP), the European Green Deal, and the Farm to Fork Strategy promote circular economy principles and better use of milling by-products, positioning wheat middlings as an environmentally credible feed ingredient that helps address carbon and waste reduction objectives.

North America Wheat Middling Market Trends

North America is a core demand center for wheat middlings, supported by a large, efficient wheat milling base and highly industrialized livestock and feed sectors. The United States drives most regional consumption through substantial milling capacity in major wheat-producing states such as Kansas, North Dakota, and Montana, and through the scale of its beef and dairy industries, which depend on consistent, energy-dense by-products in ration formulation. Close proximity between grain-growing regions, mills, and feed manufacturers reduces logistics complexity and supports reliable supply into commercial feedlots and dairy operations. Canada provides a complementary contribution, with prairie wheat production feeding domestic milling and supporting cattle, dairy, and other livestock systems that rely on structured and well-organized feed markets.

The regulatory and technical environment in North America further enhances the strategic role of wheat middlings in feed strategies. Oversight from federal agencies and industry bodies, including feed ingredient definition frameworks and safety standards, supports product consistency, facilitates interstate trade, and underpins export credibility. Advanced formulation practices, supported by nutrition software and precision feeding approaches, enable feed manufacturers to fine-tune wheat middling inclusion rates to balance cost control with performance, while emerging applications in pet food and organic or specialty livestock programs expand the addressable market.

Competitive Landscape

The global wheat middling market structure showcases moderate fragmentation, with influence concentrated among large participants such as Archer Daniels Midland Company, Cargill, Incorporated, Bunge Limited, Ardent Mills, and Grain Millers, Inc. This pattern has been arising because wheat middlings have been produced as a by-product of flour milling rather than through dedicated assets, so available volumes have been tied closely to overall wheat processing activity. As a result, the most impactful suppliers have been integrated agribusiness groups and major milling companies that have maintained multi-regional footprints and long-standing relationships with leading feed manufacturers. For strategy planning, stakeholders have been benefiting from viewing this segment as part of a broader grain value chain rather than as an isolated commodity, since control over milling capacity has been directly shaping bargaining power in wheat middlings.

Competitive positioning has been differing based on scale, customer focus, and service model. Global players have been leveraging extensive product portfolios, nutrition expertise, and cross-border logistics capabilities to serve multinational feed producers and export-oriented channels, which has been allowing them to integrate wheat middlings into comprehensive feed ingredient offerings. Regional and local specialists have been concentrating on proximity, fast response, and flexible delivery terms that align with the operational needs of nearby feed mills, so they have often been winning business on speed and adaptability rather than brand recognition. Although direct product differentiation has remained limited, suppliers have been able to secure advantage through consistent quality, reliable supply, and strong technical support, and those that invest in these areas will have strengthened customer loyalty and justified modest pricing premiums where performance and continuity of supply are critical to feed formulators.

Key Industry Development

- In September 2025, Archer-Daniels-Midland and Alltech announced plans of forming a North American animal feed joint venture. Alltech will contribute its Hubbard Feeds (18 U.S. mills) and Masterfeeds (15 Canadian mills) operations, while ADM will add its 11 U.S. feed mills to create an industry-leading portfolio serving livestock, equine, and leisure animal markets.

- In July 2025, Bunge Global SA finalized its long-delayed merger with Glencore-backed grain handler Viterra, closing a roughly US$ 34 billion deal first announced two years earlier that creates a new powerhouse in global crop trading and processing.

- In May 2025, Romer Labs introduced the USDA-approved DON WATEX® Kit, which uses a water-based extraction method for accurate quantitative detection of deoxynivalenol (DON) in wheat and corn. Approved wheat matrices for use with the test kit include whole grain wheat flour, wheat middlings, wheat red dog flour, and wheat screenings.

Companies Covered in Wheat Middling Market

- Archer Daniels Midland Company

- Cargill, Incorporated

- Bunge Limited

- General Mills, Inc.

- Ardent Mills

- Associated British Foods plc

- Grain Millers, Inc.

- Wilmar International Limited

- ConAgra Brands, Inc.

- Bay State Milling Company

- Siemer Milling Company

- Hodgson Mill, Inc.

- Cereal Food Processors

- Didion Milling, Inc.

Frequently Asked Questions

The global wheat middling market is projected to reach US$ 37.5 billion in 2026.

The market is primarily driven by expanding global livestock and poultry production, coupled with the need for cost-effective, nutritionally reliable feed ingredients.

The market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Growth in organic and specialty livestock systems, pet nutrition, and emerging applications in insect farming and sustainable feed formulations that favor traceable, value-added by-products can generate massive opportunities.

Archer Daniels Midland Company, Cargill, Incorporated, Bunge Limited, Ardent Mills and Grain Millers, Inc. are some of the key players in the market.