- Food Ingredients & Additives

- Vacuum Salt Market

Vacuum Salt Market Size, Share, and Growth Forecast 2026 - 2033

Vacuum Salt Market by Form (Granular, Fine, Briquette), Application (Water Softeners & Water Treatment, De-icing, Anticaking, Flavouring Agents, Others), End-user (Households, Industrial), and Regional Analysis, 2026 - 2033

Vacuum Salt Market Size and Trend Analysis

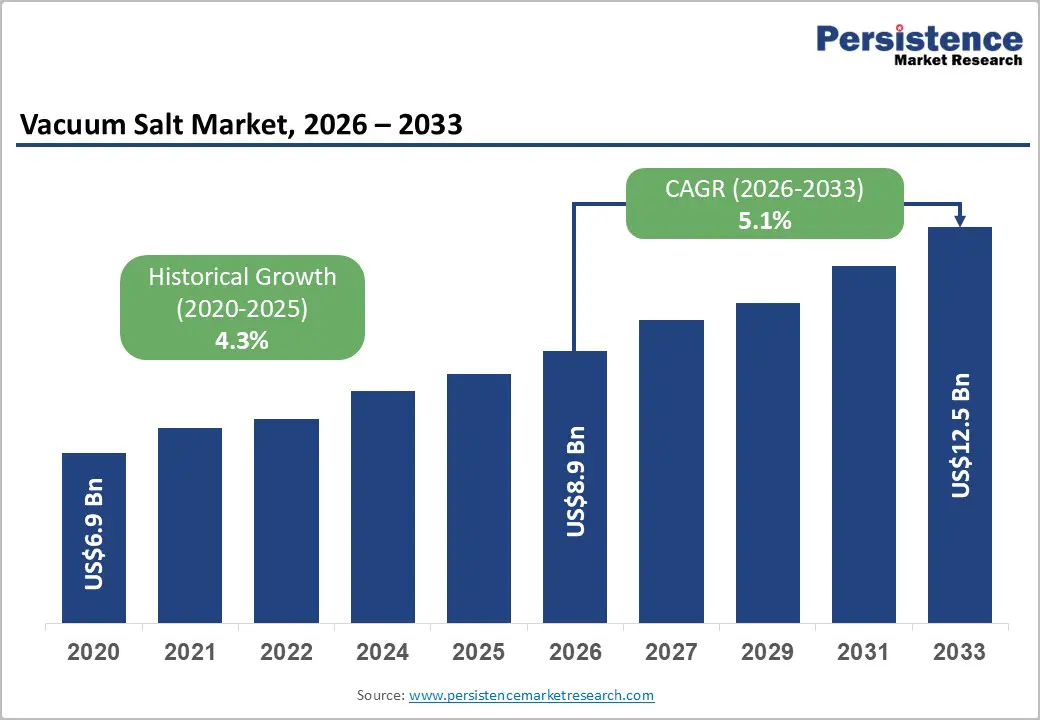

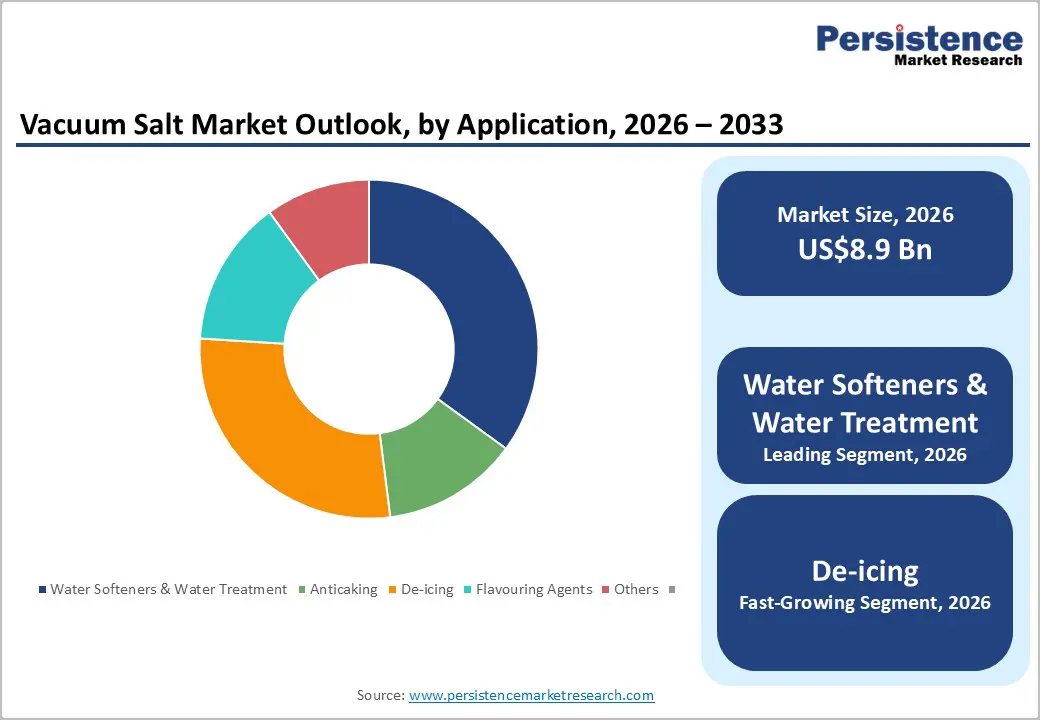

The global vacuum salt market size is expected to be valued at US$ 8.9 billion in 2026 and projected to reach US$ 12.5 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

The global market is witnessing steady growth, driven by increasing demand for high-purity salt across food, industrial, and household applications. Vacuum salt is produced through the vacuum evaporation process, ensuring superior quality, safety, and consistent purity compared to conventional salt production methods. It plays a critical role in the food and beverage industry as a flavoring agent that enhances taste and product stability. Rising consumer awareness regarding health and preference for cleaner, safer ingredients is further accelerating demand. Additionally, food manufacturers increasingly prefer vacuum salt due to its high sodium chloride content and low impurities. Expanding applications in water treatment, pharmaceuticals, and chemicals are also contributing to the market’s overall growth trajectory.

Key Industry Highlights:

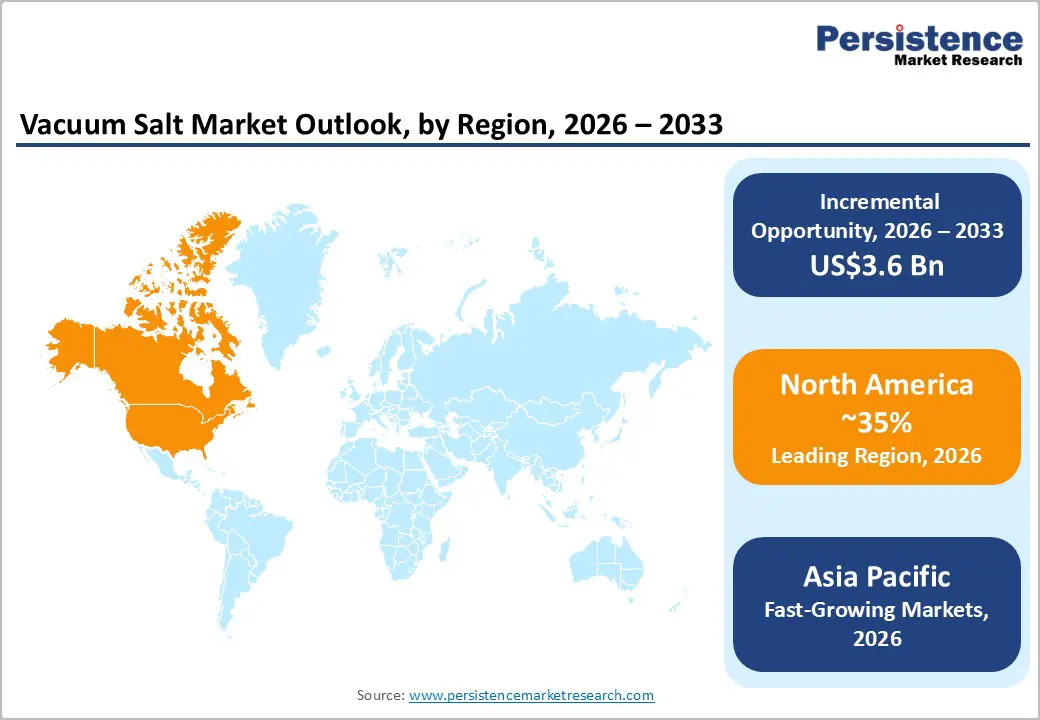

- North America leads the vacuum salt market with ~35% share in 2025, supported by strong chemical demand, de-icing applications, and established infrastructure.

- Asia Pacific is the fastest-growing region, driven by industrialization, chemical and textile expansion, and rising investments in water treatment across China, India, and ASEAN.

- By form, granular vacuum salt dominates with ~57% share in 2025 due to extensive use in water softening, industrial processes, and select food applications.

- Water treatment and de-icing are key applications, with strong demand in North America and increasing adoption of high-purity vacuum salt in specialized usage areas.

- Opportunities lie in food- and pharma-grade salts and Asia Pacific growth, where high-purity products support regulatory compliance, efficiency improvements, and longer equipment lifespans.

| Key Insights | Details |

|---|---|

| Vacuum Salt Market Size (2026E) | US$ 8.9 billion |

| Market Value Forecast (2033F) | US$ 12.5 billion |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.3% |

Market Dynamics

Drivers - Rising Demand from Chemical Industry to Boost Sales

The chemical industry is one of the largest consumers of salt, accounting for a significant share of global demand due to its role as a critical raw material. High chemical purity is essential for processes such as chlor-alkali production, where salt is used to manufacture chlorine, caustic soda, and soda ash. Vacuum salt, with its superior purity levels (≥99.8-99.9% NaCl), low impurities, and high solubility, is highly preferred in these applications. Its consistent composition ensures efficient chemical reactions, reduces equipment corrosion, and improves overall process reliability, making it indispensable for modern chemical manufacturing.

In addition, the growing production of specialty chemicals such as fluorinated compounds, antimicrobials, flame retardants, organic solvents, and certain metals is further driving demand for high-quality salt inputs. Manufacturers are increasingly prioritizing vacuum salt to meet stringent quality and regulatory standards while optimizing operational efficiency. As global chemical output continues to expand, particularly in emerging markets, vacuum salt producers are strategically targeting this sector to strengthen their market position and capture higher-value opportunities.

Preference for Use in Animal Feed Production to Propel Market Growth

Salt plays a vital role in animal nutrition, supporting essential biological functions such as nerve transmission, digestion, and metabolic balance. Traditionally, low-cost salts like rock salt have been used in feed production; however, these often contain impurities that can impact animal health and productivity. With increasing regulatory scrutiny and a growing focus on feed quality, manufacturers are shifting toward high-purity ingredients. Vacuum salt, known for its consistent composition and minimal contaminants, is gaining traction as a reliable input for premium animal feed formulations.

This trend is particularly evident in ruminant nutrition, where sodium intake is critical for maintaining optimal milk production and overall livestock performance. As the demand for high-quality dairy and meat products rises globally, feed producers are under pressure to enhance feed efficiency and nutritional outcomes. The adoption of vacuum salt enables manufacturers to differentiate their products in a competitive market while meeting stricter quality standards. Consequently, the increasing preference for high-grade feed ingredients is expected to significantly contribute to the growth of the vacuum salt market.

Restraints - Seasonality of De-icing Products to Hinder Market Growth

The de-icing segment represents a significant yet highly seasonal application of salt, and it is largely dominated by low-cost rock or mined salt due to its affordability and widespread availability. Vacuum salt, being relatively more expensive, is typically used only in specific situations where higher purity or performance is required. As a result, its penetration in the de-icing market remains limited and dependent on exceptional conditions such as severe winter storms or supply shortages of conventional salt. This cost sensitivity restricts the consistent demand for vacuum salt in this segment.

Moreover, the increasing impact of climate change has led to unpredictable and often milder winter conditions across many regions, particularly in North America and Europe. Reduced frequency and intensity of snowfall directly affect the demand for de-icing salts, creating volatility in consumption patterns. This uncertainty makes it challenging for manufacturers to rely on the de-icing sector as a stable revenue stream. Consequently, the seasonal and climate-dependent nature of this application acts as a key restraint, limiting the steady growth potential of the vacuum salt market.

Opportunities - Fast-Growing Demand for Fine Vacuum Salt in High-Value Food and Pharma Applications

Fine-grained vacuum salt is emerging as a significant opportunity in the market, driven by increasing demand from food processors and pharmaceutical manufacturers for high-purity, precisely specified ingredients. With purity levels of ≥99.8-99.9% NaCl, fine vacuum salt offers superior flowability, uniform particle size, and residue-free solubility. These properties are essential in applications such as bakery products, cheese processing, meat curing, snack seasonings, and ready-to-eat meals, where consistency and quality directly impact product performance. As regulatory standards tighten globally, manufacturers are shifting toward premium-grade inputs to ensure compliance and maintain product integrity.

In addition, the growing trend of premiumization and clean-label products is encouraging the adoption of high-quality salt across developed and emerging markets. Leading producers are focusing on expanding applications in dairy, soups, dressings, and processed meat products to align with evolving consumer preferences. With rising global processed food consumption and increasing export requirements, fine vacuum salt is positioned as the fastest-growing form segment. It enables manufacturers to achieve functional benefits while enhancing product quality, thereby unlocking higher-value growth opportunities in both food and pharmaceutical sectors.

Category-wise Analysis

Form Insights

Within the vacuum salt market, the Granular form segment accounts for around 57% of total revenues in 2025, making it the clear leader due to its versatility and suitability for water softening, industrial brine preparation, and certain food applications. Granular and tabletized vacuum salts are heavily used in ion-exchange water softeners, where controlled grain size and low fines ensure efficient brine formation and reliable resin regeneration. Producers such as K+S and specialist PDV suppliers highlight granular PDV salt as a core product for both general industrial usage and water treatment, reflecting its role as a workhorse grade across sectors. While fine and briquetted formats are important for specific niches, the dominance of granular vacuum salt is reinforced by its broad compatibility with dosing systems, silo handling, and bulk logistics in high-volume applications.

End-user Insights

Across end users, the Industrial and Chemicals segments together account for the largest share of vacuum salt consumption, reflecting the critical role of high-purity sodium chloride as a feedstock in chlor-alkali, detergents, pulp and paper, textiles, and other process industries. Evaporated and vacuum salts supplied by companies such as CIECH S.A., K+S, and Tata Chemicals Europe (British Salt) are widely used in electrolysis, soda ash production, and other heavy chemical processes where impurities can affect yields and equipment life. At the same time, food and pharmaceutical end users represent a rapidly expanding demand base for food-grade and technical-grade vacuum salt, as noted by European producers and specialty suppliers of ≥99.8-99.9% NaCl products. As processed food manufacturing and pharma production capacity increase in emerging markets, the industrial and chemical segment is expected to retain leadership in absolute volume, while food and pharmaceutical uses exhibit some of the fastest growth rates.

Regional Insights

North America Vacuum Salt Market Trends and Insights

North America holds a leading position in the global vacuum salt market, accounting for approximately 35% of total revenues in 2025. This dominance is supported by a strong base of chemical manufacturing, extensive winter road infrastructure, and widespread adoption of residential and industrial water softening systems. The region remains one of the largest salt producers globally, with key production concentrated in multiple states, supplying both bulk salt and high-purity vacuum salt for specialized applications. A considerable portion of domestic salt production is further processed into evaporated and vacuum salts to cater to higher-value industries such as chemicals, food processing, and water treatment.

De-icing represents a major share of total salt consumption in the region, while chemical manufacturing, food processing, and water treatment collectively contribute to steady demand for vacuum salt. Market players focus on supplying high-purity grades that meet stringent standards for performance and safety. Additionally, a mature ecosystem characterized by advanced processing technologies, efficient logistics, and product innovation supports sustained value growth, even as overall volume growth remains relatively stable.

Europe Vacuum Salt Market Trends and Insights

Europe represents a well-established market for vacuum salt, supported by a long history of brine extraction and advanced crystallization technologies. Countries such as Germany, Poland, Austria, Spain, and the United Kingdom serve as key production hubs, supplying a diverse range of vacuum salt products across industries. These salts, often reaching purity levels of up to 99.9% NaCl, are widely used in food processing, water treatment, chemical manufacturing, de-icing, and animal feed applications. The region’s strong emphasis on quality and safety standards ensures consistent demand for high-purity vacuum salt in sectors such as dairy, meat processing, bakery, and convenience foods.

Regulatory frameworks under European Union legislation play a crucial role in shaping the market, influencing product specifications, environmental practices, and end-use applications. Increasing focus on sustainability and environmental impact, particularly related to de-icing and industrial processes, is driving investments in energy-efficient production technologies and improved brine management systems. At the same time, growing consumer demand for clean-label and traceable ingredients is encouraging food manufacturers to adopt premium-grade vacuum salt, supporting stable growth across major European markets.

Asia Pacific Vacuum Salt Market Trends and Insights

Asia Pacific is the fastest-growing region in the global vacuum salt market, driven by rapid industrialization, expanding chemical and textile industries, and increasing investments in water treatment infrastructure. Countries such as China, India, and those in Southeast Asia are witnessing strong growth in demand for high-purity salt used in industrial applications, including chlor-alkali production, detergents, dyeing, and other chemical processes. The region also benefits from large-scale salt production, with China leading global output and several countries enhancing their refining capabilities to meet rising domestic and export demand.

In addition to industrial growth, increasing urbanization and rising disposable incomes are fueling demand for processed and packaged food products, which require high-quality vacuum salt for consistency and safety. Producers are expanding their offerings to cater to food processing, personal care, and water treatment applications, leveraging the superior purity and functional properties of vacuum salt. With ongoing investments in production capacity and infrastructure development, the region is expected to record the highest growth rate, making it a key focus area for market expansion and future opportunities.

Competitive Landscape

The global vacuum salt market is moderately consolidated, with multinational corporations accounting for approximately 40-45% of total market share. Leading players focus on expanding their presence among global food manufacturers, driven by increasing demand in emerging and non-traditional markets. Companies are also strengthening their portfolios through strategic partnerships and capacity expansions. For instance, under its Shaping 2030 strategy, K+S Aktiengesellschaft entered into an agreement with an Australia-based salt producer to procure up to 90,000 tons annually of specialty fertilizer potassium sulfate (SOP). This move supports portfolio diversification and enhances supply capabilities alongside its existing production base.

Key Developments:

- In September 2025, CIECH S.A. expanded its evaporated salt production capacity in Europe to meet growing demand from food processing and water treatment sectors.

- In February 2026, the Board of Directors of Tata Chemicals approved the establishment of a greenfield manufacturing facility in Valinokkam, Ramanathapuram district, Tamil Nadu, for the production of iodised vacuum salt dried (IVSD).

Companies Covered in Vacuum Salt Market

- K+S Aktiengesellschaft

- CIECH S.A.

- Tata Chemicals Ltd.

- AkzoNobel N.V.

- Suedwestdeutsche Salzwerke AG

- INEOS Group Limited

- Dominion Salt Limited

- Cerebos Ltd

- Cheetham Salt Group

- ACI Limited

- WA Salt Group

- Infosa

- Nirma Limited

- Zoutman NV

- Others

Frequently Asked Questions

The global vacuum salt market is expected to reach around US$ 8.9 billion in 2026.

Demand is driven by rising use of high-purity vacuum salt in water treatment, chlor-alkali processes, and growing food and pharmaceutical applications requiring stringent purity and safety standards.

North America leads the vacuum salt market with around 35% share, supported by strong chemical industry demand, de-icing needs, and widespread adoption of water softening systems.

Key opportunities lie in food- and pharma-grade fine vacuum salts and Asia-Pacific markets, driven by industrial expansion, water treatment demand, and need for high-purity, efficient processing inputs.

The top 5 players such as Tata Chemicals, AkzoNobel N.V., CIECH S.A., K + S Aktiengesellschaft, and INEOS Group Ltd. hold close to 80% of the market share.