- Industrial Machinery

- Liquid Ring Vacuum Pump Market

Liquid Ring Vacuum Pump Market Size, Share, and Growth Forecast for 2025 - 2032

Liquid Ring Vacuum Pump Market By Product Type (Single Stage Pump, Others), Material Type (Stainless Steel, Cast Iron, Others), Flowrates (25–600 m³/h, Others), End-user Industry (Chemical & Petrochemical, Others), and Regional Analysis 2025 - 2032

Liquid Ring Vacuum Pump Market Size and Trends Analysis

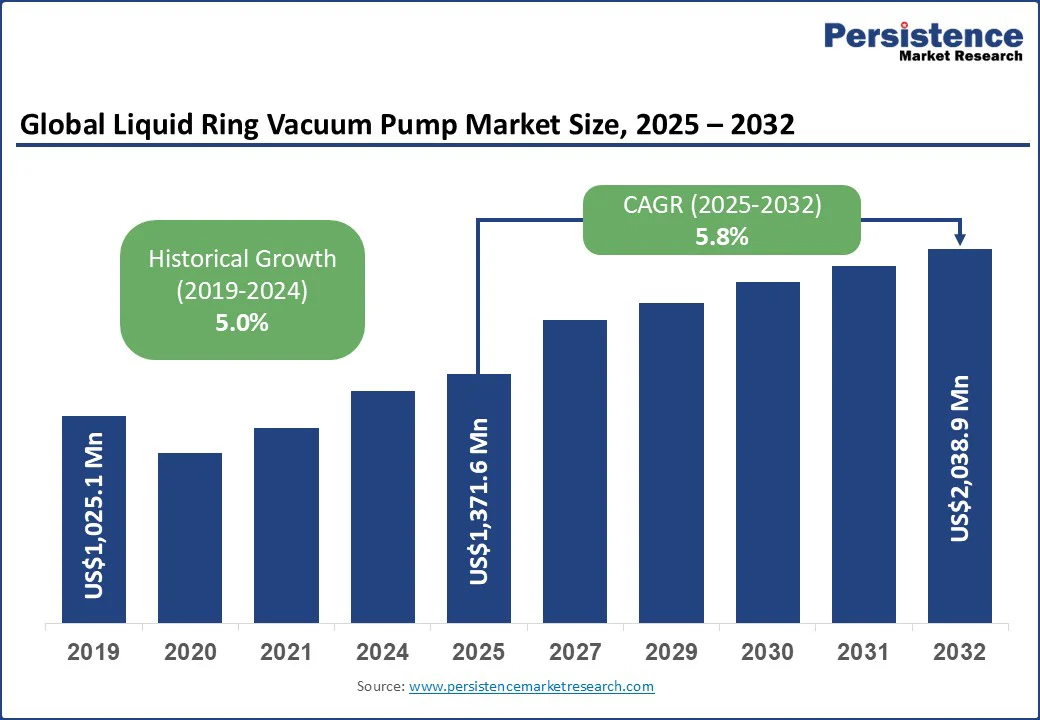

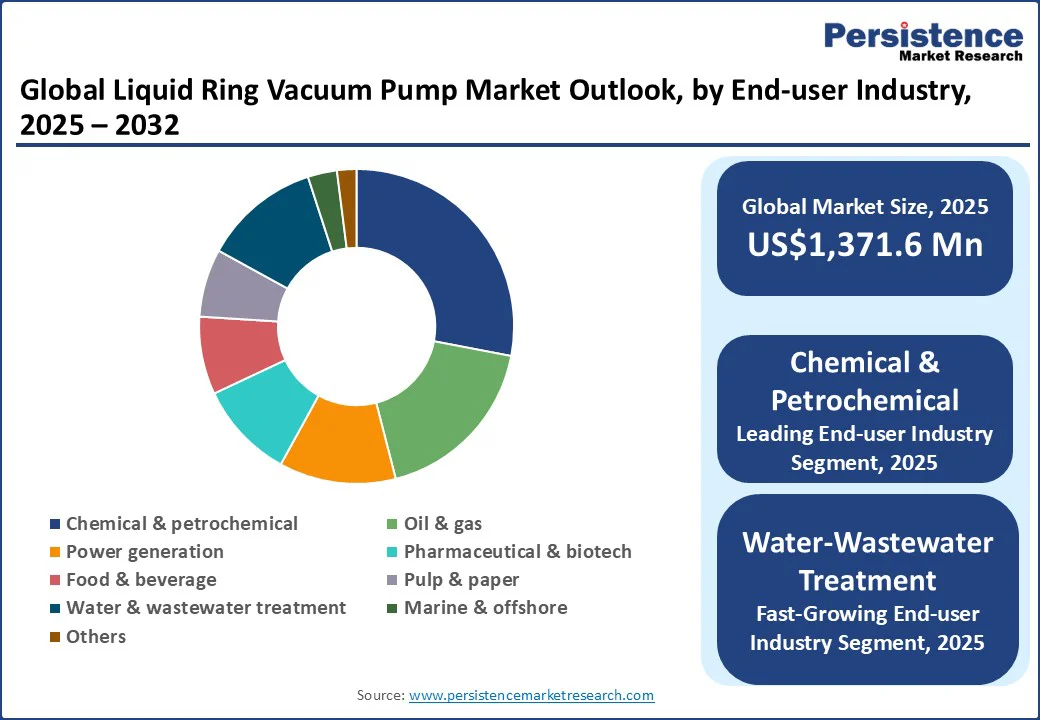

The global liquid ring vacuum pump market size is likely to be valued at US$ 1,371.6 Mn in 2025 and is expected to reach US$2,038.9 Mn by 2032, growing at a CAGR of 5.8% during the forecast period from 2025 to 2032, driven by stringent industrial regulations, increasing adoption of vacuum pumps across chemical, petrochemical, wastewater treatment sectors, and continuous technological innovations enhancing efficiency and reliability.

Key Industry Highlights:

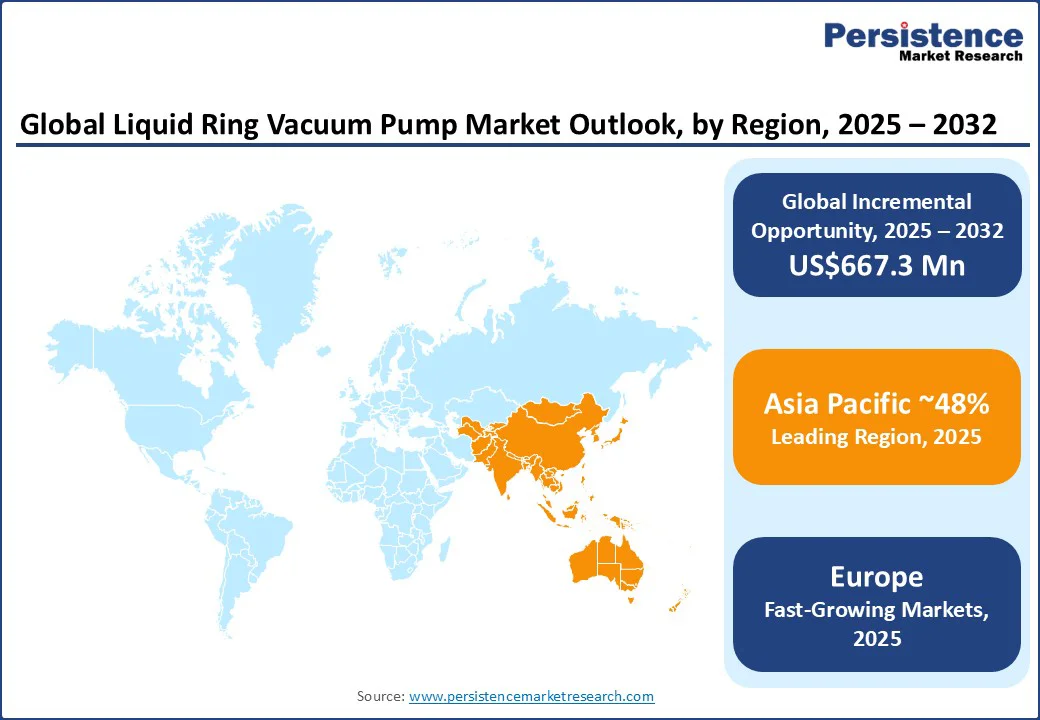

- Leading Region: Asia Pacific is anticipated to hold the largest market share of approximately 48% in 2025, driven by rapid industrialization, rising chemical and wastewater treatment operations, and growing investments in energy-efficient vacuum technologies.

- Fastest-growing Region: Europe stands out as the fastest-growing regional market, expanding at a 6.1% CAGR, supported by Germany’s technological leadership, stringent sustainability policies under the European Green Deal, and rising investments in pharmaceuticals, chemical processing, and water management.

- Dominant Product Type: Single-stage pumps are projected to account for a majority share of around 62% in 2025, supported by widespread adoption in medium-flow applications across chemical, pharmaceutical, and food processing industries due to their cost-effectiveness and operational reliability.

- Leading Material Type: Stainless steel components are increasingly used, representing over 55% of material demand, propelled by stringent corrosion-resistance standards and rising adoption in chemical, biotech, and marine sectors.

- Leading End-user: The chemical and petrochemical industry continues to lead consumption, benefiting from regulatory compliance requirements, process automation investments, and the need for efficient vacuum systems in large-scale production.

| Key Insights | Details |

|---|---|

|

Liquid Ring Vacuum Pump Market Size (2025E) |

US$1,371.6 Mn |

|

Market Value Forecast (2032F) |

US$2,038.9 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Industrial Regulations and Technological Advancements

Stringent industrial regulations combined with continuous technological innovation are driving global demand for liquid ring vacuum pumps. Industries such as chemical, pharmaceutical, and wastewater treatment increasingly require efficient, compliant pumping solutions that reduce emissions, enhance safety, and optimize energy usage. Technological improvements, including corrosion-resistant materials, optimized impeller designs, and automated control systems, have strengthened operational reliability and efficiency, promoting widespread adoption across multiple end-use sectors.

Governmental frameworks, including the U.S. Environmental Protection Agency (EPA) guidelines and the European Industrial Emissions Directive (IED), have mandated stricter environmental compliance, fueling the adoption of advanced vacuum technologies. Studies from the International Water Association (IWA) indicate that energy-efficient pumping systems in wastewater treatment can reduce operational costs by up to 20%, while pharmaceutical industry standards, as outlined by the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), encourage automated, high-reliability vacuum solutions. These factors collectively reinforce sustained market growth and long-term investments in advanced liquid ring vacuum pump systems.

Operational Limitations and Maintenance Complexity Hinder Market Expansion

The market faces challenges primarily due to operational limitations and maintenance complexity. These pumps are less efficient in handling highly viscous or solid-laden fluids, restricting adoption in chemical, pulp, and wastewater applications, where process fluids often contain suspended solids or high particulate content. This inefficiency results in reduced throughput and higher energy consumption, directly affecting production schedules.

Routine maintenance requirements, such as seal integrity checks, corrosion management, and periodic liquid replacement, further add to operational downtime and labor dependency. For industries operating under strict process timelines or with limited technical expertise, these factors discourage adoption and slow market penetration, creating practical barriers that limit widespread utilization of liquid ring vacuum pumps despite regulatory and technological support for their deployment.

Sustainability and Digital Integration Drive Future Growth

Rising emphasis on sustainability and digitalization across industrial operations is creating significant growth potential for liquid ring vacuum pumps. Industries are increasingly adopting energy-efficient, environmentally compliant pumping solutions that reduce water consumption, optimize energy usage, and enable real-time performance monitoring. Innovations such as IoT-enabled sensors, predictive maintenance systems, and automated flow control enhance operational efficiency, minimize downtime, and strengthen long-term reliability, positioning these pumps as essential components of modern industrial infrastructure.

Government programs, including the European Green Deal and the U.S. Department of Energy’s Industrial Efficiency Initiatives, are driving adoption of advanced, energy-saving technologies. Leading manufacturers are investing in research and development to integrate digital controls, corrosion-resistant materials, and modular designs, expanding pump applications across chemical, pharmaceutical, and wastewater treatment sectors. Strategic deployment of sustainable and digitally enhanced vacuum systems is expected to accelerate global adoption, reinforcing market growth throughout the forecast period.

Category-wise Analysis

Product Type Insights

Single-stage pumps are expected to dominate the market with a 62.0% share in 2025, supported by their cost-effectiveness, ease of operation, and strong demand in medium-flow applications across chemical, food processing, and general manufacturing industries. Their steady adoption reflects reliability in industries where consistent performance outweighs the need for advanced configurations.

In contrast, two-stage pumps, growing at a 6.3% CAGR, are gaining traction in sectors requiring deeper vacuum levels, such as pharmaceuticals, biotech, and power generation. This growth is further supported by stricter environmental compliance policies in North America and Europe, where efficient vacuum technologies are being promoted through industrial modernization programs. The product landscape highlights a balance between reliance on proven solutions and the accelerating shift toward advanced pump systems shaped by evolving process demands and regulatory frameworks.

End-user Insights

The chemical and petrochemical industry is projected to account for a 28.0% share of the market in 2025, driven by the sector’s extensive reliance on reliable vacuum systems for process efficiency, safety, and adherence to strict environmental regulations. Growing production capacities, coupled with increasing emphasis on energy-efficient operations, have reinforced the adoption of advanced pump technologies across refineries, chemical plants, and related facilities.

Water and wastewater treatment is the fastest-growing segment with a 6.6% CAGR, benefiting from increasing global investments in sustainable infrastructure and government-backed initiatives such as the European Industrial Emissions Directive and the U.S. Clean Water Act. Pharmaceuticals and food & beverage industries are also enhancing demand, supported by stringent quality standards and rising production scales. In parallel, oil & gas, power generation, and marine sectors maintain steady uptake, relying on specialized vacuum solutions to ensure operational reliability and compliance, which further strengthens the market’s long-term expansion trajectory.

Regional Insights

Asia Pacific Liquid Ring Vacuum Pump Market Trends - China Leads Asia Pacific Market Driven by Industrial Expansion and Strategic Investments

Asia Pacific is likely to account for approximately 48.0% of the market share in 2025, with China leading due to its extensive chemical, petrochemical, and wastewater treatment industries that demand reliable, energy-efficient vacuum solutions. In 2023, the Chinese government implemented the 14th Five-Year Plan for Ecological and Environmental Protection, emphasizing the adoption of advanced, energy-efficient technologies across industrial sectors. This policy framework has accelerated the integration of liquid ring vacuum pumps in various applications, aligning with national goals for sustainability and energy efficiency.

India, Japan, and South Korea are experiencing significant growth in their industrial sectors. India's "Make in India" initiative and investments in chemicals and pharmaceuticals are boosting demand for high-performance pumps. Japan's eco-friendly manufacturing and government sustainability programs promote energy-efficient vacuum systems. Meanwhile, South Korea's emphasis on smart manufacturing accelerates the use of advanced vacuum technologies in chemical processing and wastewater treatment. These trends reflect the region's dynamic growth through strategic collaborations and supportive policies.

North America Liquid Ring Vacuum Pump Market Trends - The U.S. Leads Fueled by Industrial Modernization and Strategic Initiatives

North America is likely to command approximately 22.0% of the market share in 2025, anchored by the expansive chemical, pharmaceutical, and water treatment sectors in the U.S. that demand high-efficiency vacuum systems. In April 2023, Atlas Copco completed the acquisition of Trillium US Inc., a well-regarded provider of vacuum pump services and light manufacturing, reinforcing localized production of advanced vacuum technologies and strengthening its North American footprint.

Canada is equally advancing with strong governmental support for industrial sustainability and efficiency, stimulating adoption in chemical processing and wastewater treatment. Across the region, rising capital investments in biotechnology, pharmaceuticals, and automation are fueling demand for dependable, high-performance pump solutions. Concurrently, rigorous environmental standards, particularly U.S. EPA regulations on energy and emissions, are driving industries toward greener, technologically advanced systems. These strategic expansions, combined with regulatory incentives, are anchoring North America as a robust and steadily growing regional market.

Europe Liquid Ring Vacuum Pump Market Trends - Germany Drives European Market with Industrial Innovation and Regulatory Support

Europe is likely to account for approximately 20.0% of the market share in 2025, with Germany leading due to its strong chemical, pharmaceutical, and wastewater treatment industries that require reliable, energy-efficient vacuum solutions. In October 2023, Busch Vacuum Solutions introduced the new generation of its MINK MM dry claw vacuum pumps. These pumps are designed to minimize operating costs, reduce energy consumption, and lower CO? emissions through reduced raw material requirements, aligning with stringent environmental standards and reinforcing Germany's market dominance.

Growing emphasis on sustainability, process automation, and industrial modernization is boosting demand in France, the U.K., and Italy. European governments are actively promoting energy efficiency and emission reduction through initiatives such as the European Green Deal and industrial decarbonization programs, encouraging industries to adopt advanced vacuum systems. Rising investments in pharmaceutical production, chemical processing, and water management projects are accelerating market uptake, while technological advancements and regulatory incentives are supporting the deployment of high-performance liquid ring vacuum pumps. These trends highlight Europe’s strong growth potential and its role as a significant contributor to the global market.

Competitive Landscape

The global liquid ring vacuum pump market is driven by manufacturers advancing innovation, expanding production capacity, and forming strategic collaborations, with a focus on energy-efficient and digitally integrated vacuum systems. Robust supplier and distributor networks ensure timely delivery, high-quality support, and responsive service, enabling widespread adoption across the chemical, pharmaceutical, and wastewater industries. These initiatives strengthen competition, drive continuous product improvement, and enhance operational reliability, reinforcing market resilience and supporting sustained global expansion.

Key Industry Developments

- In July 2025, Busch Vacuum Solutions introduced the COBRA NC 2500 C, the world's largest dry and air-cooled screw vacuum pump. This innovative pump features an integrated radiator cooling system, eliminating the need for external water cooling. The design enhances operational flexibility and reduces environmental impact, making it ideal for industries requiring high-performance vacuum technology.

- In May 2022, Atlas Copco launched the GHS 1402-2002 VSD+ series, a range of oil-sealed rotary screw vacuum pumps. These pumps offered improved performance, optimal oil separation, and a smaller footprint. The user-friendly HEX@ controller provides intelligent networking capabilities, aligning with Industry 4.0 standards.

- In October 2021, Atlas Copco announced the acquisition of HHV Pumps Pvt. Ltd., a leading vacuum pump manufacturer in India. This acquisition strengthened Atlas Copco's presence in the Asia Pacific region and enhanced its capabilities in providing vacuum solutions to a wide range of industries.

Companies Covered in Liquid Ring Vacuum Pump Market

- Busch Vacuum Solutions

- Atlas Copco

- Gardner Denver (NASH)

- DEKKER Vacuum Technologies

- Elmo Rietschle (Gardner Denver)

- Pfeiffer Vacuum

- Edwards Vacuum

- Graham Manufacturing

- Vacuubrand

- Vacuum Research Corporation

- Kinney Vacuum

- Tuthill Vacuum & Blower Systems

- Metallurgical High Vacuum Corporation

- ACI Medical

- Binaca Pumps

Frequently Asked Questions

The liquid ring vacuum pump market is set to reach US$1,371.6 Mn in 2025.

Stringent industrial regulations combined with continuous technological advancements are driving the widespread adoption of liquid ring vacuum pumps across global industries.

The liquid ring vacuum pump market is estimated to grow at a CAGR of 5.8% from 2025 to 2032.

The liquid ring vacuum pump market is poised for growth as industries increasingly adopt sustainable technologies and digitally integrated systems to enhance efficiency, compliance, and operational performance.

The major players dominating the liquid ring vacuum pump market are Busch Vacuum Solutions, Atlas Copco, Gardner Denver (NASH), DEKKER Vacuum Technologies, Elmo Rietschle (Gardner Denver), and Pfeiffer Vacuum.