- Home Appliances

- Bagless Vacuum Cleaner Market

Bagless Vacuum Cleaner Market Size, Share, and Growth Forecast, 2026 - 2033

Bagless Vacuum Cleaner Market by Product Type (Handheld, Canister, Stick, Robotic), Application (Commercial, Industrial, Residential), Power Type (Cord-powered, Cordless), and Regional Analysis for 2026 - 2033

Bagless Vacuum Cleaner Market Share and Trends Analysis

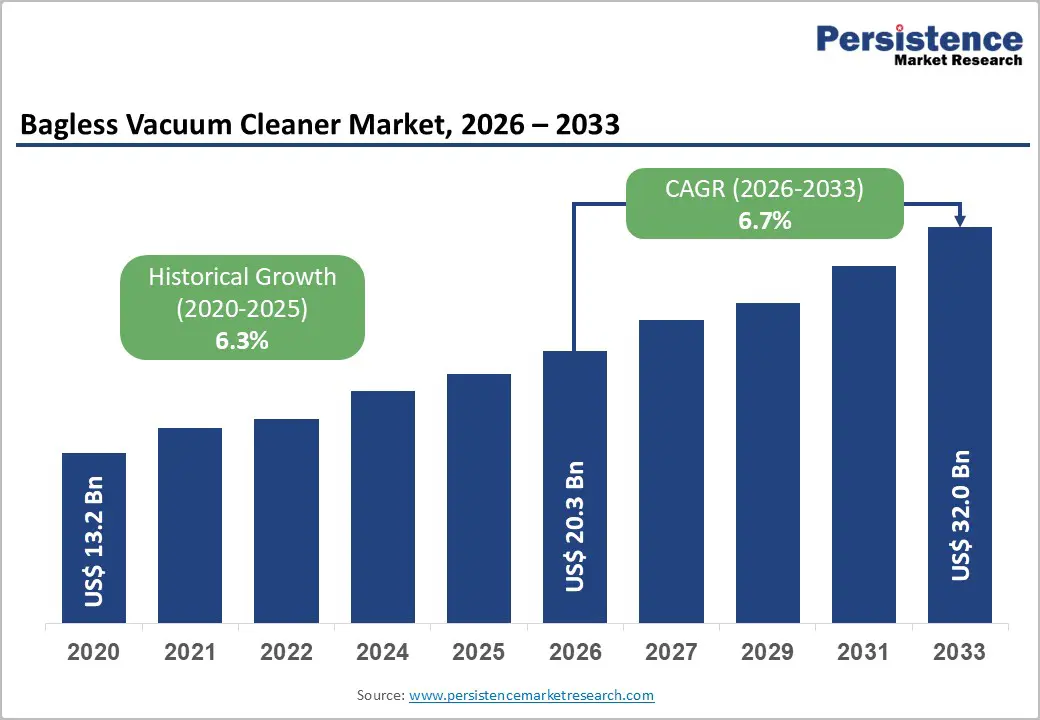

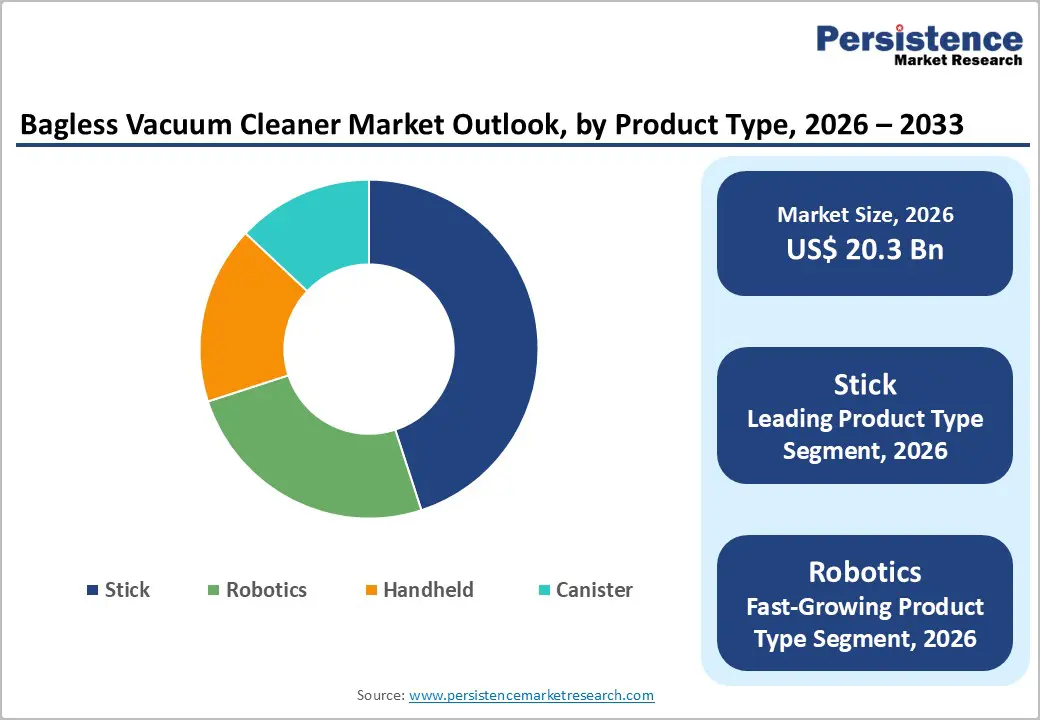

The global bagless vacuum cleaner market size is likely to be valued at US$ 20.3 billion in 2026, and is projected to reach US$ 32.0 billion by 2033, growing at a CAGR of 6.7% during the forecast period 2026 - 2033.

The market expansion is driven by urbanization, rising disposable income, and growing consumer preference for low-maintenance cleaning solutions. Technological improvements in cyclonic suction, high-efficiency particulate air (HEPA) filtration, and energy efficiency have strengthened product differentiation. Continued residential construction growth, increasing penetration of cordless and robotic formats, and regulatory shifts toward energy-efficient appliances support steady medium-term demand growth.

Key Industry Highlights

- Product Type Dominance: Stick is poised to dominate the revenue share with approximately 44% in 2026, while robotic is likely to be the fastest-growing segment during the 2026 - 2033 forecast period.

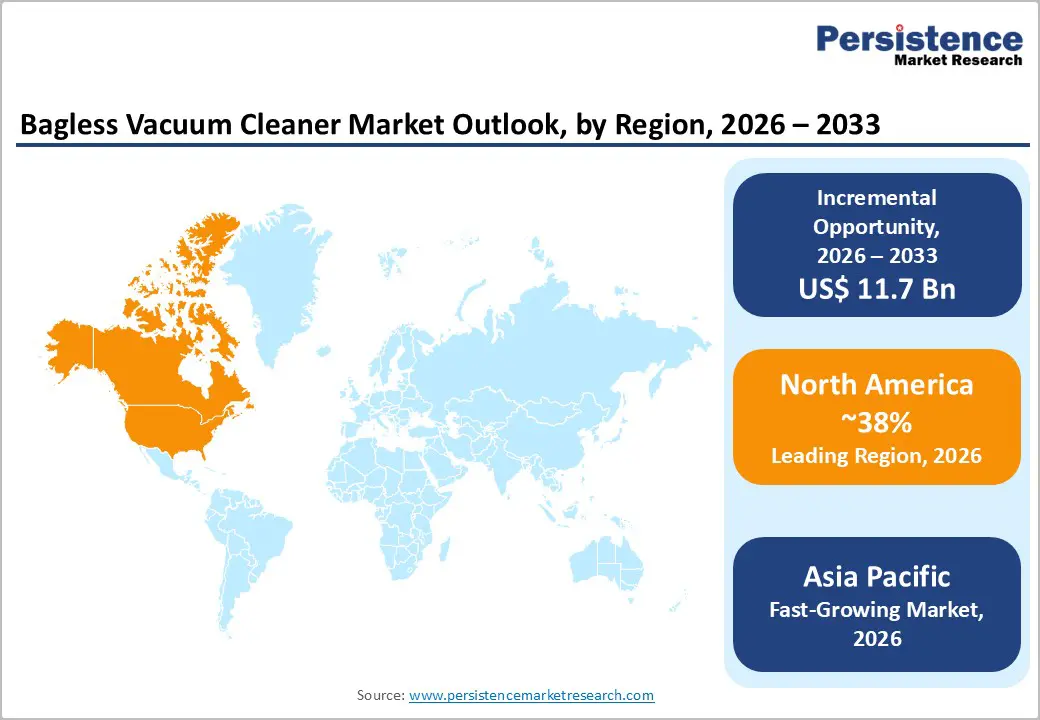

- Dominant Region: North America is expected to command about 38% market share in 2026, owing to strong consumer purchasing power and extensive appliance penetration.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing through 2033, due to the booming expansion of urban populations.

- Application Leadership: Residential applications are projected to capture roughly 80% of the revenue share in 2026, with commercial applications showing the fastest growth from 2026 to 2033.

| Key Insights | Details |

|---|---|

| Bagless Vacuum Cleaner Market Size (2026E) | US$ 20.3 Bn |

| Market Value Forecast (2033F) | US$ 32.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Advancements in Cyclonic and Filtration Systems

Manufacturers are improving cyclonic separation systems to strengthen dust capture and prevent filter blockage in bagless vacuum cleaners. These engineering upgrades maintain strong suction during extended operation and improve overall cleaning efficiency. Policy initiatives are also shaping product development. The United States Department of Energy (DOE) and the European Commission (EC) Ecodesign Directive are encouraging appliance manufacturers to reduce energy consumption while maintaining effective performance. As a result, companies are designing vacuum models that use less electricity yet deliver consistent cleaning results. These improvements support energy efficiency goals and appeal to households seeking environmentally responsible appliances.

Filtration technology is also advancing to address indoor air quality concerns. HEPA filters that meet guidance from the United States Environmental Protection Agency (EPA) are capturing fine particles such as allergens and dust. Increased awareness of airborne pollutants and household hygiene is strengthening demand for vacuum systems that improve indoor air conditions. Manufacturers are positioning these filtration features in premium product lines, which supports higher pricing and margin growth. Future designs are expected to incorporate intelligent sensors that regulate airflow and optimize filtration performance, which will further enhance cleaning effectiveness and consumer trust in health focused home appliances.

Growth in Smart and Cordless Appliance Penetration

Advances in lithium-ion battery technology are improving performance of cordless vacuum cleaners. Industry assessments from the International Energy Agency (IEA) indicate that newer battery systems provide longer operating time and shorter charging cycles. Manufacturers are using these improvements to expand production of cordless stick vacuum models, most of which use bagless dust collection systems. Lightweight materials and compact motor designs are increasing portability, which allows users to clean multiple surfaces, such as stairs, furniture, and tight spaces, more efficiently. These features align with demand from urban households that prioritize convenience, mobility, and fast setup in home cleaning appliances.

Smart home adoption is also influencing product design across the vacuum cleaner market. The International Telecommunication Union (ITU) highlights rapid expansion of Internet of Things (IoT) integration in household appliances. Modern vacuum models now offer mobile app control, enabling diagnostics, cleaning reports, and suction adjustments for different floor surfaces. Many systems also connect with voice assistants that allow scheduled cleaning routines and automated operation. Manufacturers are developing advanced models with artificial intelligence (AI)-based navigation and obstacle detection to improve cleaning precision. These capabilities are strengthening product differentiation and positioning bagless cordless vacuum cleaners as key components within connected home ecosystems.

Technological Stagnation Challenges

Manufacturers in the bagless vacuum cleaner market face innovation constraints because product differentiation has been gradual. Many models offer similar performance features, which makes it difficult for brands to stand out in a competitive retail environment. Consumers increasingly expect advanced functions such as automated dust disposal systems and adaptive suction control, yet some companies remain cautious about large research and development (R&D) investments. This slow pace of innovation leads to product similarity across competing brands, encouraging consumers to rely on established manufacturers rather than explore new entrants.

As differentiation declines, competition often shifts toward pricing strategies instead of technological advancement. Companies frequently introduce incremental improvements such as ergonomic handles or cosmetic design updates rather than transformative product changes. This pattern reduces opportunities to attract younger consumers who prefer smart home integration and connected appliance capabilities. To strengthen competitiveness, manufacturers are exploring collaboration with technology developers and robotics specialists to introduce more intelligent cleaning systems. Early adoption of advanced automation and smart functionality may help leading brands capture technology-focused households and stimulate the bagless vacuum cleaner market growth.

Ecological Concerns and Sustainability Struggles

Rising environmental awareness is creating strategic pressure for manufacturers in the bagless vacuum cleaner market. Consumers increasingly prefer appliances with a lower ecological impact, including products made from recycled materials or that facilitate easier component recycling. Bagless models reduce waste generated by disposable vacuum bags, yet many units contain mixed plastic components that are difficult to recycle at the end of life. This challenge is prompting manufacturers to reassess product design, material sourcing, and manufacturing processes. Brands that fail to demonstrate credible sustainability commitments risk losing relevance among environmentally conscious buyers.

Energy efficiency is another concern shaping purchasing decisions. High-performance vacuum motors often require greater electricity consumption, which conflicts with consumer expectations for low-impact appliances. Manufacturers face technical and financial barriers when redesigning motor systems or supply chains to meet stricter sustainability standards. As a result, some companies are exploring modular product architectures and biodegradable materials that align with circular-economy principles. Environmental certifications and eco-focused product development strategies are becoming important competitive factors. Companies that invest early in sustainable design and energy-efficient technologies are strengthening brand trust and long-term market positioning.

Expansion into Commercial and Hospitality Segments

Commercial cleaning services are increasingly replacing bagged canister vacuums with bagless systems to reduce consumable waste and operating expenses. Facilities such as office complexes, hotels, and hospitals require equipment that can cover large floor areas without frequent interruptions for bag replacement. Cleaning staff also benefit from transparent dust containers that allow quick visual confirmation of debris collection. Manufacturers are introducing backpack-style bagless vacuums designed for extended use in multi-floor environments. These units improve mobility and productivity while providing strong suction on mixed surfaces, including carpets and hard flooring. The transition reflects operational priorities among facility managers who aim to lower maintenance costs and improve cleaning efficiency.

A significant opportunity exists for durable, high-capacity bagless backpack models engineered for intensive commercial use. Many current products generate noise levels that disrupt quiet environments such as hospital wards or meeting spaces. Equipment durability is also critical because commercial units operate for long daily shifts. Manufacturers that develop quieter motor systems, reinforced housings, and ergonomic carrying structures can address these gaps effectively. Additional features, such as simplified dust-disposal mechanisms and HEPA filtration systems, will help meet hygiene requirements in sensitive facilities. Companies that deliver reliable professional-grade solutions are likely to secure long-term contracts with facility management providers.

Integration of AI and Smart Home Ecosystems

Vacuum cleaners are evolving from basic mechanical appliances into connected devices supported by IoT technology. Manufacturers are integrating sensors that detect floor surfaces such as hardwood or carpet and automatically adjust suction levels. These systems improve energy efficiency and extend battery life during cleaning cycles. Many models now connect with voice assistants such as Amazon Alexa and Google Home, allowing users to start or pause cleaning with voice commands. Smart connectivity also enables remote monitoring through mobile applications, allowing households to manage cleaning schedules and device performance within broader smart home ecosystems.

Interoperability standards such as Matter are improving compatibility among connected devices from different manufacturers. AI-powered functions are also emerging in advanced vacuum systems that monitor component conditions and notify users when maintenance tasks, such as filter replacement, are required. Application-based scheduling aligns cleaning routines with household activities, improving convenience for busy users. Manufacturers are differentiating products through software-driven features that add capabilities such as obstacle detection and optimized cleaning routes. Future product development is expected to combine smart connectivity with robotic automation, positioning vacuum cleaners as integrated components within connected home service platforms.

Category-wise Analysis

Product Type Insights

Stick vacuum cleaners are anticipated to hold the largest share among product types, generating about 44% of the market revenue in 2026. Consumers prefer stick bagless models because they combine lightweight construction with flexible cleaning functions. These devices operate in upright mode for floor cleaning and convert into handheld units for furniture, stairs, and confined areas. Cordless operation and compact storage make them suitable for urban apartments and households that prioritize quick daily cleaning. Strong suction performance also supports the removal of pet hair and fine debris, which reinforces their popularity among modern households seeking convenient cleaning appliances.

Robotic vacuum cleaners are expected to exhibit the fastest growth during the 2026-2033 forecast period. These devices provide automated cleaning through integrated navigation technology and mobile application control. Built-in mapping systems guide movement across rooms, while scheduling functions allow users to manage cleaning remotely. Improvements in battery capacity support longer operating cycles, and sensor systems help avoid obstacles such as furniture or cables. Manufacturers are enhancing AI capabilities to improve dirt detection and optimize cleaning routes. Self-emptying docking systems are also increasing convenience, which strengthens demand among technology-oriented consumers and supports integration within smart home environments.

Application Insights

Residential use is likely to capture nearly 80% of the bagless vacuum cleaner market revenue share in 2026. Households rely on bagless vacuum cleaners for routine cleaning across living areas such as kitchens, bedrooms, and hallways. Users value the simple dust disposal process that eliminates the need for disposable bags while maintaining strong suction for surfaces such as carpets, hardwood flooring, and tiles. Adoption is widespread in urban apartments and suburban homes where frequent cleaning is required to remove pet hair, food debris, and everyday dust. Compact product designs and cordless operation also support easy storage and flexible use across multi-level homes.

Commercial applications are expected to record the fastest growth between 2026 and 2033. Facilities such as hospitals, hotels, and entertainment venues are adopting bagless vacuum systems to reduce plastic waste and improve operational efficiency. High-traffic environments require equipment with strong suction capacity and quick dust removal to maintain hygiene standards. Professional equipment brands such as Kärcher and Nilfisk are introducing durable models designed for extended use in commercial settings. Facility managers prefer these systems because they reduce consumable costs, support environmental compliance, and maintain consistent cleaning performance.

Regional Insights

North America Bagless Vacuum Cleaner Market Trends

North America is slated to secure an estimated 38% of the bagless vacuum cleaner market share in 2026, with the United States generating the majority of regional demand. Consumers in this market favor premium appliances that address specific household needs, particularly for pet hair and allergen removal. High capacity upright models remain popular for deep carpet cleaning, while cordless stick vacuums provide flexibility for cleaning furniture, stairs, and confined areas. Manufacturers such as SharkNinja and Bissell are strengthening their product portfolios with features such as anti-tangle brush systems and detachable canister designs that simplify maintenance and improve performance.

Product development in the region is also influenced by evolving regulatory frameworks. Policies supporting Right to Repair initiatives are encouraging manufacturers to design appliances with replaceable batteries, serviceable motors, and modular components. These changes extend product life cycles and reduce electronic waste. Companies are responding by offering spare parts and digital maintenance guides through mobile applications to support consumer repairs. This regulatory environment is promoting competition based on product durability and serviceability, while reinforcing North America’s role as a leading market for innovation in home appliance technology.

Europe Bagless Vacuum Cleaner Market Trends

The Europe bagless vacuum cleaner market is shaped by strict energy efficiency regulations and coordinated environmental policy frameworks. Germany, the United Kingdom, and France serve as major centers for both manufacturing and consumer demand. The European Union (EU) Ecodesign and Energy Labelling regulations set limits on power consumption and noise emissions for household appliances. Manufacturers such as Miele and Bosch are optimizing airflow systems and motor efficiency to maintain strong suction while reducing electricity use. These requirements are encouraging companies to redesign motors, filtration systems, and airflow channels to meet sustainability standards while maintaining cleaning performance.

European consumers often prefer bagless canister vacuum models because of their durable construction and advanced filtration capabilities. These systems perform well across multiple floor surfaces such as stone, wood, and carpeted areas. Many brands emphasize sealed dust containment systems that prevent allergen release during disposal, which appeals to households concerned about indoor air quality. The regional market reflects a strong preference for durable appliances that deliver long term reliability rather than short term trends. Manufacturers are also exploring renewable and recyclable materials to align with European Union sustainability goals. This regulatory and consumer environment is positioning Europe as an influential market that shapes global appliance design standards.

Asia Pacific Bagless Vacuum Cleaner Market Trends

Asia Pacific is projected to be the fastest-growing regional market for bagless vacuum cleaners, powered by rapid urbanization and strong manufacturing capacity. China serves as the largest production and consumption hub, while India and Japan are also generating rising household demand. Regional manufacturers are expanding production of cordless and robotic vacuum models at competitive prices, which accelerates adoption across mass consumer markets. Efficient supply chains and large scale electronics manufacturing allow companies to introduce new models quickly while maintaining cost advantages. Urban households are favoring compact stick vacuums and robotic systems that operate effectively in smaller apartments and hard floor environments.

Urban lifestyle changes are reinforcing demand for lightweight and space efficient cleaning appliances. Companies such as Dreame and Tineco are expanding market presence by incorporating AI-based navigation and advanced dirt detection features. Investment activity is increasing as manufacturers target the expanding middle class that seeks technologically advanced yet affordable appliances. Several governments in the region are supporting electronics manufacturing through policy incentives and industrial development programs. As product innovation and large scale production expand, Asia Pacific manufacturers are strengthening export capacity and influencing global trends in smart home cleaning technology.

Competitive Landscape

The global bagless vacuum cleaner market structure is moderately consolidated, with major manufacturers such as Dyson, SharkNinja, Bissell, Samsung, and LG collectively accounting for about 58% of the total market share. These companies compete through technological innovation, product design, and strong global distribution networks. Their portfolios span cordless stick models, robotic systems, and upright vacuum cleaners that target both premium and mid-range consumer segments.

Leading brands are increasingly prioritizing sustainability in product development. Manufacturers are introducing vacuum models built with recyclable materials and energy efficient motor systems to meet rising demand for environmentally responsible appliances. Companies are also expanding capacity through mergers, acquisitions, and strategic partnerships that support faster innovation and larger production volumes. These strategies enable the integration of advanced filtration technologies and improved product durability while aligning with global regulations focused on waste reduction and energy efficiency.

Key Industry Developments

- In December 2025, ECOVACS launched the DEEBOT X11 OmniCyclone in India as a premium robotic vacuum and mop designed for intelligent home cleaning. The device features advanced OZMO Roller 2.0 technology that delivers about 3800 Pa mopping pressure, significantly stronger than conventional systems, along with high-power suction and automated maintenance functions. The model integrates vacuuming and mopping with smart navigation and a bagless OmniCyclone station for debris management.

- In August 2025, Milagrow launched the BlackCat 25 Ultra in India, the country's first AI-powered self-emptying bagless robotic vacuum cleaner priced at INR 30,990 on its website and Amazon. Featuring the BharatBot 0.24 AI engine, 12,000 Pa suction (25,000 Pa in base), 32 sensors with LiDAR mapping, 120-minute runtime covering 2,500 sq. ft.

- In May 2025, Dyson unveiled the PencilVac, described as the world’s slimmest vacuum cleaner with a handle only 38 mm in diameter. Despite its ultra-thin design, it uses a compact Hyperdymium motor spinning up to 140,000 rpm and a four-cone “Fluffycones” cleaner head that prevents hair tangling while maintaining strong suction.

Companies Covered in Bagless Vacuum Cleaner Market

- Dyson Ltd.

- SharkNinja Operating LLC

- Bissell Inc.

- Samsung Electronics

- LG Electronics

- Tineco Intelligent Technology

- Roborock

- AB Electrolux

- Miele & Cie. KG

- Robert Bosch GmbH

- Panasonic Corporation

- iRobot Corporation

- Dreame Technology

- Kärcher

- Nilfisk

Frequently Asked Questions

The global bagless vacuum cleaner market is projected to reach US$ 20.3 billion in 2026.

The market is driven by the highly accelerated urbanization in Asia Pacific, Latin America, and Africa that is boosting demand for compact, low-maintenance cleaners in dense households.

The market is poised to witness a CAGR of 6.7% from 2026 to 2033.

Major opportunities lie in commercial sectors such as hospitals seek durable bagless models for hygiene and sustainability.

Dyson, SharkNinja, Bissell, Samsung, and LG. are some of the key players in the market.