- Industrial Machinery

- Vacuum Lifter Market

Vacuum Lifter Market Size, Share, and Growth Forecast 2025 - 2032

Vacuum Lifter Market by Product Type (Electro-Pneumatic Vacuum Lifters, Others), Payload Capacity (Lightweight, Medium weight, Heavyweight), End-user (Manufacturing, Construction, Aerospace, Food and Beverage, Others), and Regional Analysis for 2025 - 2032

Vacuum Lifter Market Size and Trends Analysis

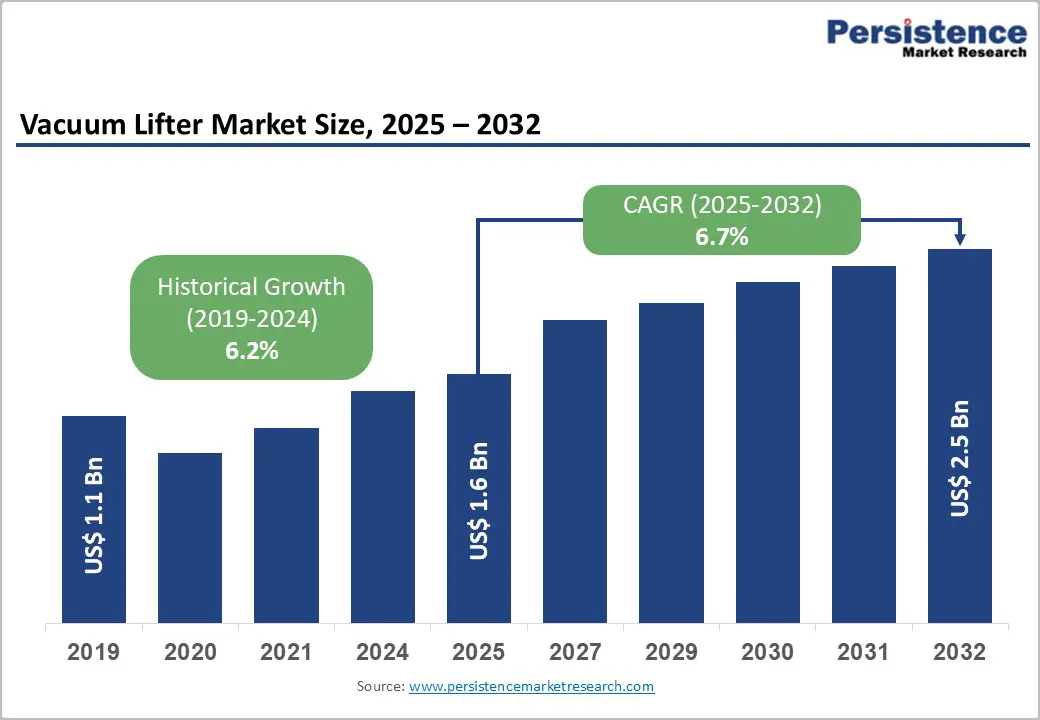

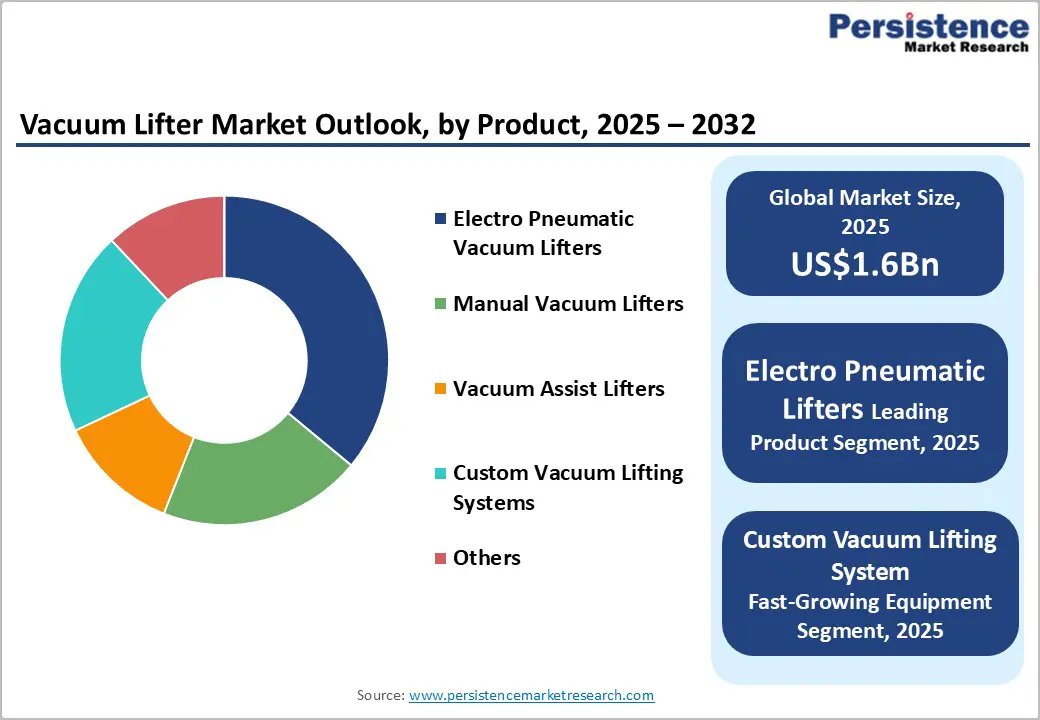

The global vacuum lifter market size is likely to be valued at US$1.6 billion in 2025 and is expected to reach US$2.5 billion by 2032, growing at a CAGR of 6.7% during the forecast period from 2025 and 2032, driven by increasing demand for efficient, safe, and ergonomic material handling solutions across manufacturing, construction, aerospace, logistics, and warehousing industries.

Rising labor costs, stricter workplace safety regulations, and the need to minimize manual-handling injuries are key factors driving adoption. Technological advancements in electro-pneumatic, vacuum-assisted, and custom lifting systems are expanding operational flexibility, enabling industries to handle a wide range of payloads, from lightweight components to heavy materials.

Key Industry Highlights

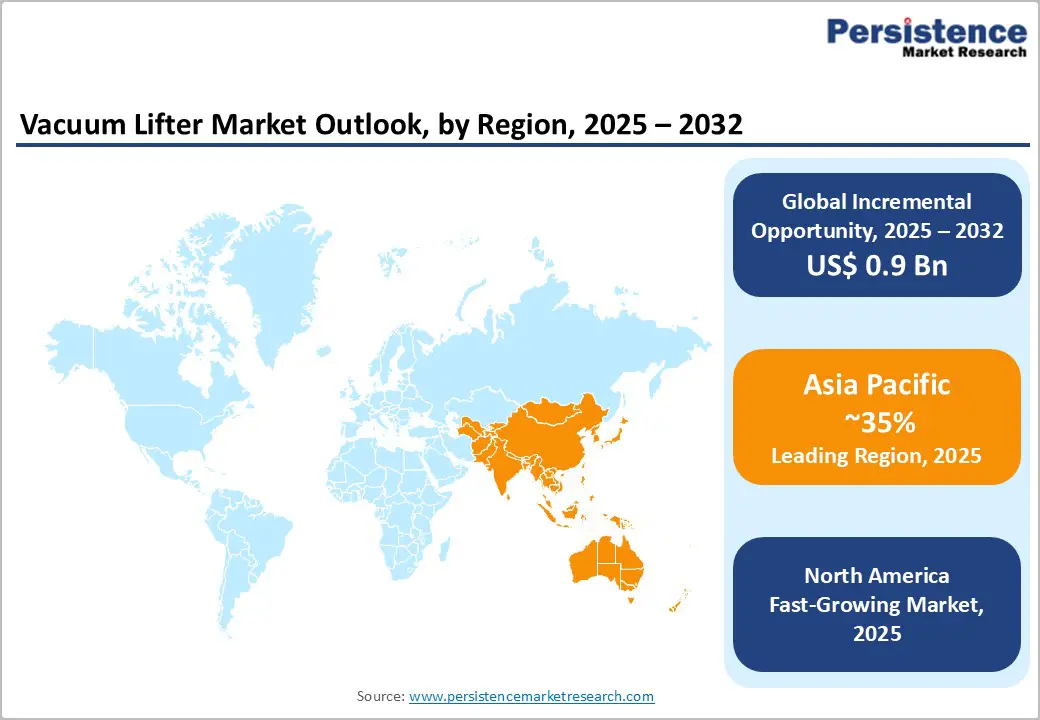

- Leading Region: Asia Pacific leads, with over 35% market share in 2025, driven by strong manufacturing expansion, rising automation adoption, and increasing investments in construction and industrial sectors across China, India, Japan, and ASEAN.

- Fastest-growing Region: North America is the fastest-growing region, driven by a strong manufacturing base and strict OSHA and ANSI safety regulations. The region’s focus on automation, smart factories, and advanced electro-pneumatic lifters drives growth across the aerospace, logistics, and e-commerce sectors.

- Leading Product Type: Electro-pneumatic vacuum lifters lead the market with around 40% revenue share in 2025, driven by superior control, safety, and efficiency in automated manufacturing and construction.

- Leading Payload Capacity: Heavyweight vacuum lifters lead with over 50% market revenue share, driven by their critical role in construction, manufacturing, and warehousing for handling heavy materials, including steel, glass, and large machinery.

- Leading End-user Type: The manufacturing sector leads with about 35% market revenue share, driven by strong demand from automotive, aerospace, and heavy machinery industries for efficient and safe material handling.

| Key Insights | Details |

|---|---|

| Vacuum Lifting Market Size (2025E) | US$1.6 Bn |

| Market Value Forecast (2032F) | US$2.5 Bn |

| Projected Growth CAGR (2025 - 2032) | 6.7% |

| Historical Market Growth (2019 - 2024) | 6.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Innovations in Vacuum Lifting Systems

Modern systems use electro-pneumatic controls, advanced vacuum pumps, and sensor integration to precisely handle payloads ranging from lightweight components to materials weighing over 500 kg. Custom lifting configurations cater to sectors such as aerospace, electronics, and heavy machinery manufacturing. Ergonomic designs and automated safety features, such as emergency shutdowns and power loss check valves, enhance operator comfort and reduce workplace injuries. Integration with automated production lines and industry technologies ensures smooth workflows, real-time monitoring, and predictive maintenance, boosting efficiency and minimizing downtime.

Digital connectivity and automation have further expanded the capabilities of vacuum lifters. Smart systems now include IoT controls, remote diagnostics, and data analytics, enabling facility managers to monitor performance, optimize lifting cycles, and schedule maintenance. Portable and modular lifters are gaining popularity in construction, warehousing, and logistics. Manufacturers such as Anver, Schmalz, and Aardwolf continue to invest in R&D to improve precision, load capacity, and adaptability, making vacuum lifters a key component of industrial safety and efficiency.

Need for Skilled Workforce and Training

The widespread adoption of vacuum lifting systems is often constrained by the requirement for a skilled workforce capable of operating, maintaining, and troubleshooting advanced lifting equipment. Modern systems, especially electro-pneumatic and custom vacuum lifters, incorporate sophisticated controls, sensors, and automation features that necessitate specialized knowledge for safe and efficient operation. For many small and medium-sized enterprises (SMEs), particularly in emerging markets, the lack of trained personnel can slow deployment and reduce overall productivity.

Continuous training and upskilling are essential to ensure operators adhere to safety standards and maximize system performance. Inadequate training can lead to operational errors, increased maintenance issues, and potential workplace accidents, discouraging companies from investing in advanced lifting solutions. Manufacturers often provide technical support and training programs, but these require time and financial investments. The need for skilled labor and structured training programs remains a significant restraint in expanding vacuum lifter adoption across the industrial, construction, and logistics sectors.

Customization and Payload Capacity Expansion

Industries such as aerospace, construction, and electronics increasingly require specialized lifting systems designed to handle unique materials, shapes, and production processes. Manufacturers are responding by offering modular designs, configurable suction systems, and adaptable control mechanisms that cater to diverse operational requirements while improving safety and precision. Integration with smart factory systems and digital monitoring allows operators to optimize lifting cycles, track performance, and reduce downtime, enhancing operational efficiency. The trend toward tailored vacuum lifter solutions is expected to accelerate adoption in emerging markets, where customized material-handling solutions are in high demand.

Expanding payload capacity is another critical opportunity area, driven by the growing need to lift heavier and more complex components in sectors such as heavy machinery, shipbuilding, and infrastructure development. Technological advancements in vacuum pump design, high-strength materials, and automation integration are enabling lifters to handle loads exceeding 1,000 kg without compromising stability or control. The development of hybrid electro-pneumatic and vacuum-assist systems allows for precise handling of oversized or irregularly shaped items, opening new applications across manufacturing and logistics. This combination of high-capacity performance and versatility positions vacuum lifters as essential tools for modern industrial operations.

Category-wise Analysis

Product Type Insights

Electro-pneumatic vacuum lifters dominate the market, accounting for 40% of revenue in 2025. Their widespread use is driven by superior automation compatibility, precise handling, and enhanced safety features, making them ideal for a wide range of industrial applications. These systems combine pneumatic suction with electronic control, ensuring stable and efficient material handling for loads of various sizes and weights. The J. Schmalz SLG/LSG series, for instance, is commonly used in automotive and logistics due to its reliability and seamless integration with automated systems. Ongoing advancements in sensor-based load monitoring and IoT connectivity further boost operational efficiency.

The custom vacuum lifting system segment is the fastest-growing, driven by the demand for specialized solutions in industries such as aerospace, electronics, and heavy machinery, where standard lifters cannot meet specific needs. These systems offer flexibility with configurable suction pads, adjustable load capacities, and automated control options tailored to individual applications. Examples include Aardwolf’s modular lifters and Wood’s Powr-Grip heavy-duty vacuum systems, designed for handling irregular or oversized components. The trend toward high-capacity, task-specific lifters with ergonomic designs for operator safety is accelerating adoption in both developed and emerging markets.

Payload Capacity Type Insights

Heavyweight vacuum lifters (over 500 kg) dominate the market, accounting for over 50% of the revenue share in 2025, reflecting their critical role in heavy-duty industrial operations. These lifters are extensively used in sectors such as construction, manufacturing, and warehousing, where large and dense materials such as steel sheets, glass panels, and heavy machinery components must be handled safely and efficiently. For example, the Schmalz VacuMaster coil lifter, which can handle loads up to 750 kg and is used for handling heavy coils and large sheet materials in production plants. Their ability to lift bulky loads with precision reduces the risk of manual labor, enhances workflow efficiency, and supports integration with automated handling systems.

Medium-weight vacuum lifters (151 kg to 500 kg) represent the fastest-growing segment. Their popularity stems from their balance of lifting power, cost efficiency, and ergonomic design, making them ideal for flexible operations across manufacturing, logistics, and packaging. These lifters are ideal for flexible operations across manufacturing, logistics, and packaging, where moderate payloads require maneuverability and ease of integration with automated processes. For example, Wood’s Powr-Grip mid-capacity lifters are widely used for glass handling. Their compact size, versatility, and quick setup make them suitable for mid-scale applications, supporting safer workflows and higher productivity, fueling rapid market growth.

End-user Type Insights

The manufacturing sector leads the vacuum lifter market, accounting for around 35% of the revenue share in 2025. Industries such as automotive, aerospace, and heavy machinery are increasingly adopting advanced lifting solutions to enhance safety, precision, and efficiency in assembly and material handling. In aerospace, custom vacuum lifting systems are used to handle large composite panels and fuselage sections. The integration of automation and ergonomic designs further drives adoption, improving safety and boosting throughput across production facilities. As manufacturers prioritize lean operations and workforce safety, the demand for reliable vacuum lifters continues to grow.

The construction industry is the fastest-growing end-user segment, fueled by rapid urbanization and large-scale infrastructure projects globally. Vacuum lifters are increasingly employed to safely handle heavy glass façades, precast concrete elements, and structural steel beams, particularly in high-rise and smart infrastructure projects in the Asia-Pacific and North America. For instance, Elephant Lifting Products’ Glass Lifting Vacuum Systems are commonly used on commercial construction sites to install large panes with precision and minimal risk. The adoption of vacuum lifters in modular construction and prefabrication yards is also rising as contractors seek safer, more efficient alternatives to traditional rigging, further driving growth in this segment.

Regional Insights

North America Vacuum Lifter Market Trends

North America is emerging as the fastest-growing region in the vacuum lifter market, fueled by the rapid adoption of automation technologies, increasing investments in smart factories, and a strong focus on workplace safety and ergonomics. The U.S. leads regional demand, supported by a robust manufacturing and logistics sector that is incorporating advanced vacuum lifting systems into production, assembly, and warehousing operations. For instance, Wood’s Powr-Grip 3000 Series vacuum lifters are commonly used in automotive and metal fabrication plants to safely lift heavy steel plates and components. The integration of ergonomic lifters with existing material-handling systems boosts productivity while reducing worker fatigue.

The region is also seeing a widespread adoption of IoT-enabled and electro-pneumatic vacuum lifters, which offer enhanced efficiency, minimized downtime, and predictive maintenance capabilities. The rise of e-commerce and logistics infrastructure is driving the need for versatile, safe lifting solutions to support high-volume operations in distribution centers and fulfillment hubs. Increasing demand for precision handling in industries such as electronics and aerospace is further driving equipment upgrades and custom solutions. The use of Caldwell vacuum tube lifters in warehousing and heavy machinery assembly highlights how scalable and adaptable vacuum lifting technologies are meeting a wide range of industrial needs across North America.

Europe Vacuum Lifter Equipment Market Trends

Europe is experiencing a steady growth in the vacuum lifter market, driven by advancements in manufacturing, automation, and construction. Countries, including Germany, Italy, and the U.K., lead in adoption, backed by strong industrial foundations and a commitment to workplace safety and energy-efficient lifting solutions. Strict EU regulations on safety and ergonomics are fueling demand for automated vacuum lifters that offer enhanced control and precision. Increased awareness of operator safety and the need to reduce musculoskeletal injuries are pushing companies to replace manual handling with mechanized solutions, contributing to market growth.

The region's growth is further supported by ongoing investments in smart manufacturing and robotics, particularly in the automotive, aerospace, and glass-handling sectors. European companies are increasingly adopting electro-pneumatic and custom-designed vacuum lifters to improve production efficiency and reduce risks associated with manual labor. For example, Bystronic Glass vacuum lifting systems are widely used in large-scale glass fabrication and construction projects, showcasing Europe’s focus on technological innovation, safety compliance, and operational efficiency.

Asia Pacific Vacuum Lifter Equipment Market Trends

Asia Pacific leads the vacuum lifter market, accounting for over 35% of the market in 2025, driven by rapid industrialization, infrastructure development, and the growth of manufacturing sectors in China and India. The region’s dominance in automotive, electronics, and construction industries creates strong demand for advanced lifting solutions that improve productivity and safety. Timmer vacuum lifting systems, known for their reliability and flexibility, are increasingly adopted in Southeast Asia’s glass and steel manufacturing plants. The rise of smart warehouses and automated production facilities has further accelerated the use of vacuum lifters, reducing manual labor and boosting throughput.

The market expansion is further supported by increasing automation, favorable manufacturing costs, and government-driven industrial initiatives. Both local and global companies are investing in capacity expansions and product customization to meet the diverse needs of the region, solidifying Asia Pacific's position as a key growth driver in the global vacuum lifter industry. Gis vacuum lifting solutions, for instance, are widely used in precision electronics assembly and modular production lines, reflecting the region's shift toward automated and high-precision material handling. Governments in China and India are also promoting industrial upgrades and safety programs, offering additional incentives to adopt vacuum lifters.

Competitive Landscape

The global vacuum lifter market exhibits a moderately fragmented structure, driven by the presence of both established international manufacturers and a growing number of regional and specialized producers. Continuous industrial expansion, rising automation adoption, and increasing emphasis on ergonomic material handling have lowered barriers to entry, enabling mid-sized companies to compete alongside larger corporations. With key leaders including J. Schmalz, Anver, Wood’s Powr-Grip, Caldwell, and Timmer, the competitive landscape reflects strong brand recognition backed by extensive distribution networks and after-sales support.

These players compete through continuous R&D investment, product diversification, regional expansion, and strategic partnerships with system integrators and industrial automation providers. Manufacturers also focus on enhancing service quality, offering training programs and maintenance packages to improve customer retention. Cost-competitive and tailored solutions from regional vendors are challenging legacy players, particularly in emerging markets, where demand for affordable yet reliable vacuum lifters is rising.

Key Industry Developments:

- In 2025, GRABO launched the HIGH FLOW electric vacuum lifter, designed to handle extremely porous and heavy materials with enhanced vacuum technology. Featuring a smart foam seal, ergonomic T-handle, and a new pistol-grip design, the HIGH FLOW delivers precise, effortless lifting of challenging surfaces such as dry cast pavers and patio bricks. Its high vacuum flow rate ensures secure handling, setting a new benchmark for portable industrial lifting solutions.

- In January 2025, Schmalz unveiled the redesigned JumboFlex vacuum tube lifter, enhancing ergonomics, efficiency, and usability. The new control handle adapts to all hand sizes, while dual operating buttons allow precise up-and-down movement and floating load positioning. Optimized for handling workpieces up to 50 kg, the updated JumboFlex reduces training time, minimizes worker fatigue, and enables faster, more accurate operations in high-cycle industrial environments.

Companies Covered in Vacuum Lifter Market

- Aardwolf

- Anver

- Bystronic Glass

- J. Schmalz

- WoodS Powr-Grip

- Acimex

- Fezer

- Barbaric

- Biesse

- Carl Stahl

- Elephant

- Fukoku

- Gis

- Ingersoll-Rand

- Kilner Vacuumation

- Natsu Machine

- Ox Worldwide

Frequently Asked Questions

The global vacuum lifter market is valued at US$1.6 billion in 2025 and expected to reach US$2.5 billion by 2032, reflecting robust growth.

Key drivers include increasing automation and workplace safety regulations, expanding manufacturing and construction activities, and advances in vacuum lifting technology.

Electro-pneumatic vacuum lifters lead with 40% share, driven by superior control, safety, and efficiency in automated manufacturing and construction.

Asia Pacific dominates, capturing over 35%, driven by rapid industrialization and infrastructure growth.

Opportunities exist in emerging markets, the development of custom vacuum lifters, and integration with IoT and Industry 4.0 technologies.